|

市场调查报告书

商品编码

1298311

3D 石墨烯市场:按应用(复合材料、传感器、储能等):2021-2031 年全球机会分析和行业预测3D Graphene Market By Application (Composites, Sensors, Energy storage, Others): Global Opportunity Analysis and Industry Forecast, 2021-2031 |

||||||

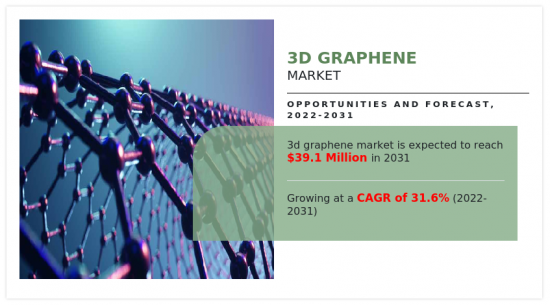

2021年全球3D石墨烯市场价值为250万美元,预计2022年至2031年復合年增长率为31.6%,到2031年达到3910万美元。

基于3D石墨烯的架构直接用于超级电容器。 由于 3D 互连结构和石墨烯优异的电子导电性的结合,3D 石墨烯结构有望用作超级电容器电极。 3D石墨烯材料有时被称为石墨烯气凝胶和使用石墨烯墨水製成的3D打印石墨烯纳米结构。 石墨烯是一层六边形排列的碳原子的单原子层。 堆迭多层石墨烯会产生石墨,石墨通常被用作铅笔的“核心”。

然而,由于石墨烯片的密集堆迭,石墨的机械性能相对较弱。 为了克服这个问题,石墨烯片可以通过充满空气的孔分离,以形成石墨烯的多孔版本,称为石墨烯气凝胶。 这使得可以形成三维结构,同时保持石墨烯独特的性能。 3D石墨烯由于其高表面积和吸附能力等特性,也被用作化学工业中的有效催化剂。 全球化学品需求的激增预计将增加对3D石墨烯的需求,并推动全球3D石墨烯行业的增长。

3D石墨烯广泛应用于核电站。 核电站在生产冷却反应堆所需的重水时会排放多达一百万吨二氧化碳。 曼彻斯特大学的研究人员表示,3D石墨烯膜可用于使重水更具成本效益且环保。 与现有技术相比,3D 石墨烯有可能将核电站重水生产和净化相关的能源成本降低 100 倍或更多。 3D石墨烯的特殊性质可以实现基本粒子的有效分离,使该方法有效且经济。

由于静电和疏水相互作用可以同时发生以及较大的比表面积,3D石墨烯在水污染物的吸附方面显示出光明的前景。 3D石墨烯用于净化水并去除细菌和其他杂质。 近年来,基于3D石墨烯的宏观结构(3D GBM)因其在水处理行业的巨大潜力而引起了越来越多的兴趣。 3D GBM将大表面积和物理互连的多孔网络等独特的结构特性与高导电性、良好的化学和热稳定性、超轻量和高太阳能热转换效率等其他特性结合在一起,其优异的性能使其成为一种有吸引力的材料通过吸附、电容去离子和太阳能热蒸馏进行水净化。 此外,3D GBM可用作封装粉末状纳米材料和製造整体吸附剂和光电催化剂的框架,因此在水处理中的潜在应用数量很多。

3D 石墨烯市场按应用和地区细分。 按用途可分为储能、传感器、催化剂等。 按地区划分,我们分析了北美、欧洲、亚太地区和拉美地区。 3D石墨烯市场的领先公司有ACS Material、American Elements、CVD Equipment Corporation、G6 Materials Corp.、Graphex Group、Integrated Graphene Ltd.、Lyten, Inc.、Nano Dimension、NANOCHEMAZONE、Ultrananotech Private Limited. is。

COVID-19 对全球 3D 石墨烯市场的影响

在 COVID-19 大流行期间,汽车销量下降导致主要汽车製造商推迟了对电动汽车的最终投资决定。 因此,由于石墨烯用于电池、复合材料等,其需求量有所下降。 3D石墨烯广泛应用于电子、汽车等领域。 这些行业正在蓬勃发展并成功启动生产过程。 因此,自新冠疫情以来,对 3D 石墨烯的需求有所增加。

内容

第一章简介

第 2 章执行摘要

第三章市场概述

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资领域

- 波特五力分析

- 供应商的议价能力

- 买家的议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争强度

- 市场动态

- 协调员

- 电子领域的有利用途

- 太阳能使用激增

- 各种最终用途行业的高需求

- 阻碍因素

- 3D石墨烯的製造成本较高

- 机会

- 3D石墨烯在医疗领域的应用不断增加

- 技术进步突飞猛进

- 协调员

- COVID-19 对市场的影响分析

- 主要监管分析

- 专利情况

- 价值链分析

第 4 章 3D 石墨烯市场:按应用划分

- 概述

- 市场规模和预测

- 复合材料

- 主要市场趋势、增长因素和增长机会

- 市场规模和预测:按地区划分

- 市场份额分析:按国家/地区划分

- 传感器

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按地区划分

- 市场份额分析:按国家/地区划分

- 能源储存

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按地区划分

- 市场份额分析:按国家/地区划分

- 其他

- 主要市场趋势、增长因素和机遇

- 市场规模和预测:按地区划分

- 市场份额分析:按国家/地区划分

第 5 章 3D 石墨烯市场:按地区

- 概述

- 市场规模和预测:按地区划分

- 北美

- 主要趋势和机遇

- 市场规模和预测:按应用分类

- 市场规模/预测:按国家/地区划分

- 美国

- 主要市场趋势、增长因素和机遇

- 市场规模和预测:按应用分类

- 加拿大

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 墨西哥

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 欧洲

- 主要趋势和机遇

- 市场规模和预测:按应用分类

- 市场规模/预测:按国家/地区划分

- 德国

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 英国

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 法国

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 意大利

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 西班牙

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 欧洲其他地区

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 亚太地区

- 主要趋势和机遇

- 市场规模和预测:按应用分类

- 市场规模/预测:按国家/地区划分

- 中国

- 主要市场趋势、增长因素、增长机会

- 市场规模和预测:按应用分类

- 印度

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 韩国

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 日本

- 主要市场趋势、增长因素、增长机会

- 市场规模和预测:按应用分类

- 澳大利亚

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 亚太地区其他地区

- 主要市场趋势、增长因素和机遇

- 市场规模和预测:按应用分类

- 拉丁美洲/中东/非洲

- 主要趋势和机遇

- 市场规模和预测:按应用分类

- 市场规模/预测:按国家/地区划分

- 巴西

- 主要市场趋势、增长因素、增长机会

- 市场规模和预测:按应用分类

- 沙特阿拉伯

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 南非

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

- 其他地区

- 主要市场趋势、增长动力和机遇

- 市场规模和预测:按应用分类

第 6 章竞争格局

- 简介

- 关键成功策略

- 10家主要公司的产品图谱

- 竞赛仪表板

- 比赛热图

- 2021 年关键人物定位

第7章公司简介

- AMERICAN ELEMENTS

- Integrated Graphene Ltd.

- ACS Material

- NANOCHEMAZONE

- Ultrananotech Private Limited.

- CVD Equipment Corporation

- Lyten, Inc.

- Graphex Group

- Nano Dimension

- G6 Materials Corp.

The global 3D graphene market was valued at $2.5 million in 2021, and is projected to reach $39.1 million by 2031, growing at a CAGR of 31.6% from 2022 to 2031.

3D graphene-based architectures are directly used in supercapacitors. 3D graphene architectures are promising for use as electrodes in supercapacitors due to the combination of the 3D interconnection structure and the excellent electron conductivity of graphene. 3D graphene material can be referred to as a graphene aerogel or a 3D-printed graphene nanostructure that is created using graphene inks. Graphene is a one-atom-thick layer of carbon atoms arranged in a hexagonal pattern. When multiple layers of graphene are stacked on top of each other, the resulting material is known as graphite, which is commonly used as the "lead" in pencils.

However, the mechanical properties of graphite are relatively weak due to the close stacking of the graphene sheets. To overcome this, a porous version of graphene, known as a graphene aerogel, can be created by separating the graphene sheets with air-filled pores. This allows the three-dimensional structure to retain the unique properties of graphene. In addition, 3D graphene is used in the chemical industry as an effective catalyst because of its properties such as high surface area and adsorption power. The surge in demand for chemicals worldwide is expected to increase 3D graphene demand and thus, drive the growth of the global 3D graphene industry.

3D graphene is used extensively in nuclear power plants. A million tons of CO2 are emitted during the production of the heavy water needed in nuclear power plants to cool the reactors, which is also expensive to generate. A more cost-effective and environment-friendly way to create heavy water is by using 3D graphene membranes, according to researchers at the University of Manchester. As comparison to present technology, 3D graphene could help lower the energy costs associated with producing heavy water and decontamination in nuclear power plants by more than 100 times. The potential to effectively separate sub-atomic particles due to the special characteristics of 3D graphene makes this method effective and economical.

The simultaneous electrostatic and hydrophobic interactions that can be produced, along with the large specific surface area, indicate that 3D graphene has a bright future in the absorption of water pollutants. It is used in water purification and removing germs and other impurities. In recent times, 3D graphene-based macrostructures (3D GBMs) have attracted more interest because of their enormous potential for use in the water treatment industry. 3D GBMs are fascinating materials for water purification through adsorption, capacitive deionization, and solar distillation because of their distinctive structural characteristics such as large surface area and physically interconnected porous network and excellent qualities like high electrical conductivity, good chemical/thermal stability, ultra lightness, and high solar-to-thermal conversion efficiency. Moreover, 3D GBMs have a much greater number of potential uses in water treatment since they may be used as frameworks to encapsulate powder nanomaterials and create monolithic adsorbents and photo-/electrocatalysts.

The 3D graphene market is segmented into application and region. By application, the market is divided into energy storage, sensors, catalysis, and others. Region-wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA. The key players operating in the 3D graphene market are ACS Material, American Elements, CVD Equipment Corporation, G6 Materials Corp., Graphex Group, Integrated Graphene Ltd., Lyten, Inc., Nano Dimension, NANOCHEMAZONE and Ultrananotech Private Limited.

IMPACT OF COVID-19 ON THE GLOBAL 3D GRAPHENE MARKET

During the COVID-19 pandemic, the final investment decision for electric vehicles is getting delayed by the key automotive players, owing to decreased automotive sales. This has resulted in decrease in demand for graphene as graphene is used in batteries, composites, and others. 3D graphene is widely used in electronic, automotive, and other sectors. These industries have gained momentum and started their production process smoothly. Hence, the demand for 3D graphene has increased post COVID.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the 3d graphene market analysis from 2021 to 2031 to identify the prevailing 3d graphene market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the 3d graphene market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global 3d graphene market trends, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Application

- Composites

- Sensors

- Energy storage

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- South Korea

- Japan

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- AMERICAN ELEMENTS

- Integrated Graphene Ltd.

- ACS Material

- Ultrananotech Private Limited.

- Nano Dimension

- Graphex Group

- Lyten, Inc.

- NANOCHEMAZONE

- CVD Equipment Corporation

- G6 Materials Corp.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Bargaining power of suppliers

- 3.3.2. Bargaining power of buyers

- 3.3.3. Threat of substitutes

- 3.3.4. Threat of new entrants

- 3.3.5. Intensity of rivalry

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Lucrative use from electronics sector

- 3.4.1.2. Surge in solar energy usage

- 3.4.1.3. High demand from various end-use industries

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. High production cost of 3D graphene

- 3.4.3. Opportunities

- 3.4.3.1. Rise in use of 3D graphene in the medical sector

- 3.4.3.2. Surge in technological advancements

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Key Regulation Analysis

- 3.7. Patent Landscape

- 3.8. Value Chain Analysis

CHAPTER 4: 3D GRAPHENE MARKET, BY APPLICATION

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Composites

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Sensors

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Energy storage

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Others

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

CHAPTER 5: 3D GRAPHENE MARKET, BY REGION

- 5.1. Overview

- 5.1.1. Market size and forecast By Region

- 5.2. North America

- 5.2.1. Key trends and opportunities

- 5.2.2. Market size and forecast, by Application

- 5.2.3. Market size and forecast, by country

- 5.2.3.1. U.S.

- 5.2.3.1.1. Key market trends, growth factors and opportunities

- 5.2.3.1.2. Market size and forecast, by Application

- 5.2.3.2. Canada

- 5.2.3.2.1. Key market trends, growth factors and opportunities

- 5.2.3.2.2. Market size and forecast, by Application

- 5.2.3.3. Mexico

- 5.2.3.3.1. Key market trends, growth factors and opportunities

- 5.2.3.3.2. Market size and forecast, by Application

- 5.3. Europe

- 5.3.1. Key trends and opportunities

- 5.3.2. Market size and forecast, by Application

- 5.3.3. Market size and forecast, by country

- 5.3.3.1. Germany

- 5.3.3.1.1. Key market trends, growth factors and opportunities

- 5.3.3.1.2. Market size and forecast, by Application

- 5.3.3.2. UK

- 5.3.3.2.1. Key market trends, growth factors and opportunities

- 5.3.3.2.2. Market size and forecast, by Application

- 5.3.3.3. France

- 5.3.3.3.1. Key market trends, growth factors and opportunities

- 5.3.3.3.2. Market size and forecast, by Application

- 5.3.3.4. Italy

- 5.3.3.4.1. Key market trends, growth factors and opportunities

- 5.3.3.4.2. Market size and forecast, by Application

- 5.3.3.5. Spain

- 5.3.3.5.1. Key market trends, growth factors and opportunities

- 5.3.3.5.2. Market size and forecast, by Application

- 5.3.3.6. Rest of Europe

- 5.3.3.6.1. Key market trends, growth factors and opportunities

- 5.3.3.6.2. Market size and forecast, by Application

- 5.4. Asia-Pacific

- 5.4.1. Key trends and opportunities

- 5.4.2. Market size and forecast, by Application

- 5.4.3. Market size and forecast, by country

- 5.4.3.1. China

- 5.4.3.1.1. Key market trends, growth factors and opportunities

- 5.4.3.1.2. Market size and forecast, by Application

- 5.4.3.2. India

- 5.4.3.2.1. Key market trends, growth factors and opportunities

- 5.4.3.2.2. Market size and forecast, by Application

- 5.4.3.3. South Korea

- 5.4.3.3.1. Key market trends, growth factors and opportunities

- 5.4.3.3.2. Market size and forecast, by Application

- 5.4.3.4. Japan

- 5.4.3.4.1. Key market trends, growth factors and opportunities

- 5.4.3.4.2. Market size and forecast, by Application

- 5.4.3.5. Australia

- 5.4.3.5.1. Key market trends, growth factors and opportunities

- 5.4.3.5.2. Market size and forecast, by Application

- 5.4.3.6. Rest of Asia-Pacific

- 5.4.3.6.1. Key market trends, growth factors and opportunities

- 5.4.3.6.2. Market size and forecast, by Application

- 5.5. LAMEA

- 5.5.1. Key trends and opportunities

- 5.5.2. Market size and forecast, by Application

- 5.5.3. Market size and forecast, by country

- 5.5.3.1. Brazil

- 5.5.3.1.1. Key market trends, growth factors and opportunities

- 5.5.3.1.2. Market size and forecast, by Application

- 5.5.3.2. Saudi Arabia

- 5.5.3.2.1. Key market trends, growth factors and opportunities

- 5.5.3.2.2. Market size and forecast, by Application

- 5.5.3.3. South Africa

- 5.5.3.3.1. Key market trends, growth factors and opportunities

- 5.5.3.3.2. Market size and forecast, by Application

- 5.5.3.4. Rest of LAMEA

- 5.5.3.4.1. Key market trends, growth factors and opportunities

- 5.5.3.4.2. Market size and forecast, by Application

CHAPTER 6: COMPETITIVE LANDSCAPE

- 6.1. Introduction

- 6.2. Top winning strategies

- 6.3. Product Mapping of Top 10 Player

- 6.4. Competitive Dashboard

- 6.5. Competitive Heatmap

- 6.6. Top player positioning, 2021

CHAPTER 7: COMPANY PROFILES

- 7.1. AMERICAN ELEMENTS

- 7.1.1. Company overview

- 7.1.2. Key Executives

- 7.1.3. Company snapshot

- 7.1.4. Operating business segments

- 7.1.5. Product portfolio

- 7.2. Integrated Graphene Ltd.

- 7.2.1. Company overview

- 7.2.2. Key Executives

- 7.2.3. Company snapshot

- 7.2.4. Operating business segments

- 7.2.5. Product portfolio

- 7.2.6. Key strategic moves and developments

- 7.3. ACS Material

- 7.3.1. Company overview

- 7.3.2. Key Executives

- 7.3.3. Company snapshot

- 7.3.4. Operating business segments

- 7.3.5. Product portfolio

- 7.4. NANOCHEMAZONE

- 7.4.1. Company overview

- 7.4.2. Key Executives

- 7.4.3. Company snapshot

- 7.4.4. Operating business segments

- 7.4.5. Product portfolio

- 7.5. Ultrananotech Private Limited.

- 7.5.1. Company overview

- 7.5.2. Key Executives

- 7.5.3. Company snapshot

- 7.5.4. Operating business segments

- 7.5.5. Product portfolio

- 7.6. CVD Equipment Corporation

- 7.6.1. Company overview

- 7.6.2. Key Executives

- 7.6.3. Company snapshot

- 7.6.4. Operating business segments

- 7.6.5. Product portfolio

- 7.6.6. Business performance

- 7.7. Lyten, Inc.

- 7.7.1. Company overview

- 7.7.2. Key Executives

- 7.7.3. Company snapshot

- 7.7.4. Operating business segments

- 7.7.5. Product portfolio

- 7.7.6. Key strategic moves and developments

- 7.8. Graphex Group

- 7.8.1. Company overview

- 7.8.2. Key Executives

- 7.8.3. Company snapshot

- 7.8.4. Operating business segments

- 7.8.5. Product portfolio

- 7.8.6. Business performance

- 7.9. Nano Dimension

- 7.9.1. Company overview

- 7.9.2. Key Executives

- 7.9.3. Company snapshot

- 7.9.4. Operating business segments

- 7.9.5. Product portfolio

- 7.9.6. Business performance

- 7.10. G6 Materials Corp.

- 7.10.1. Company overview

- 7.10.2. Key Executives

- 7.10.3. Company snapshot

- 7.10.4. Operating business segments

- 7.10.5. Product portfolio

- 7.10.6. Business performance

LIST OF TABLES

- TABLE 01. GLOBAL 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 02. 3D GRAPHENE MARKET FOR COMPOSITES, BY REGION, 2021-2031 ($THOUSAND)

- TABLE 03. 3D GRAPHENE MARKET FOR SENSORS, BY REGION, 2021-2031 ($THOUSAND)

- TABLE 04. 3D GRAPHENE MARKET FOR ENERGY STORAGE, BY REGION, 2021-2031 ($THOUSAND)

- TABLE 05. 3D GRAPHENE MARKET FOR OTHERS, BY REGION, 2021-2031 ($THOUSAND)

- TABLE 06. 3D GRAPHENE MARKET, BY REGION, 2021-2031 ($THOUSAND)

- TABLE 07. NORTH AMERICA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 08. NORTH AMERICA 3D GRAPHENE MARKET, BY COUNTRY, 2021-2031 ($THOUSAND)

- TABLE 09. U.S. 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 10. CANADA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 11. MEXICO 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 12. EUROPE 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 13. EUROPE 3D GRAPHENE MARKET, BY COUNTRY, 2021-2031 ($THOUSAND)

- TABLE 14. GERMANY 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 15. UK 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 16. FRANCE 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 17. ITALY 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 18. SPAIN 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 19. REST OF EUROPE 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 20. ASIA-PACIFIC 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 21. ASIA-PACIFIC 3D GRAPHENE MARKET, BY COUNTRY, 2021-2031 ($THOUSAND)

- TABLE 22. CHINA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 23. INDIA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 24. SOUTH KOREA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 25. JAPAN 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 26. AUSTRALIA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 27. REST OF ASIA-PACIFIC 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 28. LAMEA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 29. LAMEA 3D GRAPHENE MARKET, BY COUNTRY, 2021-2031 ($THOUSAND)

- TABLE 30. BRAZIL 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 31. SAUDI ARABIA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 32. SOUTH AFRICA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 33. REST OF LAMEA 3D GRAPHENE MARKET, BY APPLICATION, 2021-2031 ($THOUSAND)

- TABLE 34. AMERICAN ELEMENTS: KEY EXECUTIVES

- TABLE 35. AMERICAN ELEMENTS: COMPANY SNAPSHOT

- TABLE 36. AMERICAN ELEMENTS: PRODUCT SEGMENTS

- TABLE 37. AMERICAN ELEMENTS: PRODUCT PORTFOLIO

- TABLE 38. INTEGRATED GRAPHENE LTD.: KEY EXECUTIVES

- TABLE 39. INTEGRATED GRAPHENE LTD.: COMPANY SNAPSHOT

- TABLE 40. INTEGRATED GRAPHENE LTD.: PRODUCT SEGMENTS

- TABLE 41. INTEGRATED GRAPHENE LTD.: PRODUCT PORTFOLIO

- TABLE 42. INTEGRATED GRAPHENE LTD.: KEY STRATERGIES

- TABLE 43. ACS MATERIAL: KEY EXECUTIVES

- TABLE 44. ACS MATERIAL: COMPANY SNAPSHOT

- TABLE 45. ACS MATERIAL: PRODUCT SEGMENTS

- TABLE 46. ACS MATERIAL: PRODUCT PORTFOLIO

- TABLE 47. NANOCHEMAZONE: KEY EXECUTIVES

- TABLE 48. NANOCHEMAZONE: COMPANY SNAPSHOT

- TABLE 49. NANOCHEMAZONE: PRODUCT SEGMENTS

- TABLE 50. NANOCHEMAZONE: PRODUCT PORTFOLIO

- TABLE 51. ULTRANANOTECH PRIVATE LIMITED.: KEY EXECUTIVES

- TABLE 52. ULTRANANOTECH PRIVATE LIMITED.: COMPANY SNAPSHOT

- TABLE 53. ULTRANANOTECH PRIVATE LIMITED.: PRODUCT SEGMENTS

- TABLE 54. ULTRANANOTECH PRIVATE LIMITED.: PRODUCT PORTFOLIO

- TABLE 55. CVD EQUIPMENT CORPORATION: KEY EXECUTIVES

- TABLE 56. CVD EQUIPMENT CORPORATION: COMPANY SNAPSHOT

- TABLE 57. CVD EQUIPMENT CORPORATION: PRODUCT SEGMENTS

- TABLE 58. CVD EQUIPMENT CORPORATION: PRODUCT PORTFOLIO

- TABLE 59. LYTEN, INC.: KEY EXECUTIVES

- TABLE 60. LYTEN, INC.: COMPANY SNAPSHOT

- TABLE 61. LYTEN, INC.: PRODUCT SEGMENTS

- TABLE 62. LYTEN, INC.: PRODUCT PORTFOLIO

- TABLE 63. LYTEN, INC.: KEY STRATERGIES

- TABLE 64. GRAPHEX GROUP: KEY EXECUTIVES

- TABLE 65. GRAPHEX GROUP: COMPANY SNAPSHOT

- TABLE 66. GRAPHEX GROUP: PRODUCT SEGMENTS

- TABLE 67. GRAPHEX GROUP: PRODUCT PORTFOLIO

- TABLE 68. NANO DIMENSION: KEY EXECUTIVES

- TABLE 69. NANO DIMENSION: COMPANY SNAPSHOT

- TABLE 70. NANO DIMENSION: PRODUCT SEGMENTS

- TABLE 71. NANO DIMENSION: PRODUCT PORTFOLIO

- TABLE 72. G6 MATERIALS CORP.: KEY EXECUTIVES

- TABLE 73. G6 MATERIALS CORP.: COMPANY SNAPSHOT

- TABLE 74. G6 MATERIALS CORP.: PRODUCT SEGMENTS

- TABLE 75. G6 MATERIALS CORP.: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. 3D GRAPHENE MARKET, 2021-2031

- FIGURE 02. SEGMENTATION OF 3D GRAPHENE MARKET, 2021-2031

- FIGURE 03. TOP INVESTMENT POCKETS IN 3D GRAPHENE MARKET (2022-2031)

- FIGURE 04. LOW BARGAINING POWER OF SUPPLIERS

- FIGURE 05. LOW BARGAINING POWER OF BUYERS

- FIGURE 06. LOW THREAT OF SUBSTITUTES

- FIGURE 07. LOW THREAT OF NEW ENTRANTS

- FIGURE 08. LOW INTENSITY OF RIVALRY

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBAL3D GRAPHENE MARKET

- FIGURE 10. IMPACT OF KEY REGULATION: 3D GRAPHENE MARKET

- FIGURE 11. PATENT ANALYSIS BY COMPANY

- FIGURE 12. PATENT ANALYSIS BY COUNTRY

- FIGURE 13. VALUE CHAIN ANALYSIS: 3D GRAPHENE MARKET

- FIGURE 14. 3D GRAPHENE MARKET, BY APPLICATION, 2021(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF 3D GRAPHENE MARKET FOR COMPOSITES, BY COUNTRY 2021 AND 2031(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF 3D GRAPHENE MARKET FOR SENSORS, BY COUNTRY 2021 AND 2031(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF 3D GRAPHENE MARKET FOR ENERGY STORAGE, BY COUNTRY 2021 AND 2031(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF 3D GRAPHENE MARKET FOR OTHERS, BY COUNTRY 2021 AND 2031(%)

- FIGURE 19. 3D GRAPHENE MARKET BY REGION, 2021

- FIGURE 20. U.S. 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 21. CANADA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 22. MEXICO 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 23. GERMANY 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 24. UK 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 25. FRANCE 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 26. ITALY 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 27. SPAIN 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 28. REST OF EUROPE 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 29. CHINA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 30. INDIA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 31. SOUTH KOREA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 32. JAPAN 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 33. AUSTRALIA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 34. REST OF ASIA-PACIFIC 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 35. BRAZIL 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 36. SAUDI ARABIA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 37. SOUTH AFRICA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 38. REST OF LAMEA 3D GRAPHENE MARKET, 2021-2031 ($THOUSAND)

- FIGURE 39. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 40. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 41. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 42. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 43. COMPETITIVE DASHBOARD

- FIGURE 44. COMPETITIVE HEATMAP: 3D GRAPHENE MARKET

- FIGURE 45. TOP PLAYER POSITIONING, 2021

- FIGURE 46. CVD EQUIPMENT CORPORATION: NET REVENUE, 2019-2021 ($MILLION)

- FIGURE 47. CVD EQUIPMENT CORPORATION: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 48. GRAPHEX GROUP: NET REVENUE, 2019-2021 ($MILLION)

- FIGURE 49. GRAPHEX GROUP: REVENUE SHARE BY SEGMENT, 2021 (%)

- FIGURE 50. GRAPHEX GROUP: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 51. NANO DIMENSION: NET REVENUE, 2019-2021 ($MILLION)

- FIGURE 52. NANO DIMENSION: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 53. G6 MATERIALS CORP.: NET REVENUE, 2020-2022 ($MILLION)

2024-2032 年按类型(单层和双层石墨烯、少层石墨烯、氧化石墨烯、石墨烯奈米片等)、应用、最终用途行业和地区分類的石墨烯市场报告

2024-2032 年按类型(单层和双层石墨烯、少层石墨烯、氧化石墨烯、石墨烯奈米片等)、应用、最终用途行业和地区分類的石墨烯市场报告 MXene材料的全球市场:考察·预测 (~2030年)

MXene材料的全球市场:考察·预测 (~2030年) 欧洲二维材料市场:分析与预测(2022-2031)

欧洲二维材料市场:分析与预测(2022-2031) 石墨烯市场、份额、市场规模、趋势、行业分析报告:按产品、按最终用途、按地区、按细分市场、预测,2024-2032年

石墨烯市场、份额、市场规模、趋势、行业分析报告:按产品、按最终用途、按地区、按细分市场、预测,2024-2032年 2D 材料市场:按材料类型、最终用户划分 - 2024-2030 年全球预测

2D 材料市场:按材料类型、最终用户划分 - 2024-2030 年全球预测 石墨烯市场规模、份额和趋势分析报告:2024-2030 年按产品、应用、最终用途、地区和细分市场进行的预测

石墨烯市场规模、份额和趋势分析报告:2024-2030 年按产品、应用、最终用途、地区和细分市场进行的预测 亚太地区二维材料市场 - 分析与预测(2022-2031)

亚太地区二维材料市场 - 分析与预测(2022-2031) 全球石墨烯市场(2023)

全球石墨烯市场(2023) 石墨烯市场:按类型(石墨烯奈米片、氧化石墨烯)、用途(生物工程、复合材料、储能)- COVID-19、俄罗斯-乌克兰衝突、高通膨的累积影响- 2023-2030 年世界预测

石墨烯市场:按类型(石墨烯奈米片、氧化石墨烯)、用途(生物工程、复合材料、储能)- COVID-19、俄罗斯-乌克兰衝突、高通膨的累积影响- 2023-2030 年世界预测 全球二维材料市场 (2022-2031):按最终用户、材料类型和地区/国家分类的分析和预测

全球二维材料市场 (2022-2031):按最终用户、材料类型和地区/国家分类的分析和预测