|

市场调查报告书

商品编码

1414704

全球肾臟和泌尿系统设备市场:按产品、应用和最终用户:机会分析和产业预测(2023-2032)Nephrology and Urology Devices Market By Product, By Applications, By End User : Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

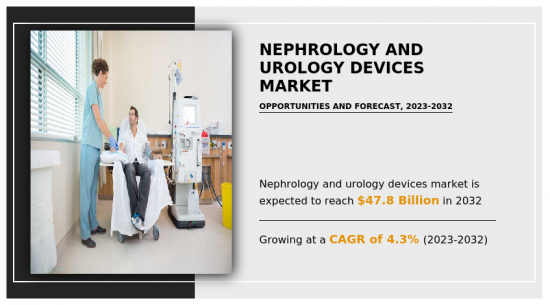

预计2022年全球肾臟和泌尿系统设备市场规模将达313亿美元,2023年至2032年复合年增长率为4.3%,2032年将达478亿美元。

肾臟和泌尿系统设备是专门设计用于诊断、监测和治疗肾臟和泌尿道相关疾病的医疗设备和装置。这些设备在肾臟病学/泌尿器官系统领域发挥着重要作用,肾臟病学/泌尿学是专注于研究和治疗肾臟和泌尿系统系统疾病的医学专业。肾臟病设备包括血液透析机机、腹膜透析设备、监测和维持透析血管通路的设备以及评估肾功能和相关参数的诊断工具。泌尿系统设备包括导尿管、泌尿系统内视镜、尿道支架、肾结石治疗碎石机、尿液动力学检测设备等。

由于肾臟疾病、尿道感染、肾结石和其他泌尿系统系统疾病的盛行率不断上升,肾臟和泌尿系统设备市场正在显着增长,这是肾臟和泌尿系统设备市场的关键驱动因素。此外,技术进步正在开发更有效率、侵入性更小的泌尿系统和肾臟病手术设备。这包括改进的影像技术、机器人手术以及用于治疗肾结石的碎石机等创新设备。此外,肾臟病学和泌尿系统向微创手术的转变进一步推动了市场成长。

内视镜、雷射系统和腹腔镜器械等设备因其恢復时间更快和併发症风险更低而需求量很大。

然而,泌尿系统设备的高成本,如输尿管镜和输尿管镜的临床障碍以及感染风险,是全球肾臟和泌尿系统设备市场的抑制因素。相反,医疗保健支出的增加和技术进步的不断发展预计将为市场成长创造有利可图的机会。

肾臟和泌尿系统设备市场分为产品、应用、最终用户和地区。依产品分为设备和耗材/配件。设备领域进一步分为透析设备、内视镜、雷射碾碎、内视镜成像系统等。透析设备又分为血液透析机机和腹膜透析设备。内视镜分为膀胱镜、输尿管镜等。耗材及配件细分市场进一步分为透析耗材、导管及导管导引线、支架、切片检查装置等。依用途分为肾臟病、泌尿系统癌/BPH等。依最终用户分为医院、透析中心等。

目录

第一章简介

第 2 章执行摘要

第三章市场概况

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 肾臟和泌尿系统疾病盛行率上升

- 科技进步快速提升

- 对微创医疗程序的需求不断增长

- 抑制因素

- 泌尿系统设备高成本

- 机会

- 新兴市场的成长机会

- 促进因素

第四章肾臟和泌尿系统设备市场:副产品

- 概述

- 装置

- 耗材及配件

第五章肾臟及泌尿系统设备市场:依应用分类

- 概述

- 肾臟疾病

- 泌尿系统癌症/良性摄护腺增生

- 其他的

第六章肾臟和泌尿系统设备市场:依最终用户分类

- 概述

- 医院

- 透析中心

- 其他的

第七章肾臟和泌尿系统设备市场:按地区

- 概述

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 其他的

- 亚太地区

- 日本

- 中国

- 印度

- 澳洲

- 韩国

- 其他的

- 拉丁美洲/中东/非洲

- 巴西

- 沙乌地阿拉伯

- 南非

- 其他的

第八章 竞争形势

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争对手仪表板

- 竞争热图

- 主要企业定位(2022年)

第九章 公司简介

- Medtronic plc

- Boston Scientific Corporation

- B. Braun SE

- Baxter International Inc.

- Coloplast

- Olympus Corporation

- Stryker Corporation.

- Teleflex Incorporated

- Becton, Dickinson and Company

- Karl Storz GmbH & Co. KG

According to a new report published by Allied Market Research, titled, "Nephrology and Urology Devices Market," The nephrology and urology devices market was valued at $31.3 billion in 2022, and is estimated to reach $47.8 billion by 2032, growing at a CAGR of 4.3% from 2023 to 2032.

Nephrology and urology devices are medical devices & equipment designed specifically for diagnosing, monitoring, & treating conditions related to the kidneys & the urinary tract. These devices play a crucial role in the fields of nephrology and urology, which are medical specialties focused on the study & treatment of kidney and urinary system disorders. Nephrology devices include hemodialysis & peritoneal dialysis machines, devices for monitoring & maintaining vascular access for dialysis, as well as diagnostic tools for evaluating kidney function and related parameters. Urological devices include urinary catheters, urological endoscopes, urinary stents, lithotripters for kidney stone treatment, and equipment for urodynamic testing, among others.

The nephrology and urology devices market has experienced significant growth owing to rise in incidence of kidney diseases, urinary tract infections, kidney stones, and other urological conditions is a significant driver for the nephrology and urology devices market. In addition, ongoing technological advancements have led to the development of more efficient and minimally invasive devices for urological and nephrological procedures. This includes improved imaging techniques, robotic surgery, and innovative devices like lithotripters for kidney stone treatment. Furthermore, shift toward minimally invasive procedures in nephrology and urology further drives the market growth. Devices such as

1) endoscopes, laser systems, and laparoscopic instruments are in demand due to their reduced recovery times and lower risk of complications.

However, the high cost associated with urology devices such as

1) ureteroscopes, clinical barriers for ureteroscopes, and risk of infection act as restraints for the global nephrology and urology devices market. Conversely, an increase in healthcare expenditure and rise in technological advancements are expected to create lucrative opportunities for the growth of the market.

The nephrology and urology devices market is segmented into product, application, end user, and region. By product, the market is segregated into instruments and consumables & accessories. The instruments segment is further categorized into dialysis device, endoscopes, laser & lithotripsy devices, endovision & imaging system, and others. Dialysis device segment is further bifurcated into hemodialysis device and peritoneal dialysis device. Endoscopes segment classified into cystoscopes, ureteroscopes, and others. The consumables & accessories segment is further categorized into dialysis consumables, catheters & guidewires, stents, biopsy devices, and others. On the basis of application, the market is categorized into kidney diseases, urological cancer & BPH, and others. As per end user, it is classified into hospitals, dialysis centers, and others.

Region wise, the market is analyzed across North America (the U.S., Canada, and Mexico), Europe (Germany, France, the UK, Italy, Spain, and rest of Europe), Asia-Pacific (Japan, China, Australia, India, South Korea, and rest of Asia-Pacific), and LAMEA (Brazil, Saudi Arabia, South Africa, and rest of LAMEA).

Major key players that operate in the nephrology and urology devices market are Medtronic plc, Boston Scientific Corporation, B. Braun SE, Baxter International Inc., Coloplast, Olympus Corporation, Stryker Corporation, Teleflex Incorporated, Becton, Dickinson and Company, and Karl Storz GmbH & Co. KG. Key players have adopted product launch, product approval, acquisition, agreement, and partnership as key developmental strategies to improve the product portfolio of the nephrology and urology devices market.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the nephrology and urology devices market analysis from 2022 to 2032 to identify the prevailing nephrology and urology devices market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the nephrology and urology devices market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global nephrology and urology devices market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Additional company profiles with specific to client's interest

- Expanded list for Company Profiles

- Historic market data

Key Market Segments

By Product

- Instruments

- Type

- Dialysis Devices

Type

- Endoscopes

Type

- Laser and Lithotripsy Devices

- Endovision and Imaging Systems

- Others

- Consumables and Accessories

- Type

- Dialysis Consumables

- Catheters and Guidewires

- Stents

- Biopsy devices

- Others

By Applications

- Kidney Diseases

- Urological Cancer and BPH

- Others

By End User

- Hospitals

- Dialysis Centers

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- Japan

- China

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- South Africa

- Rest of LAMEA

Key Market Players:

- B. Braun SE

- Coloplast

- Olympus Corporation

- Stryker Corporation.

- Becton, Dickinson and Company

- Karl Storz GmbH & Co. KG

- Boston Scientific Corporation

- Baxter International Inc.

- Teleflex Incorporated

- Medtronic plc

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.3.1. Moderate bargaining power of suppliers

- 3.3.2. Low threat of new entrants

- 3.3.3. Low threat of substitutes

- 3.3.4. Low intensity of rivalry

- 3.3.5. Moderate bargaining power of buyers

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.1.1. Rise in prevalence of kidney and urological disorders

- 3.4.1.2. Surge in technological advancements

- 3.4.1.3. Rise in demand for minimally invasive medical procedures

- 3.4.2. Restraints

- 3.4.2.1. High cost of urology devices

- 3.4.3. Opportunities

- 3.4.3.1. Growth opportunities in emerging markets

- 3.4.1. Drivers

CHAPTER 4: NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Instruments

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.2.4. Instruments Nephrology and Urology Devices Market by Type

- 4.2.4.1. Dialysis Devices Nephrology and Urology Devices Market by Type

- 4.2.4.2. Endoscopes Nephrology and Urology Devices Market by Type

- 4.3. Consumables and Accessories

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.3.4. Consumables and Accessories Nephrology and Urology Devices Market by Type

CHAPTER 5: NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Kidney Diseases

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Urological Cancer and BPH

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Others

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

CHAPTER 6: NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Hospitals

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Dialysis Centers

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Others

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: NEPHROLOGY AND UROLOGY DEVICES MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by Product

- 7.2.3. Market size and forecast, by Applications

- 7.2.4. Market size and forecast, by End User

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Market size and forecast, by Product

- 7.2.5.1.2. Market size and forecast, by Applications

- 7.2.5.1.3. Market size and forecast, by End User

- 7.2.5.2. Canada

- 7.2.5.2.1. Market size and forecast, by Product

- 7.2.5.2.2. Market size and forecast, by Applications

- 7.2.5.2.3. Market size and forecast, by End User

- 7.2.5.3. Mexico

- 7.2.5.3.1. Market size and forecast, by Product

- 7.2.5.3.2. Market size and forecast, by Applications

- 7.2.5.3.3. Market size and forecast, by End User

- 7.3. Europe

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by Product

- 7.3.3. Market size and forecast, by Applications

- 7.3.4. Market size and forecast, by End User

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Market size and forecast, by Product

- 7.3.5.1.2. Market size and forecast, by Applications

- 7.3.5.1.3. Market size and forecast, by End User

- 7.3.5.2. France

- 7.3.5.2.1. Market size and forecast, by Product

- 7.3.5.2.2. Market size and forecast, by Applications

- 7.3.5.2.3. Market size and forecast, by End User

- 7.3.5.3. UK

- 7.3.5.3.1. Market size and forecast, by Product

- 7.3.5.3.2. Market size and forecast, by Applications

- 7.3.5.3.3. Market size and forecast, by End User

- 7.3.5.4. Italy

- 7.3.5.4.1. Market size and forecast, by Product

- 7.3.5.4.2. Market size and forecast, by Applications

- 7.3.5.4.3. Market size and forecast, by End User

- 7.3.5.5. Spain

- 7.3.5.5.1. Market size and forecast, by Product

- 7.3.5.5.2. Market size and forecast, by Applications

- 7.3.5.5.3. Market size and forecast, by End User

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Market size and forecast, by Product

- 7.3.5.6.2. Market size and forecast, by Applications

- 7.3.5.6.3. Market size and forecast, by End User

- 7.4. Asia-Pacific

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by Product

- 7.4.3. Market size and forecast, by Applications

- 7.4.4. Market size and forecast, by End User

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. Japan

- 7.4.5.1.1. Market size and forecast, by Product

- 7.4.5.1.2. Market size and forecast, by Applications

- 7.4.5.1.3. Market size and forecast, by End User

- 7.4.5.2. China

- 7.4.5.2.1. Market size and forecast, by Product

- 7.4.5.2.2. Market size and forecast, by Applications

- 7.4.5.2.3. Market size and forecast, by End User

- 7.4.5.3. India

- 7.4.5.3.1. Market size and forecast, by Product

- 7.4.5.3.2. Market size and forecast, by Applications

- 7.4.5.3.3. Market size and forecast, by End User

- 7.4.5.4. Australia

- 7.4.5.4.1. Market size and forecast, by Product

- 7.4.5.4.2. Market size and forecast, by Applications

- 7.4.5.4.3. Market size and forecast, by End User

- 7.4.5.5. South Korea

- 7.4.5.5.1. Market size and forecast, by Product

- 7.4.5.5.2. Market size and forecast, by Applications

- 7.4.5.5.3. Market size and forecast, by End User

- 7.4.5.6. Rest of Asia-Pacific

- 7.4.5.6.1. Market size and forecast, by Product

- 7.4.5.6.2. Market size and forecast, by Applications

- 7.4.5.6.3. Market size and forecast, by End User

- 7.5. LAMEA

- 7.5.1. Key market trends, growth factors and opportunities

- 7.5.2. Market size and forecast, by Product

- 7.5.3. Market size and forecast, by Applications

- 7.5.4. Market size and forecast, by End User

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Market size and forecast, by Product

- 7.5.5.1.2. Market size and forecast, by Applications

- 7.5.5.1.3. Market size and forecast, by End User

- 7.5.5.2. Saudi Arabia

- 7.5.5.2.1. Market size and forecast, by Product

- 7.5.5.2.2. Market size and forecast, by Applications

- 7.5.5.2.3. Market size and forecast, by End User

- 7.5.5.3. South Africa

- 7.5.5.3.1. Market size and forecast, by Product

- 7.5.5.3.2. Market size and forecast, by Applications

- 7.5.5.3.3. Market size and forecast, by End User

- 7.5.5.4. Rest of LAMEA

- 7.5.5.4.1. Market size and forecast, by Product

- 7.5.5.4.2. Market size and forecast, by Applications

- 7.5.5.4.3. Market size and forecast, by End User

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product mapping of top 10 player

- 8.4. Competitive dashboard

- 8.5. Competitive heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. Medtronic plc

- 9.1.1. Company overview

- 9.1.2. Key executives

- 9.1.3. Company snapshot

- 9.1.4. Operating business segments

- 9.1.5. Product portfolio

- 9.1.6. Business performance

- 9.1.7. Key strategic moves and developments

- 9.2. Boston Scientific Corporation

- 9.2.1. Company overview

- 9.2.2. Key executives

- 9.2.3. Company snapshot

- 9.2.4. Operating business segments

- 9.2.5. Product portfolio

- 9.2.6. Business performance

- 9.2.7. Key strategic moves and developments

- 9.3. B. Braun SE

- 9.3.1. Company overview

- 9.3.2. Key executives

- 9.3.3. Company snapshot

- 9.3.4. Operating business segments

- 9.3.5. Product portfolio

- 9.3.6. Business performance

- 9.4. Baxter International Inc.

- 9.4.1. Company overview

- 9.4.2. Key executives

- 9.4.3. Company snapshot

- 9.4.4. Operating business segments

- 9.4.5. Product portfolio

- 9.4.6. Business performance

- 9.4.7. Key strategic moves and developments

- 9.5. Coloplast

- 9.5.1. Company overview

- 9.5.2. Key executives

- 9.5.3. Company snapshot

- 9.5.4. Operating business segments

- 9.5.5. Product portfolio

- 9.5.6. Business performance

- 9.5.7. Key strategic moves and developments

- 9.6. Olympus Corporation

- 9.6.1. Company overview

- 9.6.2. Key executives

- 9.6.3. Company snapshot

- 9.6.4. Operating business segments

- 9.6.5. Product portfolio

- 9.6.6. Business performance

- 9.6.7. Key strategic moves and developments

- 9.7. Stryker Corporation.

- 9.7.1. Company overview

- 9.7.2. Key executives

- 9.7.3. Company snapshot

- 9.7.4. Operating business segments

- 9.7.5. Product portfolio

- 9.7.6. Business performance

- 9.8. Teleflex Incorporated

- 9.8.1. Company overview

- 9.8.2. Key executives

- 9.8.3. Company snapshot

- 9.8.4. Operating business segments

- 9.8.5. Product portfolio

- 9.8.6. Business performance

- 9.8.7. Key strategic moves and developments

- 9.9. Becton, Dickinson and Company

- 9.9.1. Company overview

- 9.9.2. Key executives

- 9.9.3. Company snapshot

- 9.9.4. Operating business segments

- 9.9.5. Product portfolio

- 9.9.6. Business performance

- 9.9.7. Key strategic moves and developments

- 9.10. Karl Storz GmbH & Co. KG

- 9.10.1. Company overview

- 9.10.2. Key executives

- 9.10.3. Company snapshot

- 9.10.4. Operating business segments

- 9.10.5. Product portfolio

LIST OF TABLES

- TABLE 01. GLOBAL NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 02. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR INSTRUMENTS, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. GLOBAL INSTRUMENTS NEPHROLOGY AND UROLOGY DEVICES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL DIALYSIS DEVICES NEPHROLOGY AND UROLOGY DEVICES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 05. GLOBAL ENDOSCOPES NEPHROLOGY AND UROLOGY DEVICES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 06. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR CONSUMABLES AND ACCESSORIES, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL CONSUMABLES AND ACCESSORIES NEPHROLOGY AND UROLOGY DEVICES MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 08. GLOBAL NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 09. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR KIDNEY DISEASES, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR UROLOGICAL CANCER AND BPH, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. GLOBAL NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 13. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR HOSPITALS, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR DIALYSIS CENTERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 15. NEPHROLOGY AND UROLOGY DEVICES MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 16. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 18. NORTH AMERICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 19. NORTH AMERICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 20. NORTH AMERICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 21. U.S. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 22. U.S. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 23. U.S. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 24. CANADA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 25. CANADA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 26. CANADA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 27. MEXICO NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 28. MEXICO NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 29. MEXICO NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 30. EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 31. EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 32. EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 33. EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 34. GERMANY NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 35. GERMANY NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 36. GERMANY NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 37. FRANCE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 38. FRANCE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 39. FRANCE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 40. UK NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 41. UK NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 42. UK NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 43. ITALY NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 44. ITALY NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 45. ITALY NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 46. SPAIN NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 47. SPAIN NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 48. SPAIN NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 49. REST OF EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 50. REST OF EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 51. REST OF EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 52. ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 53. ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 54. ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 55. ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 56. JAPAN NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 57. JAPAN NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 58. JAPAN NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 59. CHINA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 60. CHINA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 61. CHINA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 62. INDIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 63. INDIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 64. INDIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 65. AUSTRALIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 66. AUSTRALIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 67. AUSTRALIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 68. SOUTH KOREA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 69. SOUTH KOREA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 70. SOUTH KOREA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 71. REST OF ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 72. REST OF ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 73. REST OF ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 74. LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 75. LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 76. LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 77. LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 78. BRAZIL NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 79. BRAZIL NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 80. BRAZIL NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 81. SAUDI ARABIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 82. SAUDI ARABIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 83. SAUDI ARABIA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 84. SOUTH AFRICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 85. SOUTH AFRICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 86. SOUTH AFRICA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 87. REST OF LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 88. REST OF LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022-2032 ($MILLION)

- TABLE 89. REST OF LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 90. MEDTRONIC PLC: KEY EXECUTIVES

- TABLE 91. MEDTRONIC PLC: COMPANY SNAPSHOT

- TABLE 92. MEDTRONIC PLC: PRODUCT SEGMENTS

- TABLE 93. MEDTRONIC PLC: PRODUCT PORTFOLIO

- TABLE 94. MEDTRONIC PLC: KEY STRATERGIES

- TABLE 95. BOSTON SCIENTIFIC CORPORATION: KEY EXECUTIVES

- TABLE 96. BOSTON SCIENTIFIC CORPORATION: COMPANY SNAPSHOT

- TABLE 97. BOSTON SCIENTIFIC CORPORATION: PRODUCT SEGMENTS

- TABLE 98. BOSTON SCIENTIFIC CORPORATION: PRODUCT PORTFOLIO

- TABLE 99. BOSTON SCIENTIFIC CORPORATION: KEY STRATERGIES

- TABLE 100. B. BRAUN SE: KEY EXECUTIVES

- TABLE 101. B. BRAUN SE: COMPANY SNAPSHOT

- TABLE 102. B. BRAUN SE: PRODUCT SEGMENTS

- TABLE 103. B. BRAUN SE: PRODUCT PORTFOLIO

- TABLE 104. BAXTER INTERNATIONAL INC.: KEY EXECUTIVES

- TABLE 105. BAXTER INTERNATIONAL INC.: COMPANY SNAPSHOT

- TABLE 106. BAXTER INTERNATIONAL INC.: PRODUCT SEGMENTS

- TABLE 107. BAXTER INTERNATIONAL INC.: PRODUCT PORTFOLIO

- TABLE 108. BAXTER INTERNATIONAL INC.: KEY STRATERGIES

- TABLE 109. COLOPLAST: KEY EXECUTIVES

- TABLE 110. COLOPLAST: COMPANY SNAPSHOT

- TABLE 111. COLOPLAST: PRODUCT SEGMENTS

- TABLE 112. COLOPLAST: PRODUCT PORTFOLIO

- TABLE 113. COLOPLAST: KEY STRATERGIES

- TABLE 114. OLYMPUS CORPORATION: KEY EXECUTIVES

- TABLE 115. OLYMPUS CORPORATION: COMPANY SNAPSHOT

- TABLE 116. OLYMPUS CORPORATION: PRODUCT SEGMENTS

- TABLE 117. OLYMPUS CORPORATION: PRODUCT PORTFOLIO

- TABLE 118. OLYMPUS CORPORATION: KEY STRATERGIES

- TABLE 119. STRYKER CORPORATION.: KEY EXECUTIVES

- TABLE 120. STRYKER CORPORATION.: COMPANY SNAPSHOT

- TABLE 121. STRYKER CORPORATION.: PRODUCT SEGMENTS

- TABLE 122. STRYKER CORPORATION.: PRODUCT PORTFOLIO

- TABLE 123. TELEFLEX INCORPORATED: KEY EXECUTIVES

- TABLE 124. TELEFLEX INCORPORATED: COMPANY SNAPSHOT

- TABLE 125. TELEFLEX INCORPORATED: PRODUCT SEGMENTS

- TABLE 126. TELEFLEX INCORPORATED: PRODUCT PORTFOLIO

- TABLE 127. TELEFLEX INCORPORATED: KEY STRATERGIES

- TABLE 128. BECTON, DICKINSON AND COMPANY: KEY EXECUTIVES

- TABLE 129. BECTON, DICKINSON AND COMPANY: COMPANY SNAPSHOT

- TABLE 130. BECTON, DICKINSON AND COMPANY: PRODUCT SEGMENTS

- TABLE 131. BECTON, DICKINSON AND COMPANY: PRODUCT PORTFOLIO

- TABLE 132. BECTON, DICKINSON AND COMPANY: KEY STRATERGIES

- TABLE 133. KARL STORZ GMBH & CO. KG: KEY EXECUTIVES

- TABLE 134. KARL STORZ GMBH & CO. KG: COMPANY SNAPSHOT

- TABLE 135. KARL STORZ GMBH & CO. KG: PRODUCT SEGMENTS

- TABLE 136. KARL STORZ GMBH & CO. KG: PRODUCT PORTFOLIO

LIST OF FIGURES

- FIGURE 01. NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF NEPHROLOGY AND UROLOGY DEVICES MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN NEPHROLOGY AND UROLOGY DEVICES MARKET (2022 TO 2032)

- FIGURE 04. TOP INVESTMENT POCKETS IN NEPHROLOGY AND UROLOGY DEVICES MARKET (2023-2032)

- FIGURE 05. MODERATE BARGAINING POWER OF SUPPLIERS

- FIGURE 06. LOW THREAT OF NEW ENTRANTS

- FIGURE 07. LOW THREAT OF SUBSTITUTES

- FIGURE 08. LOW INTENSITY OF RIVALRY

- FIGURE 09. MODERATE BARGAINING POWER OF BUYERS

- FIGURE 10. GLOBAL NEPHROLOGY AND UROLOGY DEVICES MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY PRODUCT, 2022 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR INSTRUMENTS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR CONSUMABLES AND ACCESSORIES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 14. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY APPLICATIONS, 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR KIDNEY DISEASES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR UROLOGICAL CANCER AND BPH, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. NEPHROLOGY AND UROLOGY DEVICES MARKET, BY END USER, 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR HOSPITALS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR DIALYSIS CENTERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF NEPHROLOGY AND UROLOGY DEVICES MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. NEPHROLOGY AND UROLOGY DEVICES MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 23. U.S. NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 24. CANADA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 25. MEXICO NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 26. GERMANY NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 27. FRANCE NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 28. UK NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 29. ITALY NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 30. SPAIN NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 31. REST OF EUROPE NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 32. JAPAN NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 33. CHINA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 34. INDIA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 35. AUSTRALIA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 36. SOUTH KOREA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 37. REST OF ASIA-PACIFIC NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 38. BRAZIL NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 39. SAUDI ARABIA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 40. SOUTH AFRICA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 41. REST OF LAMEA NEPHROLOGY AND UROLOGY DEVICES MARKET, 2022-2032 ($MILLION)

- FIGURE 42. TOP WINNING STRATEGIES, BY YEAR (2020-2023)

- FIGURE 43. TOP WINNING STRATEGIES, BY DEVELOPMENT (2020-2023)

- FIGURE 44. TOP WINNING STRATEGIES, BY COMPANY (2020-2023)

- FIGURE 45. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 46. COMPETITIVE DASHBOARD

- FIGURE 47. COMPETITIVE HEATMAP: NEPHROLOGY AND UROLOGY DEVICES MARKET

- FIGURE 48. TOP PLAYER POSITIONING, 2022

- FIGURE 49. MEDTRONIC PLC: NET SALES, 2021-2023 ($MILLION)

- FIGURE 50. MEDTRONIC PLC: REVENUE SHARE BY SEGMENT, 2023 (%)

- FIGURE 51. MEDTRONIC PLC: REVENUE SHARE BY REGION, 2023 (%)

- FIGURE 52. BOSTON SCIENTIFIC CORPORATION: NET SALES, 2020-2022 ($MILLION)

- FIGURE 53. BOSTON SCIENTIFIC CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 54. BOSTON SCIENTIFIC CORPORATION: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 55. B. BRAUN SE: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 56. B. BRAUN SE: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 57. B. BRAUN SE: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 58. BAXTER INTERNATIONAL INC.: NET SALES, 2020-2022 ($MILLION)

- FIGURE 59. BAXTER INTERNATIONAL INC.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 60. BAXTER INTERNATIONAL INC.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 61. COLOPLAST: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 62. COLOPLAST: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 63. COLOPLAST: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 64. OLYMPUS CORPORATION: NET REVENUE, 2021-2023 ($MILLION)

- FIGURE 65. OLYMPUS CORPORATION: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 66. STRYKER CORPORATION.: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 67. STRYKER CORPORATION.: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 68. STRYKER CORPORATION.: REVENUE SHARE BY REGION, 2022 (%)

- FIGURE 69. TELEFLEX INCORPORATED: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 70. TELEFLEX INCORPORATED: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 71. BECTON, DICKINSON AND COMPANY: NET REVENUE, 2020-2022 ($MILLION)

- FIGURE 72. BECTON, DICKINSON AND COMPANY: REVENUE SHARE BY SEGMENT, 2022 (%)

- FIGURE 73. BECTON, DICKINSON AND COMPANY: REVENUE SHARE BY REGION, 2022 (%)

2025年全球肾臟和泌尿系统设备市场报告

2025年全球肾臟和泌尿系统设备市场报告 肾臟和泌尿系统设备市场规模、份额和成长分析(按产品、应用和地区):产业预测(2024-2031)

肾臟和泌尿系统设备市场规模、份额和成长分析(按产品、应用和地区):产业预测(2024-2031) 肾臟病学和泌尿系统市场报告:2030 年趋势、预测和竞争分析

肾臟病学和泌尿系统市场报告:2030 年趋势、预测和竞争分析 泌尿外科器械市场:按手术类型、最终用户应用和地区划分,2024-2031 年

泌尿外科器械市场:按手术类型、最终用户应用和地区划分,2024-2031 年 肾臟和泌尿系统设备市场:按产品、应用和最终用户划分 - 全球预测 2025-2030 年肾臟病设备市场:按设备、设备类型、最终用户划分 - 全球预测 2025-2030

肾臟和泌尿系统设备市场:按产品、应用和最终用户划分 - 全球预测 2025-2030 年肾臟病设备市场:按设备、设备类型、最终用户划分 - 全球预测 2025-2030 肾臟和泌尿系统设备的全球市场规模、份额和行业趋势分析报告:按最终用途、应用、产品和地区分類的展望和预测(2023-2030)

肾臟和泌尿系统设备的全球市场规模、份额和行业趋势分析报告:按最终用途、应用、产品和地区分類的展望和预测(2023-2030) 肾臟科和泌尿系统设备市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测,2023-2030 年

肾臟科和泌尿系统设备市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测,2023-2030 年