|

市场调查报告书

商品编码

1838154

主战坦克的全球市场:2025-2035年Global Main Battle Tank Market 2025-2035 |

||||||

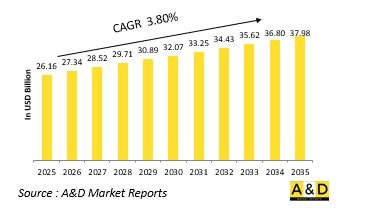

预计全球主战坦克市场规模将从2025年的261.6亿美元成长到2035年的379.8亿美元,预测期内复合年增长率为3.80%。

主战坦克市场概况:

国防领域的主战坦克 (MBT) 市场是现代地面作战的核心。它集火力、防护和机动性于一体,在从常规战争到非对称战争等各种作战中都能发挥优势。主战坦克是装甲部队的核心,在各种地形和战场上提供决定性的作战能力。现代军事理论强调多域联合作战、生存力和精确打击能力,主战坦克的演变由此而生。现今的坦克不再是孤立的作战车辆,而是能够与侦察部队、无人机和指挥中心共享即时数据的网路化作战系统。随着威胁的多样化,主战坦克的角色正在超越直接作战。它们还能发挥心理威慑作用,在攻击和维和行动中发挥重要作用。先进装甲材料、数位化火控系统和主动防护系统(APS)的引入显着提高了坦克的战备能力。此外,领土衝突和大规模地面战争的再次爆发再次凸显了装甲部队的战略重要性。作为全球现代化计画的一部分,主战坦克正在进行重新设计,以提高机动性、模组化和生存力,确保其在快速发展的国防技术和不断变化的作战环境中持续发挥作用。

技术创新对主战战车市场的影响:

技术创新正在重新定义主战坦克的能力,将其转变为高度网路化、灵活且具韧性的作战平台。复合装甲和反应装甲等装甲技术的进步,增强了坦克对抗动能和化学能弹药的生存能力。主动防护系统 (APS) 的引入,透过拦截和化解反坦克飞弹 (ATGM) 等威胁,显着提高了乘员的安全性。同时,引擎设计和混合动力推进技术的进步,提高了坦克的机动性、燃油效率和作战范围,在不牺牲动力的情况下提升了作战效率。数位化也是变革的关键驱动力。综合战场管理系统使主战坦克能够共享态势感知资料、与无人机协同作战,并在网路中心作战环境中作战。此外,先进的火控系统和光学系统支援精确瞄准,即使在不利条件下也能确保高精度。自动化和人工智慧辅助功能正在简化操作并减轻乘员负担。无人驾驶坦克和可选载人坦克的出现代表了战术灵活性的新方向。积层製造技术正在加速零件供应,模组化设计则提升了可维护性和可升级性。这些创新正在推动主战坦克发展成为技术先进的武器系统,使其能够在未来作战环境中保持优势。

主战战车市场的关键驱动因素:

主战坦克的需求受到不断变化的安全挑战、现代化需求以及技术进步的共同驱动。日益加剧的地缘政治紧张局势和高强度战争的再次出现促使世界各国军队升级其装甲部队,以增强威慑力和战备能力。主战坦克是这项努力的核心,它在陆战中提供压倒性的火力、防护和攻击能力。老旧坦克的现代化也是支撑市场成长的关键因素。许多国家正在使用数位系统、先进感测器和改进的装甲升级老旧坦克,以使其适应现代战争的需求。确保与无人系统和指挥网络的互通性也影响采购政策。此外,轻型、高机动性的主战坦克(MBT)的研发正在进行中,以应对城市战争和混合战争。随着越来越多的国家寻求加强装甲车辆製造的自给自足,国防工业合作和国内生产政策也支持市场扩张。此外,推动系统、生存力和武器装备的持续创新,也持续激发全球对主战坦克发展的兴趣。所有这些因素都使主战坦克继续成为威慑和战斗力的重要资产。

本报告研究了全球主战坦克市场,并提供了全面的市场背景分析、市场影响因素、市场规模趋势和预测,以及按细分市场和地区进行的详细分析。

目录

主战坦克市场 - 目录

主战坦克市场报告定义

主战坦克市场区隔

各地区

各类型

今后10年的主战坦克市场分析

主战坦克市场成长,变化的趋势,技术招聘概要,市场魅力

主战坦克市场上技术

影响市场的和预计的前十名技术及这些技术对市场全体带来的可能性影响

全球主战坦克市场预测

各地区主战坦克市场趋势与预测

北美

促进因素,规定,课题

PEST

市场预测与Scenario分析

主要企业

供应商阶层的形势

企业基准

欧洲

中东

亚太地区

南美

主战坦克市场各国分析

美国

防卫计划

最新消息

专利

目前技术成熟度

市场预测·Scenario分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

主战坦克市场机会矩阵

主战坦克市场报告相关专家的意见

结论

关于航空·国防市场报告

The Global Main Battle Tank market is estimated at USD 26.16 billion in 2025, projected to grow to USD 37.98 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 3.80% over the forecast period 2025-2035.

Introduction to Main Battle Tank Market:

The defense main battle tank market remains a cornerstone of modern land warfare, combining firepower, protection, and mobility to dominate in both conventional and asymmetric conflicts. Main battle tanks (MBTs) serve as the backbone of armored forces, providing decisive combat capability across varied terrains and operational theaters. The evolution of MBTs has been shaped by shifting military doctrines that emphasize multi-domain integration, survivability, and precision engagement. Modern tanks are no longer isolated battlefield platforms but networked systems capable of sharing data with reconnaissance units, drones, and command centers in real time. As threats evolve, the role of MBTs continues to expand beyond direct engagement. They serve as psychological deterrents, projecting strength and ensuring dominance during both offensive maneuvers and peacekeeping operations. The integration of advanced armor materials, digital fire-control systems, and active protection measures has elevated the combat readiness of these vehicles. Furthermore, the resurgence of territorial disputes and large-scale land conflicts has reaffirmed the strategic importance of armored formations. With modernization programs underway in multiple nations, MBTs are being redesigned for greater agility, modularity, and survivability, ensuring their continued relevance in an era of rapidly advancing defense technologies and changing combat dynamics.

Technology Impact in Main Battle Tank Market:

Technological innovation is redefining the capabilities of main battle tanks, transforming them into highly networked, adaptive, and resilient combat platforms. Advancements in armor technology, such as composite and reactive armor systems, are enhancing survivability against kinetic and chemical energy projectiles. Active protection systems now enable tanks to detect and neutralize incoming threats like anti-tank guided missiles before impact, significantly improving crew safety. At the same time, advancements in engine design and hybrid propulsion are improving mobility, fuel efficiency, and operational range without compromising power. Digitalization is another major transformation driver. Integrated battlefield management systems allow MBTs to share situational awareness data, synchronize with drones, and operate as part of network-centric warfare environments. Modern fire-control systems and advanced optics enhance targeting precision, even under adverse conditions, while automation and AI-assisted functions are simplifying operations and reducing crew workload. The emergence of unmanned or optionally manned tank concepts further illustrates the direction of technological progress, offering new tactical flexibility. Moreover, the use of additive manufacturing for spare parts and modular designs simplifies maintenance and upgrades. These innovations collectively ensure that main battle tanks continue to evolve as technologically sophisticated platforms capable of maintaining dominance in future combat scenarios.

Key Drivers in Main Battle Tank Market:

The demand for main battle tanks in the defense market is driven by a combination of evolving security challenges, modernization imperatives, and technological advancements. Increasing geopolitical tensions and the reemergence of high-intensity warfare have compelled militaries to strengthen their armored forces for deterrence and rapid response. MBTs are central to this strategy, offering unmatched firepower, protection, and shock effect in land-based combat operations. Modernization of aging fleets is a critical factor driving market growth. Many nations are upgrading legacy platforms with digital systems, advanced sensors, and improved armor configurations to meet modern warfare requirements. The push for interoperability with other battlefield assets, including unmanned systems and command networks, is also influencing procurement decisions. Additionally, the focus on urban warfare and hybrid conflict environments has led to the development of lighter, more agile MBTs capable of operating effectively in complex terrains. Defense industrial collaboration and indigenous production initiatives are also supporting demand, as countries seek self-reliance in armored vehicle manufacturing. Continuous innovation in propulsion, survivability, and weapon systems further sustains interest in MBT programs worldwide. Collectively, these factors underscore the enduring relevance of main battle tanks as essential assets in both deterrence and combat effectiveness.

Regional Trends in Main Battle Tank Market:

Regional trends in the main battle tank market are shaped by distinct strategic priorities, industrial capabilities, and threat perceptions. In technologically advanced defense regions, modernization programs focus on next-generation MBTs equipped with active protection systems, digital connectivity, and hybrid propulsion. These areas emphasize innovation, seeking to develop highly survivable and networked platforms capable of performing within multi-domain operations. The goal is to maintain armored superiority through integration of AI-based decision support, automation, and advanced situational awareness systems. In contrast, regions facing persistent territorial disputes and internal conflicts prioritize rapid acquisition and modernization of cost-effective tanks to ensure deterrence and operational readiness. These nations often pursue upgrade packages for existing fleets, balancing capability enhancement with budget constraints. Meanwhile, defense-industrial cooperation and joint development programs are fostering cross-border collaborations, enabling emerging economies to access advanced technologies while building domestic manufacturing expertise. Environmental and logistical considerations are also influencing regional strategies, with a growing emphasis on fuel efficiency and sustainability in armored vehicle design. Furthermore, the increasing focus on export-oriented production has expanded global competition, with countries positioning themselves as suppliers of advanced MBT solutions to allied and developing nations. These regional dynamics collectively shape the evolving landscape of the global main battle tank market.

Key Main Battle Tank Program:

The Indian Ministry of Defence has signed a $248-million contract with Rosoboronexport to supply advanced engines for the Indian Army's T-72 Ural main battle tanks. As part of the agreement, the Russian state-owned defense exporter will deliver 1,000-horsepower engines to replace the older 780-horsepower units currently installed on India's Soviet-era T-72 fleet. The army presently operates around 2,500 of these tanks, which have been in service since their production in the 1970s. The contract also includes a technology transfer arrangement that will enable India's state-run Armoured Vehicles Nigam Ltd. to locally manufacture the new engines under license, supporting domestic production and maintenance capabilities.

Table of Contents

Main Battle Tank Market - Table of Contents

Main Battle Tank Market Report Definition

Main Battle Tank Market Segmentation

By Region

By Type

Main Battle Tank Market Analysis for next 10 Years

The 10-year Main Battle Tank Market analysis would give a detailed overview of Main Battle Tank Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Main Battle Tank Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Main Battle Tank Market Forecast

The 10-year Main Battle Tank Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Main Battle Tank Market Trends & Forecast

The regional Main Battle Tank Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Main Battle Tank Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Main Battle Tank Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Main Battle Tank Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Type, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By Process, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Type, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By Process, 2025-2035

List of Figures

- Figure 1: Global Main Battle Tank Market Forecast, 2025-2035

- Figure 2: Global Main Battle Tank Market Forecast, By Region, 2025-2035

- Figure 3: Global Main Battle Tank Market Forecast, By Type, 2025-2035

- Figure 4: Global Main Battle Tank Market Forecast, By Process, 2025-2035

- Figure 5: North America, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 6: Europe, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 8: APAC, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 9: South America, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 10: United States, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 11: United States, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 12: Canada, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 14: Italy, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 16: France, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 17: France, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 18: Germany, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 24: Spain, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 30: Australia, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 32: India, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 33: India, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 34: China, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 35: China, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 40: Japan, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Main Battle Tank Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Main Battle Tank Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Main Battle Tank Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Main Battle Tank Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Main Battle Tank Market, By Type (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Main Battle Tank Market, By Type (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Main Battle Tank Market, By Process (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Main Battle Tank Market, By Process (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Main Battle Tank Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Main Battle Tank Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Main Battle Tank Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Main Battle Tank Market, By Region, 2025-2035

- Figure 58: Scenario 1, Main Battle Tank Market, By Type, 2025-2035

- Figure 59: Scenario 1, Main Battle Tank Market, By Process, 2025-2035

- Figure 60: Scenario 2, Main Battle Tank Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Main Battle Tank Market, By Region, 2025-2035

- Figure 62: Scenario 2, Main Battle Tank Market, By Type, 2025-2035

- Figure 63: Scenario 2, Main Battle Tank Market, By Process, 2025-2035

- Figure 64: Company Benchmark, Main Battle Tank Market, 2025-2035