|

市场调查报告书

商品编码

1344508

糖尿病足部溃伤治疗市场:各产品类型,各终端用户:全球机会分析与产业预测,2023-2032年Diabetic Foot Ulcer Treatment Market By Product, By Type, By End User: Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

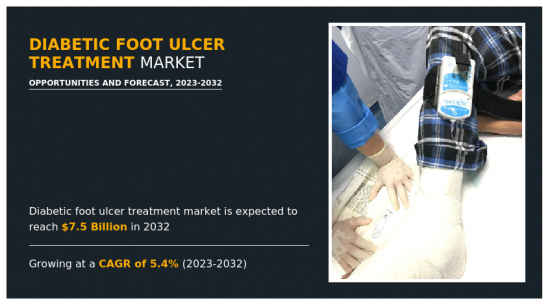

2022 年糖尿病足溃疡治疗市场价值为 44 亿美元,预计到 2032 年将达到 74 亿美元,复合年增长率为2023年至2032年为5.4%。

糖尿病足溃疡是糖尿病常见且严重的併发症。糖尿病足溃疡是糖尿病患者足部发生的开放性溃疡或伤口。糖尿病足溃疡是由多种与糖尿病相关的因素造成的,包括血液循环不良、神经病变和免疫功能下降。如果不及时治疗,糖尿病足溃疡可能会变成慢性,并促使严重的併发症,如感染、坏疽,甚至截肢。因此,正确管理和治疗糖尿病足溃疡对于预防这些併发症和促进伤口癒合至关重要。

推动糖尿病足溃疡治疗发展的主要因素是患有糖尿病足溃疡的人数不断增加、研发活动的增加以及对适当糖尿病足护理的意识的提高。久坐的生活、不健康的饮食和日益肥胖等因素加剧了全球糖尿病发生率的上升。此外,高血糖水平的延迟会促使周围神经病变,这种疾病会损害脚趾神经并减弱感觉。此外,血液循环不良(称为週边动脉疾病)会进一步损害脚部伤口的癒合。这些因素与不断发展的糖尿病族群结合,促使糖尿病足溃疡的发生频率增加。

目录

第1章 简介

第2章 摘要整理

第3章 市场概要

- 市场定义和范围

- 主要调查结果

- 影响要素

- 主要的投资机会

- 波特的五力分析

- 市场动态

- 促进因素

- 糖尿病足部溃伤的增加

- 伤口护理管理上技术的进步

- 糖尿病足部溃伤治疗的新产品销售的增加

- 阻碍因素

- 创伤护理产品的製造相关严格法规

- 机会

- 新兴市场的成长机会

- 促进因素

- COVID-19对市场的影响分析

第4章 糖尿病足部溃伤治疗药市场:各产品

- 概要

- 伤口敷料

- 创伤护理器具

- 生技药品

- 其他

第5章 糖尿病足部溃伤治疗市场:各类型

- 概要

- 神经病变性溃疡

- 缺血性溃疡

- 神经缺血性溃疡

第6章 糖尿病足部溃伤治疗市场:各终端用户

- 概要

- 医院

- 居家医疗

- 其他

第7章 糖尿病足部溃伤治疗市场:各地区

- 概要

- 北美

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 其他

- 亚太地区

- 日本

- 中国

- 印度

- 澳洲

- 韩国

- 其他

- 南美·中东·非洲

- 巴西

- 沙乌地阿拉伯

- 南非

- 其他

第8章 竞争情形

- 简介

- 主要成功策略

- 主要10企业的产品製图

- 竞争仪表板

- 竞争热图

- 主要企业的定位,2022年

第9章 企业简介

- ConvaTec Group plc

- 3M Company

- Cardinal Health Inc.

- ORGANOGENESIS HOLDINGS INC.

- Smith and Nephew plc.

- B. Braun SE

- Coloplast

- Integra LifeSciences Holdings Corporation

- Molnlycke Health Care AB

- Essity Aktiebolag AB

According to a new report published by Allied Market Research, titled, "Diabetic Foot Ulcer Treatment Market," The diabetic foot ulcer treatment market was valued at $4.4 billion in 2022, and is estimated to reach $7.4 billion by 2032, growing at a CAGR of 5.4% from 2023 to 2032. Diabetic foot ulcers are a common and serious complication of diabetes mellitus. They are open sores or wounds that typically develop on the feet of individuals with diabetes. Diabetic foot ulcers are a result of various factors, including poor circulation, nerve damage (neuropathy), and impaired immune function, which are all associated with diabetes. If left untreated, diabetic foot ulcer can become chronic, leading to severe complications such as infection, gangrene, and even amputation. Thus, proper management and treatment of diabetic foot ulcers are crucial to prevent these complications and promote wound healing.

The major factors driving the development of the diabetic foot ulcer treatments are increasing number of individuals suffering from diabetic foot ulcers, rise in R & D exercises, and surge in awareness about proper diabetic foot care. The predominance of diabetes is on the rise across the globe, fueled through factors which include sedentary life, unhealthy diets, and growing obesity. Further, delayed periods of high blood sugar level can result in peripheral neuropathy, a condition that harms the nerves in the toes and diminishes sensation. In addition, poor blood circulation, known as peripheral arterial disease, advance impairs wound healing within the feet. These components, combined with the developing diabetic populace, contribute to an expanded frequency of diabetic foot ulcers. For instance, as per, Centers for Disease Control and Prevention (CDC), 2022, almost 12% individuals with diabetes develop diabetic foot ulcers in U.S. Thus, increasing number of individuals suffering from diabetic foot ulcer has driven the request for compelling treatment options and thereby, propelling the development of the diabetic foot ulcer treatment market.

In addition, researchers and medical experts are actively involved in studying the pathophysiology of diabetic foot ulcers, exploring new treatment modalities and improving existing healing procedures. The use of advanced technology has caused the improvement of modern wound care products, bioengineered pores and skin substitutes and off-loading devices. These improvements aim to enhance wound healing, protect infections, and offer better management options for diabetic foot ulcers. Further, there are ongoing studies in field of regenerative medicine, exploring the potential of stem cells, growth factors, and tissue engineering to promote wound healing. The growing funding in research and development activities by pharmaceutical organizations, instructional institutions and healthcare companies has expanded the invention of novel therapeutic strategies, fueling the growth of the market.

Furthermore, surge in awareness about proper diabetic foot care has contributed to the growth of the diabetic foot ulcer treatment market. Healthcare organizations, diabetes associations, and healthcare professionals had been actively raising focus about the importance of foot care in individuals with diabetes. Diabetic foot ulcers can be averted or minimized through regular foot examinations, right shoes, foot hygiene, and early detection of foot ulcers. Furthermore, education campaigns and initiatives aimed at improving foot care practices have led to increased patient awareness and engagement. As individuals become more aware about the risks and consequences of diabetic foot ulcers, they are more anticipated to seek timely medical attention and adhere to preventive measures. This heightened awareness has not only improved patient outcomes but has also driven the demand for diabetic foot ulcer treatment options.

The global diabetic foot ulcer treatment market is segmented into product, type, end user, and region. On the basis of product, the market is categorized into wound care dressings, wound care devices, biologics and others. The wound care devices segment is further categorized into negative pressure wound therapy and others. Based on type, it is categorized into neuropathic ulcers, ischemic ulcers and neuroischemic ulcers. As per end user, it is segregated into hospitals, homecare settings, and others. Region wise, the market is analyzed across North America (the U.S., Canada, and Mexico), Europe (Germany, France, the UK, Italy, Spain, and rest of Europe), Asia-Pacific (Japan, China, Australia, India, South Korea, and rest of Asia-Pacific), and LAMEA (Brazil, South Africa, Saudi Arabia, and rest of LAMEA).

Major key players that operate in the global diabetic foot ulcer treatment market are ConvaTec Group plc, 3M Company, Cardinal Health Inc., Organogenesis Holdings Inc., Smith and Nephew plc., B. Braun SE, Coloplast, Integra LifeSciences Holdings Corporation, Molnlycke Health Care AB, and Essity Aktiebolag AB. The key players have adopted strategies such as acquisition, contract, product launch, and product approval to expand their product portfolio.

Key Benefits for Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the diabetic foot ulcer treatment market analysis from 2022 to 2032 to identify the prevailing diabetic foot ulcer treatment market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the diabetic foot ulcer treatment market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global diabetic foot ulcer treatment market trends, key players, market segments, application areas, and market growth strategies.

Key Market Segments

By Product

- Wound care dressings

- Wound care devices

- Type

- Negative pressure wound therapy

- Others

- Biologics

- Others

By Type

- Neuropathic ulcers

- Ischemic ulcers

- Neuroischemic ulcers

By End user

- Hospitals

- Homecare settings

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- 3M Company

- B. Braun SE

- Cardinal Health Inc.

- Coloplast

- ConvaTec Group plc

- Essity Aktiebolag AB

- Integra LifeSciences Holdings Corporation

- Molnlycke Health Care AB

- ORGANOGENESIS HOLDINGS INC.

- Smith and Nephew plc.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. High bargaining power of suppliers

- 3.3.2. Moderate threat of new entrants

- 3.3.3. Moderate threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. High bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Increase in prevalence of diabetic foot ulcer

- 3.4.1.2. Technological advancements in wound care management

- 3.4.1.3. Rise in new product launches for diabetic foot ulcer treatment

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.2.1. Stringent regulations for manufacturing of wound care products

- 3.4.3. Opportunities

- 3.4.3.1. Growing opportunity in emerging markets

- 3.5. COVID-19 Impact Analysis on the market

CHAPTER 4: DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Wound care dressings

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Wound care devices

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.3.4. Wound care devices Diabetic Foot Ulcer Treatment Market by Type

- 4.4. Biologics

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Others

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

CHAPTER 5: DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Neuropathic ulcers

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Ischemic ulcers

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Neuroischemic ulcers

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

CHAPTER 6: DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Hospitals

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Homecare settings

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Others

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: DIABETIC FOOT ULCER TREATMENT MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key trends and opportunities

- 7.2.2. Market size and forecast, by Product

- 7.2.3. Market size and forecast, by Type

- 7.2.4. Market size and forecast, by End user

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Key market trends, growth factors and opportunities

- 7.2.5.1.2. Market size and forecast, by Product

- 7.2.5.1.3. Market size and forecast, by Type

- 7.2.5.1.4. Market size and forecast, by End user

- 7.2.5.2. Canada

- 7.2.5.2.1. Key market trends, growth factors and opportunities

- 7.2.5.2.2. Market size and forecast, by Product

- 7.2.5.2.3. Market size and forecast, by Type

- 7.2.5.2.4. Market size and forecast, by End user

- 7.2.5.3. Mexico

- 7.2.5.3.1. Key market trends, growth factors and opportunities

- 7.2.5.3.2. Market size and forecast, by Product

- 7.2.5.3.3. Market size and forecast, by Type

- 7.2.5.3.4. Market size and forecast, by End user

- 7.3. Europe

- 7.3.1. Key trends and opportunities

- 7.3.2. Market size and forecast, by Product

- 7.3.3. Market size and forecast, by Type

- 7.3.4. Market size and forecast, by End user

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Key market trends, growth factors and opportunities

- 7.3.5.1.2. Market size and forecast, by Product

- 7.3.5.1.3. Market size and forecast, by Type

- 7.3.5.1.4. Market size and forecast, by End user

- 7.3.5.2. France

- 7.3.5.2.1. Key market trends, growth factors and opportunities

- 7.3.5.2.2. Market size and forecast, by Product

- 7.3.5.2.3. Market size and forecast, by Type

- 7.3.5.2.4. Market size and forecast, by End user

- 7.3.5.3. UK

- 7.3.5.3.1. Key market trends, growth factors and opportunities

- 7.3.5.3.2. Market size and forecast, by Product

- 7.3.5.3.3. Market size and forecast, by Type

- 7.3.5.3.4. Market size and forecast, by End user

- 7.3.5.4. Italy

- 7.3.5.4.1. Key market trends, growth factors and opportunities

- 7.3.5.4.2. Market size and forecast, by Product

- 7.3.5.4.3. Market size and forecast, by Type

- 7.3.5.4.4. Market size and forecast, by End user

- 7.3.5.5. Spain

- 7.3.5.5.1. Key market trends, growth factors and opportunities

- 7.3.5.5.2. Market size and forecast, by Product

- 7.3.5.5.3. Market size and forecast, by Type

- 7.3.5.5.4. Market size and forecast, by End user

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Key market trends, growth factors and opportunities

- 7.3.5.6.2. Market size and forecast, by Product

- 7.3.5.6.3. Market size and forecast, by Type

- 7.3.5.6.4. Market size and forecast, by End user

- 7.4. Asia-Pacific

- 7.4.1. Key trends and opportunities

- 7.4.2. Market size and forecast, by Product

- 7.4.3. Market size and forecast, by Type

- 7.4.4. Market size and forecast, by End user

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. Japan

- 7.4.5.1.1. Key market trends, growth factors and opportunities

- 7.4.5.1.2. Market size and forecast, by Product

- 7.4.5.1.3. Market size and forecast, by Type

- 7.4.5.1.4. Market size and forecast, by End user

- 7.4.5.2. China

- 7.4.5.2.1. Key market trends, growth factors and opportunities

- 7.4.5.2.2. Market size and forecast, by Product

- 7.4.5.2.3. Market size and forecast, by Type

- 7.4.5.2.4. Market size and forecast, by End user

- 7.4.5.3. India

- 7.4.5.3.1. Key market trends, growth factors and opportunities

- 7.4.5.3.2. Market size and forecast, by Product

- 7.4.5.3.3. Market size and forecast, by Type

- 7.4.5.3.4. Market size and forecast, by End user

- 7.4.5.4. Australia

- 7.4.5.4.1. Key market trends, growth factors and opportunities

- 7.4.5.4.2. Market size and forecast, by Product

- 7.4.5.4.3. Market size and forecast, by Type

- 7.4.5.4.4. Market size and forecast, by End user

- 7.4.5.5. South Korea

- 7.4.5.5.1. Key market trends, growth factors and opportunities

- 7.4.5.5.2. Market size and forecast, by Product

- 7.4.5.5.3. Market size and forecast, by Type

- 7.4.5.5.4. Market size and forecast, by End user

- 7.4.5.6. Rest of Asia-Pacific

- 7.4.5.6.1. Key market trends, growth factors and opportunities

- 7.4.5.6.2. Market size and forecast, by Product

- 7.4.5.6.3. Market size and forecast, by Type

- 7.4.5.6.4. Market size and forecast, by End user

- 7.5. LAMEA

- 7.5.1. Key trends and opportunities

- 7.5.2. Market size and forecast, by Product

- 7.5.3. Market size and forecast, by Type

- 7.5.4. Market size and forecast, by End user

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Key market trends, growth factors and opportunities

- 7.5.5.1.2. Market size and forecast, by Product

- 7.5.5.1.3. Market size and forecast, by Type

- 7.5.5.1.4. Market size and forecast, by End user

- 7.5.5.2. Saudi Arabia

- 7.5.5.2.1. Key market trends, growth factors and opportunities

- 7.5.5.2.2. Market size and forecast, by Product

- 7.5.5.2.3. Market size and forecast, by Type

- 7.5.5.2.4. Market size and forecast, by End user

- 7.5.5.3. South Africa

- 7.5.5.3.1. Key market trends, growth factors and opportunities

- 7.5.5.3.2. Market size and forecast, by Product

- 7.5.5.3.3. Market size and forecast, by Type

- 7.5.5.3.4. Market size and forecast, by End user

- 7.5.5.4. Rest of LAMEA

- 7.5.5.4.1. Key market trends, growth factors and opportunities

- 7.5.5.4.2. Market size and forecast, by Product

- 7.5.5.4.3. Market size and forecast, by Type

- 7.5.5.4.4. Market size and forecast, by End user

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product Mapping of Top 10 Player

- 8.4. Competitive Dashboard

- 8.5. Competitive Heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. ConvaTec Group plc

- 9.1.1. Company overview

- 9.1.2. Key Executives

- 9.1.3. Company snapshot

- 9.1.4. Operating business segments

- 9.1.5. Product portfolio

- 9.1.6. Business performance

- 9.1.7. Key strategic moves and developments

- 9.2. 3M Company

- 9.2.1. Company overview

- 9.2.2. Key Executives

- 9.2.3. Company snapshot

- 9.2.4. Operating business segments

- 9.2.5. Product portfolio

- 9.2.6. Business performance

- 9.3. Cardinal Health Inc.

- 9.3.1. Company overview

- 9.3.2. Key Executives

- 9.3.3. Company snapshot

- 9.3.4. Operating business segments

- 9.3.5. Product portfolio

- 9.3.6. Business performance

- 9.3.7. Key strategic moves and developments

- 9.4. ORGANOGENESIS HOLDINGS INC.

- 9.4.1. Company overview

- 9.4.2. Key Executives

- 9.4.3. Company snapshot

- 9.4.4. Operating business segments

- 9.4.5. Product portfolio

- 9.4.6. Business performance

- 9.4.7. Key strategic moves and developments

- 9.5. Smith and Nephew plc.

- 9.5.1. Company overview

- 9.5.2. Key Executives

- 9.5.3. Company snapshot

- 9.5.4. Operating business segments

- 9.5.5. Product portfolio

- 9.5.6. Business performance

- 9.5.7. Key strategic moves and developments

- 9.6. B. Braun SE

- 9.6.1. Company overview

- 9.6.2. Key Executives

- 9.6.3. Company snapshot

- 9.6.4. Operating business segments

- 9.6.5. Product portfolio

- 9.6.6. Business performance

- 9.7. Coloplast

- 9.7.1. Company overview

- 9.7.2. Key Executives

- 9.7.3. Company snapshot

- 9.7.4. Operating business segments

- 9.7.5. Product portfolio

- 9.7.6. Business performance

- 9.8. Integra LifeSciences Holdings Corporation

- 9.8.1. Company overview

- 9.8.2. Key Executives

- 9.8.3. Company snapshot

- 9.8.4. Operating business segments

- 9.8.5. Product portfolio

- 9.8.6. Business performance

- 9.9. Molnlycke Health Care AB

- 9.9.1. Company overview

- 9.9.2. Key Executives

- 9.9.3. Company snapshot

- 9.9.4. Operating business segments

- 9.9.5. Product portfolio

- 9.9.6. Business performance

- 9.10. Essity Aktiebolag AB

- 9.10.1. Company overview

- 9.10.2. Key Executives

- 9.10.3. Company snapshot

- 9.10.4. Operating business segments

- 9.10.5. Product portfolio

- 9.10.6. Business performance

- 9.10.7. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 02. DIABETIC FOOT ULCER TREATMENT MARKET FOR WOUND CARE DRESSINGS, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. DIABETIC FOOT ULCER TREATMENT MARKET FOR WOUND CARE DEVICES, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL WOUND CARE DEVICES DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 05. DIABETIC FOOT ULCER TREATMENT MARKET FOR BIOLOGICS, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. DIABETIC FOOT ULCER TREATMENT MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 08. DIABETIC FOOT ULCER TREATMENT MARKET FOR NEUROPATHIC ULCERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. DIABETIC FOOT ULCER TREATMENT MARKET FOR ISCHEMIC ULCERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. DIABETIC FOOT ULCER TREATMENT MARKET FOR NEUROISCHEMIC ULCERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. GLOBAL DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 12. DIABETIC FOOT ULCER TREATMENT MARKET FOR HOSPITALS, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. DIABETIC FOOT ULCER TREATMENT MARKET FOR HOMECARE SETTINGS, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. DIABETIC FOOT ULCER TREATMENT MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. DIABETIC FOOT ULCER TREATMENT MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. NORTH AMERICA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 18. NORTH AMERICA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 19. NORTH AMERICA DIABETIC FOOT ULCER TREATMENT MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 20. U.S. DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 21. U.S. DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 22. U.S. DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 23. CANADA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 24. CANADA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 25. CANADA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 26. MEXICO DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 27. MEXICO DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 28. MEXICO DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 29. EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 30. EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 31. EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 32. EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 33. GERMANY DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 34. GERMANY DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 35. GERMANY DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 36. FRANCE DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 37. FRANCE DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 38. FRANCE DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 39. UK DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 40. UK DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 41. UK DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 42. ITALY DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 43. ITALY DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 44. ITALY DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 45. SPAIN DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 46. SPAIN DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 47. SPAIN DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 48. REST OF EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 49. REST OF EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 50. REST OF EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 51. ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 52. ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 53. ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 54. ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 55. JAPAN DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 56. JAPAN DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 57. JAPAN DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 58. CHINA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 59. CHINA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 60. CHINA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 61. INDIA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 62. INDIA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 63. INDIA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 64. AUSTRALIA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 65. AUSTRALIA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 66. AUSTRALIA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 67. SOUTH KOREA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 68. SOUTH KOREA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 69. SOUTH KOREA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 70. REST OF ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 71. REST OF ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 72. REST OF ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 73. LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 74. LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 75. LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 76. LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 77. BRAZIL DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 78. BRAZIL DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 79. BRAZIL DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 80. SAUDI ARABIA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 81. SAUDI ARABIA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 82. SAUDI ARABIA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 83. SOUTH AFRICA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 84. SOUTH AFRICA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 85. SOUTH AFRICA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 86. REST OF LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 87. REST OF LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 88. REST OF LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 89. CONVATEC GROUP PLC: KEY EXECUTIVES

- TABLE 90. CONVATEC GROUP PLC: COMPANY SNAPSHOT

- TABLE 91. CONVATEC GROUP PLC: PRODUCT SEGMENTS

- TABLE 92. CONVATEC GROUP PLC: PRODUCT PORTFOLIO

- TABLE 93. CONVATEC GROUP PLC: KEY STRATERGIES

- TABLE 94. 3M COMPANY: KEY EXECUTIVES

- TABLE 95. 3M COMPANY: COMPANY SNAPSHOT

- TABLE 96. 3M COMPANY: PRODUCT SEGMENTS

- TABLE 97. 3M COMPANY: PRODUCT PORTFOLIO

- TABLE 98. CARDINAL HEALTH INC.: KEY EXECUTIVES

- TABLE 99. CARDINAL HEALTH INC.: COMPANY SNAPSHOT

- TABLE 100. CARDINAL HEALTH INC.: PRODUCT SEGMENTS

- TABLE 101. CARDINAL HEALTH INC.: PRODUCT PORTFOLIO

- TABLE 102. CARDINAL HEALTH INC.: KEY STRATERGIES

- TABLE 103. ORGANOGENESIS HOLDINGS INC.: KEY EXECUTIVES

- TABLE 104. ORGANOGENESIS HOLDINGS INC.: COMPANY SNAPSHOT

- TABLE 105. ORGANOGENESIS HOLDINGS INC.: PRODUCT SEGMENTS

- TABLE 106. ORGANOGENESIS HOLDINGS INC.: PRODUCT PORTFOLIO

- TABLE 107. ORGANOGENESIS HOLDINGS INC.: KEY STRATERGIES

- TABLE 108. SMITH AND NEPHEW PLC.: KEY EXECUTIVES

- TABLE 109. SMITH AND NEPHEW PLC.: COMPANY SNAPSHOT

- TABLE 110. SMITH AND NEPHEW PLC.: PRODUCT SEGMENTS

- TABLE 111. SMITH AND NEPHEW PLC.: PRODUCT PORTFOLIO

- TABLE 112. SMITH AND NEPHEW PLC.: KEY STRATERGIES

- TABLE 113. B. BRAUN SE: KEY EXECUTIVES

- TABLE 114. B. BRAUN SE: COMPANY SNAPSHOT

- TABLE 115. B. BRAUN SE: PRODUCT SEGMENTS

- TABLE 116. B. BRAUN SE: PRODUCT PORTFOLIO

- TABLE 117. COLOPLAST: KEY EXECUTIVES

- TABLE 118. COLOPLAST: COMPANY SNAPSHOT

- TABLE 119. COLOPLAST: PRODUCT SEGMENTS

- TABLE 120. COLOPLAST: PRODUCT PORTFOLIO

- TABLE 121. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: KEY EXECUTIVES

- TABLE 122. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: COMPANY SNAPSHOT

- TABLE 123. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: PRODUCT SEGMENTS

- TABLE 124. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: PRODUCT PORTFOLIO

- TABLE 125. MOLNLYCKE HEALTH CARE AB: KEY EXECUTIVES

- TABLE 126. MOLNLYCKE HEALTH CARE AB: COMPANY SNAPSHOT

- TABLE 127. MOLNLYCKE HEALTH CARE AB: PRODUCT SEGMENTS

- TABLE 128. MOLNLYCKE HEALTH CARE AB: PRODUCT PORTFOLIO

- TABLE 129. ESSITY AKTIEBOLAG AB: KEY EXECUTIVES

- TABLE 130. ESSITY AKTIEBOLAG AB: COMPANY SNAPSHOT

- TABLE 131. ESSITY AKTIEBOLAG AB: PRODUCT SEGMENTS

- TABLE 132. ESSITY AKTIEBOLAG AB: PRODUCT PORTFOLIO

- TABLE 133. ESSITY AKTIEBOLAG AB: KEY STRATERGIES

LIST OF FIGURES

- FIGURE 01. DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032

- FIGURE 03. TOP INVESTMENT POCKETS IN DIABETIC FOOT ULCER TREATMENT MARKET (2023-2032)

- FIGURE 04. HIGH BARGAINING POWER OF SUPPLIERS

- FIGURE 05. MODERATE THREAT OF NEW ENTRANTS

- FIGURE 06. MODERATE THREAT OF SUBSTITUTES

- FIGURE 07. LOW INTENSITY OF RIVALRY

- FIGURE 08. HIGH BARGAINING POWER OF BUYERS

- FIGURE 09. DRIVERS, RESTRAINTS AND OPPORTUNITIES: GLOBALDIABETIC FOOT ULCER TREATMENT MARKET

- FIGURE 09. DIABETIC FOOT ULCER TREATMENT MARKET, BY PRODUCT, 2022(%)

- FIGURE 10. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR WOUND CARE DRESSINGS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 11. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR WOUND CARE DEVICES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR BIOLOGICS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. DIABETIC FOOT ULCER TREATMENT MARKET, BY TYPE, 2022(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR NEUROPATHIC ULCERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR ISCHEMIC ULCERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR NEUROISCHEMIC ULCERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. DIABETIC FOOT ULCER TREATMENT MARKET, BY END USER, 2022(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR HOSPITALS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR HOMECARE SETTINGS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF DIABETIC FOOT ULCER TREATMENT MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. DIABETIC FOOT ULCER TREATMENT MARKET BY REGION, 2022

- FIGURE 23. U.S. DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 24. CANADA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 25. MEXICO DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 26. GERMANY DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 27. FRANCE DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 28. UK DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 29. ITALY DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 30. SPAIN DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 31. REST OF EUROPE DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 32. JAPAN DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 33. CHINA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 34. INDIA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 35. AUSTRALIA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 36. SOUTH KOREA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 37. REST OF ASIA-PACIFIC DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 38. BRAZIL DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 39. SAUDI ARABIA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 40. SOUTH AFRICA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 41. REST OF LAMEA DIABETIC FOOT ULCER TREATMENT MARKET, 2022-2032 ($MILLION)

- FIGURE 42. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 43. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 44. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 45. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 46. COMPETITIVE DASHBOARD

- FIGURE 47. COMPETITIVE HEATMAP: DIABETIC FOOT ULCER TREATMENT MARKET

- FIGURE 48. TOP PLAYER POSITIONING, 2022

- FIGURE 49. CONVATEC GROUP PLC: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 50. CONVATEC GROUP PLC: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 51. CONVATEC GROUP PLC: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 52. 3M COMPANY: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 53. 3M COMPANY: RESEARCH & DEVELOPMENT EXPENDITURE, 2020-2022 ($MILLION)

- FIGURE 54. 3M COMPANY: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 55. 3M COMPANY: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 56. CARDINAL HEALTH INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 57. CARDINAL HEALTH INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 58. CARDINAL HEALTH INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 59. ORGANOGENESIS HOLDINGS INC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 60. SMITH AND NEPHEW PLC.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 61. SMITH AND NEPHEW PLC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 62. SMITH AND NEPHEW PLC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 63. B. BRAUN SE: NET SALES, 2020-2022 ($MILLION)

- FIGURE 64. B. BRAUN SE: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 65. B. BRAUN SE: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 66. COLOPLAST: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 67. COLOPLAST: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 68. COLOPLAST: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 69. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 70. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 71. INTEGRA LIFESCIENCES HOLDINGS CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 72. MOLNLYCKE HEALTH CARE AB: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 73. MOLNLYCKE HEALTH CARE AB: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 74. MOLNLYCKE HEALTH CARE AB: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 75. ESSITY AKTIEBOLAG AB: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 76. ESSITY AKTIEBOLAG AB: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 77. ESSITY AKTIEBOLAG AB: REVENUE SHARE BY REGION, 2022 (%)

2030 年糖尿病溃疡治疗市场预测:按类型、治疗类型、最终用户和地区进行的全球分析糖尿病足溃疡治疗市场规模、份额和成长分析(按治疗、溃疡类型、最终用途和地区)- 产业预测 2025-2032

2030 年糖尿病溃疡治疗市场预测:按类型、治疗类型、最终用户和地区进行的全球分析糖尿病足溃疡治疗市场规模、份额和成长分析(按治疗、溃疡类型、最终用途和地区)- 产业预测 2025-2032 糖尿病足溃疡治疗市场:治疗方法、溃疡类型和最终用途分类 - 全球预测 2025-2030

糖尿病足溃疡治疗市场:治疗方法、溃疡类型和最终用途分类 - 全球预测 2025-2030 糖尿病足溃疡市场报告:2030 年趋势、预测与竞争分析到 2030 年糖尿病足溃疡治疗市场预测:按治疗类型、溃疡类型、最终用户和地区进行的全球分析

糖尿病足溃疡市场报告:2030 年趋势、预测与竞争分析到 2030 年糖尿病足溃疡治疗市场预测:按治疗类型、溃疡类型、最终用户和地区进行的全球分析 糖尿病足溃疡的全球市场规模:按治疗类型、设备、最终用户和地区划分全球糖尿病溃疡治疗市场规模:按治疗、按类型、按最终用户、按地区、范围和预测

糖尿病足溃疡的全球市场规模:按治疗类型、设备、最终用户和地区划分全球糖尿病溃疡治疗市场规模:按治疗、按类型、按最终用户、按地区、范围和预测 美国糖尿病足溃疡治疗市场规模、份额、趋势分析报告:按治疗、溃疡类型、最终用途和细分市场预测,2024-2030 年

美国糖尿病足溃疡治疗市场规模、份额、趋势分析报告:按治疗、溃疡类型、最终用途和细分市场预测,2024-2030 年 亚太地区糖尿病足溃疡市场预测至 2030 年 - 区域分析 - 按溃疡类型、治疗类型、感染严重程度和最终用户

亚太地区糖尿病足溃疡市场预测至 2030 年 - 区域分析 - 按溃疡类型、治疗类型、感染严重程度和最终用户 北美糖尿病足溃疡市场预测至 2030 年 - 区域分析 - 按溃疡类型、治疗类型、感染严重程度和最终用户

北美糖尿病足溃疡市场预测至 2030 年 - 区域分析 - 按溃疡类型、治疗类型、感染严重程度和最终用户