|

市场调查报告书

商品编码

1298376

铝铸造市场:按工艺、最终用户划分:2023-2032 年全球机遇分析和行业预测Aluminum Casting Market By Process (Die casting, Sand Casting, Permanent Mold Casting), By End-user (Building and Construction, Industrial, Transportation, Others): Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

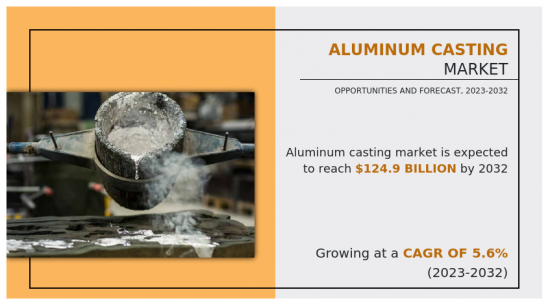

铝铸造市场预计2022年价值729亿美元,2032年达到1248亿美元,2023年至2032年復合年增长率为5.6%。

铝铸造是将熔融铝倒入模具中以製造 3D 金属零件的过程。该模具具有所需几何形状的空腔,可冷却熔融铝以形成凝固部件。铸铁、不銹钢、锰、铝等金属广泛应用于铝铸造工艺中。它们用于各种最终用途领域,包括汽车、电气/电子、建筑/施工、重型机械/设备和航空航天。

可支配收入的增加、技术升级以及原始设备製造商 (OEM) 数量的激增正在推动汽车和运输行业的显着增长。例如,根据ndia Brands Equity Foundation发布的报告,2016年至2020年,国内汽车产量将以2.36%的复合年增长率增长,2020年印度汽车产量将达到2636万辆。燃料製造的激增正在推动Maruti Suzuki和Hyundai等主要汽车製造商生产更轻的车辆以提高燃油效率。

铝铸件提供了延展性、成形性、应变硬化和强度水平参数等性能的良好组合和平衡。这些重要的特性可以减轻汽车的重量,同时提高其抗腐蚀能力。由于这些因素,铝铸件在汽车和运输领域的使用正在增加。因此,在预测期内,不断增长的汽车和运输行业对铝铸件的需求预计将增加。

此外,美国、中国、印度等发达经济体和新兴经济体已将重点放在生产具有现代化装甲装备的高科技飞机上,并已扩展到飞机活塞、轴承和其他飞机零部件的生产。用过的。这一因素可能是导致锰合金市场增长的主要驱动因素之一。此外,消费品需求的增加导致航运活动激增,从而导致货船製造激增,其中铝铸件被广泛用于生产轻质船舶部件。这可能会促进预测期内铝铸造市场的增长。

然而,铝铸造涉及多个步骤:熔化金属、将熔融金属转移至模具型腔以及凝固熔融金属。这些过程需要相对大量的热能。此外,整个过程由各种专为在高温应用中运行而製造的先进设备组成。这些因素使得铝铸造成为一种昂贵的工艺,这反过来可能会阻碍投资潜力较低的製造商进入铝铸造市场。因此,与铝铸件生产相关的高投资成本可能会阻碍预测期内的市场增长。

另一方面,技术的快速进步,加上人工智能(AI)、物联网(IOT)和机器学习(ML)技术的出现,正在推动各种消费电子产品的需求。铝铸造解决方案广泛应用于电子行业的三维零件生产。此外,主要电子製造商使用铝铸件的优点包括复合材料产量快、精度高,以及生产表面光滑的刚性铸件,不需要密集的二次加工。这些因素使得铝铸件在不断发展的电子行业中越来越受欢迎。除此之外,快速金属铸造工艺的出现为製造商提供了许多优势,例如尺寸精度高、生产能力提高和快速原型製作。这些因素正在推动电子产品製造商使用铝铸造工艺,创造利润丰厚的市场机会。

目录

第 1 章 简介

第二章执行摘要

第三章市场概况

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资口袋

- 波特五力分析

- 供应商的议价能力

- 买方议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争强度

- 市场动态

- 促进者

- 建筑业的需求不断增长

- 汽车行业需求旺盛

- 阻碍因素

- 投资成本高

- 机会

- 扩大电子领域的接受度

- 发达经济体和新兴经济体的快速工业化

- 促进者

- COVID-19 市场影响分析

- 关键监管分析

- 专利情况

- 价格分析

- 监管指南

- 价值链分析

4.按工艺划分的铝铸件市场

- 概述

- 市场规模及预测

- 压铸

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

- 砂模铸造

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

- 永久模铸造

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

5. 铝铸件市场,按最终用户划分

- 概述

- 市场规模及预测

- 建筑/施工

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

- 工业领域

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

- 航运

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

- 其他

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按地区

- 市场份额分析:按国家分类

6.按地区划分的铝铸件市场

- 概述

- 市场规模/预测:按地区

- 北美

- 主要趋势和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 市场规模/预测:按国家

- 美国

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 加拿大

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 墨西哥

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 欧洲

- 主要趋势和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 市场规模/预测:按国家

- 德国

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 英国

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 法国

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 西班牙

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 意大利

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 欧洲其他地区

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 亚太地区

- 主要趋势和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 市场规模/预测:按国家

- 中国

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 印度

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 日本

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 韩国

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 澳大利亚

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 亚太其他地区

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 拉丁美洲/中东/非洲

- 主要趋势和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 市场规模/预测:按国家

- 巴西

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 沙特阿拉伯

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 南非

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

- 其他地区

- 主要市场趋势、增长动力和机遇

- 市场规模/预测:按工艺分类

- 市场规模/预测:按最终用户分类

第7章 竞争格局

- 介绍

- 关键成功策略

- 10大公司产品图

- 比赛仪表板

- 比赛热图

- 2022 年顶级公司定位

第八章公司简介

- Alcoa Corporation

- RYOBI Aluminium Casting(UK)Ltd.

- Shandong Xinanrui Casting

- Rio Tinto

- RusAL

- Walbro

- Consolidated Metco, Inc.

- BUVO Castings

- Dynacast

- Bodine Aluminum

The aluminum casting market valued for $72.9 billion in 2022 and is estimated to reach $124.8 billion by 2032, exhibiting a CAGR of 5.6% from 2023 to 2032.

Aluminum casting is a process that involves pouring molten aluminum into a mold to create a 3D metal part. The mold contains a hollow cavity of a desired geometrical shape, and the molten aluminum is allowed to cool down to form a solidified part. Metals such as cast iron, stainless steel, manganese, aluminum, and others are widely used for aluminum casting process. It is employed in various end use sectors including automotive, electrical and electronics, building and construction, heavy machinery and equipment, aerospace, and others.

Factors such as increase in disposable income, technological upgrades, and spurring rise in number of original equipment manufacturers (OEMs) have led the automotive & transportation sector to witness a significant growth. For instance, according to a report published by India Brands Equity Foundation, the domestic automobile production increased by a CAGR of 2.36% from 2016-20 with 26.36 million vehicles being manufactured in India in 2020. The surge in fuel processing has led the key automotive manufacturers such as Maruti Suzuki and Hyundai others to produce lightweight vehicles to enhance fuel mileage.

Aluminum castings provide a favorable combination and balance of properties such as ductility, formability, strain hardening, and strength level parameters. These significant properties enable reducing the weight of vehicles and at the same time improves resistance against the effects of corrosion. This factor has led the automotive & transportation sectors to increasingly use aluminum castings. This is expected to fuel the demand for aluminum castings in the growing automotive & transportation sector during the forecast period.

Furthermore, both developed and developing economies, such as the U.S., China, India, and others have put more emphasis on producing high tech aircrafts equipped with modern armor facilities wherein sand castings are used for producing aircraft pistons, bearings, and other aircraft parts. This factor may act as one of the key drivers responsible for the growth of the manganese alloy market. Furthermore, the increase in demand for consumer goods surged the shipment activities which in turn has surged the manufacturing of cargo ships where aluminum casting is widely used for manufacturing lightweight ship components. This may augment the growth of the aluminum casting market during the forecast period.

However, aluminum casting involves several processes such as melting of metal, transferring the molten metal to mold cavity, and solidification of molten metal. These processes require a relatively large amount of heat energy. Furthermore, the overall process consists of different sophisticated equipment that are fabricated to work at high temperature application. These factors make aluminum casting an expensive process which in turn may restrain manufacturers with less investment potential to enter into aluminum casting market. Thus, high investment costs associated with the production of aluminum castings may hamper the market growth during the forecast period.

On the contrary, rapid technological advancements coupled with the emergence of artificial intelligence (AI), internet of things (IOT), and machine learning (ML) technologies have surged the demand for various consumer electronic devices. Aluminum casting solutions are widely used in electronics sector for producing three-dimensional parts. Furthermore, key electronic manufacturers are using aluminum casting owing to its advantages such as quick yield of complexes, preciseness, and production of rigid casts parts with smooth surfaces that don't need intense secondary machining. These factors have surged the popularity of aluminum castings in the growing electronics sector. In addition to this, the emergence of rapid metal casting process offers numerous advantages to the manufacturers such as high dimensional accuracy, increased production capacities, and rapid prototyping. These factors have made electronic products manufacturers become more linear toward using aluminum casting process; thus, creating lucrative opportunities for the market.

The aluminum casting market is segmented on the basis of process, end user, and region. On the basis of process, the market is categorized into die casting, sand casting, and permanent mold casting. As per end user, it is divided into transportation, industrial, building & construction, and others. Region-wise, the market is studied across North America, Europe, Asia-Pacific, and LAMEA.

The global aluminum casting market profiles leading players that include: Alcoa Corporation, Bodine Aluminum, BUVO Castings, Consolidated Metco, Inc., Dynacast, Rio Tinto, RusAL, RYOBI Aluminium Casting (UK) Ltd., Shandong Xinanrui Casting, and Walbro. The global aluminum casting market report provides in-depth competitive analysis as well as profiles of these major players.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the aluminum casting market analysis from 2022 to 2032 to identify the prevailing aluminum casting market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the aluminum casting market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global aluminum casting market trends, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Process

- Die casting

- Sand Casting

- Permanent Mold Casting

By End-user

- Industrial

- Transportation

- Others

- Building and Construction

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- Alcoa Corporation

- Bodine Aluminum

- BUVO Castings

- Consolidated Metco, Inc.

- Dynacast

- Rio Tinto

- RusAL

- RYOBI Aluminium Casting (UK) Ltd.

- Shandong Xinanrui Casting

- Walbro

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Bargaining power of suppliers

- 3.3.2. Bargaining power of buyers

- 3.3.3. Threat of substitutes

- 3.3.4. Threat of new entrants

- 3.3.5. Intensity of rivalry

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Escalating demand from building & construction sector

- 3.4.1.2. Robust demand from automotive sector

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. High investment costs

- 3.4.3. Opportunities

- 3.4.3.1. Increasing acceptance in electronics sector

- 3.4.3.2. Rapid industrialization in both developed and developing economies

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Key Regulation Analysis

- 3.7. Patent Landscape

- 3.8. Pricing Analysis

- 3.9. Regulatory Guidelines

- 3.10. Value Chain Analysis

CHAPTER 4: ALUMINUM CASTING MARKET, BY PROCESS

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Die casting

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Sand Casting

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Permanent Mold Casting

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

CHAPTER 5: ALUMINUM CASTING MARKET, BY END-USER

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Building and Construction

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Industrial

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Transportation

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Others

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

CHAPTER 6: ALUMINUM CASTING MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key trends and opportunities

- 6.2.2. Market size and forecast, by Process

- 6.2.3. Market size and forecast, by End-user

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Key market trends, growth factors and opportunities

- 6.2.4.1.2. Market size and forecast, by Process

- 6.2.4.1.3. Market size and forecast, by End-user

- 6.2.4.2. Canada

- 6.2.4.2.1. Key market trends, growth factors and opportunities

- 6.2.4.2.2. Market size and forecast, by Process

- 6.2.4.2.3. Market size and forecast, by End-user

- 6.2.4.3. Mexico

- 6.2.4.3.1. Key market trends, growth factors and opportunities

- 6.2.4.3.2. Market size and forecast, by Process

- 6.2.4.3.3. Market size and forecast, by End-user

- 6.3. Europe

- 6.3.1. Key trends and opportunities

- 6.3.2. Market size and forecast, by Process

- 6.3.3. Market size and forecast, by End-user

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. Germany

- 6.3.4.1.1. Key market trends, growth factors and opportunities

- 6.3.4.1.2. Market size and forecast, by Process

- 6.3.4.1.3. Market size and forecast, by End-user

- 6.3.4.2. UK

- 6.3.4.2.1. Key market trends, growth factors and opportunities

- 6.3.4.2.2. Market size and forecast, by Process

- 6.3.4.2.3. Market size and forecast, by End-user

- 6.3.4.3. France

- 6.3.4.3.1. Key market trends, growth factors and opportunities

- 6.3.4.3.2. Market size and forecast, by Process

- 6.3.4.3.3. Market size and forecast, by End-user

- 6.3.4.4. Spain

- 6.3.4.4.1. Key market trends, growth factors and opportunities

- 6.3.4.4.2. Market size and forecast, by Process

- 6.3.4.4.3. Market size and forecast, by End-user

- 6.3.4.5. Italy

- 6.3.4.5.1. Key market trends, growth factors and opportunities

- 6.3.4.5.2. Market size and forecast, by Process

- 6.3.4.5.3. Market size and forecast, by End-user

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Key market trends, growth factors and opportunities

- 6.3.4.6.2. Market size and forecast, by Process

- 6.3.4.6.3. Market size and forecast, by End-user

- 6.4. Asia-Pacific

- 6.4.1. Key trends and opportunities

- 6.4.2. Market size and forecast, by Process

- 6.4.3. Market size and forecast, by End-user

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Key market trends, growth factors and opportunities

- 6.4.4.1.2. Market size and forecast, by Process

- 6.4.4.1.3. Market size and forecast, by End-user

- 6.4.4.2. India

- 6.4.4.2.1. Key market trends, growth factors and opportunities

- 6.4.4.2.2. Market size and forecast, by Process

- 6.4.4.2.3. Market size and forecast, by End-user

- 6.4.4.3. Japan

- 6.4.4.3.1. Key market trends, growth factors and opportunities

- 6.4.4.3.2. Market size and forecast, by Process

- 6.4.4.3.3. Market size and forecast, by End-user

- 6.4.4.4. South Korea

- 6.4.4.4.1. Key market trends, growth factors and opportunities

- 6.4.4.4.2. Market size and forecast, by Process

- 6.4.4.4.3. Market size and forecast, by End-user

- 6.4.4.5. Australia

- 6.4.4.5.1. Key market trends, growth factors and opportunities

- 6.4.4.5.2. Market size and forecast, by Process

- 6.4.4.5.3. Market size and forecast, by End-user

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Key market trends, growth factors and opportunities

- 6.4.4.6.2. Market size and forecast, by Process

- 6.4.4.6.3. Market size and forecast, by End-user

- 6.5. LAMEA

- 6.5.1. Key trends and opportunities

- 6.5.2. Market size and forecast, by Process

- 6.5.3. Market size and forecast, by End-user

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Key market trends, growth factors and opportunities

- 6.5.4.1.2. Market size and forecast, by Process

- 6.5.4.1.3. Market size and forecast, by End-user

- 6.5.4.2. Saudi Arabia

- 6.5.4.2.1. Key market trends, growth factors and opportunities

- 6.5.4.2.2. Market size and forecast, by Process

- 6.5.4.2.3. Market size and forecast, by End-user

- 6.5.4.3. South Africa

- 6.5.4.3.1. Key market trends, growth factors and opportunities

- 6.5.4.3.2. Market size and forecast, by Process

- 6.5.4.3.3. Market size and forecast, by End-user

- 6.5.4.4. Rest of LAMEA

- 6.5.4.4.1. Key market trends, growth factors and opportunities

- 6.5.4.4.2. Market size and forecast, by Process

- 6.5.4.4.3. Market size and forecast, by End-user

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product Mapping of Top 10 Player

- 7.4. Competitive Dashboard

- 7.5. Competitive Heatmap

- 7.6. Top player positioning, 2022

CHAPTER 8: COMPANY PROFILES

- 8.1. Alcoa Corporation

- 8.1.1. Company overview

- 8.1.2. Key Executives

- 8.1.3. Company snapshot

- 8.1.4. Operating business segments

- 8.1.5. Product portfolio

- 8.1.6. Business performance

- 8.1.7. Key strategic moves and developments

- 8.2. RYOBI Aluminium Casting (UK) Ltd.

- 8.2.1. Company overview

- 8.2.2. Key Executives

- 8.2.3. Company snapshot

- 8.2.4. Operating business segments

- 8.2.5. Product portfolio

- 8.3. Shandong Xinanrui Casting

- 8.3.1. Company overview

- 8.3.2. Key Executives

- 8.3.3. Company snapshot

- 8.3.4. Operating business segments

- 8.3.5. Product portfolio

- 8.4. Rio Tinto

- 8.4.1. Company overview

- 8.4.2. Key Executives

- 8.4.3. Company snapshot

- 8.4.4. Operating business segments

- 8.4.5. Product portfolio

- 8.4.6. Business performance

- 8.4.7. Key strategic moves and developments

- 8.5. RusAL

- 8.5.1. Company overview

- 8.5.2. Key Executives

- 8.5.3. Company snapshot

- 8.5.4. Operating business segments

- 8.5.5. Product portfolio

- 8.5.6. Business performance

- 8.5.7. Key strategic moves and developments

- 8.6. Walbro

- 8.6.1. Company overview

- 8.6.2. Key Executives

- 8.6.3. Company snapshot

- 8.6.4. Operating business segments

- 8.6.5. Product portfolio

- 8.7. Consolidated Metco, Inc.

- 8.7.1. Company overview

- 8.7.2. Key Executives

- 8.7.3. Company snapshot

- 8.7.4. Operating business segments

- 8.7.5. Product portfolio

- 8.8. BUVO Castings

- 8.8.1. Company overview

- 8.8.2. Key Executives

- 8.8.3. Company snapshot

- 8.8.4. Operating business segments

- 8.8.5. Product portfolio

- 8.9. Dynacast

- 8.9.1. Company overview

- 8.9.2. Key Executives

- 8.9.3. Company snapshot

- 8.9.4. Operating business segments

- 8.9.5. Product portfolio

- 8.10. Bodine Aluminum

- 8.10.1. Company overview

- 8.10.2. Key Executives

- 8.10.3. Company snapshot

- 8.10.4. Operating business segments

- 8.10.5. Product portfolio

LIST OF TABLES

- TABLE 01. GLOBAL ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 02. GLOBAL ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 03. ALUMINUM CASTING MARKET FOR DIE CASTING, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. ALUMINUM CASTING MARKET FOR DIE CASTING, BY REGION, 2022-2032 (KILOTON)

- TABLE 05. ALUMINUM CASTING MARKET FOR SAND CASTING, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. ALUMINUM CASTING MARKET FOR SAND CASTING, BY REGION, 2022-2032 (KILOTON)

- TABLE 07. ALUMINUM CASTING MARKET FOR PERMANENT MOLD CASTING, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. ALUMINUM CASTING MARKET FOR PERMANENT MOLD CASTING, BY REGION, 2022-2032 (KILOTON)

- TABLE 09. GLOBAL ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 10. GLOBAL ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 11. ALUMINUM CASTING MARKET FOR BUILDING AND CONSTRUCTION, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. ALUMINUM CASTING MARKET FOR BUILDING AND CONSTRUCTION, BY REGION, 2022-2032 (KILOTON)

- TABLE 13. ALUMINUM CASTING MARKET FOR INDUSTRIAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. ALUMINUM CASTING MARKET FOR INDUSTRIAL, BY REGION, 2022-2032 (KILOTON)

- TABLE 15. ALUMINUM CASTING MARKET FOR TRANSPORTATION, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. ALUMINUM CASTING MARKET FOR TRANSPORTATION, BY REGION, 2022-2032 (KILOTON)

- TABLE 17. ALUMINUM CASTING MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 18. ALUMINUM CASTING MARKET FOR OTHERS, BY REGION, 2022-2032 (KILOTON)

- TABLE 19. ALUMINUM CASTING MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 20. ALUMINUM CASTING MARKET, BY REGION, 2022-2032 (KILOTON)

- TABLE 21. NORTH AMERICA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 22. NORTH AMERICA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 23. NORTH AMERICA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 24. NORTH AMERICA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 25. NORTH AMERICA ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 26. NORTH AMERICA ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 (KILOTON)

- TABLE 27. U.S. ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 28. U.S. ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 29. U.S. ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 30. U.S. ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 31. CANADA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 32. CANADA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 33. CANADA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 34. CANADA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 35. MEXICO ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 36. MEXICO ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 37. MEXICO ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 38. MEXICO ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 39. EUROPE ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 40. EUROPE ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 41. EUROPE ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 42. EUROPE ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 43. EUROPE ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 44. EUROPE ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 (KILOTON)

- TABLE 45. GERMANY ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 46. GERMANY ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 47. GERMANY ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 48. GERMANY ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 49. UK ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 50. UK ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 51. UK ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 52. UK ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 53. FRANCE ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 54. FRANCE ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 55. FRANCE ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 56. FRANCE ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 57. SPAIN ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 58. SPAIN ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 59. SPAIN ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 60. SPAIN ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 61. ITALY ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 62. ITALY ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 63. ITALY ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 64. ITALY ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 65. REST OF EUROPE ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 66. REST OF EUROPE ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 67. REST OF EUROPE ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 68. REST OF EUROPE ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 69. ASIA-PACIFIC ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 70. ASIA-PACIFIC ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 71. ASIA-PACIFIC ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 72. ASIA-PACIFIC ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 73. ASIA-PACIFIC ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 74. ASIA-PACIFIC ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 (KILOTON)

- TABLE 75. CHINA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 76. CHINA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 77. CHINA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 78. CHINA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 79. INDIA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 80. INDIA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 81. INDIA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 82. INDIA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 83. JAPAN ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 84. JAPAN ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 85. JAPAN ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 86. JAPAN ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 87. SOUTH KOREA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 88. SOUTH KOREA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 89. SOUTH KOREA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 90. SOUTH KOREA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 91. AUSTRALIA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 92. AUSTRALIA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 93. AUSTRALIA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 94. AUSTRALIA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 95. REST OF ASIA-PACIFIC ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 96. REST OF ASIA-PACIFIC ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 97. REST OF ASIA-PACIFIC ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 98. REST OF ASIA-PACIFIC ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 99. LAMEA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 100. LAMEA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 101. LAMEA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 102. LAMEA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 103. LAMEA ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 104. LAMEA ALUMINUM CASTING MARKET, BY COUNTRY, 2022-2032 (KILOTON)

- TABLE 105. BRAZIL ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 106. BRAZIL ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 107. BRAZIL ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 108. BRAZIL ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 109. SAUDI ARABIA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 110. SAUDI ARABIA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 111. SAUDI ARABIA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 112. SAUDI ARABIA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 113. SOUTH AFRICA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 114. SOUTH AFRICA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 115. SOUTH AFRICA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 116. SOUTH AFRICA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 117. REST OF LAMEA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 ($MILLION)

- TABLE 118. REST OF LAMEA ALUMINUM CASTING MARKET, BY PROCESS, 2022-2032 (KILOTON)

- TABLE 119. REST OF LAMEA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 120. REST OF LAMEA ALUMINUM CASTING MARKET, BY END-USER, 2022-2032 (KILOTON)

- TABLE 121. ALCOA CORPORATION: KEY EXECUTIVES

- TABLE 122. ALCOA CORPORATION: COMPANY SNAPSHOT

- TABLE 123. ALCOA CORPORATION: PRODUCT SEGMENTS

- TABLE 124. ALCOA CORPORATION: PRODUCT PORTFOLIO

- TABLE 125. ALCOA CORPORATION: KEY STRATERGIES

- TABLE 126. RYOBI ALUMINIUM CASTING (UK) LTD.: KEY EXECUTIVES

- TABLE 127. RYOBI ALUMINIUM CASTING (UK) LTD.: COMPANY SNAPSHOT

- TABLE 128. RYOBI ALUMINIUM CASTING (UK) LTD.: PRODUCT SEGMENTS

- TABLE 129. RYOBI ALUMINIUM CASTING (UK) LTD.: PRODUCT PORTFOLIO

- TABLE 130. SHANDONG XINANRUI CASTING: KEY EXECUTIVES

- TABLE 131. SHANDONG XINANRUI CASTING: COMPANY SNAPSHOT

- TABLE 132. SHANDONG XINANRUI CASTING: PRODUCT SEGMENTS

- TABLE 133. SHANDONG XINANRUI CASTING: PRODUCT PORTFOLIO

- TABLE 134. RIO TINTO: KEY EXECUTIVES

- TABLE 135. RIO TINTO: COMPANY SNAPSHOT

- TABLE 136. RIO TINTO: PRODUCT SEGMENTS

- TABLE 137. RIO TINTO: PRODUCT PORTFOLIO

- TABLE 138. RIO TINTO: KEY STRATERGIES

- TABLE 139. RUSAL: KEY EXECUTIVES

- TABLE 140. RUSAL: COMPANY SNAPSHOT

- TABLE 141. RUSAL: PRODUCT SEGMENTS

- TABLE 142. RUSAL: PRODUCT PORTFOLIO

- TABLE 143. RUSAL: KEY STRATERGIES

- TABLE 144. WALBRO: KEY EXECUTIVES

- TABLE 145. WALBRO: COMPANY SNAPSHOT

- TABLE 146. WALBRO: PRODUCT SEGMENTS

- TABLE 147. WALBRO: PRODUCT PORTFOLIO

- TABLE 148. CONSOLIDATED METCO, INC.: KEY EXECUTIVES

- TABLE 149. CONSOLIDATED METCO, INC.: COMPANY SNAPSHOT

- TABLE 150. CONSOLIDATED METCO, INC.: PRODUCT SEGMENTS

- TABLE 151. CONSOLIDATED METCO, INC.: PRODUCT PORTFOLIO

- TABLE 152. BUVO CASTINGS: KEY EXECUTIVES

- TABLE 153. BUVO CASTINGS: COMPANY SNAPSHOT

- TABLE 154. BUVO CASTINGS: PRODUCT SEGMENTS

- TABLE 155. BUVO CASTINGS: PRODUCT PORTFOLIO

- TABLE 156. DYNACAST: KEY EXECUTIVES

- TABLE 157. DYNACAST: COMPANY SNAPSHOT

- TABLE 158. DYNACAST: PRODUCT SEGMENTS

- TABLE 159. DYNACAST: PRODUCT PORTFOLIO

- TABLE 160. BODINE ALUMINUM: KEY EXECUTIVES

- TABLE 161. BODINE ALUMINUM: COMPANY SNAPSHOT

- TABLE 162. BODINE ALUMINUM: PRODUCT SEGMENTS

- TABLE 163. BODINE ALUMINUM: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. ALUMINUM CASTING MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF ALUMINUM CASTING MARKET, 2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN ALUMINUM CASTING MARKET (2023-2032)

- FIGURE 04. MODERATE BARGAINING POWER OF SUPPLIERS

- FIGURE 05. HIGH BARGAINING POWER OF BUYERS

- FIGURE 06. MODERATE THREAT OF SUBSTITUTES

- FIGURE 07. MODERATE THREAT OF NEW ENTRANTS

- FIGURE 08. MODERATE INTENSITY OF RIVALRY

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBALALUMINUM CASTING MARKET

- FIGURE 10. IMPACT OF KEY REGULATION: ALUMINUM CASTING MARKET

- FIGURE 11. PATENT ANALYSIS BY COMPANY

- FIGURE 12. PATENT ANALYSIS BY COUNTRY

- FIGURE 13. PRICING ANALYSIS: ALUMINUM CASTING MARKET 2022 AND 2032

- FIGURE 14. REGULATORY GUIDELINES: ALUMINUM CASTING MARKET

- FIGURE 15. VALUE CHAIN ANALYSIS: ALUMINUM CASTING MARKET

- FIGURE 16. ALUMINUM CASTING MARKET, BY PROCESS, 2022(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR DIE CASTING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR SAND CASTING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR PERMANENT MOLD CASTING, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. ALUMINUM CASTING MARKET, BY END-USER, 2022(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR BUILDING AND CONSTRUCTION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR INDUSTRIAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR TRANSPORTATION, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF ALUMINUM CASTING MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. ALUMINUM CASTING MARKET BY REGION, 2022

- FIGURE 26. U.S. ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 27. CANADA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 28. MEXICO ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 29. GERMANY ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 30. UK ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 31. FRANCE ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 32. SPAIN ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 33. ITALY ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 34. REST OF EUROPE ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 35. CHINA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 36. INDIA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 37. JAPAN ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 38. SOUTH KOREA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 39. AUSTRALIA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 40. REST OF ASIA-PACIFIC ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 41. BRAZIL ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 42. SAUDI ARABIA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 43. SOUTH AFRICA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 44. REST OF LAMEA ALUMINUM CASTING MARKET, 2022-2032 ($MILLION)

- FIGURE 45. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 46. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 47. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 48. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 49. COMPETITIVE DASHBOARD

- FIGURE 50. COMPETITIVE HEATMAP: ALUMINUM CASTING MARKET

- FIGURE 51. TOP PLAYER POSITIONING, 2022

- FIGURE 52. ALCOA CORPORATION: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 53. ALCOA CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 54. ALCOA CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 55. RIO TINTO: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 56. RIO TINTO: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 57. RIO TINTO: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 58. RUSAL: NET REVENUE, 2019-2021 ($MILLION)

- FIGURE 59. RUSAL: REVENUE SHARE BY REGION, 2021 (%)

- FIGURE 60. RUSAL: REVENUE SHARE BY SEGMENT, 2021 (%)

全球铝铸件市场 - 2024-2031

全球铝铸件市场 - 2024-2031 铝铸造市场报告:2030 年趋势、预测与竞争分析

铝铸造市场报告:2030 年趋势、预测与竞争分析 铝铸造市场:按工艺、最终用途划分 - 2024-2030 年全球预测

铝铸造市场:按工艺、最终用途划分 - 2024-2030 年全球预测![铝铸件市场 [来源:初级和次级;製程:压铸、金属型铸造、砂型铸造;应用:汽车与非汽车] - 2023-2031 年全球产业分析、规模、份额、成长、趋势与预测](/sample/img/cover/42/1420852.png) 铝铸件市场 [来源:初级和次级;製程:压铸、金属型铸造、砂型铸造;应用:汽车与非汽车] - 2023-2031 年全球产业分析、规模、份额、成长、趋势与预测

铝铸件市场 [来源:初级和次级;製程:压铸、金属型铸造、砂型铸造;应用:汽车与非汽车] - 2023-2031 年全球产业分析、规模、份额、成长、趋势与预测 2024年铝铸件全球市场报告

2024年铝铸件全球市场报告 2030 年铝铸造产品市场预测:按产品、销售管道、应用和地区分類的全球分析

2030 年铝铸造产品市场预测:按产品、销售管道、应用和地区分類的全球分析 铝铸造品的全球市场

铝铸造品的全球市场 铝锻件市场 - 增长、趋势、COVID-19 影响和预测 (2023-2028)

铝锻件市场 - 增长、趋势、COVID-19 影响和预测 (2023-2028) 铝铸造的全球市场调查报告-产业分析,规模,占有率,成长,趋势,2022年~2028年前的预测

铝铸造的全球市场调查报告-产业分析,规模,占有率,成长,趋势,2022年~2028年前的预测 铝铸造的全球市场 (2022~2030年):成长、未来展望、竞争分析

铝铸造的全球市场 (2022~2030年):成长、未来展望、竞争分析