|

市场调查报告书

商品编码

1365595

汽车硅胶市场:按类型、按用途:2023-2032 年全球机会分析与产业预测Automotive Silicone Market By Type (Elastomers, Resins, Gels, Others), By Application (Interior and Exterior, Engines, Electrical Systems, Others): Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

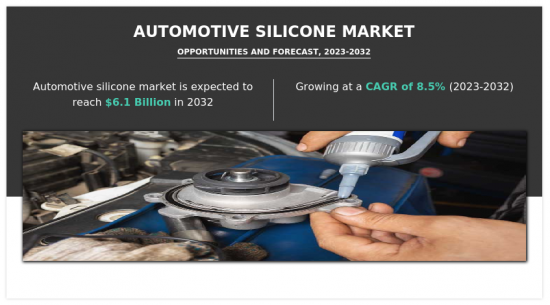

根据Allied Market Research发布的研究报告《汽车硅胶市场》,2022年汽车硅胶市场价值为27亿美元,2023年至2032年将以8.5%的年复合成长率成长,到2032年将达到61亿美元。预计达到美元。

汽车硅胶是一种特殊类型的硅胶材料,主要为汽车用途而设计。有机硅是一种柔性聚合物,具有优异的电绝缘性、耐热性和耐用性。在汽车产业,有机硅因其独特的性能和优点而被主要使用。硅胶的耐温特性使其能够承受极端高温和低温,而不会失去其物理特性。它在很宽的温度范围内保持稳定和弹性,使其适合汽车用途。

减轻汽车重量是寻求提高整体性能和燃油效率的汽车的永恆目标。汽车设计越来越多地采用碳纤维复合材料、高强度钢、铝和塑胶等轻质零件。有机硅基材料,例如黏剂、有机硅泡棉和密封剂,具有替代较重材料的潜力,并且由于其密度较低,已成为汽车产品轻量化过程中的重要一步。这些轻质有机硅材料可用于多种用途,包括密封件、垫圈、电气零件和温度控管系统,从而减轻汽车整体重量。硅基黏剂、密封剂和垫圈用于动力传动系统零件,例如变速箱、引擎和排气系统,以提高性能并减少能量损失。

汽车硅胶的原料硅是不可再生资源,其生产消耗大量能源。此外,有机硅产品不易生物分解,这可能会对废弃物管理造成挑战。随着政府和法规机构实施更严格的环境法规,汽车可能会面临后果,并转向使用比有机硅更永续的材料。有机硅产品的使用和製造会导致挥发性有机化合物 (VOC) 的排放。 VOC 是对人体有害并造成空气污染的危险化合物。挥发性有机化合物的排放通常受到严格的环境法的限制,并会影响汽车有机硅的生产和用途。此外,对永续性的日益关注也增加了对有机硅环保替代品的需求。汽车产业正在探索和采用更环保的解决方案,例如生物基聚合物和可回收材料,以减少其环境足迹。预计这将在预测期内抑制市场成长。

随着全球电动车产量迅速增加,对有机硅材料的需求预计也会激增。这是汽车硅製造商开发创新解决方案、扩大产品范围并满足电动车产业特定需求的机会。电动车在行驶时会产生热量,特别是在电池和动力传动系统系统中。基于有机硅的温度控管解决方案(凝胶、热界面材料、黏剂等)可有效管理和散热,以确保电动车组件的理想性能和安全性。此外,有机硅材料具有优异的电绝缘性能,使其适用于电动车电缆和电线绝缘、连接器和垫圈等用途。随着电动车配备先进的电子设备和电气系统,对可靠、高性能电气绝缘材料的需求将会增加。

COVID-19大流行对包括汽车硅胶行业在内的各个行业产生了积极和消极的影响。疫情扰乱了全球供应链,影响了汽车生产所需的原料、设备和零件的供应。这阻碍了全球汽车生产。在疫情爆发阶段,由于关门、旅游限制和经济不确定性,汽车产业的需求大幅下降。此外,汽车减少了产量,导致对汽车有机硅和其他相关材料的需求减少。

目录

第1章简介

第2章执行摘要

第3章市场概况

- 市场定义和范围

- 主要发现

- 影响要素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 抑制因素

- 机会

- COVID-19 市场影响分析

- 市场占有率分析

- 价值链分析

- 法规指引

- 关键法规分析

- 专利形势

第4章汽车硅胶市场:依类型

- 概述

- 弹性体

- 树脂

- 凝胶

- 其他的

第5章汽车硅胶市场:依用途

- 概述

- 外装

- 引擎

- 电子系统

- 其他的

第6章汽车硅胶市场:依地区划分

- 概述

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 法国

- 德国

- 义大利

- 西班牙

- 英国

- 其他的

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他的

- 拉丁美洲/中东/非洲

- 巴西

- 摩洛哥

- 南非

- 阿根廷

- 其他的

第7章竞争形势

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争仪表板

- 竞争热图

- 2022年主要企业定位

第8章公司简介

- Shin Etsu

- Wacker Chemie

- Siltech Corporation

- Elkem ASA

- Momentive

- Primasil Silicones

- Dowdupont

- Evonik

- KCC Corporation

- Henkel AG & Co

According to a new report published by Allied Market Research, titled, "Automotive Silicone Market," The automotive silicone market was valued at $2.7 billion in 2022, and is estimated to reach $6.1 billion by 2032, growing at a CAGR of 8.5% from 2023 to 2032.

Automotive silicone is a specific type of silicone material that is majorly designed for use in automotive applications. Silicone is a flexible polymer renowned for its excellent electrical insulation properties, temperature resistance, and durability. In the automotive industry, silicone is majorly used owing to its unique properties and benefits. The temperature resistance property of silicone can withstand extreme temperatures, both high and low, without losing its physical properties. It remains stable and flexible across an extensive temperature range, making it appropriate for automotive applications.

Automotive weight reduction is a constant goal for automakers as they seek to improve overall performance and fuel economy. Vehicle design is increasingly incorporating lightweight components including carbon fiber composites, high-strength steel, aluminum, and plastics. Because they may replace heavy materials and have a low density, silicone-based materials including adhesives, silicone foams, and sealants are a crucial step in the process of making automotive products lighter. These lightweight silicone materials are opted in various applications, such as seals, gaskets, electrical components, and thermal management systems, to reduce overall vehicle weight. Silicone-based adhesives, sealants, and gaskets are used in powertrain components, including transmissions, engines, and exhaust systems, to improve performance and reduce energy losses.

Silicon is a non-renewable resource that is used to make automotive silicone, and the procedures used to make silicone consume a lot of energy. In addition, silicone products are not easily biodegradable, leading to possible waste management challenges. As governments and regulatory bodies implement strict environmental regulations, automotive manufactures may face consequences and can diverge towards using more sustainable materials in comparison to silicone. Volatile organic compounds (VOCs) can be discharged as a result of the usage and manufacture of products with silicone as a base. VOCs are dangerous compounds that can harm human health and contribute to air pollution. Limits on VOC emissions are frequently imposed by stringent environmental laws, which may have an effect on the creation and application of automotive silicone. Moreover, the growing emphasis on sustainability has increased the demand for eco-friendly alternatives to silicone. The automotive industry is exploring and adopting greener solutions such as bio-based polymers and recyclable materials to reduce their environmental footprints. This is expected to restrain market growth during the forecast period.

As electric vehicle production surges globally, the demand for silicone-based materials is expected to surge. This provides an opportunity for automotive silicone manufacturers to develop innovative solutions, increase their product offerings, and cater to the specific needs of the EV industry. Electric vehicles generate heat during operation, particularly in the battery and powertrain systems. Silicone-based thermal management solutions, such as gels, thermal interface materials, and adhesives, can effectively manage and dissipate heat, ensuring ideal performance and safety of EV components. Moreover, silicone materials possess excellent electrical insulation properties, making them suitable for applications like cable and wire insulation, connectors, and gaskets in electric vehicles. As Evs incorporate advanced electronics and electrical systems, the demand for reliable and high-performance electrical insulation materials will increase.

The COVID-19 pandemic had both positive and negative impacts on various industries, including the automotive silicone industry. The pandemic caused disruptions in global supply chains, affecting the availability of raw materials, equipment, and components necessary for automotive production. This hampered the production of automotive globally. The automotive industry experienced a significant decline in demand during the initial stage of the pandemic owing to lockdowns, travel restrictions, and economic instability. Moreover, as a result automotive manufacturers scaled back production, leading to reduced demand for automotive silicone and other related materials.

The key players profiled in this report include: Shin Etsu, Wacker Chemie, Siltech, Elkem Silicones, Momentive Performance Materials, Primasil Silicones, Dowdupont, Evonik, KCC Corporation, and Henkel AG & Co. The market players are continuously striving to achieve a dominant position in this competitive market using strategies such as collaborations and acquisitions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the automotive silicone market analysis from 2022 to 2032 to identify the prevailing automotive silicone market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the automotive silicone market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global automotive silicone market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 20% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline talk to the sales executive to know more)

- Investment Opportunities

- Technology Trend Analysis

- New Product Development/ Product Matrix of Key Players

- Regulatory Guidelines

- Strategic Recommedations

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Criss-cross segment analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- List of customers/consumers/raw material suppliers- value chain analysis

- SWOT Analysis

Key Market Segments

By Type

- Elastomers

- Resins

- Gels

- Others

By Application

- Interior and Exterior

- Engines

- Electrical Systems

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Morocco

- South Africa

- Argentina

- Rest of LAMEA

Key Market Players:

- Dowdupont

- Elkem ASA

- Evonik

- Henkel AG & Co

- KCC Corporation

- Momentive

- Primasil Silicones

- Shin Etsu

- Siltech Corporation

- Wacker Chemie

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research Methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. COVID-19 Impact Analysis on the market

- 3.6. Market Share Analysis

- 3.7. Value Chain Analysis

- 3.8. Regulatory Guidelines

- 3.9. Key Regulation Analysis

- 3.10. Patent Landscape

CHAPTER 4: AUTOMOTIVE SILICONE MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Elastomers

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Resins

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Gels

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Others

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

CHAPTER 5: AUTOMOTIVE SILICONE MARKET, BY APPLICATION

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Interior and Exterior

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Engines

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Electrical Systems

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Others

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

CHAPTER 6: AUTOMOTIVE SILICONE MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key trends and opportunities

- 6.2.2. Market size and forecast, by Type

- 6.2.3. Market size and forecast, by Application

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Key market trends, growth factors and opportunities

- 6.2.4.1.2. Market size and forecast, by Type

- 6.2.4.1.3. Market size and forecast, by Application

- 6.2.4.2. Canada

- 6.2.4.2.1. Key market trends, growth factors and opportunities

- 6.2.4.2.2. Market size and forecast, by Type

- 6.2.4.2.3. Market size and forecast, by Application

- 6.2.4.3. Mexico

- 6.2.4.3.1. Key market trends, growth factors and opportunities

- 6.2.4.3.2. Market size and forecast, by Type

- 6.2.4.3.3. Market size and forecast, by Application

- 6.3. Europe

- 6.3.1. Key trends and opportunities

- 6.3.2. Market size and forecast, by Type

- 6.3.3. Market size and forecast, by Application

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. France

- 6.3.4.1.1. Key market trends, growth factors and opportunities

- 6.3.4.1.2. Market size and forecast, by Type

- 6.3.4.1.3. Market size and forecast, by Application

- 6.3.4.2. Germany

- 6.3.4.2.1. Key market trends, growth factors and opportunities

- 6.3.4.2.2. Market size and forecast, by Type

- 6.3.4.2.3. Market size and forecast, by Application

- 6.3.4.3. Italy

- 6.3.4.3.1. Key market trends, growth factors and opportunities

- 6.3.4.3.2. Market size and forecast, by Type

- 6.3.4.3.3. Market size and forecast, by Application

- 6.3.4.4. Spain

- 6.3.4.4.1. Key market trends, growth factors and opportunities

- 6.3.4.4.2. Market size and forecast, by Type

- 6.3.4.4.3. Market size and forecast, by Application

- 6.3.4.5. UK

- 6.3.4.5.1. Key market trends, growth factors and opportunities

- 6.3.4.5.2. Market size and forecast, by Type

- 6.3.4.5.3. Market size and forecast, by Application

- 6.3.4.6. Rest of Europe

- 6.3.4.6.1. Key market trends, growth factors and opportunities

- 6.3.4.6.2. Market size and forecast, by Type

- 6.3.4.6.3. Market size and forecast, by Application

- 6.4. Asia-Pacific

- 6.4.1. Key trends and opportunities

- 6.4.2. Market size and forecast, by Type

- 6.4.3. Market size and forecast, by Application

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Key market trends, growth factors and opportunities

- 6.4.4.1.2. Market size and forecast, by Type

- 6.4.4.1.3. Market size and forecast, by Application

- 6.4.4.2. Japan

- 6.4.4.2.1. Key market trends, growth factors and opportunities

- 6.4.4.2.2. Market size and forecast, by Type

- 6.4.4.2.3. Market size and forecast, by Application

- 6.4.4.3. India

- 6.4.4.3.1. Key market trends, growth factors and opportunities

- 6.4.4.3.2. Market size and forecast, by Type

- 6.4.4.3.3. Market size and forecast, by Application

- 6.4.4.4. South Korea

- 6.4.4.4.1. Key market trends, growth factors and opportunities

- 6.4.4.4.2. Market size and forecast, by Type

- 6.4.4.4.3. Market size and forecast, by Application

- 6.4.4.5. Australia

- 6.4.4.5.1. Key market trends, growth factors and opportunities

- 6.4.4.5.2. Market size and forecast, by Type

- 6.4.4.5.3. Market size and forecast, by Application

- 6.4.4.6. Rest of Asia-Pacific

- 6.4.4.6.1. Key market trends, growth factors and opportunities

- 6.4.4.6.2. Market size and forecast, by Type

- 6.4.4.6.3. Market size and forecast, by Application

- 6.5. LAMEA

- 6.5.1. Key trends and opportunities

- 6.5.2. Market size and forecast, by Type

- 6.5.3. Market size and forecast, by Application

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Key market trends, growth factors and opportunities

- 6.5.4.1.2. Market size and forecast, by Type

- 6.5.4.1.3. Market size and forecast, by Application

- 6.5.4.2. Morocco

- 6.5.4.2.1. Key market trends, growth factors and opportunities

- 6.5.4.2.2. Market size and forecast, by Type

- 6.5.4.2.3. Market size and forecast, by Application

- 6.5.4.3. South Africa

- 6.5.4.3.1. Key market trends, growth factors and opportunities

- 6.5.4.3.2. Market size and forecast, by Type

- 6.5.4.3.3. Market size and forecast, by Application

- 6.5.4.4. Argentina

- 6.5.4.4.1. Key market trends, growth factors and opportunities

- 6.5.4.4.2. Market size and forecast, by Type

- 6.5.4.4.3. Market size and forecast, by Application

- 6.5.4.5. Rest of LAMEA

- 6.5.4.5.1. Key market trends, growth factors and opportunities

- 6.5.4.5.2. Market size and forecast, by Type

- 6.5.4.5.3. Market size and forecast, by Application

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product Mapping of Top 10 Player

- 7.4. Competitive Dashboard

- 7.5. Competitive Heatmap

- 7.6. Top player positioning, 2022

CHAPTER 8: COMPANY PROFILES

- 8.1. Shin Etsu

- 8.1.1. Company overview

- 8.1.2. Key Executives

- 8.1.3. Company snapshot

- 8.2. Wacker Chemie

- 8.2.1. Company overview

- 8.2.2. Key Executives

- 8.2.3. Company snapshot

- 8.3. Siltech Corporation

- 8.3.1. Company overview

- 8.3.2. Key Executives

- 8.3.3. Company snapshot

- 8.4. Elkem ASA

- 8.4.1. Company overview

- 8.4.2. Key Executives

- 8.4.3. Company snapshot

- 8.5. Momentive

- 8.5.1. Company overview

- 8.5.2. Key Executives

- 8.5.3. Company snapshot

- 8.6. Primasil Silicones

- 8.6.1. Company overview

- 8.6.2. Key Executives

- 8.6.3. Company snapshot

- 8.7. Dowdupont

- 8.7.1. Company overview

- 8.7.2. Key Executives

- 8.7.3. Company snapshot

- 8.8. Evonik

- 8.8.1. Company overview

- 8.8.2. Key Executives

- 8.8.3. Company snapshot

- 8.9. KCC Corporation

- 8.9.1. Company overview

- 8.9.2. Key Executives

- 8.9.3. Company snapshot

- 8.10. Henkel AG & Co

- 8.10.1. Company overview

- 8.10.2. Key Executives

- 8.10.3. Company snapshot

LIST OF TABLES

- TABLE 01. GLOBAL AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 02. AUTOMOTIVE SILICONE MARKET FOR ELASTOMERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. AUTOMOTIVE SILICONE MARKET FOR RESINS, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. AUTOMOTIVE SILICONE MARKET FOR GELS, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. AUTOMOTIVE SILICONE MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. GLOBAL AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 07. AUTOMOTIVE SILICONE MARKET FOR INTERIOR AND EXTERIOR, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. AUTOMOTIVE SILICONE MARKET FOR ENGINES, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. AUTOMOTIVE SILICONE MARKET FOR ELECTRICAL SYSTEMS, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. AUTOMOTIVE SILICONE MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. AUTOMOTIVE SILICONE MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. NORTH AMERICA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 13. NORTH AMERICA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 14. NORTH AMERICA AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 15. U.S. AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 16. U.S. AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 17. CANADA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 18. CANADA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 19. MEXICO AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 20. MEXICO AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 21. EUROPE AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 22. EUROPE AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 23. EUROPE AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 24. FRANCE AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 25. FRANCE AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 26. GERMANY AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 27. GERMANY AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 28. ITALY AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 29. ITALY AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 30. SPAIN AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 31. SPAIN AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 32. UK AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 33. UK AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 34. REST OF EUROPE AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 35. REST OF EUROPE AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 36. ASIA-PACIFIC AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 37. ASIA-PACIFIC AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 38. ASIA-PACIFIC AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 39. CHINA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 40. CHINA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 41. JAPAN AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 42. JAPAN AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 43. INDIA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 44. INDIA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 45. SOUTH KOREA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 46. SOUTH KOREA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 47. AUSTRALIA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 48. AUSTRALIA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 49. REST OF ASIA-PACIFIC AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 50. REST OF ASIA-PACIFIC AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 51. LAMEA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 52. LAMEA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 53. LAMEA AUTOMOTIVE SILICONE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 54. BRAZIL AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 55. BRAZIL AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 56. MOROCCO AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 57. MOROCCO AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 58. SOUTH AFRICA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 59. SOUTH AFRICA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 60. ARGENTINA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 61. ARGENTINA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 62. REST OF LAMEA AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 63. REST OF LAMEA AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 64. SHIN ETSU: KEY EXECUTIVES

- TABLE 65. SHIN ETSU: COMPANY SNAPSHOT

- TABLE 66. WACKER CHEMIE: KEY EXECUTIVES

- TABLE 67. WACKER CHEMIE: COMPANY SNAPSHOT

- TABLE 68. SILTECH CORPORATION: KEY EXECUTIVES

- TABLE 69. SILTECH CORPORATION: COMPANY SNAPSHOT

- TABLE 70. ELKEM ASA: KEY EXECUTIVES

- TABLE 71. ELKEM ASA: COMPANY SNAPSHOT

- TABLE 72. MOMENTIVE: KEY EXECUTIVES

- TABLE 73. MOMENTIVE: COMPANY SNAPSHOT

- TABLE 74. PRIMASIL SILICONES: KEY EXECUTIVES

- TABLE 75. PRIMASIL SILICONES: COMPANY SNAPSHOT

- TABLE 76. DOWDUPONT: KEY EXECUTIVES

- TABLE 77. DOWDUPONT: COMPANY SNAPSHOT

- TABLE 78. EVONIK: KEY EXECUTIVES

- TABLE 79. EVONIK: COMPANY SNAPSHOT

- TABLE 80. KCC CORPORATION: KEY EXECUTIVES

- TABLE 81. KCC CORPORATION: COMPANY SNAPSHOT

- TABLE 82. HENKEL AG & CO: KEY EXECUTIVES

- TABLE 83. HENKEL AG & CO: COMPANY SNAPSHOT

LIST OF FIGURES

- FIGURE 01. AUTOMOTIVE SILICONE MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF AUTOMOTIVE SILICONE MARKET, 2022-2032

- FIGURE 03. AUTOMOTIVE SILICONE MARKET,2022-2032

- FIGURE 04. TOP INVESTMENT POCKETS IN AUTOMOTIVE SILICONE MARKET (2023-2032)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL AUTOMOTIVE SILICONE MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. REGULATORY GUIDELINES: AUTOMOTIVE SILICONE MARKET

- FIGURE 12. IMPACT OF KEY REGULATION: AUTOMOTIVE SILICONE MARKET

- FIGURE 13. PATENT ANALYSIS BY COMPANY

- FIGURE 14. PATENT ANALYSIS BY COUNTRY

- FIGURE 15. AUTOMOTIVE SILICONE MARKET, BY TYPE, 2022(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR ELASTOMERS, BY COUNTRY 2022-2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR RESINS, BY COUNTRY 2022-2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR GELS, BY COUNTRY 2022-2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR OTHERS, BY COUNTRY 2022-2032(%)

- FIGURE 20. AUTOMOTIVE SILICONE MARKET, BY APPLICATION, 2022(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR INTERIOR AND EXTERIOR, BY COUNTRY 2022-2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR ENGINES, BY COUNTRY 2022-2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR ELECTRICAL SYSTEMS, BY COUNTRY 2022-2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF AUTOMOTIVE SILICONE MARKET FOR OTHERS, BY COUNTRY 2022-2032(%)

- FIGURE 25. AUTOMOTIVE SILICONE MARKET BY REGION, 2022

- FIGURE 26. U.S. AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 27. CANADA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 28. MEXICO AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 29. FRANCE AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 30. GERMANY AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 31. ITALY AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 32. SPAIN AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 33. UK AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 34. REST OF EUROPE AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 35. CHINA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 36. JAPAN AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 37. INDIA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 38. SOUTH KOREA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 39. AUSTRALIA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 40. REST OF ASIA-PACIFIC AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 41. BRAZIL AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 42. MOROCCO AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 43. SOUTH AFRICA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 44. ARGENTINA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 45. REST OF LAMEA AUTOMOTIVE SILICONE MARKET, 2022-2032 ($MILLION)

- FIGURE 46. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 47. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 48. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 49. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 50. COMPETITIVE DASHBOARD

- FIGURE 51. COMPETITIVE HEATMAP: AUTOMOTIVE SILICONE MARKET

- FIGURE 52. TOP PLAYER POSITIONING, 2022

2025年全球硅胶(不含树脂)市场报告

2025年全球硅胶(不含树脂)市场报告 硅胶:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

硅胶:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 水性硅胶市场规模、份额、趋势分析报告:按类型、应用、最终用途、地区、细分市场预测,2025-2030 年

水性硅胶市场规模、份额、趋势分析报告:按类型、应用、最终用途、地区、细分市场预测,2025-2030 年 全球汽车硅胶市场报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年2025 年全球汽车硅胶市场报告2025 年电气和电子产品全球硅胶市场报告汽车护理产品中硅胶的市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测,2025-2030 年

全球汽车硅胶市场报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年2025 年全球汽车硅胶市场报告2025 年电气和电子产品全球硅胶市场报告汽车护理产品中硅胶的市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测,2025-2030 年 医用级硅胶市场报告:2031 年趋势、预测与竞争分析2025 年全球重型机械硅胶市场报告

医用级硅胶市场报告:2031 年趋势、预测与竞争分析2025 年全球重型机械硅胶市场报告 2025 年至 2033 年期间硅胶市场报告,按产品类型(弹性体、流体、凝胶、树脂)、应用(工业流程、建筑材料、家庭和个人护理、交通运输、能源、医疗保健、电子等)和地区划分

2025 年至 2033 年期间硅胶市场报告,按产品类型(弹性体、流体、凝胶、树脂)、应用(工业流程、建筑材料、家庭和个人护理、交通运输、能源、医疗保健、电子等)和地区划分