|

市场调查报告书

商品编码

1820817

小型武器和轻武器的全球市场:2025年~2035年Global Small Arms and Light Weapons Market 2025-2035 |

||||||

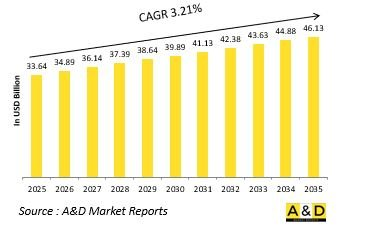

全球轻小型武器市场规模预计在2025年达到336.4亿美元,预计到2035年将增长至461.3亿美元,2025年至2035年的复合年增长率 (CAGR) 为3.21%。

轻小型武器市场简介

防御性轻小型武器市场涵盖各种步兵武器,这些武器在各种作战场景中都具有机动性、易用性和战术灵活性。这些武器包括步枪、手枪、机关枪、榴弹发射器和其他小型武器,构成了地面部队作战能力的支柱。小型武器和轻武器在军事行动中仍然至关重要,使部队能够以精确和敏捷的方式参与近距离作战、防御行动和非对称战争。儘管重型武器系统取得了进步,但它们在常规和非常规衝突中的有效性确保了它们仍然具有重要意义。这些武器在维和任务、边境安全、反恐和城市战环境中也至关重要,在这些环境中,机动性和快速反应至关重要。随着战争日益分散化和不对称化,对可靠、轻巧和多功能小型武器的需求持续增长。现代军事战略强调模组化、人体工学设计和更高的杀伤力,正在推动该领域的技术创新。除了战场作用外,小型武器还对威慑能力、部队战备和特种作战效能做出了重大贡献,使其成为全球军队的宝贵资产。

科技对轻小武器市场的影响

技术进步正在重塑轻小型武器市场格局,显着提升其性能、适应性和作战效用。现代设计扩大采用轻质合金和复合材料等先进材料,提高了武器的耐用性,同时减少了士兵的疲劳。精密工程和模组化系统实现了快速客製化和任务特定配置,使部队能够根据不同的作战环境调整武器。改进的光学系统、夜视系统和热成像技术提高了目标捕获和交战精度,即使在能见度较差的条件下也能实现。数位火控系统和智慧武器技术正在将轻小型武器转变为网路化资产,并将其与战场通讯和指挥系统整合。抑制器技术和改进的后座力管理系统正在提高作战期间的隐身性和可控性。此外,弹药设计的创新,包括更高的杀伤力、更轻的重量和环保材料的使用,进一步提高了效能和永续性。此外,积层製造和先进的生产技术加快了开发週期,并实现了经济高效的升级。总的来说,这些技术创新提升了轻小型武器的战术价值,使军队能够在日益复杂和快速发展的作战环境中以更高的精度、灵活性和态势优势作战。

轻小型武器市场的关键驱动因素

推动防御性轻小武器市场成长的主要因素是不断发展的安全挑战和不断变化的作战条件。叛乱、恐怖主义和城市衝突等非对称威胁的兴起,推动了对紧凑、可靠和多功能武器的需求。现代军事理论越来越强调快速机动、灵活部署和近距离作战,而所有这些都严重依赖先进的轻小型武器。特种作战部队的扩张及其对高性能、特定任务武器的需求也是一个关键驱动因素。地缘政治紧张局势、跨境衝突和领土争端促使国防部队升级步兵武器,以维持战术优势。旨在提高杀伤力、生存力和作战效能的现代化项目和以士兵为中心的方法正在进一步加速武器采购。此外,製造技术和模组化武器系统的进步鼓励定期升级和更换。国际合作与防务伙伴关係也支持该领域的技术转移和能力提升。各国努力在常规和非常规战场保持战备状态,对轻小型武器的投资仍然是一项战略重点,以确保其在更广泛的国防现代化战略中持续发展并发挥关键作用。

轻小型武器市场的区域趋势

轻小型武器市场的区域动态反映了不同的安全优先事项和作战需求。北美凭藉大规模的现代化项目、先进的步兵计划以及对技术先进的武器系统的关注,保持领先地位。欧洲国家优先考虑现代化和标准化工作,以提高盟军之间的互通性,同时应对恐怖主义和混合战争等不断演变的威胁。在亚太地区,领土衝突升级、军事扩张迅速以及地面部队投入不断增加,极大地推动了对先进小型武器的需求。中东国家持续致力于加强反恐能力和国内安全部队,从而增加了特种武器的采购。拉丁美洲和非洲国家虽然服务于较小的市场,但其对小型武器的投资主要用于边境安全、国内防御和反叛乱行动。在政府主导的旨在减少对外国供应商依赖和加强国内国防工业的举措的支持下,该地区的国内製造能力正在不断提升。此外,合资企业、国防伙伴关係和技术转移协议正在促进下一代武器系统的全球应用。这些地区趋势凸显了小型武器在国家安全战略中的持久重要性,以及其在当代国防理论中不断演变的作用。

重大小型武器与轻武器计画

据国防部消息人士透露,根据与俄罗斯达成的国防协议,印度陆军将在2025年接收7万支AK-203突击步枪,并在2026年接收另外10万支。

此次交付是印度与莫斯科达成的一项更广泛协议的一部分,旨在为印度士兵提供世界上最先进、最可靠的突击步枪。美国陆军已于2024年接收了35,000支轻型武器。

目录

小型武器和轻武器市场报告定义

小型武器和轻武器市场区隔

各地区

各类型

各终端用户

未来10年轻型武器市场分析

本章透过对轻型武器市场10年的分析,详细概述了轻型武器市场的成长、变化趋势、技术采用概况和市场吸引力。

轻小型武器市场技术

本部分探讨了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的潜在影响。

全球轻小型武器市场预测

本部分对轻小型武器市场未来10年的预测涵盖了上述细分市场。

轻小型武器市场趋势及各区域预测

本部分涵盖区域轻小型武器市场趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术层面。此外,本部分也提供详细的区域市场预测和情境分析。区域分析包括对主要公司的分析、供应商格局和公司基准分析。目前市场规模是基于常规情境估算。

北美

驱动因素、限制因素与挑战

PEST

市场预测与Scenario分析

主要企业

供应商阶层的形势

企业基准

欧洲

中东

亚太地区

南美

小型武器与轻武器市场国家分析

本章涵盖该市场的主要国防项目以及该市场的最新新闻和专利申请。本章也提供未来10年的市场预测和国家层级的情境分析。

美国

防卫计划

最新消息

专利

这个市场上目前技术成熟度

市场预测与Scenario分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

小型武器与轻武器市场机会矩阵

机会矩阵帮助读者了解该市场中机会较高的市场区隔。

小型武器与轻武器市场报告专家意见

我们提供关于该市场分析潜力的专家意见。

结论

关于航空·国防市场报告

The Global Small Arms and Light Weapons market is estimated at USD 33.64 billion in 2025, projected to grow to USD 46.13 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 3.21% over the forecast period 2025-2035.

Introduction to Small Arms and Light Weapons Market:

The defense small arms and light weapons market encompasses a broad range of infantry weapons designed for mobility, ease of use, and tactical versatility across diverse combat scenarios. These include rifles, pistols, machine guns, grenade launchers, and other portable weapons that serve as the backbone of ground forces' combat capabilities. Small arms and light weapons remain essential for military operations, enabling forces to engage in close-quarters combat, defensive operations, and asymmetric warfare with precision and agility. Their effectiveness in both conventional conflicts and irregular engagements has ensured their continued relevance despite advancements in heavier weapon systems. These weapons are also crucial in peacekeeping missions, border security, counterterrorism, and urban warfare environments, where mobility and rapid response are paramount. As warfare becomes increasingly decentralized and asymmetric, the demand for reliable, lightweight, and multi-functional small arms continues to rise. Modern military strategies emphasize modularity, ergonomic design, and improved lethality, driving innovation in this domain. Beyond their battlefield roles, small arms also contribute significantly to deterrence capabilities, force readiness, and special operations effectiveness, making them indispensable assets for armed forces worldwide and ensuring sustained investment and modernization within this critical segment of the defense industry.

Technology Impact in Small Arms and Light Weapons Market:

Technological advancements are reshaping the landscape of the small arms and light weapons market, significantly enhancing their performance, adaptability, and operational utility. Modern designs increasingly incorporate advanced materials such as lightweight alloys and composites, improving weapon durability while reducing soldier fatigue. Precision engineering and modular systems allow for rapid customization and mission-specific configurations, enabling forces to adapt weapons to varied operational environments. Enhanced optics, night vision, and thermal imaging sights are improving target acquisition and engagement accuracy, even under low-visibility or adverse conditions. Digital fire-control systems and smart weapon technologies are beginning to transform small arms into networked assets, integrating them with battlefield communication and command systems. Suppressor technologies and improved recoil management systems are enhancing stealth and control during operations. Additionally, innovations in ammunition design - including enhanced lethality, reduced weight, and environmentally friendly materials - are further increasing effectiveness and sustainability. Additive manufacturing and advanced production techniques are also accelerating development cycles and enabling cost-efficient upgrades. These technological innovations collectively elevate the tactical value of small arms, allowing military forces to operate with greater precision, flexibility, and situational advantage in increasingly complex and fast-evolving combat environments.

Key Drivers in Small Arms and Light Weapons Market:

Several key factors are fueling the growth of the defense small arms and light weapons market, driven primarily by evolving security challenges and shifting warfare dynamics. The rise of asymmetric threats, including insurgencies, terrorism, and urban conflicts, has heightened the need for compact, reliable, and versatile weaponry. Modern military doctrines increasingly emphasize rapid mobility, flexible deployment, and close-quarters engagement, all of which rely heavily on advanced small arms. The expansion of special operations forces and their demand for high-performance, mission-specific weapons is another significant driver. Geopolitical tensions, cross-border disputes, and territorial conflicts are prompting defense forces to upgrade their infantry arsenals to maintain tactical superiority. Modernization programs and soldier-centric initiatives aimed at improving lethality, survivability, and operational effectiveness are further accelerating procurement. Moreover, advancements in manufacturing technologies and modular weapon systems are encouraging periodic upgrades and replacements. International collaborations and defense partnerships also support technology transfer and capability enhancement in this domain. As nations seek to maintain readiness across both conventional and unconventional battlefields, investment in small arms and light weapons remains a strategic priority, ensuring their continued evolution and critical role within broader defense modernization strategies.

Regional Trends in Small Arms and Light Weapons Market:

Regional dynamics in the small arms and light weapons market reflect diverse security priorities and operational requirements. North America maintains a leading position, driven by extensive modernization programs, advanced infantry equipment initiatives, and a focus on technologically sophisticated weapon systems. European countries are prioritizing modernization and standardization efforts to enhance interoperability among allied forces, while also responding to evolving threats such as terrorism and hybrid warfare. In the Asia-Pacific region, rising territorial disputes, rapid military expansion, and growing investments in ground forces are significantly boosting demand for advanced small arms. Middle Eastern nations continue to focus on strengthening counterterrorism capabilities and enhancing internal security forces, leading to increased procurement of specialized weapons. Latin American and African countries, while smaller markets, are investing in small arms primarily for border security, internal defense, and counterinsurgency operations. Indigenous manufacturing capabilities are expanding across regions, supported by government-led initiatives to reduce reliance on foreign suppliers and strengthen domestic defense industries. Additionally, joint ventures, defense partnerships, and technology transfer agreements are facilitating the introduction of next-generation weapon systems globally. These regional trends highlight the enduring importance of small arms in national security strategies and their evolving role in modern defense doctrines.

Key Small Arms and Light Weapons Program:

The Indian Army is scheduled to receive 70,000 AK-203 assault rifles in 2025, followed by an additional 100,000 units in 2026, under a defense agreement with Russia, according to defense sources.

This shipment, forming part of a broader deal with Moscow, is intended to provide Indian soldiers with one of the most advanced and dependable assault rifles globally. The Army has already taken delivery of 35,000 of these rifles in 2024.

Table of Contents

Small Arms and Light Weapons Market Report Definition

Small Arms and Light Weapons Market Segmentation

By Region

By Type

By End - User

Small Arms and Light Weapons Market Analysis for next 10 Years

The 10-year Small Arms and Light Weapons Market analysis would give a detailed overview of Small Arms and Light Weapons Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Small Arms and Light Weapons Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Small Arms and Light Weapons Market Forecast

The 10-year Small Arms and Light Weapons Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Small Arms and Light Weapons Market Trends & Forecast

The regional Small Arms and Light Weapons Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Small Arms and Light Weapons Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Small Arms and Light Weapons Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Small Arms and Light Weapons Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By End User, 2025-2035

List of Figures

- Figure 1: Global Small arms and light weapons Market Forecast, 2025-2035

- Figure 2: Global Small arms and light weapons Market Forecast, By Region, 2025-2035

- Figure 3: Global Small arms and light weapons Market Forecast, By Type, 2025-2035

- Figure 4: Global Small arms and light weapons Market Forecast, By End User, 2025-2035

- Figure 5: North America, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 6: Europe, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 8: APAC, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 9: South America, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 10: United States, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 11: United States, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 12: Canada, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 14: Italy, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 16: France, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 17: France, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 18: Germany, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 24: Spain, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 30: Australia, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 32: India, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 33: India, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 34: China, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 35: China, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 40: Japan, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Small arms and light weapons Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Small arms and light weapons Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Small arms and light weapons Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Small arms and light weapons Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Small arms and light weapons Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Small arms and light weapons Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Small arms and light weapons Market, By End User (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Small arms and light weapons Market, By End User (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Small arms and light weapons Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Small arms and light weapons Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Small arms and light weapons Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Small arms and light weapons Market, By Region, 2025-2035

- Figure 58: Scenario 1, Small arms and light weapons Market, By Type, 2025-2035

- Figure 59: Scenario 1, Small arms and light weapons Market, By End User, 2025-2035

- Figure 60: Scenario 2, Small arms and light weapons Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Small arms and light weapons Market, By Region, 2025-2035

- Figure 62: Scenario 2, Small arms and light weapons Market, By Type, 2025-2035

- Figure 63: Scenario 2, Small arms and light weapons Market, By End User, 2025-2035

- Figure 64: Company Benchmark, Small arms and light weapons Market, 2025-2035