|

市场调查报告书

商品编码

1414746

石膏和干墙市场:按产品、最终用户、厚度:2023-2032 年全球机会分析和产业预测Gypsum & Drywall Market By PRODUCT (Wallboard, Ceiling Board, Pre-decorated Board, Others), By END-USER (Commercial, Residential), By Thickness (1/2 Inch, 5/8 Inch, More than 5/8 Inch): Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

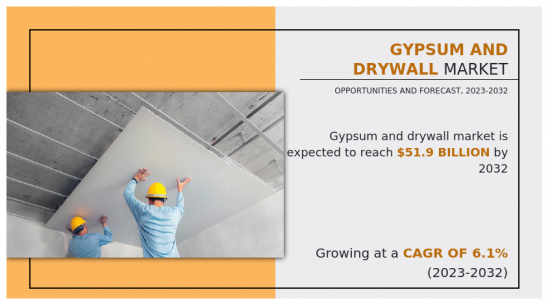

2022年石膏和干墙市场价值为293亿美元,预计2023年至2032年复合年增长率为6.1%,到2032年将达到519亿美元。

石膏/干墙是一种用于建造墙壁、天花板和隔间的建筑材料。这些板是通过在石膏中添加足够的水和添加剂以形成半液体浆料而製成的。这种结合产生硫酸钙,随着时间的结晶,硫酸钙会重结晶并恢復到原来的岩石状态。这些石膏板由于重量轻且易于适应无梁结构的墙壁而常用于建筑领域。

由于都市化的加快,建筑和基础设施开发的增加预计将在预测期内推动市场。石膏板广泛用于墙壁、隔间和天花板的建造,使其成为新建和计划计划的重要组成部分。住宅和企业重建和升级住宅,以提高美观性、实用性和能源效率。石膏板由于其多功能性、易于安装且能够实现所需的饰面而经常用于内装维修。石膏板被认为是重要建筑材料的建设产业的成长也是预计推动石膏板市场成长的主要因素之一。石膏板具有成本效益且易于安装。因此,它可以轻鬆替代建筑中使用的其他建筑材料,例如胶合板、砖块和木材。因此,预计在预测期内对石膏板的需求将会增加。涉及商业、机构、工业和住宅开拓的公司在製造隔间墙、天花板和隔间屏系统时选择石膏板可能会促进石膏和干墙市场的成长。

预计市场将因个人对环境问题和原材料价格波动的日益担忧而受到阻碍。石膏板的生产需要提取和加工自然资源,这对环境有负面影响。该行业对采矿作业、废弃物产生和能源使用的担忧与日俱增。当干墙被倾倒在垃圾掩埋场时,水分会将其内部的硫酸盐转化为有害的硫化氢。遵守环境法规和采用永续实践使得製造商很难以低成本生产这些干墙。所有这些因素预计将限制预测期内的市场成长。

预计对绿色建筑材料的需求不断增长将为石膏板市场的公司创造利润丰厚的机会。为了减少对环境的影响,製造商专注于生产环保石膏板,例如:

1 回收率高或挥发性有机化合物(VOC)排放低的物品。这就是为什么我们生产具有改进的防火、隔音、防潮和抗衝击性能的石膏板,以满足不断变化的客户需求和监管要求。此外,近年来主要行业相关人员的技术进步和新型製造技术的开发推动了石膏板行业的扩张。所有这些因素预计将为预测期内的市场成长创造绝佳机会。

目录

第一章简介

第 2 章执行摘要

第三章市场概况

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 抑制因素

- 机会

- 平均售价

- 市场占有率分析

- 品牌占有率分析

- 贸易资料分析

- 产品消费

- 价值链分析

- 监管指引

- 关键监管分析

- 赎回场景

- 专利形势

第四章石膏和干墙市场:副产品

- 概述

- 墙板

- 天花板

- 装饰板

- 其他的

第五章石膏和干墙市场:依最终用户分类

- 概述

- 商业的

- 住宅

第六章石膏和干墙市场:按厚度

- 概述

- 1/2 英寸

- 5/8英寸

- 5/8吋或以上

第七章石膏和干墙市场:按地区

- 概述

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他的

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他的

- 拉丁美洲/中东/非洲

- 巴西

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他的

第八章 竞争形势

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争对手仪表板

- 竞争热图

- 2022年主要企业定位

第九章 公司简介

- Saint-Gobain

- USG Corporation.

- TECNI-GYPSUM

- NATIONAL GYPPSUM(NGC)

- Knauf Gips KG

- GYPLAC SA

- BEIJING NEW BUILDINGS MATERIAL(GROUP)CO. LTD.

- American Gypsum Company LLC

- Lafarge Group

- Global Mining Company LLC(GMC)

According to a new report published by Allied Market Research, titled, "Gypsum & Drywall Market," The gypsum & drywall market was valued at $29.3 billion in 2022, and is estimated to reach $51.9 billion by 2032, growing at a CAGR of 6.1% from 2023 to 2032.

Gypsum & drywall is a construction material that is used in constructing walls, ceilings, and partitions. These boards are made by combining gypsum with a sufficient amount of water and additives to make a semi-liquid slurry. This combination yields calcium sulphate, which recrystallizes over time, restoring the original rock condition. These gypsum boards are commonly used in the building sector because of their low weight and simple adaption to walls without beam structure.

The market is expected to be driven by increasing building and infrastructure development as a result of rising urbanization during the forecast period. Gypsum boards are widely used in the construction of walls, partitions, and ceilings, making them essential in both new and restoration projects. Homeowners and businesses renovate and upgrade their homes in order to increase their beauty, utility, and energy efficiency. Gypsum boards are often used in interior renovations due to its versatility, ease of installation, and ability to achieve desired finishes. Growth in the construction industry, where gypsum boards are recognized as essential building materials, is also one of the key factors anticipated to drive the growth of the gypsum board market. Gypsum boards are cost-effective and simple to install. Therefore, they may easily replace other building materials like plywood, bricks, wood, and others that are used in construction. The demand for gypsum boards during the forecast years is likely to increase as a result. By choosing gypsum boards when creating partition walls, ceilings, and dividing screen systems, the businesses involved in developing commercial, institutional, industrial, and residential subdivisions are likely to boost the market growth for gypsum & drywall market.

The market is projected to be hampered by increase in environmental concerns among individuals as well as fluctuation in raw material pricing. Gypsum board manufacture requires the extraction and processing of natural resources, which has a negative environmental impact. Concerns about mining operations, trash creation, and energy usage are rising in the business. When gypsum board is deposited into landfills, the sulfate in it is converted into hazardous hydrogen sulfide owing to moisture. Compliance with environmental rules and the adoption of sustainable practices are making it difficult for manufacturers to make these drywalls at a low cost. All these factors are predicted to restrict market growth during the forecast period.

The rising demand for green building materials is projected to generate beneficial possibilities for companies operating in the gypsum board market. To reduce environmental effect, manufacturers are focused on the creation of eco-friendly gypsum boards, such as

1) those with a high recycled content or low volatile organic compound (VOC) emission. This involves producing gypsum boards with increased fire resistance, sound insulation, moisture resistance, and impact resistance qualities to fulfill changing client needs and regulatory requirements. In addition, technological advancements and the development of novel manufacturing techniques by key industry players have boosted the expansion of the gypsum board sector in recent years. All these factors are anticipated to create excellent opportunities for the market growth during the forecast period.

The key players profiled in this report include: Saint-Gobain, USG Corporation., TECNI-GYPSUM, NATIONAL GYPPSUM (NGC), Knauf Gips KG, GYPLAC SA, BEIJING NEW BUILDINGS MATERIAL (GROUP) CO. LTD., American Gypsum Company LLC, Lafarge Group, and Global Mining Company LLC (GMC). The market players are continuously striving to achieve a dominant position in this competitive market using strategies such as

1) collaborations and acquisitions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the gypsum & drywall market analysis from 2022 to 2032 to identify the prevailing gypsum & drywall market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the gypsum & drywall market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global gypsum & drywall market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Product Life Cycles

- Go To Market Strategy

- New Product Development/ Product Matrix of Key Players

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Criss-cross segment analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- Market share analysis of players at global/region/country level

- SWOT Analysis

Key Market Segments

By PRODUCT

- Wallboard

- Ceiling Board

- Pre-decorated Board

- Others

By END-USER

- Commercial

- Residential

By Thickness

- More than 5/8 Inch

- 1/2 Inch

- 5/8 Inch

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- United Arab Emirates

- South Africa

- Rest of LAMEA

Key Market Players:

- Saint-Gobain

- USG Corporation.

- TECNI-GYPSUM

- NATIONAL GYPPSUM (NGC)

- Knauf Gips KG

- GYPLAC SA

- BEIJING NEW BUILDINGS MATERIAL (GROUP) CO. LTD.

- American Gypsum Company LLC

- Lafarge Group

- Global Mining Company LLC (GMC)

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. Average Selling Price

- 3.6. Market Share Analysis

- 3.7. Brand Share Analysis

- 3.8. Trade Data Analysis

- 3.9. Product Consumption

- 3.10. Value Chain Analysis

- 3.11. Regulatory Guidelines

- 3.12. Key Regulation Analysis

- 3.13. Reimbursement Scenario

- 3.14. Patent Landscape

CHAPTER 4: GYPSUM & DRYWALL MARKET, BY PRODUCT

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Wallboard

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Ceiling Board

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Pre-decorated Board

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

- 4.5. Others

- 4.5.1. Key market trends, growth factors and opportunities

- 4.5.2. Market size and forecast, by region

- 4.5.3. Market share analysis by country

CHAPTER 5: GYPSUM & DRYWALL MARKET, BY END-USER

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Commercial

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Residential

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: GYPSUM & DRYWALL MARKET, BY THICKNESS

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. 1/2 Inch

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. 5/8 Inch

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. More than 5/8 Inch

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: GYPSUM & DRYWALL MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by PRODUCT

- 7.2.3. Market size and forecast, by END-USER

- 7.2.4. Market size and forecast, by Thickness

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Market size and forecast, by PRODUCT

- 7.2.5.1.2. Market size and forecast, by END-USER

- 7.2.5.1.3. Market size and forecast, by Thickness

- 7.2.5.2. Canada

- 7.2.5.2.1. Market size and forecast, by PRODUCT

- 7.2.5.2.2. Market size and forecast, by END-USER

- 7.2.5.2.3. Market size and forecast, by Thickness

- 7.2.5.3. Mexico

- 7.2.5.3.1. Market size and forecast, by PRODUCT

- 7.2.5.3.2. Market size and forecast, by END-USER

- 7.2.5.3.3. Market size and forecast, by Thickness

- 7.3. Europe

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by PRODUCT

- 7.3.3. Market size and forecast, by END-USER

- 7.3.4. Market size and forecast, by Thickness

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Market size and forecast, by PRODUCT

- 7.3.5.1.2. Market size and forecast, by END-USER

- 7.3.5.1.3. Market size and forecast, by Thickness

- 7.3.5.2. UK

- 7.3.5.2.1. Market size and forecast, by PRODUCT

- 7.3.5.2.2. Market size and forecast, by END-USER

- 7.3.5.2.3. Market size and forecast, by Thickness

- 7.3.5.3. France

- 7.3.5.3.1. Market size and forecast, by PRODUCT

- 7.3.5.3.2. Market size and forecast, by END-USER

- 7.3.5.3.3. Market size and forecast, by Thickness

- 7.3.5.4. Spain

- 7.3.5.4.1. Market size and forecast, by PRODUCT

- 7.3.5.4.2. Market size and forecast, by END-USER

- 7.3.5.4.3. Market size and forecast, by Thickness

- 7.3.5.5. Italy

- 7.3.5.5.1. Market size and forecast, by PRODUCT

- 7.3.5.5.2. Market size and forecast, by END-USER

- 7.3.5.5.3. Market size and forecast, by Thickness

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Market size and forecast, by PRODUCT

- 7.3.5.6.2. Market size and forecast, by END-USER

- 7.3.5.6.3. Market size and forecast, by Thickness

- 7.4. Asia-Pacific

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by PRODUCT

- 7.4.3. Market size and forecast, by END-USER

- 7.4.4. Market size and forecast, by Thickness

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. China

- 7.4.5.1.1. Market size and forecast, by PRODUCT

- 7.4.5.1.2. Market size and forecast, by END-USER

- 7.4.5.1.3. Market size and forecast, by Thickness

- 7.4.5.2. Japan

- 7.4.5.2.1. Market size and forecast, by PRODUCT

- 7.4.5.2.2. Market size and forecast, by END-USER

- 7.4.5.2.3. Market size and forecast, by Thickness

- 7.4.5.3. India

- 7.4.5.3.1. Market size and forecast, by PRODUCT

- 7.4.5.3.2. Market size and forecast, by END-USER

- 7.4.5.3.3. Market size and forecast, by Thickness

- 7.4.5.4. South Korea

- 7.4.5.4.1. Market size and forecast, by PRODUCT

- 7.4.5.4.2. Market size and forecast, by END-USER

- 7.4.5.4.3. Market size and forecast, by Thickness

- 7.4.5.5. Australia

- 7.4.5.5.1. Market size and forecast, by PRODUCT

- 7.4.5.5.2. Market size and forecast, by END-USER

- 7.4.5.5.3. Market size and forecast, by Thickness

- 7.4.5.6. Rest of Asia-Pacific

- 7.4.5.6.1. Market size and forecast, by PRODUCT

- 7.4.5.6.2. Market size and forecast, by END-USER

- 7.4.5.6.3. Market size and forecast, by Thickness

- 7.5. LAMEA

- 7.5.1. Key market trends, growth factors and opportunities

- 7.5.2. Market size and forecast, by PRODUCT

- 7.5.3. Market size and forecast, by END-USER

- 7.5.4. Market size and forecast, by Thickness

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Market size and forecast, by PRODUCT

- 7.5.5.1.2. Market size and forecast, by END-USER

- 7.5.5.1.3. Market size and forecast, by Thickness

- 7.5.5.2. Saudi Arabia

- 7.5.5.2.1. Market size and forecast, by PRODUCT

- 7.5.5.2.2. Market size and forecast, by END-USER

- 7.5.5.2.3. Market size and forecast, by Thickness

- 7.5.5.3. United Arab Emirates

- 7.5.5.3.1. Market size and forecast, by PRODUCT

- 7.5.5.3.2. Market size and forecast, by END-USER

- 7.5.5.3.3. Market size and forecast, by Thickness

- 7.5.5.4. South Africa

- 7.5.5.4.1. Market size and forecast, by PRODUCT

- 7.5.5.4.2. Market size and forecast, by END-USER

- 7.5.5.4.3. Market size and forecast, by Thickness

- 7.5.5.5. Rest of LAMEA

- 7.5.5.5.1. Market size and forecast, by PRODUCT

- 7.5.5.5.2. Market size and forecast, by END-USER

- 7.5.5.5.3. Market size and forecast, by Thickness

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product mapping of top 10 player

- 8.4. Competitive dashboard

- 8.5. Competitive heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. Saint-Gobain

- 9.1.1. Company overview

- 9.1.2. Key executives

- 9.1.3. Company snapshot

- 9.2. USG Corporation.

- 9.2.1. Company overview

- 9.2.2. Key executives

- 9.2.3. Company snapshot

- 9.3. TECNI-GYPSUM

- 9.3.1. Company overview

- 9.3.2. Key executives

- 9.3.3. Company snapshot

- 9.4. NATIONAL GYPPSUM (NGC)

- 9.4.1. Company overview

- 9.4.2. Key executives

- 9.4.3. Company snapshot

- 9.5. Knauf Gips KG

- 9.5.1. Company overview

- 9.5.2. Key executives

- 9.5.3. Company snapshot

- 9.6. GYPLAC SA

- 9.6.1. Company overview

- 9.6.2. Key executives

- 9.6.3. Company snapshot

- 9.7. BEIJING NEW BUILDINGS MATERIAL (GROUP) CO. LTD.

- 9.7.1. Company overview

- 9.7.2. Key executives

- 9.7.3. Company snapshot

- 9.8. American Gypsum Company LLC

- 9.8.1. Company overview

- 9.8.2. Key executives

- 9.8.3. Company snapshot

- 9.9. Lafarge Group

- 9.9.1. Company overview

- 9.9.2. Key executives

- 9.9.3. Company snapshot

- 9.10. Global Mining Company LLC (GMC)

- 9.10.1. Company overview

- 9.10.2. Key executives

- 9.10.3. Company snapshot

LIST OF TABLES

- TABLE 01. GLOBAL GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 02. GYPSUM & DRYWALL MARKET FOR WALLBOARD, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. GYPSUM & DRYWALL MARKET FOR CEILING BOARD, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GYPSUM & DRYWALL MARKET FOR PRE-DECORATED BOARD, BY REGION, 2022-2032 ($MILLION)

- TABLE 05. GYPSUM & DRYWALL MARKET FOR OTHERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. GLOBAL GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 07. GYPSUM & DRYWALL MARKET FOR COMMERCIAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 08. GYPSUM & DRYWALL MARKET FOR RESIDENTIAL, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. GLOBAL GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 10. GYPSUM & DRYWALL MARKET FOR 1/2 INCH, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. GYPSUM & DRYWALL MARKET FOR 5/8 INCH, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. GYPSUM & DRYWALL MARKET FOR MORE THAN 5/8 INCH, BY REGION, 2022-2032 ($MILLION)

- TABLE 13. GYPSUM & DRYWALL MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 14. NORTH AMERICA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 15. NORTH AMERICA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 16. NORTH AMERICA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 17. NORTH AMERICA GYPSUM & DRYWALL MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 18. U.S. GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 19. U.S. GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 20. U.S. GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 21. CANADA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 22. CANADA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 23. CANADA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 24. MEXICO GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 25. MEXICO GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 26. MEXICO GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 27. EUROPE GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 28. EUROPE GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 29. EUROPE GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 30. EUROPE GYPSUM & DRYWALL MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 31. GERMANY GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 32. GERMANY GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 33. GERMANY GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 34. UK GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 35. UK GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 36. UK GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 37. FRANCE GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 38. FRANCE GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 39. FRANCE GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 40. SPAIN GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 41. SPAIN GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 42. SPAIN GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 43. ITALY GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 44. ITALY GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 45. ITALY GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 46. REST OF EUROPE GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 47. REST OF EUROPE GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 48. REST OF EUROPE GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 49. ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 50. ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 51. ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 52. ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 53. CHINA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 54. CHINA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 55. CHINA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 56. JAPAN GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 57. JAPAN GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 58. JAPAN GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 59. INDIA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 60. INDIA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 61. INDIA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 62. SOUTH KOREA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 63. SOUTH KOREA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 64. SOUTH KOREA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 65. AUSTRALIA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 66. AUSTRALIA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 67. AUSTRALIA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 68. REST OF ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 69. REST OF ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 70. REST OF ASIA-PACIFIC GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 71. LAMEA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 72. LAMEA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 73. LAMEA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 74. LAMEA GYPSUM & DRYWALL MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 75. BRAZIL GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 76. BRAZIL GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 77. BRAZIL GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 78. SAUDI ARABIA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 79. SAUDI ARABIA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 80. SAUDI ARABIA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 81. UNITED ARAB EMIRATES GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 82. UNITED ARAB EMIRATES GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 83. UNITED ARAB EMIRATES GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 84. SOUTH AFRICA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 85. SOUTH AFRICA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 86. SOUTH AFRICA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 87. REST OF LAMEA GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022-2032 ($MILLION)

- TABLE 88. REST OF LAMEA GYPSUM & DRYWALL MARKET, BY END-USER, 2022-2032 ($MILLION)

- TABLE 89. REST OF LAMEA GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022-2032 ($MILLION)

- TABLE 90. SAINT-GOBAIN: KEY EXECUTIVES

- TABLE 91. SAINT-GOBAIN: COMPANY SNAPSHOT

- TABLE 92. USG CORPORATION.: KEY EXECUTIVES

- TABLE 93. USG CORPORATION.: COMPANY SNAPSHOT

- TABLE 94. TECNI-GYPSUM: KEY EXECUTIVES

- TABLE 95. TECNI-GYPSUM: COMPANY SNAPSHOT

- TABLE 96. NATIONAL GYPPSUM (NGC): KEY EXECUTIVES

- TABLE 97. NATIONAL GYPPSUM (NGC): COMPANY SNAPSHOT

- TABLE 98. KNAUF GIPS KG: KEY EXECUTIVES

- TABLE 99. KNAUF GIPS KG: COMPANY SNAPSHOT

- TABLE 100. GYPLAC SA: KEY EXECUTIVES

- TABLE 101. GYPLAC SA: COMPANY SNAPSHOT

- TABLE 102. BEIJING NEW BUILDINGS MATERIAL (GROUP) CO. LTD.: KEY EXECUTIVES

- TABLE 103. BEIJING NEW BUILDINGS MATERIAL (GROUP) CO. LTD.: COMPANY SNAPSHOT

- TABLE 104. AMERICAN GYPSUM COMPANY LLC: KEY EXECUTIVES

- TABLE 105. AMERICAN GYPSUM COMPANY LLC: COMPANY SNAPSHOT

- TABLE 106. LAFARGE GROUP: KEY EXECUTIVES

- TABLE 107. LAFARGE GROUP: COMPANY SNAPSHOT

- TABLE 108. GLOBAL MINING COMPANY LLC (GMC): KEY EXECUTIVES

- TABLE 109. GLOBAL MINING COMPANY LLC (GMC): COMPANY SNAPSHOT

LIST OF FIGURES

- FIGURE 01. GYPSUM & DRYWALL MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF GYPSUM & DRYWALL MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN GYPSUM & DRYWALL MARKET

- FIGURE 04. TOP INVESTMENT POCKETS IN GYPSUM & DRYWALL MARKET (2023-2032)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL GYPSUM & DRYWALL MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. REGULATORY GUIDELINES: GYPSUM & DRYWALL MARKET

- FIGURE 12. IMPACT OF KEY REGULATION: GYPSUM & DRYWALL MARKET

- FIGURE 13. PATENT ANALYSIS BY COMPANY

- FIGURE 14. PATENT ANALYSIS BY COUNTRY

- FIGURE 15. GYPSUM & DRYWALL MARKET, BY PRODUCT, 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR WALLBOARD, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR CEILING BOARD, BY COUNTRY 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR PRE-DECORATED BOARD, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR OTHERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. GYPSUM & DRYWALL MARKET, BY END-USER, 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR COMMERCIAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR RESIDENTIAL, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. GYPSUM & DRYWALL MARKET, BY THICKNESS, 2022 AND 2032(%)

- FIGURE 24. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR 1/2 INCH, BY COUNTRY 2022 AND 2032(%)

- FIGURE 25. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR 5/8 INCH, BY COUNTRY 2022 AND 2032(%)

- FIGURE 26. COMPARATIVE SHARE ANALYSIS OF GYPSUM & DRYWALL MARKET FOR MORE THAN 5/8 INCH, BY COUNTRY 2022 AND 2032(%)

- FIGURE 27. GYPSUM & DRYWALL MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 28. U.S. GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 29. CANADA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 30. MEXICO GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 31. GERMANY GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 32. UK GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 33. FRANCE GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 34. SPAIN GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 35. ITALY GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 36. REST OF EUROPE GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 37. CHINA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 38. JAPAN GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 39. INDIA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 40. SOUTH KOREA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 41. AUSTRALIA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 42. REST OF ASIA-PACIFIC GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 43. BRAZIL GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 44. SAUDI ARABIA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 45. UNITED ARAB EMIRATES GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 46. SOUTH AFRICA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 47. REST OF LAMEA GYPSUM & DRYWALL MARKET, 2022-2032 ($MILLION)

- FIGURE 48. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 49. COMPETITIVE DASHBOARD

- FIGURE 50. COMPETITIVE HEATMAP: GYPSUM & DRYWALL MARKET

- FIGURE 51. TOP PLAYER POSITIONING, 2022

全球石膏和干墙市场

全球石膏和干墙市场 2025年全球石膏基干墙市场报告石膏灰泥市场规模、份额、趋势分析报告:依石膏系统、原料、最终用途、地区、细分市场预测,2025-2030 年

2025年全球石膏基干墙市场报告石膏灰泥市场规模、份额、趋势分析报告:依石膏系统、原料、最终用途、地区、细分市场预测,2025-2030 年 石膏板市场 - 全球产业规模、份额、趋势、机会和预测,按类型、形式、最终用户部门、地区和竞争进行细分,2020-2030 年预测

石膏板市场 - 全球产业规模、份额、趋势、机会和预测,按类型、形式、最终用户部门、地区和竞争进行细分,2020-2030 年预测 亚太地区石膏板和替代品市场:按最终用户应用、类型、材料和国家 - 分析和预测(2023-2033)

亚太地区石膏板和替代品市场:按最终用户应用、类型、材料和国家 - 分析和预测(2023-2033) 石膏板市场:按类型、形式和最终用途区域划分 - 2025-2030 年全球预测防水防潮石膏板市场:按材料类型、应用和最终用户划分-2025-2030年全球预测

石膏板市场:按类型、形式和最终用途区域划分 - 2025-2030 年全球预测防水防潮石膏板市场:按材料类型、应用和最终用户划分-2025-2030年全球预测 欧洲石膏板和替代品市场:按最终用户应用、类型、材料和国家 - 分析和预测(2023-2033)

欧洲石膏板和替代品市场:按最终用户应用、类型、材料和国家 - 分析和预测(2023-2033) 干墙市场报告:2030 年趋势、预测与竞争分析

干墙市场报告:2030 年趋势、预测与竞争分析 石膏板和替代品市场:全球和区域分析(2023-2033)

石膏板和替代品市场:全球和区域分析(2023-2033)