|

市场调查报告书

商品编码

1850138

赌场管理系统:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Casino Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

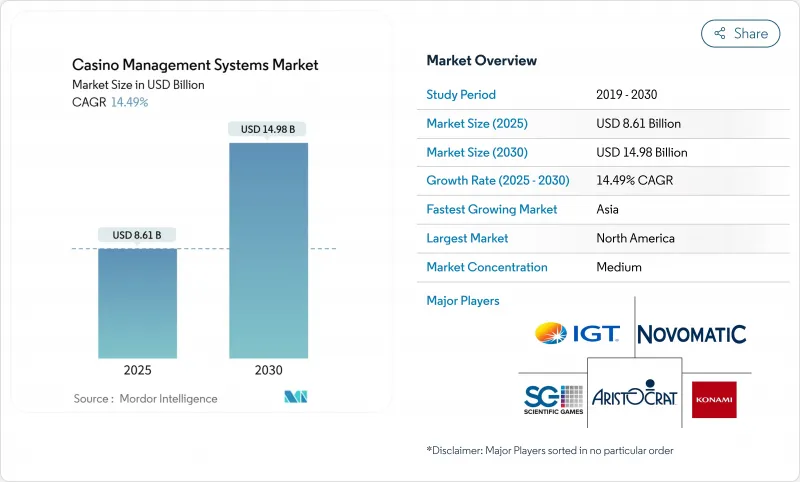

预计 2024 年赌场管理系统市场价值将达到 75.7 亿美元,到 2030 年预计将达到 169.4 亿美元,2025 年至 2030 年的复合年增长率为 14.49%。

随着营运商从交易监控转向数据主导的决策、预测分析和无现金运营,需求加速成长。亚太地区综合度假村的扩张、美国体育博彩的成长以及洗钱防制法规是关键的成长动力,而持续的劳动力短缺和网路攻击风险正在抑製成长势头。云端运算的采用正在改变部落和小型场所的成本结构,使它们无需高昂的资本支出即可获得企业级功能。同时,随着供应商竞相将人工智慧融入玩家追踪、安全和行销工作流程,以分析为中心的模组正在重塑竞争定位。

全球赌场管理系统市场趋势与洞察

亚洲各地综合度假村建设进展迅速

亚洲综合度假村的快速建设,以及旨在将博彩、酒店和零售业务整合到单一资料层的新项目,正在加速对端到端赌场管理系统的需求。 2024年7月,银河娱乐推出了一款智慧赌桌,可将即时投注数据传输到分析引擎,这充分展现了这些新度假村必须管理的数据规模。新濠博亚娱乐将类似的技术与永续性仪表板结合,将能源使用与宾客行为联繫起来,突显了其现代化平台如何在收益优化与环境目标之间取得平衡。此外,随着业务扩展到菲律宾、日本和阿联酋,多物业营运商正在寻求跨司法管辖区的合规工具。这些需求推动了更高价值的合约签订,这些合约捆绑了会计、玩家追踪、酒店和零售模组。拥有预先整合区域合规库的供应商将获得先发优势,预计将推动该地区赌场管理系统市场持续实现两位数成长。

强制性无现金/TITO法规

澳洲2024年的改革强制要求使用银行卡并设定1000澳元现金限额,这迫使昆士兰州所有机构升级其支付、追踪和反洗钱能力。内华达州逐步推动无现金支付,反映了监管和消费者压力不断汇聚的趋势。 Everi和Crane Payment Innovations等供应商正在推出可改装到现有基础设施中的钱包整合服务,因此无需彻底维修即可逐步采用。合规期限缩小了决策窗口,推动了赌场管理系统市场的短期支出激增。长期的银行卡交易历史为忠诚度和负责任博彩演算法提供了丰富的数据集,加强了对分析的策略重点。

备受瞩目的网路攻击

2024年,米高梅度假村和凯撒娱乐遭遇网路攻击,数百万客户记录被洩露,促使整个行业重新评估安全通讯协定。由于董事会要求更高的渗透测试门槛,勒索软体保险费的上涨和法律责任风险正在推迟采购决策。虽然供应商目前正在整合脸部辨识和行为分析技术来即时识别诈欺活动,但更严格的存取控制策略可能会使使用者工作流程更加复杂。由于销售週期延长和安全成本的上升超过了内容管理系统(CMS)的升级,整体影响可能是短期成长的下行压力。

細項分析

到 2024 年,软体将占据赌场管理系统市场的 70%,这反映了其在会计、玩家追踪和法规遵循方面的作用。大型营运商青睐功能丰富的套件,例如 IGT ADVANTAGE,它捆绑了核心笼、老虎机和行销模组。美国和澳洲的监管审核要求每日汇出会计数据,这强调了软体的重要性。然而,随着机构寻求客製化整合、分析调整和全天候託管支持,服务收入成长更快,复合年增长率达到 18.7%。脸部认证、无现金钱包和体育博彩数据馈送的加入增加了系统复杂性,推动了对专业服务的需求。包括服务在内的赌场管理系统市场预计将从 2024 年的 22.7 亿美元扩大到 2030 年的 63.6 亿美元。

嵌入供应商生态系统的顾问公司如今会指导场馆进行分阶段部署,以最大程度地减少停机时间。一个值得注意的例子是 eConnect 和 Table Trac 在德克萨斯州州一家美洲原住民赌场的联合部署,该整合服务将脸部辨识与即时赌区资料结合。随着 CMS 平台逐渐演变为战略情报中心而非后勤部门实用程序,定期服务合约为供应商提供了稳定的年金收入,并加剧了认证实施合作伙伴之间的竞争。

到2024年,本地部署系统的份额将达到82%,因为许多监管机构仍然要求游戏资料在本地存储,并在网路中断期间保持持续可用性。高可用性丛集和专用光纤链路有助于降低停机风险,但资本和人事费用仍然很高。目前,云端采用率仅18%,但随着供应商加强加密、提供区域资料中心并获得监管部门的核准,其复合年增长率将达到22.4%。受云端采用推动的赌场管理系统市场规模预计到2030年将达到48.8亿美元。

部落和小型商业场所正在蓬勃发展,因为它们无需搭建昂贵的伺服器机房即可获得企业级功能。 IGT 声称,其补充云层可在五年内将总拥有成本降低 30%,其弹性处理能力可在离峰时段降低能源成本。新泽西州和昆士兰州的监管机构已发布指导意见,承认在交易日誌不可篡改的情况下,云端技术是可接受的选择。随着安全认证的广泛应用,中端区域营运商正开始转型,这标誌着整个赌场管理系统市场部署组合的转捩点。

赌场管理系统市场细分:按组件(软体、服务)、按部署类型(本地部署、云端基础)、按用途(会计与监控、保全与监控、酒店与度假村管理、分析与报告、其他)、按最终用户(中小型赌场、大型赌场)以及按地区。市场预测以货币单位(美元)提供。

区域分析

2024年,北美将贡献38%的赌场管理系统市场收益。美国体育博彩的扩张将推动支出成长,而加拿大安大略省市场的需求也将增加。部落赌场将采用云端平台来弥补IT方面的差距,并整合脸部认证以确保安全。 2025年1月,伊利诺州、田纳西州和新泽西州将推出23项新法规,迫使业者升级其报告和自我隔离介面。由于云端技术应用的加速和跨通路忠诚度的提升,区域成长率将超过全球平均。

亚太地区是成长最快的地区,复合年增长率达18.1%。澳门和菲律宾的智慧赌桌能够捕捉到精细的博彩数据,而澳洲的「了解你的客户」规则正在加速无现金支付的普及。日本首个综合度假村的落成以及印度潜在的监管改革,可能在2020年下半年释放巨大的需求潜力。儘管澳门面临资金限制,但亚太其他地区正在建造配备人工智慧基础设施的待开发区度假村,这将推动亚太赌场管理系统市场规模到2030年突破40亿美元。

欧洲市场正受到严格的反洗钱指令和负责任博彩标准的塑造。欧盟第六号指令已触发能够侦测实际所有权风险的分析模组的升级。英国引入了新的技术标准,限制自动播放并加快旋转速率披露,强制内容合规性更新。拉丁美洲是一个新兴的热点。巴西将于2025年1月1日开始对iGaming进行监管,预计将推动供应商在地化,以适应葡萄牙语介面和当地税收要求。中东和非洲仍在发展中,但受到阿联酋和沙乌地阿拉伯旅游主导计划的支持,一旦立法允许,这些计画可能会采用度假村规模的CMS套件。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 亚洲各地综合度假村的快速建造推动了CMS的采用

- 澳洲和内华达州强制实施无现金/TITO 法规

- 美国体育博彩合法化促使忠诚度系统升级

- Tribal Casino 实施云端基础的CMS 来填补 IT 短缺

- 欧盟第六项反洗钱指令加速了分析模组的需求

- 矿井作业劳动力短缺推动自动化模组的采用

- 市场限制

- 备受瞩目的网路攻击增加了企业责任

- 澳门特许经营经营资本支出冻结导致CMS新契约延期

- GDPR 等严格的资料隐私规则限制了玩家追踪的深度

- 由于网路和手机游戏,实体店客流量下降

- 监理展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 投资分析

第五章市场规模与成长预测(价值)

- 按组件

- 软体

- 服务

- 依部署方式

- 本地部署

- 云端基础

- 依目的

- 会计和笼子管理

- 安全与监控

- 酒店和度假村管理

- 分析和报告

- 玩家追踪和忠诚度

- 媒体管理与数位电子看板

- 行销与推广

- 按最终用户

- 中小型赌场

- 大型赌场

- 按地区

- 北美洲

- 美国

- 加拿大

- 南美洲

- 巴西

- 阿根廷

- 墨西哥

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 其他亚太地区

- 中东和非洲

- 中东

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲国家

- 北美洲

第六章 竞争态势

- Strategic Developments

- Vendor Positioning Analysis

- 公司简介

- International Game Technology PLC

- Aristocrat Leisure Ltd.

- Novomatic AG

- Scientific Games Corp.(Light & Wonder)

- Konami Gaming Inc.

- Bally Technologies Inc.

- Winsystems Inc.

- TCS John Huxley

- Agilysys Inc.

- Oracle Hospitality

- Everi Holdings Inc.

- Table Trac Inc.

- DJOY Group Ltd.

- Amatic Industries GmbH

- Bluberi Gaming Technologies Inc.

- Apex Gaming Technology

- Decart Ltd.

- TransAct Technologies Inc.

- Genesis Gaming Solutions Inc.

- Syswin Solutions

- CasinoTrac

- Tangam Systems Inc.

- Axes.ai

- Advansys doo

- BetConstruct

- CT Gaming

- QUONTRA Solutions

第七章 市场机会与未来展望

The casino management system market is valued at USD 7.57 billion in 2024 and is forecast to reach USD 16.94 billion by 2030, advancing at a 14.49% CAGR from 2025 to 2030.

Demand accelerates as operators move from transactional oversight toward data-driven decision making, predictive analytics, and cashless operations. Asia-Pacific integrated-resort expansion, expanding U.S. sports wagering, and stricter anti-money-laundering rules are key growth catalysts, while persistent labor shortages and cyber-breach risks temper momentum. Cloud deployment is transforming cost structures for tribal and small properties, allowing them to access enterprise-grade capabilities without high capital outlays. Meanwhile, analytics-centric modules are reshaping competitive positioning as vendors race to embed artificial intelligence into player tracking, security, and marketing workflows.

Global Casino Management Systems Market Trends and Insights

Rapid Integrated-Resort Builds Across Asia

Asia's pipeline of integrated resorts is accelerating demand for end-to-end casino management systems as new properties aim to unify gaming, hospitality, and retail operations under a single data layer. July 2024 saw Galaxy Entertainment deploy smart tables that stream real-time wagering data to analytics engines, showcasing the scale of data that new venues must manage. Melco Resorts has paired similar technology with sustainability dashboards that tie energy use to guest behaviour, highlighting how modern platforms now balance revenue optimisation with environmental targets. Multi-property operators also seek cross-jurisdiction compliance tools as expansions reach the Philippines, Japan, and the United Arab Emirates. These requirements are propelling higher-value contracts that bundle accounting, player-tracking, hotel, and retail modules. Vendors able to pre-integrate regional compliance libraries are gaining early-mover advantage, positioning the casino management system market for sustained double-digit growth in the region.

Mandatory Cashless / TITO Regulations

Australia's 2024 reforms mandate carded play and sub-AUD 1,000 cash limits, forcing every property in Queensland to upgrade payment, tracking, and AML capabilities. Nevada's gradual push toward cashless floors mirrors this trajectory, converging regulatory and consumer pressure. Vendors such as Everi and Crane Payment Innovations respond with wallet integrations that retrofit into existing infrastructures, allowing gradual adoption without full rip-and-replace projects. Compliance deadlines compress decision windows, driving near-term spending spikes within the casino management system market. Long-term, card-based transaction histories supply richer datasets for loyalty and responsible-gaming algorithms, reinforcing the strategic pivot toward analytics.

High-Profile Cyber-breaches

The 2024 attacks on MGM Resorts and Caesars exposed millions of patron records, prompting industry-wide reassessment of security protocols. Rising ransomware premiums and liability risks delay procurement decisions as boards demand higher penetration-test thresholds. Vendors now integrate facial recognition and behavioural analytics to identify fraud in real time, but tighter access control policies can complicate user workflows. The overall effect is longer sales cycles and incremental security spend that can crowd out broader CMS upgrades, applying downward pressure on near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- U.S. Sports-Betting Legalisation

- Cloud-based CMS Adoption by Tribal Casinos

- Macau Concession CapEx Freeze

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 70% of the casino management system market in 2024, reflecting its role in accounting, player tracking, and regulatory compliance. Large operators favour feature-rich suites such as IGT ADVANTAGE that bundle core cage, slot, and marketing modules. Regulatory audits in the United States and Australia require daily accounting exports, reinforcing software's criticality. However, services revenue is rising faster, growing at an 18.7% CAGR as properties seek custom integrations, analytics tuning, and 24x7 managed support. System complexity has increased with the addition of facial recognition, cashless wallets, and sports-book data feeds, boosting demand for professional services. The casino management system market size linked to services is projected to expand from USD 2.27 billion in 2024 to USD 6.36 billion in 2030.

Consulting firms embedded within vendor ecosystems now guide properties through staged deployments that minimise downtime. A notable example is the joint implementation by eConnect and Table Trac at a Native American casino in Texas, where integration services united facial recognition with real-time pit data. As CMS platforms evolve into strategic intelligence hubs rather than back-office utilities, recurring service contracts give vendors stable annuity streams, intensifying competition for certified implementation partners.

On-premise systems commanded an 82% share in 2024 because many regulators still require local storage of wagering data and continuous availability during network outages. High-availability clusters and dedicated fiber links help mitigate downtime risk, yet capital and staffing costs remain high. Cloud deployments, while only 18% today, are scaling at 22.4% CAGR as vendors strengthen encryption, offer region-specific data centres, and secure regulatory approvals. The casino management system market size attached to cloud installations is expected to reach USD 4.88 billion by 2030.

Tribal and small commercial properties drive momentum because they gain enterprise-grade functionality without building costly server rooms. IGT pitches a 30% total cost of ownership reduction over five years for its supplemental cloud layer, citing elastic processing that lowers energy costs during off-peak periods. Regulators in New Jersey and Queensland have issued guidance that recognises cloud as an acceptable option when transactional logs remain immutable. As security certifications proliferate, mid-tier regional operators are beginning phased migrations, signalling a tipping point in the deployment mix across the casino management system market.

Casino Management Systems Market Segmented by Component (Software, Services), Deployment Mode (On-Premise, Cloud-Based), Purpose (Accounting and Cage Operations, Security and Surveillance, Hotel and Resort Management, Analytics and Reporting, and More), End-User (Small and Medium Casinos, Large Casinos), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38% of the casino management system market revenue in 2024. The United States drives spend with expanding sports betting, while Canada's Ontario market adds incremental demand. Tribal casinos deploy cloud platforms to mitigate IT gaps and integrate facial recognition for security, exemplified by the Texas installation linking CasinoTrac data with eConnect biometrics. Compliance calendars remain active; January 2025 imposes 23 new mandates across Illinois, Tennessee, and New Jersey, pushing operators to upgrade reporting and self-exclusion interfaces. Accelerated cloud adoption and cross-channel loyalty upgrades keep regional growth above the global average.

Asia-Pacific is the fastest-growing territory, posting an 18.1% CAGR. Smart tables in Macau and the Philippines capture granular wagering data, while Australia's identity-verification rules accelerate cashless adoption. Japan's first integrated resort and India's potential regulatory reforms could unlock significant latent demand later in the decade. Despite capital constraints in Macau, properties elsewhere in the region are building greenfield resorts with AI-ready infrastructure, helping the casino management system market size in Asia-Pacific surpass USD 4 billion by 2030.

Europe's market is shaped by stringent AML directives and responsible-gaming standards. The EU 6th directive has triggered upgrades to analytics modules capable of detecting beneficial-ownership risks. The UK introduced new technical standards that limit autoplay and speed up spin-rate disclosures, forcing content compliance updates. Latin America is an emerging hotspot; Brazil began regulated iGaming on January 1 2025 and is expected to drive vendor localisation efforts for Portuguese interfaces and local tax requirements. The Middle East and Africa remain nascent but are underpinned by tourism-led projects in the UAE and Saudi Arabia that could adopt resort-scale CMS suites once legislation permits.

- International Game Technology PLC

- Aristocrat Leisure Ltd.

- Novomatic AG

- Scientific Games Corp. (Light & Wonder)

- Konami Gaming Inc.

- Bally Technologies Inc.

- Winsystems Inc.

- TCS John Huxley

- Agilysys Inc.

- Oracle Hospitality

- Everi Holdings Inc.

- Table Trac Inc.

- DJOY Group Ltd.

- Amatic Industries GmbH

- Bluberi Gaming Technologies Inc.

- Apex Gaming Technology

- Decart Ltd.

- TransAct Technologies Inc.

- Genesis Gaming Solutions Inc.

- Syswin Solutions

- CasinoTrac

- Tangam Systems Inc.

- Axes.ai

- Advansys d.o.o.

- BetConstruct

- CT Gaming

- QUONTRA Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Integrated-Resort Builds Across Asia Driving CMS Roll-outs

- 4.2.2 Mandatory Cashless/TITO Regulations in Australia & Nevada

- 4.2.3 U.S. Sports-Betting Legalisation Fuelling Loyalty-System Upgrades

- 4.2.4 Cloud-based CMS Adoption by Tribal Casinos to Offset IT Shortfalls

- 4.2.5 EU 6th AML Directive Accelerating Analytics-Module Demand

- 4.2.6 Labour Shortage in Pit Operations Prompting Automation Modules

- 4.3 Market Restraints

- 4.3.1 High-Profile Cyber-breaches Increasing Operator Liability

- 4.3.2 Macau Concession CapEx Freeze Delaying New CMS Contracts

- 4.3.3 Stricter GDPR-style Data-Privacy Rules Curb Player-Tracking Depth

- 4.3.4 Land-based Footfall Erosion from Online & Mobile Gaming

- 4.4 Regulatory Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.3 By Purpose

- 5.3.1 Accounting and Cage Operations

- 5.3.2 Security and Surveillance

- 5.3.3 Hotel and Resort Management

- 5.3.4 Analytics and Reporting

- 5.3.5 Player Tracking and Loyalty

- 5.3.6 Media Management and Digital Signage

- 5.3.7 Marketing and Promotions

- 5.4 By End Users

- 5.4.1 Small and Medium Casinos

- 5.4.2 Large Casinos

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Mexico

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 New Zealand

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 International Game Technology PLC

- 6.3.2 Aristocrat Leisure Ltd.

- 6.3.3 Novomatic AG

- 6.3.4 Scientific Games Corp. (Light & Wonder)

- 6.3.5 Konami Gaming Inc.

- 6.3.6 Bally Technologies Inc.

- 6.3.7 Winsystems Inc.

- 6.3.8 TCS John Huxley

- 6.3.9 Agilysys Inc.

- 6.3.10 Oracle Hospitality

- 6.3.11 Everi Holdings Inc.

- 6.3.12 Table Trac Inc.

- 6.3.13 DJOY Group Ltd.

- 6.3.14 Amatic Industries GmbH

- 6.3.15 Bluberi Gaming Technologies Inc.

- 6.3.16 Apex Gaming Technology

- 6.3.17 Decart Ltd.

- 6.3.18 TransAct Technologies Inc.

- 6.3.19 Genesis Gaming Solutions Inc.

- 6.3.20 Syswin Solutions

- 6.3.21 CasinoTrac

- 6.3.22 Tangam Systems Inc.

- 6.3.23 Axes.ai

- 6.3.24 Advansys d.o.o.

- 6.3.25 BetConstruct

- 6.3.26 CT Gaming

- 6.3.27 QUONTRA Solutions

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

赌场管理系统市场(按组件、安全系统、支付系统、最终用户和应用划分)—2025-2032 年全球预测

赌场管理系统市场(按组件、安全系统、支付系统、最终用户和应用划分)—2025-2032 年全球预测 日本赌场管理系统市场报告(按组件、应用、最终用户和地区)2025 年至 2033 年

日本赌场管理系统市场报告(按组件、应用、最终用户和地区)2025 年至 2033 年 2026 年至 2032 年赌场管理系统市场(按模组、应用和地区划分)2025 年至 2033 年赌场管理系统市场报告(按组件、应用、最终用户和地区)

2026 年至 2032 年赌场管理系统市场(按模组、应用和地区划分)2025 年至 2033 年赌场管理系统市场报告(按组件、应用、最终用户和地区) 欧洲赌场管理:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

欧洲赌场管理:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 赌场管理系统市场规模、份额、趋势分析报告:按应用程式、地区、细分市场、预测,2025 年至 2030 年

赌场管理系统市场规模、份额、趋势分析报告:按应用程式、地区、细分市场、预测,2025 年至 2030 年 赌场管理系统市场规模、份额、成长分析,按组件、按应用、按最终用户、按地区 - 行业预测,2024-2031 年

赌场管理系统市场规模、份额、成长分析,按组件、按应用、按最终用户、按地区 - 行业预测,2024-2031 年 赌场管理系统的全球市场规模、占有率和行业趋势分析报告:2023-2030 年按组件、最终用户、应用程式和地区分類的展望和预测

赌场管理系统的全球市场规模、占有率和行业趋势分析报告:2023-2030 年按组件、最终用户、应用程式和地区分類的展望和预测