|

市场调查报告书

商品编码

1735754

无人海上战斗的全球市场(2025年~2035年)Global Unmanned Naval Combat Market 2025-2035 |

||||||

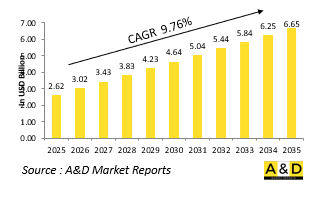

2025年全球无人海战市场规模估计为26.2亿美元,预计到2035年将达到66.5亿美元,复合年增长率为9.76%。

科技对无人海战市场的影响

科技创新正在推动无人海战系统能力与效能的空前提升。现代技术进步使这些平台能够自主操作、在复杂的海洋环境中航行、避开障碍物并在无人直接控制的情况下进行作战行动。感测器技术的突破性进展增强了威胁侦测、目标定位和环境感知能力,使无人舰艇能够即时收集和传递关键数据。通讯系统不断发展,能够透过安全的高频宽链路支援远洋通信,从而促进与指挥部和盟军的远端协调和资料共享。人工智慧和机器学习演算法现已融入这些系统中,从而实现自适应行为、预测性决策和作战优化。此外,微型电子设备和高效能推进系统正在扩大作战范围和续航能力,同时减少维修需求。电子战套件和模组化有效载荷舱的整合使这些平台能够在侦察、进攻和防御角色之间无缝转换。重要的是,这些系统旨在与载人舰艇、飞机和水下平台协同工作,从而创造一个紧密联繫、互联互通的作战环境。科技的影响不仅重塑了海军的作战方式,也重新定义了在不断发展的海战领域中关于兵力投射、威胁交战和海上态势优势的战略思维。

无人海上作战市场的关键推动因素

海上安全课题日益复杂,促使全球国防领域纷纷采用无人海上作战系统。其中一个主要推动因素是需要在广阔且往往有争议的海域保持持续的监视和威慑,且不将人员暴露于高风险环境中。这些系统具有灵活性,可在和平时期巡逻和现役作战场景中运行,从而能够高度适应不断变化的作战环境。降低与传统海军舰队相关的营运成本的愿望也是无人系统吸引力的一部分,因为无人系统通常需要更少的资源来部署和维护。地缘政治紧张局势以及围绕关键海上航线、领海和海底资源的竞争凸显了先进海上能力的重要性,并正在加速对无人平台的投资。向分散式海上作战的转变进一步凸显了对能够快速应对不对称威胁的网路化、敏捷和可扩展系统的需求。此外,不断发展的政策凸显了将无人系统融入海军联合作战和合成作战的重要性,以增强互通性和战略覆盖范围。这些平台能够单独或与有人平台协同执行侦察、攻击和扫雷任务,在多功能性、生存力和快速反应能力需求的驱动下,已成为未来海上战略的关键。

无人海上作战市场的区域趋势

全球国防领域日益认识到无人海上作战系统的战略潜力,而区域趋势则反映了基于安全关切和海洋地理环境的不同优先事项。在亚太地区,沿海衝突和对海域感知的需求正在推动对自主水面和水下平台的投资。拥有漫长海岸线和活跃海上航线的国家正在优先发展监视和反潜能力,以确保海上控制。北美,尤其是美国,正在寻求建立一支综合无人机舰队,以补充现有海军力量,重点是远程作战、情报收集和精确打击。欧洲国家正在推行联合开发项目,重点关注模组化设计和互通性,以支持国内和联盟主导的行动。该方法还包括整合水面和水下系统,以应对从海盗到领土入侵等一系列威胁。

本报告提供全球无人海上战斗市场相关调查分析,提供今后10年成长促进因素,预测,各地区趋势等资讯。

目录

无人海上战斗市场报告定义

无人海上战斗市场区隔

按诱导

各类型

各地区

今后10年的无人海上战斗市场分析

无人海上战斗市场技术

全球无人海上战斗市场预测

地区的无人海上战斗市场趋势与预测

北美

促进因素,阻碍因素,课题

PEST

市场预测与情势分析

主要企业

供应商层级格局

企业基准

欧洲

中东

亚太地区

南美

无人海上战斗市场分析:各国

美国

防卫计划

最新消息

专利

这个市场上目前技术成熟度

市场预测与情势分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

无人海上战斗市场机会矩阵

无人海上战斗市场报告相关专家的意见

结论

关于Aviation and Defense Market Reports

The Global Unmanned Naval Combat market is estimated at USD 2.62 billion in 2025, projected to grow to USD 6.65 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 9.76% over the forecast period 2025-2035.

Introduction to Unmanned Naval Combat Market:

Unmanned naval combat systems are transforming maritime warfare by introducing autonomy, precision, and persistent presence into naval operations without endangering human crews. These systems, which include surface and underwater vehicles, offer a range of strategic advantages-conducting surveillance, mine countermeasures, electronic warfare, and even offensive strikes. As naval domains become increasingly contested, defense forces are turning to unmanned platforms to extend operational reach, monitor vast maritime regions, and respond to threats more swiftly. Unlike traditional vessels, unmanned systems can operate for prolonged durations, often in environments too dangerous or remote for manned crews. They can also be deployed in swarms or coordinated units, offering layered and adaptive maritime defense. Global interest in these capabilities is expanding, with militaries seeking to modernize their fleets and adopt technologies that support multidomain operations. The development of these systems reflects a strategic shift in naval doctrine-prioritizing versatility, survivability, and real-time intelligence. As threats at sea become more complex, nations are investing in unmanned naval combat solutions to enhance deterrence, protect trade routes, and ensure maritime dominance. These platforms are no longer peripheral; they are becoming essential components of future naval warfare, seamlessly integrating with traditional assets and contributing to a more agile and resilient maritime force.

Technology Impact in Unmanned Naval Combat Market:

Technological innovation is driving unprecedented progress in the capabilities and effectiveness of unmanned naval combat systems. Modern advancements have enabled these platforms to operate autonomously, navigating complex maritime environments, avoiding obstacles, and executing missions without direct human control. Breakthroughs in sensor technologies have enhanced threat detection, target identification, and environmental awareness, allowing unmanned vessels to gather and relay critical data in real time. Communication systems have evolved to support secure, high-bandwidth links across vast ocean distances, facilitating remote coordination and data sharing with command centers and allied units. Artificial intelligence and machine learning algorithms are now embedded into these systems, enabling adaptive behaviors, predictive decision-making, and mission optimization. In addition, miniaturized electronics and efficient propulsion systems are extending operational range and endurance while reducing maintenance requirements. The integration of electronic warfare suites and modular payload bays allows these platforms to transition seamlessly between surveillance, offensive, and defensive roles. Importantly, these systems are being designed to collaborate with manned vessels, aircraft, and underwater platforms, creating a connected and cohesive combat environment. The technological impact is not only reshaping how naval forces conduct operations but also redefining strategic thinking about force deployment, threat engagement, and maritime situational dominance in the evolving theater of naval warfare.

Key Drivers in Unmanned Naval Combat Market:

The increasing complexity of maritime security challenges is fueling the adoption of unmanned naval combat systems across global defense communities. A major driver is the need to maintain persistent surveillance and deterrence across vast and often contested maritime regions without exposing personnel to high-risk environments. These systems offer the flexibility to operate in both peacetime patrols and active combat scenarios, making them highly adaptable to changing mission profiles. The desire to reduce the operational costs associated with traditional naval fleets also contributes to their appeal, as unmanned systems generally require fewer resources to deploy and sustain. Geopolitical tensions and competition over critical sea lanes, territorial waters, and undersea resources have underscored the importance of advanced maritime capabilities, prompting accelerated investment in unmanned platforms. The shift toward distributed maritime operations has further highlighted the need for networked, agile, and scalable systems that can respond swiftly to asymmetric threats. Additionally, evolving doctrines emphasize the importance of integrating unmanned systems into joint and coalition naval operations, enhancing interoperability and strategic reach. The ability to carry out reconnaissance, strike, and mine-clearing missions independently or in tandem with crewed assets has solidified these platforms as a cornerstone of future naval strategy, driven by the demand for versatility, survivability, and rapid response.

Regional Trends in Unmanned Naval Combat Market:

Global defense sectors are increasingly recognizing the strategic potential of unmanned naval combat systems, and regional trends reflect diverse priorities based on security concerns and maritime geography. In the Asia-Pacific region, coastal disputes and the need for maritime domain awareness are prompting significant investment in autonomous surface and underwater platforms. Nations with expansive coastlines and active shipping routes are focusing on surveillance and anti-submarine capabilities to ensure maritime control. In North America, particularly the United States, efforts are directed toward building integrated unmanned fleets that complement existing naval power, emphasizing long-range operations, intelligence gathering, and precision engagement. European countries are pursuing cooperative development programs, focusing on modular designs and interoperability to support both national and alliance-led missions. Their approach often includes combining surface and underwater systems to address a range of threats, from piracy to territorial incursion. In the Middle East, unmanned naval systems are being adopted to secure ports, monitor vital chokepoints, and conduct persistent patrols around key maritime infrastructure. African and Latin American regions are gradually exploring unmanned capabilities for coastal security and counter-smuggling operations, often in partnership with more established defense producers. Across all regions, the common thread is a growing emphasis on autonomy, adaptability, and integration into broader maritime defense architectures.

Key Unmanned Naval Combat Program:

HD Hyundai Heavy Industries (HD HHI), in collaboration with the Republic of Korea (ROK) Navy, is advancing the development of a naval combat unmanned surface vessel (USV), seen as a potential game-changer in future maritime operations. Designed to operate in frontline areas, the combat USV will undertake reconnaissance and close-combat missions, effectively reducing the need for manned vessels. It is expected to play a central role in future manned-unmanned teaming systems at sea. HD HHI plans to hold a kickoff meeting later this month and will spend the next eight months on concept design, aiming to complete this phase by December. The work will define the combat USV's performance requirements, key technologies, and procurement strategies. With this initiative, HD HHI intends to propose mission solutions tailored to future multi-domain warfare, while developing a USV that surpasses current manned platforms in reliability and cost-efficiency. The company has reaffirmed its commitment to leading the advancement of integrated manned-unmanned systems, starting with this project.

Table of Contents

Unmanned Naval Combat Market Report Definition

Unmanned Naval Combat Market Segmentation

By Guidance

By Type

By Region

Unmanned Naval Combat Market Analysis for next 10 Years

The 10-year Unmanned Naval Combat Market analysis would give a detailed overview of mortar ammunition market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Unmanned Naval Combat Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Unmanned Naval Combat Market Forecast

The 10-year Unmanned Naval Combat Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Unmanned Naval Combat Market Trends & Forecast

The regional Unmanned Naval Combat Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Unmanned Naval Combat Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Unmanned Naval Combat Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Power Unit, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Power Unit, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Application, 2025-2035

List of Figures

- Figure 1: Global Unmanned Naval Combat Market Forecast, 2025-2035

- Figure 2: Global Unmanned Naval Combat Market Forecast, By Region, 2025-2035

- Figure 3: Global Unmanned Naval Combat Market Forecast, By Power Unit, 2025-2035

- Figure 4: Global Unmanned Naval Combat Market Forecast, By Application, 2025-2035

- Figure 5: North America, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 6: Europe, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 8: APAC, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 9: South America, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 10: United States, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 11: United States, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 12: Canada, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 14: Italy, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 16: France, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 17: France, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 18: Germany, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 24: Spain, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 30: Australia, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 32: India, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 33: India, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 34: China, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 35: China, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 40: Japan, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Unmanned Naval Combat Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Unmanned Naval Combat Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Unmanned Naval Combat Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Unmanned Naval Combat Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Unmanned Naval Combat Market, By Power Unit (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Unmanned Naval Combat Market, By Power Unit (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Unmanned Naval Combat Market, By Application (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Unmanned Naval Combat Market, By Application (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Unmanned Naval Combat Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Unmanned Naval Combat Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Unmanned Naval Combat Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Unmanned Naval Combat Market, By Region, 2025-2035

- Figure 58: Scenario 1, Unmanned Naval Combat Market, By Power Unit, 2025-2035

- Figure 59: Scenario 1, Unmanned Naval Combat Market, By Application, 2025-2035

- Figure 60: Scenario 2, Unmanned Naval Combat Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Unmanned Naval Combat Market, By Region, 2025-2035

- Figure 62: Scenario 2, Unmanned Naval Combat Market, By Power Unit, 2025-2035

- Figure 63: Scenario 2, Unmanned Naval Combat Market, By Application, 2025-2035

- Figure 64: Company Benchmark, Unmanned Naval Combat Market, 2025-2035