|

市场调查报告书

商品编码

1680167

全球国防涡轮喷射发动机市场:2025-2035年Global Defense Turbojet Engine Market 2025-2035 |

||||||

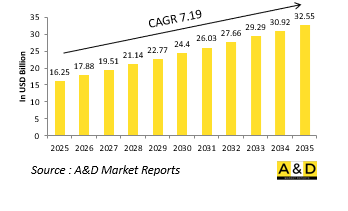

全球国防涡轮喷射发动机市场规模预计到2025年将成长至 162.5亿美元,到2035年将成长至 325.5亿美元,2025-2035年预测期内的年复合成长率(CAGR)为 7.19%。

全球国防涡轮喷射发动机市场仍然是军事航空领域的重要领域,为执行作战、侦察和战略防御任务的高速飞机提供动力。涡轮喷射发动机以超音速提供高推力而闻名,长期以来一直是战斗机、轰炸机和无人机系统(UAS)的支柱。现代战斗机日益转向涡轮扇发动机以实现更高的燃油效率和航程,但涡轮喷气发动机在某些国防应用中仍然发挥着重要作用,例如高速拦截器、巡航导弹和瞄准无人机。随着世界各国军队不断对其空军进行现代化改造,对先进涡轮喷射发动机的需求将保持稳定,特别是对于下一代飞弹系统和超音速无人机。市场上进行越来越多的研究和开发,致力于提高引擎性能、降低燃料消耗以及整合先进材料以提高耐用性和运行效率。随着地缘政治紧张局势加剧和空中优势投入不断增加,世界各国都优先研发和采购先进的涡轮喷射发动机,以维持空战战略优势。

技术进步塑造国防涡轮喷射发动机市场,创新重点是提高推力重量比、燃油效率和材料科学。其中最重要的进展之一是将先进的复合材料和陶瓷基复合材料(CMC)整合到引擎结构中,提高了耐热性并减轻了整体重量。这使得工作温度更高、引擎寿命更长,这些因素对于高性能军用航空非常重要。此外,完全授权数位引擎控制(FADEC)等数位引擎控制系统的引进提高了引擎的反应能力、最佳化了燃油消耗并提供了预测性维护功能,减少了停机时间和营运成本。另一个变革趋势是变循环引擎的不断发展,其中气流和燃烧特性可以即时调整。这种适应性强的引擎将提高军用飞机的多功能性,使其在亚音速飞行期间能够有效利用燃料,同时在需要时保持高速性能。积层製造(3D 列印)也彻底改变涡轮喷射发动机的製造过程,能够快速製作原型并生产结构完整性更高的复杂引擎零件。除了这些进步之外,对混合推进系统的研究也在增加,国防承包商探索将电气元件整合到涡轮喷气发动机设计中的可能性,以提高效率并减少热信号。

有几个关键因素推动了国防涡轮喷射发动机市场的成长,包括国防预算的增加、增强空战能力的需求以及飞弹技术的广泛采用。其中一个主要驱动因素是全球都强调维持空中优势,各国都在寻求开发和部署速度更快、能够超越对手的飞机。高超音速武器计画的兴起推动了对先进涡轮喷射发动机和冲压喷射发动机推进技术的投资增加,而主要军事大国为高速飞弹和无人平台开发下一代吸气式发动机。涡轮喷射发动机在巡航飞弹中的持续应用也是推动市场成长的主要因素。这些引擎提供了远程打击能力所需的速度和可靠性,使其成为任何现代军事武器库的重要组成部分。此外,用于侦察、作战和电子战的无人机系统的部署日益增多,推动了对更轻、推力更大的涡轮喷气发动机的需求,这些发动机可以支援快速机动性和延长飞行时间。人们对超音速战斗机(包括第六代战斗机计画)的兴趣日益浓厚,这也影响了涡轮喷射发动机的发展,军队寻求平衡速度、效率和隐身特性的推进解决方案。

国防涡轮喷射发动机市场的区域趋势因军事优先事项、技术能力和战略目标而异。北美仍然是涡轮喷射发动机发展的主导力量,美国在创新和生产方面都处于领先地位。美国军方对下一代飞机、高超音速武器和先进飞弹系统的投资推动对高性能涡轮喷射推进系统的持续研究。Pratt & Whitney、General Electric Aviation、Honeywell等领先的国防承包商处于开发尖端发动机技术的前沿,利用材料科学、数位控制系统、增材製造等领域的进步。美国空军致力于快速攻击能力,包括高超音速巡航飞弹和先进无人机,这将确保对涡轮喷射发动机解决方案的持续需求。此外,B-52 同温层堡垒等传统飞机的升级也在进行中,包括目的是提高燃油效率和性能的引擎现代化计划。加拿大虽然不是涡轮喷射发动机的主要生产国,但它在研发合作中发挥着重要作用,并支持北约的战略举措。

本报告涵盖全球国防涡轮喷射发动机市场,并提供了依细分市场的10年市场预测、技术趋势、机会分析、公司概况和国家资料。

目录

国防涡轮喷射发动机市场报告定义

国防涡轮喷射发动机市场细分

- 依地区

- 依用途

- 依最终用户

未来 10年国防涡轮喷射发动机市场分析

国防涡轮喷射发动机市场市场技术

全球国防涡轮喷射发动机市场预测

国防涡轮喷射发动机市场趋势与预测(依地区)

- 北美洲

- 驱动因素、限制因素与挑战

- PEST

- 大型公司

- 供应商层级结构

- 企业基准

- 市场预测与情境分析

- 欧洲

- 中东

- 亚太地区

- 南美洲

国防涡轮喷射发动机市场国家分析

- 美国

- 计划地图

- 最新消息

- 专利

- 目前该市场的技术成熟度

- 市场预测与情境分析

- 加拿大

- 义大利

- 法国

- 德国

- 荷兰

- 比利时

- 西班牙

- 瑞典

- 希腊

- 澳洲

- 南非

- 印度

- 中国

- 俄罗斯

- 韩国

- 日本

- 马来西亚

- 新加坡

- 巴西

国防涡轮喷射发动机市场机会矩阵

国防涡轮喷射发动机市场报告专家意见

结论

关于航空和国防市场报告

The Global defense turbojet engine market is estimated at USD 16.25 billion in 2025, projected to grow to USD 32.55 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 7.19% over the forecast period 2025-2035.

Introduction to Defense Turbojet Engine Market:

The global defense turbojet engine market remains a vital segment of military aviation, powering high-speed aircraft designed for combat, reconnaissance, and strategic defense missions. Turbojet engines, known for their ability to deliver high thrust at supersonic speeds, have long been a cornerstone of fighter jets, bombers, and unmanned aerial systems (UAS). While modern combat aircraft have largely transitioned to turbofan engines for greater fuel efficiency and range, turbojets still play a significant role in specific defense applications, including high-speed interceptor aircraft, cruise missiles, and target drones. As global military forces continue to modernize their air fleets, the demand for advanced turbojet engines remains steady, particularly for next-generation missile systems and supersonic UAVs. The market is witnessing ongoing research and development efforts focused on enhancing engine performance, reducing fuel consumption, and integrating cutting-edge materials that improve durability and operational efficiency. With rising geopolitical tensions and increased investments in air superiority, countries across the world are prioritizing the development and procurement of advanced turbojet engines to maintain strategic advantages in aerial combat.

Technology Impact in Defense Turbojet Engine Market:

Technological advancements are shaping the defense turbojet engine market, with innovations focused on thrust-to-weight ratio improvements, fuel efficiency, and materials science. One of the most significant developments is the integration of advanced composite materials and ceramic matrix composites (CMCs) into engine construction, which enhances thermal resistance and reduces overall weight. This allows for higher operational temperatures and improved engine longevity, crucial factors in high-performance military aviation. Additionally, the incorporation of digital engine control systems, such as Full Authority Digital Engine Control (FADEC), has improved engine responsiveness, optimized fuel consumption, and provided predictive maintenance capabilities, reducing downtime and operational costs. The ongoing development of variable cycle engines, which can adjust airflow and combustion characteristics in real-time, is another transformative trend. These adaptive engines enable greater versatility in military aircraft, allowing for efficient fuel use during subsonic flight while maintaining high-speed performance when needed. Additive manufacturing, or 3D printing, has also revolutionized turbojet production, allowing for rapid prototyping and the creation of complex engine components with improved structural integrity. In addition to these advancements, research into hybrid propulsion systems is gaining traction, with defense contractors exploring the potential for integrating electrical components into turbojet designs to enhance efficiency and reduce thermal signatures.

Key Drivers in Defense Turbojet Engine Market:

Several key factors are driving the growth of the defense turbojet engine market, including increasing defense budgets, the need for enhanced aerial combat capabilities, and the proliferation of missile technology. One of the primary drivers is the global emphasis on maintaining air superiority, as nations seek to develop and deploy high-speed aircraft capable of outmaneuvering adversaries. The rise of hypersonic weapons programs has further intensified investments in advanced turbojet and ramjet propulsion technologies, with leading military powers developing next-generation air-breathing engines for high-speed missiles and unmanned platforms. The continued relevance of turbojet engines in cruise missiles is another major factor propelling market growth. These engines provide the necessary speed and reliability for long-range strike capabilities, making them an essential component of modern military arsenals. In addition, the increasing deployment of unmanned aerial systems for reconnaissance, combat, and electronic warfare applications is driving demand for lightweight, high-thrust turbojet engines capable of supporting rapid maneuverability and extended flight durations. The resurgence of interest in supersonic combat aircraft, including sixth-generation fighter programs, is also influencing turbojet engine development, as military forces seek propulsion solutions that balance speed, efficiency, and stealth characteristics.

Regional Trends in Defense Turbojet Engine Market:

Regional trends in the defense turbojet engine market vary based on military priorities, technological capabilities, and strategic objectives. North America remains a dominant force in turbojet engine development, with the United States leading in both innovation and production. The U.S. military's investments in next-generation aircraft, hypersonic weapons, and advanced missile systems are driving continued research into high-performance turbojet propulsion. Major defense contractors such as Pratt & Whitney, General Electric Aviation, and Honeywell are at the forefront of developing cutting-edge engine technologies, leveraging advancements in materials science, digital control systems, and additive manufacturing. The U.S. Air Force's focus on high-speed strike capabilities, including hypersonic cruise missiles and advanced UAVs, ensures sustained demand for turbojet engine solutions. Additionally, ongoing upgrades to legacy aircraft, such as the B-52 Stratofortress, include engine modernization programs aimed at improving fuel efficiency and performance. Canada, while not a major producer of turbojet engines, remains an important player in research and development collaborations, supporting NATO's strategic initiatives.

In Europe, the defense turbojet engine market is driven by multinational defense projects and a strong emphasis on indigenous engine development. Countries such as France, the United Kingdom, and Germany are leading the charge in high-performance military propulsion technologies, with companies like Rolls-Royce, Safran Aircraft Engines, and MTU Aero Engines developing advanced turbojet and turbofan solutions. The Future Combat Air System (FCAS) and Tempest programs, spearheaded by European nations, include significant investments in next-generation propulsion technologies, ensuring continued advancements in turbojet engine capabilities. France's Safran has been actively working on high-thrust military engines, supporting both national defense programs and international collaborations. The United Kingdom's Rolls-Royce has played a crucial role in developing advanced propulsion solutions for both manned and unmanned aircraft, including efforts to integrate variable cycle engines into future fighter jets. Additionally, Europe's emphasis on cruise missile development, including the MBDA Storm Shadow and the Meteor air-to-air missile, has driven demand for compact, high-efficiency turbojet engines tailored for missile applications.

The Asia-Pacific region is witnessing rapid growth in the defense turbojet engine market, fueled by increasing military expenditures, indigenous defense manufacturing initiatives, and regional security concerns. China has emerged as a major player, investing heavily in the development of high-performance jet engines to reduce reliance on foreign suppliers. The country's efforts to develop indigenous turbojet engines for fighter jets, UAVs, and missile systems underscore its ambition to achieve self-sufficiency in military propulsion technology. China's advancements in hypersonic weapons, including scramjet and ramjet propulsion research, further highlight its strategic focus on high-speed aerial warfare. India is also making significant strides in turbojet engine development, with the Gas Turbine Research Establishment (GTRE) working on indigenous jet propulsion solutions for combat aircraft and cruise missiles. Japan and South Korea, both key defense players in the region, are investing in next-generation propulsion technologies as part of their respective military modernization efforts. Japan's collaboration with international defense contractors on advanced fighter programs, such as the F-X stealth fighter, includes research into high-performance jet engines tailored for future aerial combat.

Key Defense Turbojet Engine Program:

AZAD Engineering Ltd has secured a contract from the Gas Turbine Research Establishment (GTRE), an R&D organization under the Defence Research and Development Organisation (DRDO) and the Union Defence Ministry, to develop advanced turbo engines for India's defense programs. The company announced that it has been selected as GTRE's exclusive industry partner to bring this design to fruition. The contract encompasses the full-scale manufacturing and assembly of a cutting-edge gas turbine engine essential for defense applications.

GE Aerospace has secured a $1.1 billion multiyear contract from the U.S. Department of Defense for the procurement of T700 turbine engines, which will power Army helicopters and support other military branches. Awarded on June 12, the contract is set to run until June 13, 2029, ensuring a steady supply of T700 engines for the Army's Apache and Black Hawk helicopters. Additionally, the engines will be utilized by the Navy, Air Force, and foreign military sales partners. The initial delivery order under the contract includes 20 engines designated for the production line of the Army's UH-60M Black Hawk, the latest variant of the helicopter.

Table of Contents

Defense Turbojet Engines Market Report Definition

Defense Turbojet Engines Market Segmentation

By Region

By Application

By End User

Defense Turbojet Engines Market Analysis for next 10 Years

The 10-year defense turbojet engines market analysis would give a detailed overview of defense turbojet engines market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Turbojet Engines Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Turbojet Engines Market Forecast

The 10-year defense turbojet engines market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Turbojet Engines Market Trends & Forecast

The regional defense turbojet engines market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

REST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Market Forecast & Scenario Analysis

Europe

Middle East

APAC

South America

Country Analysis of Defense Turbojet Engines Market

This chapter deals with the key programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Program Mapping

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Turbojet Engines Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Turbojet Engines Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Application, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By End User, 2025-2035

List of Figures

- Figure 1: Global Defense Turbojet Engine Market Forecast, 2025-2035

- Figure 2: Global Defense Turbojet Engine Market Forecast, By Region, 2025-2035

- Figure 3: Global Defense Turbojet Engine Market Forecast, By Application, 2025-2035

- Figure 4: Global Defense Turbojet Engine Market Forecast, By End User, 2025-2035

- Figure 5: North America, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 9: South America, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 10: United States, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 16: France, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 17: France, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 32: India, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 33: India, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 34: China, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 35: China, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Turbojet Engine Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Turbojet Engine Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Turbojet Engine Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Turbojet Engine Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Turbojet Engine Market, By Application (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Turbojet Engine Market, By Application (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Turbojet Engine Market, By End User (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Turbojet Engine Market, By End User (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Turbojet Engine Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Turbojet Engine Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Turbojet Engine Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Turbojet Engine Market, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Turbojet Engine Market, By Application, 2025-2035

- Figure 59: Scenario 1, Defense Turbojet Engine Market, By End User, 2025-2035

- Figure 60: Scenario 2, Defense Turbojet Engine Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Turbojet Engine Market, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Turbojet Engine Market, By Application, 2025-2035

- Figure 63: Scenario 2, Defense Turbojet Engine Market, By End User, 2025-2035

- Figure 64: Company Benchmark, Defense Turbojet Engine Market, 2025-2035

2025-2030 年全球航空发动机市场预测(按发动机类型、飞机类型、技术和分销管道划分)

2025-2030 年全球航空发动机市场预测(按发动机类型、飞机类型、技术和分销管道划分) 全球加力燃烧室市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

全球加力燃烧室市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年) 2025年全球民航机燃气涡轮机发动机市场报告2025年全球航空燃气涡轮机市场报告2025年全球飞机涡轮扇发动机市场报告

2025年全球民航机燃气涡轮机发动机市场报告2025年全球航空燃气涡轮机市场报告2025年全球飞机涡轮扇发动机市场报告 飞机用涡扇发动机的全球市场评估,各级推力,飞机类别,各技术,各地区,机会,预测,2018年~2032年

飞机用涡扇发动机的全球市场评估,各级推力,飞机类别,各技术,各地区,机会,预测,2018年~2032年 2025-2029年全球民航机燃气涡轮机发动机市场飞机用引擎的全球市场:各引擎类型,各平台,各地区,机会,预测,2018年~2032年2025年全球航空发动机市场报告

2025-2029年全球民航机燃气涡轮机发动机市场飞机用引擎的全球市场:各引擎类型,各平台,各地区,机会,预测,2018年~2032年2025年全球航空发动机市场报告 全球航空发动机市场:产业分析、规模、份额、成长、趋势和预测(2025-2032 年)

全球航空发动机市场:产业分析、规模、份额、成长、趋势和预测(2025-2032 年)