|

市场调查报告书

商品编码

1404472

汽车缸套 - 2024年至2029年市场占有率分析、产业趋势与统计、成长预测Automotive Cylinder Liner - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

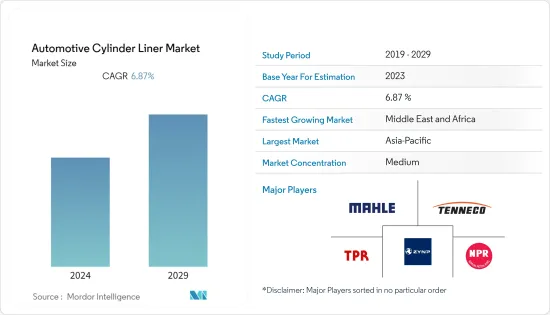

汽车缸套市场规模为50.5亿美元,预计净收入将超过70.4亿美元,预测期内复合年增长率为6.87%。

主要亮点

- 商用车销量的增加和汽车持有的增加是全球汽车市场成长的关键决定因素,这对汽车缸套的需求有正面影响。商用车成长主要受到电子商务扩张和商用运输车辆增加的影响。此外,工业化和基础设施的不断发展,支撑着汽车工业的进步和开拓,也支撑着商用车市场的成长。根据国际汽车製造商工业预测,2022年全球新型商用车销售量将达2,410万辆。

- 此外,重点地区对氢电动商用车的需求不断增长,促使缸套製造商开发先进技术。几家主要企业正在推出用于氢电动卡车的缸套技术,这推动了市场需求的激增。此外,车辆报废计划以及有关车辆长度和负载容量限制的严格监管标准也可能有助于推动市场需求。

- 由于印度和中国汽车工业的潜力不断上升,亚太地区预计将成为主导汽车缸套消费市场的最大地区。此外,美国等美国各国从中国、日本等经济体采购原料和引擎零件,并将其组装在完整的引擎室中。随着汽车销售和汽车产量的增加,该地区对汽缸套的需求预计将保持在高水准。

汽车缸套市场趋势

小客车市场将在预测期内获得牵引力

- 小客车是新兴国家最常见的交通途径。随着人均收入的增加,新兴国家的小客车数量也在增加,这些因素预计将对汽车缸套持有产生正面影响。印度等新兴国家正在寻找更好的小客车燃料,例如乙醇,这将对市场成长产生正面影响。

- 例如,2023 年 8 月,Toyota Innova 成为世界上第一辆仅使用乙醇运作的弹性燃料汽车。丰田汽车将成为世界上第一家推出 100% 乙醇汽车的汽车製造商。 2023 年 8 月,印度联邦部长推出了一款基于丰田最受欢迎的小客车Innova 打造的汽车。 Innova 成为世界上第一款由具有灵活燃油电动证书的 Bharat VI 期车辆提供动力的车型。一年前,这家日本主要汽车製造商发布了由氢燃料电池驱动的 Mirai。

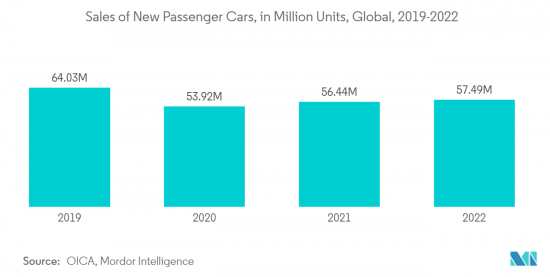

- 由于排放法规收紧、电动车的普及以及内燃机(ICE)汽车对环境的有害影响而导致石化燃料燃料蕴藏量短缺,可能会对市场成长构成挑战。然而,新兴国家需要电动车的基础设施发展,充电设施很可能在预测期内推动内燃机市场的扩张。根据国际汽车工业协会(OICA)的数据,2022年全球新小客车销量达到5,740万辆,较2021与前一年同期比较增1.9%。在南非、泰国等国家,2022年新小客车销售量与前一年同期比较成长19.5%及10.0%。

- 此外,预计都市化的提高和消费者对使用私人交通途径的偏好的转变预计将推动全球汽车行业的发展,进而推动对先进汽车缸套市场的需求。根据世界银行预测,2022年印度都市化将达36%,而2018年为34%。随着越来越多的消费者迁移到新兴市场的都市区,个人交通将成为首选,导致全球汽车缸套市场的成长。

预测期内亚太地区将占据最大的市场占有率

- 由于中国和印度汽车产业的扩张,亚太汽车缸套市场的缸套产品销售量不断成长。两国都在促进汽车销售,创造了对引擎的大量需求。

- 印度是主要的汽车出口国之一,从目前的流动性扩张计划来看,预计很快就会出现强劲的出口成长。此外,印度政府对汽车产业的大力支持以及主要汽车製造商在印度市场的存在,帮助印度发展成为主要的汽车出口国之一。 2000年4月至2022年9月,汽车产业累计接受直接投资约337.7亿美元。印度政府预计到 2024 年将汽车产业规模扩大一倍,达到 180 亿美元。此外,中国在汽车工业产量和引擎产量方面在亚太地区占据主导地位。

- 2022年中国汽车销量为2,680万辆,较2021年的2,627万辆与前一年同期比较增2.2%。主要发动机製造商和目标商标产品製造商 (OEM) 正在增加对该地区的投资、扩张和发展。这在长期预测期内抑制了对汽缸套的需求。

- 例如,2022年3月,哈尔滨东安汽车发动机公布了2022年投资计划,建造高效增程发动机生产线,包括加工中心、打标机、拧紧机、黏合机等设备。此外,该计划将由哈尔滨东安汽车发动机子公司哈尔滨东安汽车发动机製造有限公司共同维护,总投资为7233万元人民币(1085万美元)。

- 因此,随着亚太地区小客车和商用车产业的扩张,汽车缸套市场的需求预计在未来几年将迅速扩大。然而,政府将重点转向电动车的普及可能会严重阻碍因素亚太地区的长期产品成长。然而,在短期内,向汽车电动的竞争转变对这些政府构成了重大挑战。因此,在预测期内,汽车缸套产品的需求仍然强劲。

汽车缸套产业概况

汽车气缸套市场呈现出适度的分散程度,有组织和参与企业共同参与企业了产业形势。缸套市场的主要竞争包括 Mahle GmBH、Tenneco Inc.、TPR、Nippon Piston Ring 和 ZYNP。重要製造商正在大力投资汽车缸套研发,以提高盈利和产品效率。

为了降低与原材料采购相关的风险,公司正在采取积极主动的方法并扩大与主要原材料供应商的关係。这项策略成功地确保了气缸套生产所需原材料的稳定和持续供应。

2022年10月,莱茵金属与华域汽车系统的合资企业莱茵金属股份公司铸造部门赢得了为英国知名跑车製造商供应V8引擎缸体的重要订单。尤其是V8引擎拥有令人印象深刻的接近四位数的马力。

2022年4月,丰田北美公司宣布拟投资3.83亿美元在美国兴建四家工厂。该投资旨在准备一款混合和传统动力传动系统生产的新型四缸引擎。引擎生产范围包括端到端组装,包括引擎缸盖、缸套和各种其他零件。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月分析师支持

目录

第一章简介

- 调查先决条件

- 调查范围

第二章调查方法

第三章执行摘要

第四章市场动态

- 市场驱动因素

- 商用车销售量增加

- 其他的

- 市场抑制因素

- 电动车的快速普及

- 其他的

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 买家/消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争公司之间敌对关係的强度

第五章市场区隔(市场规模-美元)

- 依材料类型

- 铸铁

- 不銹钢

- 铝

- 钛

- 按燃料

- 汽油

- 柴油引擎

- 透过联繫

- 湿式缸套

- 干式汽缸套

- 按车型

- 小客车

- 轻型商用车

- 中型/大型商用车

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 欧洲其他地区

- 亚太地区

- 印度

- 中国

- 日本

- 韩国

- 其他亚太地区

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他中东/非洲

- 北美洲

第六章竞争形势

- 供应商市场占有率

- 公司简介

- Mahle GmbH

- Tenneco Inc.

- GKN Zhongyuan Cylinder Liner Company Limited

- Melling Cylinder Sleeves

- TPR Co. Ltd

- Westwood Cylinder Liners Ltd

- Darton International Inc.

- ZYNP International Corporation

- Laystall Engineering Co. Ltd

- India Pistons Ltd

- Nippon Piston Ring Co. Ltd

- Motordetal

- Kusalava International

- Cooper Corp.

- Yoosung Enterprise Co. Ltd

- Yangzhou Wutingqiao Cylinder Liner Co. Ltd

- Chengdu Galaxy Power Co. Ltd

第七章 市场机会及未来趋势

- 混合衬里的采用增加

The automotive cylinder liner market is valued at USD 5.05 billion and is anticipated to surpass a net valuation of USD 7.04 billion, registering a CAGR of 6.87% over the forecast period.

Key Highlights

- Rising sales of commercial vehicles and increasing vehicle parc globally serve as major determinants for the growth of the automotive market across the world, which, in turn, is positively impacting the demand for the automotive cylinder liner. Commercial vehicle growth is primarily influenced by the expansion of e-commerce and the increasing use of commercial vehicles for transportation. Aside from that, rising industrialization and infrastructure development, which support advancement and development in the automotive industry, drive market growth for commercial vehicles. According to the International Organization of Motor Vehicle Manufacturers, global new commercial vehicle sales touched 24.1 million units in 2022.

- Further, rising demand for hydrogen electric commercial vehicles across major regions is pushing cylinder liner manufacturers to develop advanced technology. Several key players are introducing cylinder liner technology for hydrogen-electric trucks, which in turn is likely to enhance the surging demand in the market. Furthermore, vehicle scrappage programs and stringent regulatory norms for vehicle length and loading limits, among other parameters, will contribute to driving the demand of the market.

- Asia-Pacific is the largest region that is expected to dominate the consumption of automotive cylinder liners market, owing to the increased potential of the automotive industry in India and China. Moreover, various countries across the globe, such as the United States, source raw materials and engine components from China, Japan, and other economies to assemble them under the complete engine chamber. With rising automotive sales and auto production, the region's demand for cylinder liners is expected to remain high.

Automotive Cylinder Liner Market Trends

Passenger Car Segment of the Market to Gain Traction during the forecast period

- Passenger cars are the most common form of transport in emerging countries. As per capita income increases, the number of passenger cars is also increasing in developing countries, and such factors are likely to positively impact the automotive cylinder liner market. Emerging countries such as India are looking for better fuel for their passenger cars, such as ethanol, which will positively impact the market growth.

- For instance, in August 2023, Toyota Innova became the world's first flexible fuel vehicle that can run entirely on ethanol. Toyota Motor will become the first automaker in the world to introduce cars powered by 100% ethanol. India Union Minister launched a vehicle based on Toyota's most popular passenger car, the Innova, in August 2023. Innova became the first model in the world to feature a Bharat Phase VI vehicle with a flexible fuel electric certificate. The launch comes a year after the Japanese auto giant introduced the Mirai, which uses hydrogen fuel cells as fuel.

- Increasing emissions regulations, penetration of electric vehicles, and lack of fossil fuel reserves due to the toxic impact of internal combustion engine (ICE) vehicles on the environment could challenge the growth of the market. However, in emerging countries, there needs to be more infrastructure for electric vehicles, and charging facilities could facilitate the expansion of the internal combustion engine market during the forecast period. According to the International Organization of Motor Vehicle Manufacturers (OICA), global new passenger car sales touched 57.4 million in 2022, recording a Y-o-Y growth of 1.9% compared to 2021. Countries such as South Africa and Thailand have witnessed 19.5% and 10.0% Y-o-Y growth in their new passenger car sales in 2022 compared to the previous year.

- Further, the rising urbanization rate and consumers shifting preference towards availing of private transportation medium is anticipated to drive the automotive industry around the globe, which in turn is expected to drive the demand for advanced automotive cylinder liner market. According to the World Bank, the urbanization rate in India stood at 36% in 2022, compared to 34% in 2018. As more consumers migrate to urban areas in developing nations, there will exist a preference for personal mobility, which in turn will lead to the growth of the automotive cylinder liner market across the world.

Asia-Pacific to Hold Largest Market Share During Forecast Period

- The Asia-Pacific automotive cylinder liner market is witnessing elevated sales of cylinder liner products owing to the expanding auto sector of China and India. Both countries are fuelling vehicle sales, generating a significant amount of engine demand.

- India is one of the major automobile exporters, and strong export growth is expected shortly, seeing its present mobility expansion projects. Furthermore, favorable initiatives by the government of India to support the automotive industry and the presence of major automakers in the Indian market are assisting in developing India as one of the major automobile exporters. The automotive sector received a cumulative FDI inflow of approximately USD 33.77 billion between April 2000 and September 2022. The government of India expects to double the automotive sector size to USD 18 billion by 2024. Further, China holds the dominating hand in the Asia-Pacific region regarding auto industry throughput and engine production.

- In 2022, the total number of vehicles sold in China stood up at 26.8 million units as compared to 26.27 million units in 2021, registering a year-on-year growth of 2.2%. The region is witnessing extended investment, expansion, and development proliferated by key engine manufacturers and original equipment manufacturers (OEMs). This has mitigated demand for cylinder liners over the longer-term forecast period.

- For instance, in March 2022, Harbin Dongan Auto Engine Co. Ltd. unveiled its investment plan for 2022 for building a production line for high-efficiency extended-range engines, which will involve the machining center, marking machines, tightening machines, gluing machines, and other equipment. Further, the project will be jointly maintained by Harbin Dongan Automotive Engine Manufacturing Co. Ltd, the subsidiary of Harbin Dongan Auto Engine, with a total investment of CNY 72.33 million (USD 10.85 million).

- Therefore, with the expanding passenger car and commercial vehicle industry of the Asia-Pacific region, the demand for the automotive cylinder liner market will showcase a rapid surge in the coming years. However, shifting the government's focus to promote the adoption of electric vehicles might potentially act as a major deterrent to the growth of these products in the long run in the Asia-Pacific region. However, a competitive shift towards electrification of vehicle fleets in the short run is a major challenge for these governments. Therefore, the demand for automotive cylinder liner products remains strong during the forecast period.

Automotive Cylinder Liner Industry Overview

The automotive cylinder liner market exhibits a moderate level of fragmentation, with a mix of organized and unorganized players shaping the industry landscape. Among the key contenders in the cylinder liner market, notable players include Mahle GmBH, Tenneco Inc., TPR Co. Ltd., Nippon Piston Ring Co. Ltd., and ZYNP, among others. Significant manufacturers are channeling substantial investments into the research and development of automotive cylinder liners with the aim of enhancing profitability and product efficiency.

To mitigate the risks associated with raw material procurement, companies have adopted a proactive approach, maintaining extended relationships with their primary raw material suppliers. This strategy has proven successful in ensuring a consistent and uninterrupted supply of materials necessary for cylinder liner production.

In October 2022, Rheinmetall AG's Castings business unit, a joint venture between Rheinmetall and HUAYU Automotive Systems Co. Ltd., secured a significant order to supply a V8 engine block to a renowned English sports car manufacturer. Notably, the V8 engines boast an impressive horsepower output, approaching four figures.

In April 2022, Toyota Motor North America disclosed its intention to invest USD 383 million in four U.S.-based plants. This investment is aimed at preparing for the production of a new four-cylinder engine variant tailored for both hybrid and conventional powertrains. The scope of engine production encompasses end-to-end assembly, encompassing engine heads, liners, and various other components.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rising Sales of Commercial Vehicles

- 4.1.2 Others

- 4.2 Market Restraints

- 4.2.1 Rapid Adoption of Electric Vehicles

- 4.2.2 Others

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Material Type

- 5.1.1 Cast Iron

- 5.1.2 Stainless Steel

- 5.1.3 Aluminum

- 5.1.4 Titanium

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.3 By Contact

- 5.3.1 Wet Cylinder Liner

- 5.3.2 Dry Cylinder Liner

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commerical Vehicles

- 5.4.3 Medium and Heavy-Duty Commercial Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Latin America

- 5.5.4.1 Mexico

- 5.5.4.2 Brazil

- 5.5.4.3 Argentina

- 5.5.4.4 Rest of Latin America

- 5.5.5 Middle East & Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Mahle GmbH

- 6.2.2 Tenneco Inc.

- 6.2.3 GKN Zhongyuan Cylinder Liner Company Limited

- 6.2.4 Melling Cylinder Sleeves

- 6.2.5 TPR Co. Ltd

- 6.2.6 Westwood Cylinder Liners Ltd

- 6.2.7 Darton International Inc.

- 6.2.8 ZYNP International Corporation

- 6.2.9 Laystall Engineering Co. Ltd

- 6.2.10 India Pistons Ltd

- 6.2.11 Nippon Piston Ring Co. Ltd

- 6.2.12 Motordetal

- 6.2.13 Kusalava International

- 6.2.14 Cooper Corp.

- 6.2.15 Yoosung Enterprise Co. Ltd

- 6.2.16 Yangzhou Wutingqiao Cylinder Liner Co. Ltd

- 6.2.17 Chengdu Galaxy Power Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Adoption of Hybrid Liners