|

市场调查报告书

商品编码

1930541

全球反潜战 (ASW) 市场 (2026-2036)Global Anti Submarine Warfare Market 2026-2036 |

||||||

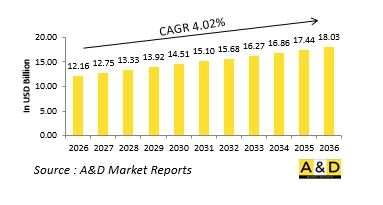

据估计,全球反潜战 (ASW) 市场在 2026 年的价值为 121.6 亿美元,预计到 2036 年将达到 180.3 亿美元,2026 年至 2036 年的复合年增长率 (CAGR) 为 4.02%。

引言

反潜战 (ASW) 是海军作战中一个高度专业化且具有战略意义的关键领域,其重点在于探测、追踪和摧毁那些本身俱有隐蔽性和挑战性的水下威胁。潜水艇在威慑、情报收集和海上拒止方面发挥着至关重要的作用,因此是海军部队的首要关注点。反潜作战(ASW)并非单一能力,而是涵盖平台、感测器、人员和战术的综合系统,需要在广阔的海洋空间内协同作战。水面舰艇、潜水艇、海上巡逻机、直升机、无人系统和固定式水下感测器网路共同合作。现代潜舰的静音性能不断提升,续航力也随之增强,这增加了水下作战的复杂性,并使反潜作战成为海军的核心能力。除了衝突局势之外,这些能力还有助于海上监视、水下基础设施保护和战略稳定。随着海军竞争的加剧和水下领域的日益拥挤,反潜作战作为海上安全和海军优势的关键支柱,将继续发展壮大。

科技对反潜作战 (ASW) 的影响

技术进步从根本上重塑了反潜作战,其探测范围更广、资料融合能力更强、反应速度更快。先进的声吶系统,包括主动声吶、被动声吶和低频声吶,能够在各种声学环境中进行有效探测。改进的讯号处理技术使操作人员能够更准确地从背景噪音中识别潜艇。感测器融合技术整合了声学、磁学和环境数据,从而提供水下态势的全面视图。自主水下航行器 (AUV) 将监视范围扩展到有人平台难以到达的区域。机载系统部署了先进的感测器,能够快速覆盖广阔的海洋区域。安全的资料链路实现了海军作战单位之间的即时水下资讯共享。模拟和建模工具支援在高度复杂的水下环境中进行作战规划和操作人员训练。这些技术进步正在将反潜作战 (ASW) 从被动侦察行动转变为主动和预测性的海上防御能力。

反潜作战 (ASW) 的关键驱动因素

对先进反潜作战 (ASW) 能力的需求源自于潜舰的战略价值及其所带来的挑战。潜艇的扩散和技术的日益复杂化增加了对有效反制措施的需求。保护海军作战部队、商业航道和水下通讯基础设施进一步凸显了水下监视的重要性。海军现代化计划将水下优势作为更广泛海上主导权的先决条件。联合行动需要在空中、水面和水下领域具备整合的反潜能力。无人和自主系统的扩展也推动了对探测、规避和追踪技术的投资。训练和战备要求强调持续监视和快速反应。此外,从战略威慑的角度来看,反潜作战 (ASW) 对于维护海上力量平衡至关重要。这些驱动因素要求持续关注并加强水下防御能力。

反潜战 (ASW) 的区域趋势

各区域的反潜战 (ASW) 策略反映了各自独特的海洋地理环境和威胁认知。北美军队强调深海监视和盟军海军网路的整合。欧洲军队则专注于狭窄水域监视和合作行动,以保护水下基础设施。亚太地区各国由于海上交通繁忙和沿海环境复杂,将反潜能力列为优先事项。中东国家则致力于保障狭窄水道和近海资产的安全。非洲海上力量优先发展监视和能力建设,以监控不断扩大的海洋区域。在整个区域内,对感测器网路、培训和海上安全合作框架的投资都在增加。这些区域趋势凸显了地理环境、联盟关係以及不断演变的水下挑战如何塑造反潜战 (ASW) 战略。 本报告分析了全球反潜战 (ASW) 市场,深入探讨了影响该市场的技术、未来十年的预测以及区域趋势。

目录

反潜战 (ASW) 市场报告定义

反潜战 (ASW) 市场区隔

按地区

按应用

按平台

未来十年反潜战 (ASW) 市场分析

反潜战 (ASW) 市场技术

全球反潜战 (ASW) 市场预测

区域反潜战 (ASW) 市场趋势及预测

北美

驱动因素、限制因素及挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级状况

公司标竿分析

欧洲

中东

亚太地区

南美洲

反潜战(ASW)市场分析中的国家

美国

国防项目

最新资讯

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

反潜战(ASW)市场机会矩阵

专家对反潜战(ASW)市场的看法报告

结论

关于航空与国防市场报告

The Global Anti Submarine Warfare market is estimated at USD 12.16 billion in 2026, projected to grow to USD 18.03 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.02% over the forecast period 2026-2036.

Introduction

Anti submarine warfare represents a highly specialized and strategically vital discipline within naval operations, focused on detecting, tracking, and neutralizing underwater threats that are inherently stealthy and difficult to counter. Submarines play a decisive role in deterrence, intelligence gathering, and sea denial, making them a priority concern for maritime forces. Anti submarine warfare is not a single capability but a coordinated system of platforms, sensors, personnel, and tactics operating across vast ocean spaces. It involves surface vessels, submarines, maritime patrol aircraft, helicopters, unmanned systems, and fixed underwater sensor networks working in coordination. The growing quietness and endurance of modern submarines have increased the complexity of underwater operations, elevating anti submarine warfare as a core naval competency. Beyond conflict scenarios, these capabilities also support maritime surveillance, protection of undersea infrastructure, and strategic stability. As naval competition intensifies and underwater domains become more congested, anti submarine warfare continues to evolve as a critical pillar of maritime security and naval superiority.

Technology Impact in Anti Submarine Warfare

Technological progress has fundamentally reshaped anti submarine warfare by expanding detection ranges, improving data fusion, and accelerating response timelines. Advanced sonar systems, including active, passive, and low-frequency variants, enable more effective detection across varied acoustic environments. Improvements in signal processing allow operators to distinguish submarines from background noise with greater confidence. Sensor fusion technologies integrate acoustic, magnetic, and environmental data to create a comprehensive underwater picture. Autonomous underwater vehicles extend surveillance coverage into areas difficult for crewed platforms to access. Airborne systems deploy advanced sensors that rapidly cover large maritime zones. Secure data links enable real-time sharing of underwater intelligence across naval task groups. Simulation and modeling tools support mission planning and operator training in highly complex underwater conditions. These technological advancements transform anti submarine warfare from reactive search operations into proactive and predictive maritime defense capabilities.

Key Drivers in Anti Submarine Warfare

The demand for advanced anti submarine warfare capabilities is driven by the strategic value of submarines and the challenges they pose. Submarine proliferation and technological sophistication increase the need for effective countermeasures. Protection of naval task forces, commercial shipping routes, and undersea communication infrastructure reinforces the importance of underwater surveillance. Naval modernization programs prioritize undersea dominance as a prerequisite for broader maritime control. Joint operations require integrated anti submarine capabilities across air, surface, and subsurface domains. The expansion of unmanned and autonomous systems also drives investment in counter-detection and tracking technologies. Training and readiness requirements emphasize continuous monitoring and rapid response. Additionally, strategic deterrence considerations make anti submarine warfare essential for maintaining balance in maritime power. These drivers ensure sustained focus on enhancing underwater defense capabilities.

Regional Trends in Anti Submarine Warfare

Regional approaches to anti submarine warfare reflect distinct maritime geographies and threat perceptions. North American forces emphasize deep-ocean surveillance and integration across allied naval networks. European navies focus on monitoring constrained seas and protecting undersea infrastructure through cooperative operations. Asia-Pacific countries prioritize anti submarine capabilities due to dense maritime traffic and complex littoral environments. Middle Eastern forces concentrate on securing narrow waterways and offshore assets. African maritime forces emphasize surveillance and capacity-building to monitor expanding maritime zones. Across regions, there is increasing investment in sensor networks, training, and cooperative maritime security frameworks. These regional trends highlight how anti submarine warfare strategies are shaped by geography, alliances, and evolving underwater challenges.

Key Anti Submarine Warfare Program:

The Royal Navy awarded a £40 million contract in 2025 to replenish sonobuoy inventories for maritime patrol aircraft conducting anti-submarine operations in the North Atlantic. Ultra Maritime secured a CAD $200 million contract to equip Netherlands and Belgian surface combatants with integrated ASW sensor suites combining hull-mounted sonar, towed arrays, and acoustic processing systems. These investments address growing undersea threats from advanced diesel-electric and nuclear-powered submarines operated by peer competitors.

Table of Contents

Anti Submarine Warfare Market - Table of Contents

Anti Submarine Warfare Market Report Definition

Anti Submarine Warfare Market Segmentation

By Region

By Application

By Platform

Anti Submarine Warfare Market Analysis for next 10 Years

The 10-year anti submarine warfare market analysis would give a detailed overview of Anti Submarine Warfare Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Anti Submarine Warfare Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Anti Submarine Warfare Market Forecast

The 10-year Anti Submarine Warfare Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Anti Submarine Warfare Market Trends & Forecast

The regional Anti Submarine Warfare Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Anti Submarine Warfare Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Anti Submarine Warfare Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Anti Submarine Warfare Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Application, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Application, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Platform, 2026-2036

List of Figures

- Figure 1: Global Anti Submarine Warfare Market Forecast, 2026-2036

- Figure 2: Global Anti Submarine Warfare Market Forecast, By Region, 2026-2036

- Figure 3: Global Anti Submarine Warfare Market Forecast, By Application, 2026-2036

- Figure 4: Global Anti Submarine Warfare Market Forecast, By Platform, 2026-2036

- Figure 5: North America, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 6: Europe, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 7: Middle East, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 8: APAC, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 9: South America, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 10: United States, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 11: United States, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 12: Canada, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 14: Italy, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 16: France, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 17: France, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 18: Germany, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 24: Spain, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 30: Australia, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 32: India, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 33: India, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 34: China, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 35: China, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 40: Japan, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Anti Submarine Warfare Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Anti Submarine Warfare Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Anti Submarine Warfare Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Anti Submarine Warfare Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Anti Submarine Warfare Market, By Application (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Anti Submarine Warfare Market, By Application (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Anti Submarine Warfare Market, By Platform (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Anti Submarine Warfare Market, By Platform (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Anti Submarine Warfare Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Anti Submarine Warfare Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Anti Submarine Warfare Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Anti Submarine Warfare Market, By Region, 2026-2036

- Figure 58: Scenario 1, Anti Submarine Warfare Market, By Application, 2026-2036

- Figure 59: Scenario 1, Anti Submarine Warfare Market, By Platform, 2026-2036

- Figure 60: Scenario 2, Anti Submarine Warfare Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Anti Submarine Warfare Market, By Region, 2026-2036

- Figure 62: Scenario 2, Anti Submarine Warfare Market, By Application, 2026-2036

- Figure 63: Scenario 2, Anti Submarine Warfare Market, By Platform, 2026-2036

- Figure 64: Company Benchmark, Anti Submarine Warfare Market, 2026-2036