|

市场调查报告书

商品编码

1513374

按类型和应用分類的全球电子元件市场:机会分析和产业预测(2024-2032)Electronic Components Market By Type, By Application : Global Opportunity Analysis and Industry Forecast, 2024-2032 |

||||||

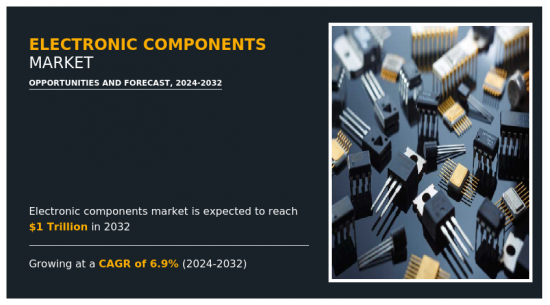

预计2023年全球电子元件市场规模将达6,000亿美元,2032年将达1兆美元,2024年至2032年复合年增长率为6.9%。

电子元件包含对电子设备和系统的功能至关重要的各种基本元件。这些元件包括电阻器、电容器、电感器、二极体、电晶体、积体电路、连接器以及各种被动和主动电子元件。电子元件是建构电子电路的基本元件,促进电流流动、讯号处理、电压调节以及其他各行业电子设备运作所需且关键的其他功能。

由于快速的技术进步、不断变化的客户偏好以及随时间变化的行业趋势,电子元件市场的性质据说是动态且不断变化的。电子元件不断因小型化、提高效率和新功能等技术创新而转变。零件製造商面临 5G、物联网 (IoT)、人工智慧 (AI) 和自动驾驶汽车等新兴技术的新机会和威胁。此外,全球化和供应链的相互依赖正在影响市场动态,影响电子元件的价格、可用性、品质等。随着消费者偏好转向绿色和永续的电子产品,需要透过永续的製造流程生产环保组件。最后,遵守监管标准不仅对电子元件供应商的打入市场策略产生重大影响,而且对电子元件製造商的产品开发策略(包括製造方法)产生重大影响。在所有这些变数中,适应性、创新技术进步、商业模式理解和策略合作伙伴关係有助于应对这个市场领域的复杂性,并确保我在不断变化的环境中的竞争力。

按类型划分,市场分为主动元件、被动元件和电子机械元件。 2022年,主动元件在收益方面占据市场主导地位。此外,被动元件领域预计将在预测期内呈现最高的复合年增长率。由于被动元件在通讯、汽车电子和消费性电子等各种电子应用中的重要性,因此被认为是预测期内成长最快、年复合成长率最高的领域。由于物联网设备、智慧家电和电动车的快速采用,电阻器、电容器和电感器等被动元件可能会经历繁荣。这些元件在各个工业领域的广泛采用也得益于被动元件技术的改进,包括更小的尺寸、更高的性能水平以及更高的整体可靠性。

根据应用,它们分为消费性电子、汽车、工业自动化、通讯、航太和国防、医疗保健、能源和电力等。 2022年,消费性电子产业在收益方面占据市场主导地位。然而,预计汽车产业在预测期内将呈现最高的复合年增长率。由于汽车电子产品日益复杂和扩散、电动车和智慧功能等技术进步以及汽车需求不断增加(尤其是在亚太地区),汽车电子元件市场成长最快。

相关人员的主要利益

- 该报告定量分析了2023年至2032年电子元件市场的细分市场、当前趋势、估计和动态,并确定了电子元件市场的强大机会。

- 我们提供市场研究以及与市场驱动因素、市场限制和市场机会相关的资讯。

- 波特的五力分析揭示了买家和供应商的潜力,帮助相关人员做出利润驱动的业务决策并加强供应商和买家网路。

- 对电子元件市场细分的详细分析有助于识别市场机会。

- 每个地区的主要国家都根据其对全球市场的收益贡献绘製了地图。

- 市场公司定位有助于基准化分析并提供对市场公司当前地位的清晰了解。

- 该报告包括对区域和全球电子元件市场趋势、主要企业、细分市场、应用领域和市场成长策略的分析。

使用此报告可以进行报告客製化(请联络销售人员以了解额外费用和时间表)

- 按地区分類的新参与企业

- 新产品开发/主要企业产品矩阵

- 国家、区域和全球各级的患者/流行病学资料

- 历史市场资料

- 主要企业详细资料(Excel 格式,包括位置、联络资讯、供应商/供应商网路等)

- 全球/区域/国家层级公司的市场占有率分析

- SWOT分析

目录

第一章简介

第 2 章执行摘要

第三章市场概况

- 市场定义和范围

- 主要发现

- 影响因素

- 主要投资机会

- 波特五力分析

- 市场动态

- 促进因素

- 抑制因素

- 机会

第四章电子元件市场:依类型

- 概述

- 主动元件

- 被动元件

- 机电零件

第五章电子元件市场:依应用分类

- 概述

- 家用电子产品

- 车

- 工业自动化

- 通讯

- 航太/国防

- 卫生保健

- 能源/电力

- 其他的

第六章电子元件市场:按地区

- 概述

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 其他的

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他的

- 拉丁美洲

- 巴西

- 阿根廷

- 其他的

- 中东/非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 其他的

第七章 竞争格局

- 介绍

- 关键成功策略

- 10家主要企业产品图谱

- 竞争对手仪表板

- 竞争热图

- 主要企业定位(2023年)

第八章 公司简介

- NXP Semiconductors NV

- Panasonic Corporation

- Renesas Electric Corporation

- API Technologies Corp

- AVX Corporation

- Eaton Corp.

- Datronix Holdings

- Fujitsu Component

- fci electronics

- Hitachi AIC

The electronics components market was valued at $0.6 trillion in 2023 and is estimated to reach $1.0 trillion by 2032, exhibiting a CAGR of 6.9% from 2024 to 2032.

Electronics components, within the context of the market, encompass a wide range of fundamental building blocks essential for the functioning of electronic devices and systems. These components include resistors, capacitors, inductors, diodes, transistors, integrated circuits, connectors, and various passive and active electronic elements. They serve as the foundational elements upon which electronic circuits are built, facilitating the flow of electric current, signal processing, voltage regulation, and other crucial functions necessary for the operation of electronic devices across diverse industries.

The nature of the electronics components market is described as dynamic and ever-changing due to swift technological advances, shifting customer preferences, and industry trends that change over time. The electronic component landscape keeps being reshaped by technological innovations such as miniaturization, improved efficiency, and new functionalities. Component manufacturers are faced with new opportunities and threats in emerging technologies like 5G, the Internet of Things (IoT), artificial intelligence (AI), and self-driving cars. Moreover, globalization and supply chain interdependencies influence market dynamics thereby affecting pricing, availability, and quality of electronic components among other factors. The shift in consumers taste towards environmentally friendly and sustainable electronic goods has therefore necessitated manufacturing environmentally conscious components through sustainable manufacturing processes. Lastly, regulatory standards conformity significantly influences product development strategies for electronics component manufacturers including manufacturing practices as well as market entry strategies for electronics component suppliers. Amongst all these variables adaptability; innovative technology advancement; an understanding of the business model; and strategic partnerships helped navigate through the complexities of this market sector guaranteeing competitiveness in a continuously evolving environment.

Based on type, the market is divided into active components, passive components, and electromechanical components. In 2022, active components dominated the market in terms of revenue. Moreover, the passive components segment is projected to have the highest CAGR during the forecast period. Passive constituents are believed to be the fastest-growing segment with the highest annual CAGR during the forecast period due to their significance across various electronic applications like telecommunications, automotive electronics, and consumer electronics. Passive elements such as resistors, capacitors, and inductors will witness a boom due to the rapid popularity of IoT devices, smart appliances, and electric vehicles. Besides, the wide adoption of these components across various industry domains can be attributed to improved passive component technologies including miniaturization, better performance levels as well as increased overall reliability.

On the basis of application, the market is classified into consumer electronics, automotive, industrial automation, telecommunication, aerospace and defense, healthcare, energy and power, and others. In 2022, the consumer electronics segment dominated the market in terms of revenue. However, the automotive segment is expected to manifest the highest CAGR during the forecast period. The automotive sector in the electronics components market is the fastest growing due to the increasing complexity and popularity of automotive electronics, advancements in technologies such as electric vehicles and smart features, and the growing demand for vehicles, especially in the Asia-Pacific region.

By region, the electronics components industry opportunity is analyzed across North America (the U.S., Canada, and Mexico), Europe (the UK, Germany, France, Italy, and the rest of Europe), Asia-Pacific (China, Japan, India, South Korea, and rest of Asia-Pacific), Latin America (Brazil, Argentina, and rest of Latin America), and Middle East and Africa (UAE, Saudi Arabia, and rest of Middle East and Africa). Asia-Pacific holds a major share in the global electronics components market in the year 2023, owing to the presence of major players such as Samsung Electronics, Taiwan Semiconductor Manufacturing Company Limited, Sony Corporation, Panasonic Corporation, and Murata Manufacturing Co., Ltd.

Key Benefits For Stakeholders

- This report provides a quantitative analysis of the market segments, current trends, estimations, and dynamics of the electronic components market analysis from 2023 to 2032 to identify the prevailing electronic components market opportunities.

- The market research is offered along with information related to key drivers, restraints, and opportunities.

- Porter's five forces analysis highlights the potency of buyers and suppliers to enable stakeholders make profit-oriented business decisions and strengthen their supplier-buyer network.

- In-depth analysis of the electronic components market segmentation assists to determine the prevailing market opportunities.

- Major countries in each region are mapped according to their revenue contribution to the global market.

- Market player positioning facilitates benchmarking and provides a clear understanding of the present position of the market players.

- The report includes the analysis of the regional as well as global electronic components market trends, key players, market segments, application areas, and market growth strategies.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Upcoming/New Entrant by Regions

- New Product Development/ Product Matrix of Key Players

- Patient/epidemiology data at country, region, global level

- Historic market data

- Key player details (including location, contact details, supplier/vendor network etc. in excel format)

- Market share analysis of players at global/region/country level

- SWOT Analysis

Key Market Segments

By Type

- Active Components

- Passive Components

- Electromechanical Components

By Application

- Aerospace and Defense

- Healthcare

- Energy and Power

- Others

- Consumer Electronics

- Automotive

- Industrial Automation

- Telecommunication

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East and Africa

- UAE

- Saudi Arabia

- Rest of Middle East And Africa

Key Market Players:

- NXP Semiconductors N.V.

- Panasonic Corporation

- Renesas Electric Corporation

- API Technologies Corp

- AVX Corporation

- Eaton Corp.

- Datronix Holdings

- Fujitsu Component

- fci electronics

- Hitachi AIC

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report description

- 1.2. Key market segments

- 1.3. Key benefits to the stakeholders

- 1.4. Research methodology

- 1.4.1. Primary research

- 1.4.2. Secondary research

- 1.4.3. Analyst tools and models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO perspective

CHAPTER 3: MARKET OVERVIEW

- 3.1. Market definition and scope

- 3.2. Key findings

- 3.2.1. Top impacting factors

- 3.2.2. Top investment pockets

- 3.3. Porter's five forces analysis

- 3.4. Market dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

CHAPTER 4: ELECTRONIC COMPONENTS MARKET, BY TYPE

- 4.1. Overview

- 4.1.1. Market size and forecast

- 4.2. Active Components

- 4.2.1. Key market trends, growth factors and opportunities

- 4.2.2. Market size and forecast, by region

- 4.2.3. Market share analysis by country

- 4.3. Passive Components

- 4.3.1. Key market trends, growth factors and opportunities

- 4.3.2. Market size and forecast, by region

- 4.3.3. Market share analysis by country

- 4.4. Electromechanical Components

- 4.4.1. Key market trends, growth factors and opportunities

- 4.4.2. Market size and forecast, by region

- 4.4.3. Market share analysis by country

CHAPTER 5: ELECTRONIC COMPONENTS MARKET, BY APPLICATION

- 5.1. Overview

- 5.1.1. Market size and forecast

- 5.2. Consumer Electronics

- 5.2.1. Key market trends, growth factors and opportunities

- 5.2.2. Market size and forecast, by region

- 5.2.3. Market share analysis by country

- 5.3. Automotive

- 5.3.1. Key market trends, growth factors and opportunities

- 5.3.2. Market size and forecast, by region

- 5.3.3. Market share analysis by country

- 5.4. Industrial Automation

- 5.4.1. Key market trends, growth factors and opportunities

- 5.4.2. Market size and forecast, by region

- 5.4.3. Market share analysis by country

- 5.5. Telecommunication

- 5.5.1. Key market trends, growth factors and opportunities

- 5.5.2. Market size and forecast, by region

- 5.5.3. Market share analysis by country

- 5.6. Aerospace and Defense

- 5.6.1. Key market trends, growth factors and opportunities

- 5.6.2. Market size and forecast, by region

- 5.6.3. Market share analysis by country

- 5.7. Healthcare

- 5.7.1. Key market trends, growth factors and opportunities

- 5.7.2. Market size and forecast, by region

- 5.7.3. Market share analysis by country

- 5.8. Energy and Power

- 5.8.1. Key market trends, growth factors and opportunities

- 5.8.2. Market size and forecast, by region

- 5.8.3. Market share analysis by country

- 5.9. Others

- 5.9.1. Key market trends, growth factors and opportunities

- 5.9.2. Market size and forecast, by region

- 5.9.3. Market share analysis by country

CHAPTER 6: ELECTRONIC COMPONENTS MARKET, BY REGION

- 6.1. Overview

- 6.1.1. Market size and forecast By Region

- 6.2. North America

- 6.2.1. Key market trends, growth factors and opportunities

- 6.2.2. Market size and forecast, by Type

- 6.2.3. Market size and forecast, by Application

- 6.2.4. Market size and forecast, by country

- 6.2.4.1. U.S.

- 6.2.4.1.1. Market size and forecast, by Type

- 6.2.4.1.2. Market size and forecast, by Application

- 6.2.4.2. Canada

- 6.2.4.2.1. Market size and forecast, by Type

- 6.2.4.2.2. Market size and forecast, by Application

- 6.2.4.3. Mexico

- 6.2.4.3.1. Market size and forecast, by Type

- 6.2.4.3.2. Market size and forecast, by Application

- 6.3. Europe

- 6.3.1. Key market trends, growth factors and opportunities

- 6.3.2. Market size and forecast, by Type

- 6.3.3. Market size and forecast, by Application

- 6.3.4. Market size and forecast, by country

- 6.3.4.1. UK

- 6.3.4.1.1. Market size and forecast, by Type

- 6.3.4.1.2. Market size and forecast, by Application

- 6.3.4.2. Germany

- 6.3.4.2.1. Market size and forecast, by Type

- 6.3.4.2.2. Market size and forecast, by Application

- 6.3.4.3. France

- 6.3.4.3.1. Market size and forecast, by Type

- 6.3.4.3.2. Market size and forecast, by Application

- 6.3.4.4. Italy

- 6.3.4.4.1. Market size and forecast, by Type

- 6.3.4.4.2. Market size and forecast, by Application

- 6.3.4.5. Rest of Europe

- 6.3.4.5.1. Market size and forecast, by Type

- 6.3.4.5.2. Market size and forecast, by Application

- 6.4. Asia-Pacific

- 6.4.1. Key market trends, growth factors and opportunities

- 6.4.2. Market size and forecast, by Type

- 6.4.3. Market size and forecast, by Application

- 6.4.4. Market size and forecast, by country

- 6.4.4.1. China

- 6.4.4.1.1. Market size and forecast, by Type

- 6.4.4.1.2. Market size and forecast, by Application

- 6.4.4.2. Japan

- 6.4.4.2.1. Market size and forecast, by Type

- 6.4.4.2.2. Market size and forecast, by Application

- 6.4.4.3. India

- 6.4.4.3.1. Market size and forecast, by Type

- 6.4.4.3.2. Market size and forecast, by Application

- 6.4.4.4. South Korea

- 6.4.4.4.1. Market size and forecast, by Type

- 6.4.4.4.2. Market size and forecast, by Application

- 6.4.4.5. Rest of Asia-Pacific

- 6.4.4.5.1. Market size and forecast, by Type

- 6.4.4.5.2. Market size and forecast, by Application

- 6.5. Latin America

- 6.5.1. Key market trends, growth factors and opportunities

- 6.5.2. Market size and forecast, by Type

- 6.5.3. Market size and forecast, by Application

- 6.5.4. Market size and forecast, by country

- 6.5.4.1. Brazil

- 6.5.4.1.1. Market size and forecast, by Type

- 6.5.4.1.2. Market size and forecast, by Application

- 6.5.4.2. Argentina

- 6.5.4.2.1. Market size and forecast, by Type

- 6.5.4.2.2. Market size and forecast, by Application

- 6.5.4.3. Rest of Latin America

- 6.5.4.3.1. Market size and forecast, by Type

- 6.5.4.3.2. Market size and forecast, by Application

- 6.6. Middle East and Africa

- 6.6.1. Key market trends, growth factors and opportunities

- 6.6.2. Market size and forecast, by Type

- 6.6.3. Market size and forecast, by Application

- 6.6.4. Market size and forecast, by country

- 6.6.4.1. UAE

- 6.6.4.1.1. Market size and forecast, by Type

- 6.6.4.1.2. Market size and forecast, by Application

- 6.6.4.2. Saudi Arabia

- 6.6.4.2.1. Market size and forecast, by Type

- 6.6.4.2.2. Market size and forecast, by Application

- 6.6.4.3. Rest of Middle East And Africa

- 6.6.4.3.1. Market size and forecast, by Type

- 6.6.4.3.2. Market size and forecast, by Application

CHAPTER 7: COMPETITIVE LANDSCAPE

- 7.1. Introduction

- 7.2. Top winning strategies

- 7.3. Product mapping of top 10 player

- 7.4. Competitive dashboard

- 7.5. Competitive heatmap

- 7.6. Top player positioning, 2023

CHAPTER 8: COMPANY PROFILES

- 8.1. NXP Semiconductors N.V.

- 8.1.1. Company overview

- 8.1.2. Key executives

- 8.1.3. Company snapshot

- 8.1.4. Operating business segments

- 8.1.5. Product portfolio

- 8.1.6. Business performance

- 8.1.7. Key strategic moves and developments

- 8.2. Panasonic Corporation

- 8.2.1. Company overview

- 8.2.2. Key executives

- 8.2.3. Company snapshot

- 8.2.4. Operating business segments

- 8.2.5. Product portfolio

- 8.2.6. Business performance

- 8.2.7. Key strategic moves and developments

- 8.3. Renesas Electric Corporation

- 8.3.1. Company overview

- 8.3.2. Key executives

- 8.3.3. Company snapshot

- 8.3.4. Operating business segments

- 8.3.5. Product portfolio

- 8.3.6. Business performance

- 8.3.7. Key strategic moves and developments

- 8.4. API Technologies Corp

- 8.4.1. Company overview

- 8.4.2. Key executives

- 8.4.3. Company snapshot

- 8.4.4. Operating business segments

- 8.4.5. Product portfolio

- 8.4.6. Business performance

- 8.4.7. Key strategic moves and developments

- 8.5. AVX Corporation

- 8.5.1. Company overview

- 8.5.2. Key executives

- 8.5.3. Company snapshot

- 8.5.4. Operating business segments

- 8.5.5. Product portfolio

- 8.5.6. Business performance

- 8.5.7. Key strategic moves and developments

- 8.6. Eaton Corp.

- 8.6.1. Company overview

- 8.6.2. Key executives

- 8.6.3. Company snapshot

- 8.6.4. Operating business segments

- 8.6.5. Product portfolio

- 8.6.6. Business performance

- 8.6.7. Key strategic moves and developments

- 8.7. Datronix Holdings

- 8.7.1. Company overview

- 8.7.2. Key executives

- 8.7.3. Company snapshot

- 8.7.4. Operating business segments

- 8.7.5. Product portfolio

- 8.7.6. Business performance

- 8.7.7. Key strategic moves and developments

- 8.8. Fujitsu Component

- 8.8.1. Company overview

- 8.8.2. Key executives

- 8.8.3. Company snapshot

- 8.8.4. Operating business segments

- 8.8.5. Product portfolio

- 8.8.6. Business performance

- 8.8.7. Key strategic moves and developments

- 8.9. fci electronics

- 8.9.1. Company overview

- 8.9.2. Key executives

- 8.9.3. Company snapshot

- 8.9.4. Operating business segments

- 8.9.5. Product portfolio

- 8.9.6. Business performance

- 8.9.7. Key strategic moves and developments

- 8.10. Hitachi AIC

- 8.10.1. Company overview

- 8.10.2. Key executives

- 8.10.3. Company snapshot

- 8.10.4. Operating business segments

- 8.10.5. Product portfolio

- 8.10.6. Business performance

- 8.10.7. Key strategic moves and developments

LIST OF TABLES

- TABLE 01. GLOBAL ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 02. ELECTRONIC COMPONENTS MARKET FOR ACTIVE COMPONENTS, BY REGION, 2023-2032 ($BILLION)

- TABLE 03. ELECTRONIC COMPONENTS MARKET FOR PASSIVE COMPONENTS, BY REGION, 2023-2032 ($BILLION)

- TABLE 04. ELECTRONIC COMPONENTS MARKET FOR ELECTROMECHANICAL COMPONENTS, BY REGION, 2023-2032 ($BILLION)

- TABLE 05. GLOBAL ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 06. ELECTRONIC COMPONENTS MARKET FOR CONSUMER ELECTRONICS, BY REGION, 2023-2032 ($BILLION)

- TABLE 07. ELECTRONIC COMPONENTS MARKET FOR AUTOMOTIVE, BY REGION, 2023-2032 ($BILLION)

- TABLE 08. ELECTRONIC COMPONENTS MARKET FOR INDUSTRIAL AUTOMATION, BY REGION, 2023-2032 ($BILLION)

- TABLE 09. ELECTRONIC COMPONENTS MARKET FOR TELECOMMUNICATION, BY REGION, 2023-2032 ($BILLION)

- TABLE 10. ELECTRONIC COMPONENTS MARKET FOR AEROSPACE AND DEFENSE, BY REGION, 2023-2032 ($BILLION)

- TABLE 11. ELECTRONIC COMPONENTS MARKET FOR HEALTHCARE, BY REGION, 2023-2032 ($BILLION)

- TABLE 12. ELECTRONIC COMPONENTS MARKET FOR ENERGY AND POWER, BY REGION, 2023-2032 ($BILLION)

- TABLE 13. ELECTRONIC COMPONENTS MARKET FOR OTHERS, BY REGION, 2023-2032 ($BILLION)

- TABLE 14. ELECTRONIC COMPONENTS MARKET, BY REGION, 2023-2032 ($BILLION)

- TABLE 15. NORTH AMERICA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 16. NORTH AMERICA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 17. NORTH AMERICA ELECTRONIC COMPONENTS MARKET, BY COUNTRY, 2023-2032 ($BILLION)

- TABLE 18. U.S. ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 19. U.S. ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 20. CANADA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 21. CANADA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 22. MEXICO ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 23. MEXICO ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 24. EUROPE ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 25. EUROPE ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 26. EUROPE ELECTRONIC COMPONENTS MARKET, BY COUNTRY, 2023-2032 ($BILLION)

- TABLE 27. UK ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 28. UK ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 29. GERMANY ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 30. GERMANY ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 31. FRANCE ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 32. FRANCE ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 33. ITALY ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 34. ITALY ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 35. REST OF EUROPE ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 36. REST OF EUROPE ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 37. ASIA-PACIFIC ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 38. ASIA-PACIFIC ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 39. ASIA-PACIFIC ELECTRONIC COMPONENTS MARKET, BY COUNTRY, 2023-2032 ($BILLION)

- TABLE 40. CHINA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 41. CHINA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 42. JAPAN ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 43. JAPAN ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 44. INDIA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 45. INDIA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 46. SOUTH KOREA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 47. SOUTH KOREA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 48. REST OF ASIA-PACIFIC ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 49. REST OF ASIA-PACIFIC ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 50. LATIN AMERICA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 51. LATIN AMERICA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 52. LATIN AMERICA ELECTRONIC COMPONENTS MARKET, BY COUNTRY, 2023-2032 ($BILLION)

- TABLE 53. BRAZIL ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 54. BRAZIL ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 55. ARGENTINA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 56. ARGENTINA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 57. REST OF LATIN AMERICA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 58. REST OF LATIN AMERICA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 59. MIDDLE EAST AND AFRICA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 60. MIDDLE EAST AND AFRICA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 61. MIDDLE EAST AND AFRICA ELECTRONIC COMPONENTS MARKET, BY COUNTRY, 2023-2032 ($BILLION)

- TABLE 62. UAE ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 63. UAE ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 64. SAUDI ARABIA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 65. SAUDI ARABIA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 66. REST OF MIDDLE EAST AND AFRICA ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023-2032 ($BILLION)

- TABLE 67. REST OF MIDDLE EAST AND AFRICA ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023-2032 ($BILLION)

- TABLE 68. NXP SEMICONDUCTORS N.V.: KEY EXECUTIVES

- TABLE 69. NXP SEMICONDUCTORS N.V.: COMPANY SNAPSHOT

- TABLE 70. NXP SEMICONDUCTORS N.V.: PRODUCT SEGMENTS

- TABLE 71. NXP SEMICONDUCTORS N.V.: SERVICE SEGMENTS

- TABLE 72. NXP SEMICONDUCTORS N.V.: PRODUCT PORTFOLIO

- TABLE 73. NXP SEMICONDUCTORS N.V.: KEY STRATEGIES

- TABLE 74. PANASONIC CORPORATION: KEY EXECUTIVES

- TABLE 75. PANASONIC CORPORATION: COMPANY SNAPSHOT

- TABLE 76. PANASONIC CORPORATION: PRODUCT SEGMENTS

- TABLE 77. PANASONIC CORPORATION: SERVICE SEGMENTS

- TABLE 78. PANASONIC CORPORATION: PRODUCT PORTFOLIO

- TABLE 79. PANASONIC CORPORATION: KEY STRATEGIES

- TABLE 80. RENESAS ELECTRIC CORPORATION: KEY EXECUTIVES

- TABLE 81. RENESAS ELECTRIC CORPORATION: COMPANY SNAPSHOT

- TABLE 82. RENESAS ELECTRIC CORPORATION: PRODUCT SEGMENTS

- TABLE 83. RENESAS ELECTRIC CORPORATION: SERVICE SEGMENTS

- TABLE 84. RENESAS ELECTRIC CORPORATION: PRODUCT PORTFOLIO

- TABLE 85. RENESAS ELECTRIC CORPORATION: KEY STRATEGIES

- TABLE 86. API TECHNOLOGIES CORP: KEY EXECUTIVES

- TABLE 87. API TECHNOLOGIES CORP: COMPANY SNAPSHOT

- TABLE 88. API TECHNOLOGIES CORP: PRODUCT SEGMENTS

- TABLE 89. API TECHNOLOGIES CORP: SERVICE SEGMENTS

- TABLE 90. API TECHNOLOGIES CORP: PRODUCT PORTFOLIO

- TABLE 91. API TECHNOLOGIES CORP: KEY STRATEGIES

- TABLE 92. AVX CORPORATION: KEY EXECUTIVES

- TABLE 93. AVX CORPORATION: COMPANY SNAPSHOT

- TABLE 94. AVX CORPORATION: PRODUCT SEGMENTS

- TABLE 95. AVX CORPORATION: SERVICE SEGMENTS

- TABLE 96. AVX CORPORATION: PRODUCT PORTFOLIO

- TABLE 97. AVX CORPORATION: KEY STRATEGIES

- TABLE 98. EATON CORP.: KEY EXECUTIVES

- TABLE 99. EATON CORP.: COMPANY SNAPSHOT

- TABLE 100. EATON CORP.: PRODUCT SEGMENTS

- TABLE 101. EATON CORP.: SERVICE SEGMENTS

- TABLE 102. EATON CORP.: PRODUCT PORTFOLIO

- TABLE 103. EATON CORP.: KEY STRATEGIES

- TABLE 104. DATRONIX HOLDINGS: KEY EXECUTIVES

- TABLE 105. DATRONIX HOLDINGS: COMPANY SNAPSHOT

- TABLE 106. DATRONIX HOLDINGS: PRODUCT SEGMENTS

- TABLE 107. DATRONIX HOLDINGS: SERVICE SEGMENTS

- TABLE 108. DATRONIX HOLDINGS: PRODUCT PORTFOLIO

- TABLE 109. DATRONIX HOLDINGS: KEY STRATEGIES

- TABLE 110. FUJITSU COMPONENT: KEY EXECUTIVES

- TABLE 111. FUJITSU COMPONENT: COMPANY SNAPSHOT

- TABLE 112. FUJITSU COMPONENT: PRODUCT SEGMENTS

- TABLE 113. FUJITSU COMPONENT: SERVICE SEGMENTS

- TABLE 114. FUJITSU COMPONENT: PRODUCT PORTFOLIO

- TABLE 115. FUJITSU COMPONENT: KEY STRATEGIES

- TABLE 116. FCI ELECTRONICS: KEY EXECUTIVES

- TABLE 117. FCI ELECTRONICS: COMPANY SNAPSHOT

- TABLE 118. FCI ELECTRONICS: PRODUCT SEGMENTS

- TABLE 119. FCI ELECTRONICS: SERVICE SEGMENTS

- TABLE 120. FCI ELECTRONICS: PRODUCT PORTFOLIO

- TABLE 121. FCI ELECTRONICS: KEY STRATEGIES

- TABLE 122. HITACHI AIC: KEY EXECUTIVES

- TABLE 123. HITACHI AIC: COMPANY SNAPSHOT

- TABLE 124. HITACHI AIC: PRODUCT SEGMENTS

- TABLE 125. HITACHI AIC: SERVICE SEGMENTS

- TABLE 126. HITACHI AIC: PRODUCT PORTFOLIO

- TABLE 127. HITACHI AIC: KEY STRATEGIES

LIST OF FIGURES

- FIGURE 01. ELECTRONIC COMPONENTS MARKET, 2023-2032

- FIGURE 02. SEGMENTATION OF ELECTRONIC COMPONENTS MARKET,2023-2032

- FIGURE 03. TOP IMPACTING FACTORS IN ELECTRONIC COMPONENTS MARKET

- FIGURE 04. TOP INVESTMENT POCKETS IN ELECTRONIC COMPONENTS MARKET (2024-2032)

- FIGURE 05. BARGAINING POWER OF SUPPLIERS

- FIGURE 06. BARGAINING POWER OF BUYERS

- FIGURE 07. THREAT OF SUBSTITUTION

- FIGURE 08. THREAT OF SUBSTITUTION

- FIGURE 09. COMPETITIVE RIVALRY

- FIGURE 10. GLOBAL ELECTRONIC COMPONENTS MARKET:DRIVERS, RESTRAINTS AND OPPORTUNITIES

- FIGURE 11. ELECTRONIC COMPONENTS MARKET, BY TYPE, 2023 AND 2032(%)

- FIGURE 12. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR ACTIVE COMPONENTS, BY COUNTRY 2023 AND 2032(%)

- FIGURE 13. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR PASSIVE COMPONENTS, BY COUNTRY 2023 AND 2032(%)

- FIGURE 14. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR ELECTROMECHANICAL COMPONENTS, BY COUNTRY 2023 AND 2032(%)

- FIGURE 15. ELECTRONIC COMPONENTS MARKET, BY APPLICATION, 2023 AND 2032(%)

- FIGURE 16. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR CONSUMER ELECTRONICS, BY COUNTRY 2023 AND 2032(%)

- FIGURE 17. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR AUTOMOTIVE, BY COUNTRY 2023 AND 2032(%)

- FIGURE 18. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR INDUSTRIAL AUTOMATION, BY COUNTRY 2023 AND 2032(%)

- FIGURE 19. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR TELECOMMUNICATION, BY COUNTRY 2023 AND 2032(%)

- FIGURE 20. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR AEROSPACE AND DEFENSE, BY COUNTRY 2023 AND 2032(%)

- FIGURE 21. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR HEALTHCARE, BY COUNTRY 2023 AND 2032(%)

- FIGURE 22. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR ENERGY AND POWER, BY COUNTRY 2023 AND 2032(%)

- FIGURE 23. COMPARATIVE SHARE ANALYSIS OF ELECTRONIC COMPONENTS MARKET FOR OTHERS, BY COUNTRY 2023 AND 2032(%)

- FIGURE 24. ELECTRONIC COMPONENTS MARKET BY REGION, 2023 AND 2032(%)

- FIGURE 25. U.S. ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 26. CANADA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 27. MEXICO ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 28. UK ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 29. GERMANY ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 30. FRANCE ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 31. ITALY ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 32. REST OF EUROPE ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 33. CHINA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 34. JAPAN ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 35. INDIA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 36. SOUTH KOREA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 37. REST OF ASIA-PACIFIC ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 38. BRAZIL ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 39. ARGENTINA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 40. REST OF LATIN AMERICA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 41. UAE ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 42. SAUDI ARABIA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 43. REST OF MIDDLE EAST AND AFRICA ELECTRONIC COMPONENTS MARKET, 2023-2032 ($BILLION)

- FIGURE 44. TOP WINNING STRATEGIES, BY YEAR

- FIGURE 45. TOP WINNING STRATEGIES, BY DEVELOPMENT

- FIGURE 46. TOP WINNING STRATEGIES, BY COMPANY

- FIGURE 47. PRODUCT MAPPING OF TOP 10 PLAYERS

- FIGURE 48. COMPETITIVE DASHBOARD

- FIGURE 49. COMPETITIVE HEATMAP: ELECTRONIC COMPONENTS MARKET

- FIGURE 50. TOP PLAYER POSITIONING, 2023

全球光隔离器市场

全球光隔离器市场 2032 年电子元件市场预测:按元件类型、材料、技术、分销管道、应用、最终用户和地区进行的全球分析通用电子元件市场:依元件类型、功能、最终用途产业及地区划分

2032 年电子元件市场预测:按元件类型、材料、技术、分销管道、应用、最终用户和地区进行的全球分析通用电子元件市场:依元件类型、功能、最终用途产业及地区划分 2025年通用电子元件全球市场报告2025 年光隔离器全球市场报告2025 年全球电气和电子元件市场报告3D 列印半导体零件市场分析及预测(截至 2033 年),按类型、产品、服务、技术、组件、应用、材料类型、设备、製程、最终用户划分

2025年通用电子元件全球市场报告2025 年光隔离器全球市场报告2025 年全球电气和电子元件市场报告3D 列印半导体零件市场分析及预测(截至 2033 年),按类型、产品、服务、技术、组件、应用、材料类型、设备、製程、最终用户划分 电子元件分销市场:按类型、分销管道、最终应用分类 - 2025-2030 年全球预测电子元件服务市场:按服务类型、按元件类型、按最终用途行业、按分销管道 - 全球预测 2025-2030

电子元件分销市场:按类型、分销管道、最终应用分类 - 2025-2030 年全球预测电子元件服务市场:按服务类型、按元件类型、按最终用途行业、按分销管道 - 全球预测 2025-2030 亚太地区 C 零件市场规模和预测、区域份额、趋势和成长机会分析报告范围:按产品类型、最终用途行业、材料类型和国家/地区

亚太地区 C 零件市场规模和预测、区域份额、趋势和成长机会分析报告范围:按产品类型、最终用途行业、材料类型和国家/地区