|

市场调查报告书

商品编码

1446907

医用同位素市场:按类型、应用和最终用户分类:2023-2032 年全球机会分析和产业预测Medical Isotope Market By Type (Stable Isotopes, Radioisotopes), By Application (Diagonestic, Nuclear Therapy), By End User (Hospitals, Diagnostic Centers, Research Institutes): Global Opportunity Analysis and Industry Forecast, 2023-2032 |

||||||

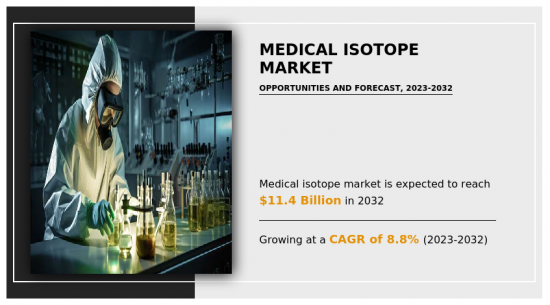

全球医用同位素市场预计将从2022年的51.425亿美元成长到2032年的113.979亿美元,2023年至2032年的复合年增长率为8.8%。

医疗专业人员使用医用同位素来诊断和治疗心臟病和癌症等健康状况。医用同位素的生产是透过两种综合技术完成的:核子反应炉和粒子加速器(线性加速器、迴旋加速器)。

核子医学用于改善多种疾病的放射治疗,包括甲状腺、肺部、骨骼和神经系统疾病。核子医学(放射性同位素)产业的特点是使用放射性材料进行研究、诊断和治疗,越来越多地使用 SPECT 和 PET,以及有关核医学的医疗保健教育和意识。癌症、心血管疾病和神经系统问题等疾病的盛行率不断增加,增加了对核子医学扫描术诊断等精密诊断工具的需求。随着新的放射性药物和诊断影像设备的开发,核子医学治疗变得更加有效和安全。这些发展扩大了核子医学的应用范围并增加了其使用。预计这些因素将在未来几年推动医用同位素市场的成长。

同位素是具有相同数量的质子但不同数量的中子的化学元素。应用于医药、工业、科学研究等各领域。然而,同位素的生产和购买成本昂贵,限制了其广泛使用。同位素的生产通常需要专用设备,例如核子反应炉或粒子加速器。这些设施的建设和运作成本高昂。同位素的处理和製造需要严格的安全法规,这增加了基础设施和营运成本。预计这些因素将限制预测期内医用同位素市场的成长。

正子断层扫描 (PET) 和单光子发射电脑断层扫描 (SPECT) 等诊断成像技术的不断进步为使用医用同位素进行精确、非侵入性的医学成像提供了机会。随着这些成像技术的不断发展,对合适同位素的需求可能会增加。医用同位素的治疗应用有显着的成长机会,特别是在癌症治疗(放射性药物治疗)方面。标靶核素疗法(例如α和β发射核素)的研究和开发正在有助于扩大癌症治疗中使用的同位素类型。此外,随着新 SPECT 和 PET 应用的发展,核医放射性同位素的需求也增加。此外,在2021年12月举行的RSNA21上,GE医疗宣布推出最先进的核医设备SPECT/CT。这些进步预计将加速放射性同位素在医学和核医学技术中的发展。所有这些因素预计将在未来几年推动医用同位素市场的扩张。

COVID-19 大流行最初对核医学放射性同位素行业产生了负面影响,暂时停止或推迟了核医学等非 COVID 诊断和治疗。例如,2021 年6 月发表在《ScienceDirect Journal》上的一份报告发现,虽然COVID-19 病例和死亡人数不断增加,但大流行期间核医学检测、核心脏成像和癌症PET/CT 的数量却在增加。研究显示,从 2020 年 6 月到 2021 年 2 月,随着 COVID-19 病例减少,手术数量增加。然而,随着自 2022 年初以来 COVID-19 病例有所下降,市场在放射学程序方面正在接近大流行前的水平,导致对核医学放射性同位素的需求增加。

相关人员的主要利益

- 本报告定量分析了 2022 年至 2032 年医用同位素市场的细分市场、当前趋势、估计/趋势和动态,并确定了医用同位素市场的有前景的机会。

- 我们提供市场研究以及与市场驱动因素、市场限制和市场机会相关的资讯。

- 波特的五力分析强调买家和供应商帮助相关人员做出利润驱动的商业决策并加强供应商-买家网路的潜力。

- 对医用同位素市场细分的详细分析有助于识别市场机会。

- 每个地区的主要国家都根据其对全球市场的收益贡献绘製了地图。

- 市场参与者定位有助于对标,并可以清楚了解市场参与者的当前地位。

- 该报告包括对区域和全球医用同位素市场趋势、主要企业、细分市场、应用领域和市场成长策略的分析。

可以使用此报告进行定制

- 产品生命週期

- 科技趋势分析

- 国家、区域和全球各级的患者/流行病学资料

- 监管指引

- 根据客户兴趣新增其他公司简介

- 按国家或地区进行的附加分析 – 市场规模和预测

- 十字交叉细分市场分析—市场规模与预测

- 公司简介的扩充列表

- 历史市场资料

- 主要参与者的详细资料(Excel格式,包括位置、联络资讯、供应商/供应商网路等)

- 客户/消费者/原料供应商名单 - 价值链分析

- 全球/区域/国家层级参与者的市场占有率分析

- SWOT分析

目录

第一章简介

第 2 章执行摘要

第三章市场概况

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 抑制因素

- 机会

- 市场占有率分析

- 价值链分析

- 监管指引

- 专利情况

第四章医用同位素市场:依类型

- 概述

- 稳定同位素

- 放射性同位素

第五章医用同位素市场:依应用分类

- 概述

- 诊断

- 核子医学治疗

第六章医用同位素市场:依最终使用者分类

- 概述

- 医院

- 诊断中心

- 研究机构

第七章医用同位素市场:依地区

- 概述

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 义大利

- 其他的

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 其他的

- 拉丁美洲/中东/非洲

- 巴西

- 沙乌地阿拉伯

- UAE

- 南非

- 其他的

第八章 竞争格局

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争对手仪表板

- 竞争热图

- 2022年主要企业定位

第九章 公司简介

- Canadian Nuclear Laboratories(CNL)

- Curium

- GE Healthcare

- Jubilant Radiopharma

- Nordion Inc.

- IBA Radiopharma Solutions

- Mallinckrodt Pharmaceuticals

- northstar medical radioisotopes, llc

- Eczacibasi-Monrol Nuclear Products

- Isotopen Technologien Munchen(ITM)

The global medical isotopes market is anticipated to reach $11,397.9 million by 2032, growing from $5,142.5 million in 2022 at a CAGR of 8.8% from 2023 to 2032.

Medical isotopes are used by medical professionals to diagnose and treat health conditions such as heart disease and cancer. The production of medical isotopes is achieved by using two overarching technologies: nuclear reactors and particle accelerators (linear accelerators, cyclotrons).

Nuclear medicine is being utilized to improve radiotherapy for a variety of ailments, including thyroid problems, lung diseases, bone diseases, and neurological disorders. The nuclear medicine (radio isotopes) industry is characterized by the use of radioactive materials for research, diagnosis, and therapy, as well as the rising use of SPECT and PET, as well as healthcare education and awareness about nuclear medicine. The increasing prevalence of diseases such as cancer, cardiovascular disease, and neurological issues has led to an increase in the demand for precise diagnostic tools such as nuclear medicine imaging. Nuclear medicine treatments have become more effective and safer as new radiopharmaceuticals and imaging instruments are being developed. These developments have broadened the applications of nuclear medicine and increased its use. These factors are expected to boost the growth of the medical isotopes market in the upcoming years.

Isotopes are chemical elemental varieties with the same number of protons but a variable number of neutrons. They are used in a variety of fields, including medicine, industry, and scientific study. However, the manufacturing and purchase of isotopes can be expensive, limiting their broad use. Isotope production frequently necessitates the use of specialist equipment such as nuclear reactors or particle accelerators. These facilities can be costly to construct and operate. Handling and manufacturing isotopes necessitate tight safety rules, which raises the cost of infrastructure and operations. These factors are expected to limit the growth of the medical isotopes market during the forecast period.

Ongoing advancements in diagnostic imaging technologies, such as Positron Emission Tomography (PET) and Single Photon Emission Computed Tomography (SPECT), create opportunities for the use of medical isotopes in accurate and non-invasive medical imaging. As these imaging techniques continue to evolve, the demand for suitable isotopes is likely to increase. The therapeutic applications of medical isotopes, particularly in cancer treatment (radiopharmaceutical therapy), offer substantial growth opportunities. R&D in targeted radionuclide therapies, such as alpha and beta emitters, contribute to expanding the range of isotopes used for cancer treatment. In addition, the demand for nuclear medicine radioisotopes is increasing as new SPECT and PET applications are developed. In addition, at RSNA21 in December 2021, GE Healthcare announced its most sophisticated SPECT/CT, a nuclear medicine system. These advances are expected to accelerate the development of radioisotopes in medicine and nuclear medicine techniques. All these factors are anticipated to drive the medical isotopes market expansion in the upcoming years.

The COVID-19 pandemic initially had a negative influence on the nuclear medicine radioisotopes industry by temporarily canceling or postponing non-COVID diagnosis and treatment, such as nuclear medicine. For example, according to a report published in ScienceDirect Journal in June 2021, the number of nuclear studies, nuclear cardiac imaging, and cancer PET/CT reduced throughout the pandemic while COVID-19 cases and deaths increased. According to the study, operations increased from June 2020 to February 2021 as COVID-19 instances decreased. However, with the drop of COVID-19 cases since early 2022, the market in terms of radiological procedures is approaching pre-pandemic levels, which is leading to an increase in demand for nuclear medicine radioisotopes.

The key players profiled in this report include Canadian Nuclear Laboratories (CNL), Curium, GE Healthcare, Jubilant Radiopharma, Nordion (Canada) Inc, IBA Radiopharma Solutions, Mallinckrodt Pharmaceuticals, NorthStar Medical Radioisotopes, Eczacibasi-Monrol Nuclear Products, and Isotopen Technologies Munchen (ITM). The market players are continuously striving to achieve a dominant position in this competitive market using strategies such as collaborations and acquisitions.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the medical isotope market analysis from 2022 to 2032 to identify the prevailing medical isotope market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the medical isotope market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global medical isotope market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Product Life Cycles

- Technology Trend Analysis

- Patient/epidemiology data at country, region, global level

- Regulatory Guidelines

- Additional company profiles with specific to client's interest

- Additional country or region analysis- market size and forecast

- Criss-cross segment analysis- market size and forecast

- Expanded list for Company Profiles

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- List of customers/consumers/raw material suppliers- value chain analysis

- Market share analysis of players at global/region/country level

- SWOT Analysis

Key Market Segments

By Application

- Diagonestic

- Nuclear Therapy

By Type

- Stable Isotopes

- Radioisotopes

By End User

- Hospitals

- Diagnostic Centers

- Research Institutes

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Russia

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- Saudi Arabia

- UAE

- South Africa

- Rest of LAMEA

Key Market Players:

- Canadian Nuclear Laboratories (CNL)

- Curium

- GE Healthcare

- Jubilant Radiopharma

- Nordion Inc.

- IBA Radiopharma Solutions

- Mallinckrodt Pharmaceuticals

- northstar medical radioisotopes, llc

- Eczacibasi-Monrol Nuclear Products

- Isotopen Technologien Munchen (ITM)

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

- 3.5. Market Share Analysis

- 3.6. Value Chain Analysis

- 3.7. Regulatory Guidelines

- 3.8. Patent Landscape

CHAPTER 4: MEDICAL ISOTOPE MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Stable Isotopes

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Radioisotopes

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

CHAPTER 5: MEDICAL ISOTOPE MARKET, BY APPLICATION

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Diagonestic

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Nuclear Therapy

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

CHAPTER 6: MEDICAL ISOTOPE MARKET, BY END USER

- 6.1. Overview

- 6.1.1. Market size and forecast

- 6.2. Hospitals

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by region

- 6.2.3. Market share analysis by country

- 6.3. Diagnostic Centers

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by region

- 6.3.3. Market share analysis by country

- 6.4. Research Institutes

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by region

- 6.4.3. Market share analysis by country

CHAPTER 7: MEDICAL ISOTOPE MARKET, BY REGION

- 7.1. Overview

- 7.1.1. Market size and forecast By Region

- 7.2. North America

- 7.2.1. Key market trends, growth factors and opportunities

- 7.2.2. Market size and forecast, by Type

- 7.2.3. Market size and forecast, by Application

- 7.2.4. Market size and forecast, by End User

- 7.2.5. Market size and forecast, by country

- 7.2.5.1. U.S.

- 7.2.5.1.1. Market size and forecast, by Type

- 7.2.5.1.2. Market size and forecast, by Application

- 7.2.5.1.3. Market size and forecast, by End User

- 7.2.5.2. Canada

- 7.2.5.2.1. Market size and forecast, by Type

- 7.2.5.2.2. Market size and forecast, by Application

- 7.2.5.2.3. Market size and forecast, by End User

- 7.2.5.3. Mexico

- 7.2.5.3.1. Market size and forecast, by Type

- 7.2.5.3.2. Market size and forecast, by Application

- 7.2.5.3.3. Market size and forecast, by End User

- 7.3. Europe

- 7.3.1. Key market trends, growth factors and opportunities

- 7.3.2. Market size and forecast, by Type

- 7.3.3. Market size and forecast, by Application

- 7.3.4. Market size and forecast, by End User

- 7.3.5. Market size and forecast, by country

- 7.3.5.1. Germany

- 7.3.5.1.1. Market size and forecast, by Type

- 7.3.5.1.2. Market size and forecast, by Application

- 7.3.5.1.3. Market size and forecast, by End User

- 7.3.5.2. UK

- 7.3.5.2.1. Market size and forecast, by Type

- 7.3.5.2.2. Market size and forecast, by Application

- 7.3.5.2.3. Market size and forecast, by End User

- 7.3.5.3. France

- 7.3.5.3.1. Market size and forecast, by Type

- 7.3.5.3.2. Market size and forecast, by Application

- 7.3.5.3.3. Market size and forecast, by End User

- 7.3.5.4. Russia

- 7.3.5.4.1. Market size and forecast, by Type

- 7.3.5.4.2. Market size and forecast, by Application

- 7.3.5.4.3. Market size and forecast, by End User

- 7.3.5.5. Italy

- 7.3.5.5.1. Market size and forecast, by Type

- 7.3.5.5.2. Market size and forecast, by Application

- 7.3.5.5.3. Market size and forecast, by End User

- 7.3.5.6. Rest of Europe

- 7.3.5.6.1. Market size and forecast, by Type

- 7.3.5.6.2. Market size and forecast, by Application

- 7.3.5.6.3. Market size and forecast, by End User

- 7.4. Asia-Pacific

- 7.4.1. Key market trends, growth factors and opportunities

- 7.4.2. Market size and forecast, by Type

- 7.4.3. Market size and forecast, by Application

- 7.4.4. Market size and forecast, by End User

- 7.4.5. Market size and forecast, by country

- 7.4.5.1. China

- 7.4.5.1.1. Market size and forecast, by Type

- 7.4.5.1.2. Market size and forecast, by Application

- 7.4.5.1.3. Market size and forecast, by End User

- 7.4.5.2. Japan

- 7.4.5.2.1. Market size and forecast, by Type

- 7.4.5.2.2. Market size and forecast, by Application

- 7.4.5.2.3. Market size and forecast, by End User

- 7.4.5.3. India

- 7.4.5.3.1. Market size and forecast, by Type

- 7.4.5.3.2. Market size and forecast, by Application

- 7.4.5.3.3. Market size and forecast, by End User

- 7.4.5.4. South Korea

- 7.4.5.4.1. Market size and forecast, by Type

- 7.4.5.4.2. Market size and forecast, by Application

- 7.4.5.4.3. Market size and forecast, by End User

- 7.4.5.5. Australia

- 7.4.5.5.1. Market size and forecast, by Type

- 7.4.5.5.2. Market size and forecast, by Application

- 7.4.5.5.3. Market size and forecast, by End User

- 7.4.5.6. Rest of Asia-Pacific

- 7.4.5.6.1. Market size and forecast, by Type

- 7.4.5.6.2. Market size and forecast, by Application

- 7.4.5.6.3. Market size and forecast, by End User

- 7.5. LAMEA

- 7.5.1. Key market trends, growth factors and opportunities

- 7.5.2. Market size and forecast, by Type

- 7.5.3. Market size and forecast, by Application

- 7.5.4. Market size and forecast, by End User

- 7.5.5. Market size and forecast, by country

- 7.5.5.1. Brazil

- 7.5.5.1.1. Market size and forecast, by Type

- 7.5.5.1.2. Market size and forecast, by Application

- 7.5.5.1.3. Market size and forecast, by End User

- 7.5.5.2. Saudi Arabia

- 7.5.5.2.1. Market size and forecast, by Type

- 7.5.5.2.2. Market size and forecast, by Application

- 7.5.5.2.3. Market size and forecast, by End User

- 7.5.5.3. UAE

- 7.5.5.3.1. Market size and forecast, by Type

- 7.5.5.3.2. Market size and forecast, by Application

- 7.5.5.3.3. Market size and forecast, by End User

- 7.5.5.4. South Africa

- 7.5.5.4.1. Market size and forecast, by Type

- 7.5.5.4.2. Market size and forecast, by Application

- 7.5.5.4.3. Market size and forecast, by End User

- 7.5.5.5. Rest of LAMEA

- 7.5.5.5.1. Market size and forecast, by Type

- 7.5.5.5.2. Market size and forecast, by Application

- 7.5.5.5.3. Market size and forecast, by End User

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top winning strategies

- 8.3. Product mapping of top 10 player

- 8.4. Competitive dashboard

- 8.5. Competitive heatmap

- 8.6. Top player positioning, 2022

CHAPTER 9: COMPANY PROFILES

- 9.1. Canadian Nuclear Laboratories (CNL)

- 9.1.1. Company overview

- 9.1.2. Key executives

- 9.1.3. Company snapshot

- 9.1.4. Operating business segments

- 9.1.5. Product portfolio

- 9.1.6. Business performance

- 9.1.7. Key strategic moves and developments

- 9.2. Curium

- 9.2.1. Company overview

- 9.2.2. Key executives

- 9.2.3. Company snapshot

- 9.2.4. Operating business segments

- 9.2.5. Product portfolio

- 9.2.6. Business performance

- 9.2.7. Key strategic moves and developments

- 9.3. GE Healthcare

- 9.3.1. Company overview

- 9.3.2. Key executives

- 9.3.3. Company snapshot

- 9.3.4. Operating business segments

- 9.3.5. Product portfolio

- 9.3.6. Business performance

- 9.3.7. Key strategic moves and developments

- 9.4. Jubilant Radiopharma

- 9.4.1. Company overview

- 9.4.2. Key executives

- 9.4.3. Company snapshot

- 9.4.4. Operating business segments

- 9.4.5. Product portfolio

- 9.4.6. Business performance

- 9.4.7. Key strategic moves and developments

- 9.5. Nordion Inc.

- 9.5.1. Company overview

- 9.5.2. Key executives

- 9.5.3. Company snapshot

- 9.5.4. Operating business segments

- 9.5.5. Product portfolio

- 9.5.6. Business performance

- 9.5.7. Key strategic moves and developments

- 9.6. IBA Radiopharma Solutions

- 9.6.1. Company overview

- 9.6.2. Key executives

- 9.6.3. Company snapshot

- 9.6.4. Operating business segments

- 9.6.5. Product portfolio

- 9.6.6. Business performance

- 9.6.7. Key strategic moves and developments

- 9.7. Mallinckrodt Pharmaceuticals

- 9.7.1. Company overview

- 9.7.2. Key executives

- 9.7.3. Company snapshot

- 9.7.4. Operating business segments

- 9.7.5. Product portfolio

- 9.7.6. Business performance

- 9.7.7. Key strategic moves and developments

- 9.8. northstar medical radioisotopes, llc

- 9.8.1. Company overview

- 9.8.2. Key executives

- 9.8.3. Company snapshot

- 9.8.4. Operating business segments

- 9.8.5. Product portfolio

- 9.8.6. Business performance

- 9.8.7. Key strategic moves and developments

- 9.9. Eczacibasi-Monrol Nuclear Products

- 9.9.1. Company overview

- 9.9.2. Key executives

- 9.9.3. Company snapshot

- 9.9.4. Operating business segments

- 9.9.5. Product portfolio

- 9.9.6. Business performance

- 9.9.7. Key strategic moves and developments

- 9.10. Isotopen Technologien Munchen (ITM)

- 9.10.1. Company overview

- 9.10.2. Key executives

- 9.10.3. Company snapshot

- 9.10.4. Operating business segments

- 9.10.5. Product portfolio

- 9.10.6. Business performance

- 9.10.7. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 02. MEDICAL ISOTOPE MARKET FOR STABLE ISOTOPES, BY REGION, 2022-2032 ($MILLION)

- TABLE 03. MEDICAL ISOTOPE MARKET FOR RADIOISOTOPES, BY REGION, 2022-2032 ($MILLION)

- TABLE 04. GLOBAL MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 05. MEDICAL ISOTOPE MARKET FOR DIAGONESTIC, BY REGION, 2022-2032 ($MILLION)

- TABLE 06. MEDICAL ISOTOPE MARKET FOR NUCLEAR THERAPY, BY REGION, 2022-2032 ($MILLION)

- TABLE 07. GLOBAL MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 08. MEDICAL ISOTOPE MARKET FOR HOSPITALS, BY REGION, 2022-2032 ($MILLION)

- TABLE 09. MEDICAL ISOTOPE MARKET FOR DIAGNOSTIC CENTERS, BY REGION, 2022-2032 ($MILLION)

- TABLE 10. MEDICAL ISOTOPE MARKET FOR RESEARCH INSTITUTES, BY REGION, 2022-2032 ($MILLION)

- TABLE 11. MEDICAL ISOTOPE MARKET, BY REGION, 2022-2032 ($MILLION)

- TABLE 12. NORTH AMERICA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 13. NORTH AMERICA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 14. NORTH AMERICA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 15. NORTH AMERICA MEDICAL ISOTOPE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 16. U.S. MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 17. U.S. MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 18. U.S. MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 19. CANADA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 20. CANADA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 21. CANADA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 22. MEXICO MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 23. MEXICO MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 24. MEXICO MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 25. EUROPE MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 26. EUROPE MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 27. EUROPE MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 28. EUROPE MEDICAL ISOTOPE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 29. GERMANY MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 30. GERMANY MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 31. GERMANY MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 32. UK MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 33. UK MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 34. UK MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 35. FRANCE MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 36. FRANCE MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 37. FRANCE MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 38. RUSSIA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 39. RUSSIA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 40. RUSSIA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 41. ITALY MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 42. ITALY MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 43. ITALY MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 44. REST OF EUROPE MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 45. REST OF EUROPE MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 46. REST OF EUROPE MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 47. ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 48. ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 49. ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 50. ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 51. CHINA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 52. CHINA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 53. CHINA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 54. JAPAN MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 55. JAPAN MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 56. JAPAN MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 57. INDIA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 58. INDIA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 59. INDIA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 60. SOUTH KOREA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 61. SOUTH KOREA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 62. SOUTH KOREA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 63. AUSTRALIA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 64. AUSTRALIA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 65. AUSTRALIA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 66. REST OF ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 67. REST OF ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 68. REST OF ASIA-PACIFIC MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 69. LAMEA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 70. LAMEA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 71. LAMEA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 72. LAMEA MEDICAL ISOTOPE MARKET, BY COUNTRY, 2022-2032 ($MILLION)

- TABLE 73. BRAZIL MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 74. BRAZIL MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 75. BRAZIL MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 76. SAUDI ARABIA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 77. SAUDI ARABIA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 78. SAUDI ARABIA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 79. UAE MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 80. UAE MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 81. UAE MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 82. SOUTH AFRICA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 83. SOUTH AFRICA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 84. SOUTH AFRICA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 85. REST OF LAMEA MEDICAL ISOTOPE MARKET, BY TYPE, 2022-2032 ($MILLION)

- TABLE 86. REST OF LAMEA MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022-2032 ($MILLION)

- TABLE 87. REST OF LAMEA MEDICAL ISOTOPE MARKET, BY END USER, 2022-2032 ($MILLION)

- TABLE 88. CANADIAN NUCLEAR LABORATORIES (CNL): KEY EXECUTIVES

- TABLE 89. CANADIAN NUCLEAR LABORATORIES (CNL): COMPANY SNAPSHOT

- TABLE 90. CANADIAN NUCLEAR LABORATORIES (CNL): PRODUCT SEGMENTS

- TABLE 91. CANADIAN NUCLEAR LABORATORIES (CNL): SERVICE SEGMENTS

- TABLE 92. CANADIAN NUCLEAR LABORATORIES (CNL): PRODUCT PORTFOLIO

- TABLE 93. CANADIAN NUCLEAR LABORATORIES (CNL): KEY STRATERGIES

- TABLE 94. CURIUM: KEY EXECUTIVES

- TABLE 95. CURIUM: COMPANY SNAPSHOT

- TABLE 96. CURIUM: PRODUCT SEGMENTS

- TABLE 97. CURIUM: SERVICE SEGMENTS

- TABLE 98. CURIUM: PRODUCT PORTFOLIO

- TABLE 99. CURIUM: KEY STRATERGIES

- TABLE 100. GE HEALTHCARE: KEY EXECUTIVES

- TABLE 101. GE HEALTHCARE: COMPANY SNAPSHOT

- TABLE 102. GE HEALTHCARE: PRODUCT SEGMENTS

- TABLE 103. GE HEALTHCARE: SERVICE SEGMENTS

- TABLE 104. GE HEALTHCARE: PRODUCT PORTFOLIO

- TABLE 105. GE HEALTHCARE: KEY STRATERGIES

- TABLE 106. JUBILANT RADIOPHARMA: KEY EXECUTIVES

- TABLE 107. JUBILANT RADIOPHARMA: COMPANY SNAPSHOT

- TABLE 108. JUBILANT RADIOPHARMA: PRODUCT SEGMENTS

- TABLE 109. JUBILANT RADIOPHARMA: SERVICE SEGMENTS

- TABLE 110. JUBILANT RADIOPHARMA: PRODUCT PORTFOLIO

- TABLE 111. JUBILANT RADIOPHARMA: KEY STRATERGIES

- TABLE 112. NORDION INC.: KEY EXECUTIVES

- TABLE 113. NORDION INC.: COMPANY SNAPSHOT

- TABLE 114. NORDION INC.: PRODUCT SEGMENTS

- TABLE 115. NORDION INC.: SERVICE SEGMENTS

- TABLE 116. NORDION INC.: PRODUCT PORTFOLIO

- TABLE 117. NORDION INC.: KEY STRATERGIES

- TABLE 118. IBA RADIOPHARMA SOLUTIONS : KEY EXECUTIVES

- TABLE 119. IBA RADIOPHARMA SOLUTIONS : COMPANY SNAPSHOT

- TABLE 120. IBA RADIOPHARMA SOLUTIONS : PRODUCT SEGMENTS

- TABLE 121. IBA RADIOPHARMA SOLUTIONS : SERVICE SEGMENTS

- TABLE 122. IBA RADIOPHARMA SOLUTIONS : PRODUCT PORTFOLIO

- TABLE 123. IBA RADIOPHARMA SOLUTIONS : KEY STRATERGIES

- TABLE 124. MALLINCKRODT PHARMACEUTICALS: KEY EXECUTIVES

- TABLE 125. MALLINCKRODT PHARMACEUTICALS: COMPANY SNAPSHOT

- TABLE 126. MALLINCKRODT PHARMACEUTICALS: PRODUCT SEGMENTS

- TABLE 127. MALLINCKRODT PHARMACEUTICALS: SERVICE SEGMENTS

- TABLE 128. MALLINCKRODT PHARMACEUTICALS: PRODUCT PORTFOLIO

- TABLE 129. MALLINCKRODT PHARMACEUTICALS: KEY STRATERGIES

- TABLE 130. NORTHSTAR MEDICAL RADIOISOTOPES, LLC: KEY EXECUTIVES

- TABLE 131. NORTHSTAR MEDICAL RADIOISOTOPES, LLC: COMPANY SNAPSHOT

- TABLE 132. NORTHSTAR MEDICAL RADIOISOTOPES, LLC: PRODUCT SEGMENTS

- TABLE 133. NORTHSTAR MEDICAL RADIOISOTOPES, LLC: SERVICE SEGMENTS

- TABLE 134. NORTHSTAR MEDICAL RADIOISOTOPES, LLC: PRODUCT PORTFOLIO

- TABLE 135. NORTHSTAR MEDICAL RADIOISOTOPES, LLC: KEY STRATERGIES

- TABLE 136. ECZACIBASI-MONROL NUCLEAR PRODUCTS: KEY EXECUTIVES

- TABLE 137. ECZACIBASI-MONROL NUCLEAR PRODUCTS: COMPANY SNAPSHOT

- TABLE 138. ECZACIBASI-MONROL NUCLEAR PRODUCTS: PRODUCT SEGMENTS

- TABLE 139. ECZACIBASI-MONROL NUCLEAR PRODUCTS: SERVICE SEGMENTS

- TABLE 140. ECZACIBASI-MONROL NUCLEAR PRODUCTS: PRODUCT PORTFOLIO

- TABLE 141. ECZACIBASI-MONROL NUCLEAR PRODUCTS: KEY STRATERGIES

- TABLE 142. ISOTOPEN TECHNOLOGIEN MUNCHEN (ITM): KEY EXECUTIVES

- TABLE 143. ISOTOPEN TECHNOLOGIEN MUNCHEN (ITM): COMPANY SNAPSHOT

- TABLE 144. ISOTOPEN TECHNOLOGIEN MUNCHEN (ITM): PRODUCT SEGMENTS

- TABLE 145. ISOTOPEN TECHNOLOGIEN MUNCHEN (ITM): SERVICE SEGMENTS

- TABLE 146. ISOTOPEN TECHNOLOGIEN MUNCHEN (ITM): PRODUCT PORTFOLIO

- TABLE 147. ISOTOPEN TECHNOLOGIEN MUNCHEN (ITM): KEY STRATERGIES

LIST OF FIGURES

- FIGURE 01. MEDICAL ISOTOPE MARKET, 2022-2032

- FIGURE 02. SEGMENTATION OF MEDICAL ISOTOPE MARKET,2022-2032

- FIGURE 03. TOP IMPACTING FACTORS IN MEDICAL ISOTOPE MARKET

- FIGURE 04. TOP INVESTMENT POCKETS IN MEDICAL ISOTOPE MARKET (2023-2032)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL MEDICAL ISOTOPE MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. REGULATORY GUIDELINES: MEDICAL ISOTOPE MARKET

- FIGURE 12. PATENT ANALYSIS BY COMPANY

- FIGURE 13. PATENT ANALYSIS BY COUNTRY

- FIGURE 14. MEDICAL ISOTOPE MARKET, BY TYPE, 2022 AND 2032(%)

- FIGURE 15. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR STABLE ISOTOPES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR RADIOISOTOPES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 17. MEDICAL ISOTOPE MARKET, BY APPLICATION, 2022 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR DIAGONESTIC, BY COUNTRY 2022 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR NUCLEAR THERAPY, BY COUNTRY 2022 AND 2032(%)

- FIGURE 20. MEDICAL ISOTOPE MARKET, BY END USER, 2022 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR HOSPITALS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR DIAGNOSTIC CENTERS, BY COUNTRY 2022 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF MEDICAL ISOTOPE MARKET FOR RESEARCH INSTITUTES, BY COUNTRY 2022 AND 2032(%)

- FIGURE 24. MEDICAL ISOTOPE MARKET BY REGION, 2022 AND 2032(%)

- FIGURE 25. U.S. MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 26. CANADA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 27. MEXICO MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 28. GERMANY MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 29. UK MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 30. FRANCE MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 31. RUSSIA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 32. ITALY MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 33. REST OF EUROPE MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 34. CHINA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 35. JAPAN MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 36. INDIA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 37. SOUTH KOREA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 38. AUSTRALIA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 39. REST OF ASIA-PACIFIC MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 40. BRAZIL MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 41. SAUDI ARABIA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 42. UAE MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 43. SOUTH AFRICA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 44. REST OF LAMEA MEDICAL ISOTOPE MARKET, 2022-2032 ($MILLION)

- FIGURE 45. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 46. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 47. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 48. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 49. COMPETITIVE DASHBOARD

- FIGURE 50. COMPETITIVE HEATMAP: MEDICAL ISOTOPE MARKET

- FIGURE 51. TOP PLAYER POSITIONING, 2022

全球医用同位素市场

全球医用同位素市场 2025年全球医用同位素市场报告

2025年全球医用同位素市场报告 全球同位素市场(按类型和应用)- 机会分析和产业预测,2024 年至 2033 年

全球同位素市场(按类型和应用)- 机会分析和产业预测,2024 年至 2033 年 全球医用同位素市场规模、份额、趋势分析报告:2023-2030 年按类型、最终用户、应用、地区分類的展望和预测

全球医用同位素市场规模、份额、趋势分析报告:2023-2030 年按类型、最终用户、应用、地区分類的展望和预测