|

市场调查报告书

商品编码

1641752

全球鼻腔给药装置市场(按系统、容器和应用)- 机会分析和产业预测(2024-2033 年)Intranasal Drug Delivery Devices Market By System , By Container By Application : Global Opportunity Analysis and Industry Forecast, 2024-2033 |

||||||

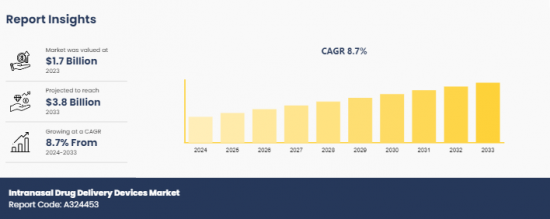

2023 年全球鼻腔给药装置市场规模价值为 17 亿美元,预计到 2033 年将达到 38 亿美元,2024 年至 2033 年的复合年增长率为 8.7%。

鼻腔给药装置是用于透过鼻腔给药治疗药物的医疗设备。这种给药途径提供了一种非侵入性且有效的方法,可以将药物直接输送到全身循环或靶向中枢神经系统,绕过胃肠道和肝臟的首过代谢。鼻用装置通常包括鼻用喷雾器、雾化器和粉末分配器,用于增强药物在鼻黏膜的吸收。

全球鼻腔给药设备市场的成长是由呼吸道疾病、过敏、偏头痛以及癫痫和阿片类药物过量摄取等需要快速用药的疾病盛行率的惊人上升所推动的。根据公共卫生研究机构卫生指标与评估研究所发布的研究报告,2019年,慢性呼吸道疾病导致400万人死亡,罹病人数达4.546亿,排名第三。此外,患者对非侵入性药物传递方法的需求激增,推动了鼻腔装置在慢性和急性疾病中的应用。此外,鼻腔给药可有效地针对中枢神经系统,因为它允许药物绕过血脑障壁。这促进了阿兹海默症和帕金森氏症等神经系统疾病的治疗研究。此外,家庭保健和自我治疗的兴起趋势推动了对易于使用的药物输送系统(包括鼻用装置)的需求,从而极大地推动了市场成长。然而,频繁使用鼻用设备会对鼻黏膜造成刺激、干燥和其他不适,从而限制了其应用并阻碍了市场成长。此外,由于稳定性问题或鼻黏膜渗透性差,并非所有药物都适合经鼻给药,这限制了这些装置的应用范围。同时,滴鼻剂和无针装置等创新正在提高药物输送的精确度和便利性。用于剂量追踪的整合感测器的智慧型设备也正在涌现,提高了患者对药物的依从性。预计这些发展将为预测期内全球市场的扩张提供有利可图的机会。

鼻腔给药装置产业分为系统、容器、应用和地区。根据系统,市场分为定量系统、多剂量系统和单位剂量系统。依容器类型分为非压力容器和压力容器。依用途可分为慢性阻塞性肺病(COPD)、鼻炎、囊肿纤维化、鼻塞、气喘等。按地区分析,市场涵盖北美、欧洲、亚太地区、拉丁美洲、中东和非洲。

主要发现

根据系统,多剂量系统部分预计将在 2024-2033 年期间占据市场主导地位。

根据船舶类型,非加压系统船舶部分预计在预测期内呈现最高成长。

根据应用,预计气喘领域在不久的将来将以惊人的速度成长。

根据地区,预计北美将在 2023 年占据鼻腔给药装置市场最大的市场占有率,并预计在预测期内占据市场主导地位。

本报告可提供客製化(请联络销售人员以了解其他费用和时间表)

- 根据客户兴趣加入公司简介

- 历史市场资料

- 导入/汇出分析/资料

目录

第 1 章 简介

第 2 章执行摘要

第三章 市场状况

- 市场定义和范围

- 主要发现

- 主要投资机会

- 关键成功策略

- 波特五力分析

- 市场动态

- 驱动程式

- 限制因素

- 机会

第四章。

- 市场概况

- 固定剂量

- 多剂量系统

- 单位剂量系统

第五章 鼻腔给药装置市场(依容器划分)

- 市场概况

- 非加压容器

- 压力容器

第六章 鼻腔给药装置市场(依应用)

- 市场概况

- 慢性阻塞性肺病

- 鼻炎

- 囊肿纤维化

- 鼻塞

- 气喘

- 其他的

7. 鼻腔给药装置市场(按地区)

- 市场概况

- 北美洲

- 主要市场趋势和机会

- 美国鼻腔给药装置市场

- 加拿大鼻腔给药装置市场

- 墨西哥鼻腔给药装置市场

- 欧洲

- 主要市场趋势和机会

- 法国鼻腔给药装置市场

- 德国鼻腔给药装置市场

- 义大利鼻腔给药装置市场

- 西班牙鼻腔给药装置市场

- 英国鼻腔给药装置市场

- 其他欧洲国家鼻腔给药装置市场

- 亚太地区

- 主要市场趋势和机会

- 中国鼻腔给药装置市场

- 日本鼻腔给药装置市场

- 印度鼻腔给药设备市场

- 韩国鼻腔给药装置市场

- 澳洲鼻腔给药装置市场

- 其他亚太地区鼻腔给药装置市场

- 拉丁美洲、中东和非洲

- 主要市场趋势和机会

- 巴西鼻腔给药装置市场

- 南非鼻腔给药装置市场

- 沙乌地阿拉伯的鼻腔给药装置市场

- 其他拉丁美洲、中东和非洲鼻腔给药装置市场

第八章 竞争格局

- 介绍

- 关键成功策略

- 前 10 家公司的产品映射

- 竞争仪錶板

- 竞争热图

- 主要企业的定位:2023年

第九章 公司简介

- AptarGroup, Inc.

- Teleflex Incorporated

- Nemera

- Becton, Dickinson And Company

- OptiNose, Inc.

- GlaxoSmithKline Plc.

- AstraZeneca

- Kurve Technology, Inc.

- Johnson And Johnson

- Merck And Co., Inc.

The intranasal drug delivery devices market was valued at $1.7 billion in 2023, and is projected to reach $3.8 billion by 2033, growing at a CAGR of 8.7% from 2024 to 2033.

Intranasal drug delivery devices are medical devices designed to administer therapeutic agents through the nasal cavity. This route of administration provides a non-invasive and efficient means to deliver drugs directly into the systemic circulation or target the central nervous system, bypassing the gastrointestinal tract and first-pass metabolism in the liver. Intranasal devices commonly include nasal sprays, nebulizers, and powder dispensers, tailored to enhance drug absorption through the nasal mucosa.

The growth of the global intranasal drug delivery devices market is driven by alarming increase in prevalence of respiratory diseases, allergies, migraines as well as conditions requiring rapid drug action, such as epilepsy and opioid overdose. According to a study published by the Institute for Health Metrics and Evaluation-a public health research institute-chronic respiratory diseases were responsible for 4.0 million deaths with a prevalence of 454.6 million cases in 2019, ranking as the third leading cause of death. In addition, surge in demand for non-invasive drug delivery methods among patients is boosting the adoption of intranasal devices for both chronic and acute conditions. Moreover, intranasal drug delivery is effective in targeting the central nervous system, as it allows drugs to bypass the blood-brain barrier. This is fostering research into treatments for neurological disorders, such as Alzheimer's and Parkinson's disease. Furthermore, rise of home healthcare and self-medication trends is driving the demand for easy-to-use drug delivery systems, including intranasal devices, which significantly fosters the market growth. However, frequent use of intranasal devices may cause irritation, dryness, or other discomfort in the nasal mucosa, which limits their adoption, thereby hampering the market growth. In addition, not all drugs are suitable for intranasal delivery due to stability issues or low permeability through the nasal mucosa, which restricts the range of applications for these devices. On the contrary, innovations such as metered-dose nasal sprays and needle-free devices improve drug delivery precision and user-friendliness. Smart devices integrated with sensors for dose tracking are also emerging, enhancing patient adherence. Such developments are expected to offer remunerative opportunities for the expansion of the global market during the forecast.

The intranasal drug delivery devices industry is segmented into system, container, application, and region. By system, the market is segregated into metered dose, multi-dose systems, and unit-dose systems. On the basis of containers, it is bifurcated into non-pressurized containers and pressurized containers. Depending on application, it is divided into chronic obstructive pulmonary disease (COPD) , rhinitis, cystic fibrosis, nasal congestion, asthma, and others. Region wise, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA.

Key Findings

By system, the multi-dose systems segment is expected to dominate the market from 2024 to 2033.

On the basis of container, the non-pressurized system containers segment is anticipated to exhibit the highest growth during the forecast period.

Depending on application, the asthma segment is projected to grow at a notable pace in the near future.

Region wise, North America held the largest market share in the intranasal drug delivery devices market in 2023, and is expected to dominate the market during the forecast period.

Competition Analysis

Competitive analysis and profiles of the major players in the global intranasal drug delivery devices market include AptarGroup, Inc., Teleflex Incorporated, Nemera, Becton, Dickinson and Company, OptiNose, Inc., GlaxoSmithKline Plc., AstraZeneca, Kurve Technology, Inc., Johnson & Johnson, and Merck & Co., Inc. These major players have adopted various key development strategies such as business expansion, new product launches, and partnerships to sustain the intense competition and gain a strong foothold in the global market.

Additional benefits you will get with this purchase are:

- Quarterly Update and* (only available with a corporate license, on listed price)

- 5 additional Company Profile of client Choice pre- or Post-purchase, as a free update.

- Free Upcoming Version on the Purchase of Five and Enterprise User License.

- 16 analyst hours of support* (post-purchase, if you find additional data requirements upon review of the report, you may receive support amounting to 16 analyst hours to solve questions, and post-sale queries)

- 15% Free Customization* (in case the scope or segment of the report does not match your requirements, 15% is equivalent to 3 working days of free work, applicable once)

- Free data Pack on the Five and Enterprise User License. (Excel version of the report)

- Free Updated report if the report is 6-12 months old or older.

- 24-hour priority response*

- Free Industry updates and white papers.

Possible Customization with this report (with additional cost and timeline, please talk to the sales executive to know more)

- Additional company profiles with specific to client's interest

- Historic market data

- Import Export Analysis/Data

Key Market Segments

By System

- Metered Dose

- Multi-Dose Systems

- Unit-Dose Systems

By Container

- Non-Pressurized Containers

- Pressurized Containers

By Application

- Chronic Obstructive Pulmonary Disease

- Rhinitis

- Cystic Fibrosis

- Nasal Congestion

- Others

By Region

- North America

- U.S.

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- Spain

- UK

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- LAMEA

- Brazil

- South Africa

- Saudi Arabia

- Rest of LAMEA

Key Market Players:

- AptarGroup, Inc.

- Teleflex Incorporated

- nemera

- Becton, Dickinson and Company

- OptiNose, Inc.

- GlaxoSmithKline plc.

- AstraZeneca

- Kurve Technology, Inc.

- Johnson & Johnson

- Merck & Co., Inc.

TABLE OF CONTENTS

CHAPTER 1: INTRODUCTION

- 1.1. Report Description

- 1.2. Key Market Segments

- 1.3. Key Benefits

- 1.4. Research Methodology

- 1.4.1. Primary Research

- 1.4.2. Secondary Research

- 1.4.3. Analyst Tools and Models

CHAPTER 2: EXECUTIVE SUMMARY

- 2.1. CXO Perspective

CHAPTER 3: MARKET LANDSCAPE

- 3.1. Market Definition and Scope

- 3.2. Key Findings

- 3.2.1. Top Investment Pockets

- 3.2.2. Top Winning Strategies

- 3.3. Porter's Five Forces Analysis

- 3.3.1. Bargaining Power of Suppliers

- 3.3.2. Threat of New Entrants

- 3.3.3. Threat of Substitutes

- 3.3.4. Competitive Rivalry

- 3.3.5. Bargaining Power among Buyers

- 3.4. Market Dynamics

- 3.4.1. Drivers

- 3.4.2. Restraints

- 3.4.3. Opportunities

CHAPTER 4: INTRANASAL DRUG DELIVERY DEVICES MARKET, BY SYSTEM

- 4.1. Market Overview

- 4.1.1 Market Size and Forecast, By System

- 4.2. Metered Dose

- 4.2.1. Key Market Trends, Growth Factors and Opportunities

- 4.2.2. Market Size and Forecast, By Region

- 4.2.3. Market Share Analysis, By Country

- 4.3. Multi-Dose Systems

- 4.3.1. Key Market Trends, Growth Factors and Opportunities

- 4.3.2. Market Size and Forecast, By Region

- 4.3.3. Market Share Analysis, By Country

- 4.4. Unit-Dose Systems

- 4.4.1. Key Market Trends, Growth Factors and Opportunities

- 4.4.2. Market Size and Forecast, By Region

- 4.4.3. Market Share Analysis, By Country

CHAPTER 5: INTRANASAL DRUG DELIVERY DEVICES MARKET, BY CONTAINER

- 5.1. Market Overview

- 5.1.1 Market Size and Forecast, By Container

- 5.2. Non-Pressurized Containers

- 5.2.1. Key Market Trends, Growth Factors and Opportunities

- 5.2.2. Market Size and Forecast, By Region

- 5.2.3. Market Share Analysis, By Country

- 5.3. Pressurized Containers

- 5.3.1. Key Market Trends, Growth Factors and Opportunities

- 5.3.2. Market Size and Forecast, By Region

- 5.3.3. Market Share Analysis, By Country

CHAPTER 6: INTRANASAL DRUG DELIVERY DEVICES MARKET, BY APPLICATION

- 6.1. Market Overview

- 6.1.1 Market Size and Forecast, By Application

- 6.2. Chronic Obstructive Pulmonary Disease

- 6.2.1. Key Market Trends, Growth Factors and Opportunities

- 6.2.2. Market Size and Forecast, By Region

- 6.2.3. Market Share Analysis, By Country

- 6.3. Rhinitis

- 6.3.1. Key Market Trends, Growth Factors and Opportunities

- 6.3.2. Market Size and Forecast, By Region

- 6.3.3. Market Share Analysis, By Country

- 6.4. Cystic Fibrosis

- 6.4.1. Key Market Trends, Growth Factors and Opportunities

- 6.4.2. Market Size and Forecast, By Region

- 6.4.3. Market Share Analysis, By Country

- 6.5. Nasal Congestion

- 6.5.1. Key Market Trends, Growth Factors and Opportunities

- 6.5.2. Market Size and Forecast, By Region

- 6.5.3. Market Share Analysis, By Country

- 6.6. Others

- 6.6.1. Key Market Trends, Growth Factors and Opportunities

- 6.6.2. Market Size and Forecast, By Region

- 6.6.3. Market Share Analysis, By Country

CHAPTER 7: INTRANASAL DRUG DELIVERY DEVICES MARKET, BY REGION

- 7.1. Market Overview

- 7.1.1 Market Size and Forecast, By Region

- 7.2. North America

- 7.2.1. Key Market Trends and Opportunities

- 7.2.2. Market Size and Forecast, By System

- 7.2.3. Market Size and Forecast, By Container

- 7.2.4. Market Size and Forecast, By Application

- 7.2.5. Market Size and Forecast, By Country

- 7.2.6. U.S. Intranasal Drug Delivery Devices Market

- 7.2.6.1. Market Size and Forecast, By System

- 7.2.6.2. Market Size and Forecast, By Container

- 7.2.6.3. Market Size and Forecast, By Application

- 7.2.7. Canada Intranasal Drug Delivery Devices Market

- 7.2.7.1. Market Size and Forecast, By System

- 7.2.7.2. Market Size and Forecast, By Container

- 7.2.7.3. Market Size and Forecast, By Application

- 7.2.8. Mexico Intranasal Drug Delivery Devices Market

- 7.2.8.1. Market Size and Forecast, By System

- 7.2.8.2. Market Size and Forecast, By Container

- 7.2.8.3. Market Size and Forecast, By Application

- 7.3. Europe

- 7.3.1. Key Market Trends and Opportunities

- 7.3.2. Market Size and Forecast, By System

- 7.3.3. Market Size and Forecast, By Container

- 7.3.4. Market Size and Forecast, By Application

- 7.3.5. Market Size and Forecast, By Country

- 7.3.6. France Intranasal Drug Delivery Devices Market

- 7.3.6.1. Market Size and Forecast, By System

- 7.3.6.2. Market Size and Forecast, By Container

- 7.3.6.3. Market Size and Forecast, By Application

- 7.3.7. Germany Intranasal Drug Delivery Devices Market

- 7.3.7.1. Market Size and Forecast, By System

- 7.3.7.2. Market Size and Forecast, By Container

- 7.3.7.3. Market Size and Forecast, By Application

- 7.3.8. Italy Intranasal Drug Delivery Devices Market

- 7.3.8.1. Market Size and Forecast, By System

- 7.3.8.2. Market Size and Forecast, By Container

- 7.3.8.3. Market Size and Forecast, By Application

- 7.3.9. Spain Intranasal Drug Delivery Devices Market

- 7.3.9.1. Market Size and Forecast, By System

- 7.3.9.2. Market Size and Forecast, By Container

- 7.3.9.3. Market Size and Forecast, By Application

- 7.3.10. UK Intranasal Drug Delivery Devices Market

- 7.3.10.1. Market Size and Forecast, By System

- 7.3.10.2. Market Size and Forecast, By Container

- 7.3.10.3. Market Size and Forecast, By Application

- 7.3.11. Rest Of Europe Intranasal Drug Delivery Devices Market

- 7.3.11.1. Market Size and Forecast, By System

- 7.3.11.2. Market Size and Forecast, By Container

- 7.3.11.3. Market Size and Forecast, By Application

- 7.4. Asia-Pacific

- 7.4.1. Key Market Trends and Opportunities

- 7.4.2. Market Size and Forecast, By System

- 7.4.3. Market Size and Forecast, By Container

- 7.4.4. Market Size and Forecast, By Application

- 7.4.5. Market Size and Forecast, By Country

- 7.4.6. China Intranasal Drug Delivery Devices Market

- 7.4.6.1. Market Size and Forecast, By System

- 7.4.6.2. Market Size and Forecast, By Container

- 7.4.6.3. Market Size and Forecast, By Application

- 7.4.7. Japan Intranasal Drug Delivery Devices Market

- 7.4.7.1. Market Size and Forecast, By System

- 7.4.7.2. Market Size and Forecast, By Container

- 7.4.7.3. Market Size and Forecast, By Application

- 7.4.8. India Intranasal Drug Delivery Devices Market

- 7.4.8.1. Market Size and Forecast, By System

- 7.4.8.2. Market Size and Forecast, By Container

- 7.4.8.3. Market Size and Forecast, By Application

- 7.4.9. South Korea Intranasal Drug Delivery Devices Market

- 7.4.9.1. Market Size and Forecast, By System

- 7.4.9.2. Market Size and Forecast, By Container

- 7.4.9.3. Market Size and Forecast, By Application

- 7.4.10. Australia Intranasal Drug Delivery Devices Market

- 7.4.10.1. Market Size and Forecast, By System

- 7.4.10.2. Market Size and Forecast, By Container

- 7.4.10.3. Market Size and Forecast, By Application

- 7.4.11. Rest of Asia-Pacific Intranasal Drug Delivery Devices Market

- 7.4.11.1. Market Size and Forecast, By System

- 7.4.11.2. Market Size and Forecast, By Container

- 7.4.11.3. Market Size and Forecast, By Application

- 7.5. LAMEA

- 7.5.1. Key Market Trends and Opportunities

- 7.5.2. Market Size and Forecast, By System

- 7.5.3. Market Size and Forecast, By Container

- 7.5.4. Market Size and Forecast, By Application

- 7.5.5. Market Size and Forecast, By Country

- 7.5.6. Brazil Intranasal Drug Delivery Devices Market

- 7.5.6.1. Market Size and Forecast, By System

- 7.5.6.2. Market Size and Forecast, By Container

- 7.5.6.3. Market Size and Forecast, By Application

- 7.5.7. South Africa Intranasal Drug Delivery Devices Market

- 7.5.7.1. Market Size and Forecast, By System

- 7.5.7.2. Market Size and Forecast, By Container

- 7.5.7.3. Market Size and Forecast, By Application

- 7.5.8. Saudi Arabia Intranasal Drug Delivery Devices Market

- 7.5.8.1. Market Size and Forecast, By System

- 7.5.8.2. Market Size and Forecast, By Container

- 7.5.8.3. Market Size and Forecast, By Application

- 7.5.9. Rest of LAMEA Intranasal Drug Delivery Devices Market

- 7.5.9.1. Market Size and Forecast, By System

- 7.5.9.2. Market Size and Forecast, By Container

- 7.5.9.3. Market Size and Forecast, By Application

CHAPTER 8: COMPETITIVE LANDSCAPE

- 8.1. Introduction

- 8.2. Top Winning Strategies

- 8.3. Product Mapping Of Top 10 Player

- 8.4. Competitive Dashboard

- 8.5. Competitive Heatmap

- 8.6. Top Player Positioning, 2023

CHAPTER 9: COMPANY PROFILES

- 9.1. AptarGroup, Inc.

- 9.1.1. Company Overview

- 9.1.2. Key Executives

- 9.1.3. Company Snapshot

- 9.1.4. Operating Business Segments

- 9.1.5. Product Portfolio

- 9.1.6. Business Performance

- 9.1.7. Key Strategic Moves and Developments

- 9.2. Teleflex Incorporated

- 9.2.1. Company Overview

- 9.2.2. Key Executives

- 9.2.3. Company Snapshot

- 9.2.4. Operating Business Segments

- 9.2.5. Product Portfolio

- 9.2.6. Business Performance

- 9.2.7. Key Strategic Moves and Developments

- 9.3. Nemera

- 9.3.1. Company Overview

- 9.3.2. Key Executives

- 9.3.3. Company Snapshot

- 9.3.4. Operating Business Segments

- 9.3.5. Product Portfolio

- 9.3.6. Business Performance

- 9.3.7. Key Strategic Moves and Developments

- 9.4. Becton, Dickinson And Company

- 9.4.1. Company Overview

- 9.4.2. Key Executives

- 9.4.3. Company Snapshot

- 9.4.4. Operating Business Segments

- 9.4.5. Product Portfolio

- 9.4.6. Business Performance

- 9.4.7. Key Strategic Moves and Developments

- 9.5. OptiNose, Inc.

- 9.5.1. Company Overview

- 9.5.2. Key Executives

- 9.5.3. Company Snapshot

- 9.5.4. Operating Business Segments

- 9.5.5. Product Portfolio

- 9.5.6. Business Performance

- 9.5.7. Key Strategic Moves and Developments

- 9.6. GlaxoSmithKline Plc.

- 9.6.1. Company Overview

- 9.6.2. Key Executives

- 9.6.3. Company Snapshot

- 9.6.4. Operating Business Segments

- 9.6.5. Product Portfolio

- 9.6.6. Business Performance

- 9.6.7. Key Strategic Moves and Developments

- 9.7. AstraZeneca

- 9.7.1. Company Overview

- 9.7.2. Key Executives

- 9.7.3. Company Snapshot

- 9.7.4. Operating Business Segments

- 9.7.5. Product Portfolio

- 9.7.6. Business Performance

- 9.7.7. Key Strategic Moves and Developments

- 9.8. Kurve Technology, Inc.

- 9.8.1. Company Overview

- 9.8.2. Key Executives

- 9.8.3. Company Snapshot

- 9.8.4. Operating Business Segments

- 9.8.5. Product Portfolio

- 9.8.6. Business Performance

- 9.8.7. Key Strategic Moves and Developments

- 9.9. Johnson And Johnson

- 9.9.1. Company Overview

- 9.9.2. Key Executives

- 9.9.3. Company Snapshot

- 9.9.4. Operating Business Segments

- 9.9.5. Product Portfolio

- 9.9.6. Business Performance

- 9.9.7. Key Strategic Moves and Developments

- 9.10. Merck And Co., Inc.

- 9.10.1. Company Overview

- 9.10.2. Key Executives

- 9.10.3. Company Snapshot

- 9.10.4. Operating Business Segments

- 9.10.5. Product Portfolio

- 9.10.6. Business Performance

- 9.10.7. Key Strategic Moves and Developments