|

市场调查报告书

商品编码

1936041

全球系留气球系统市场(2026-2036)Global Aerostat Systems Market 2026-2036 |

||||||

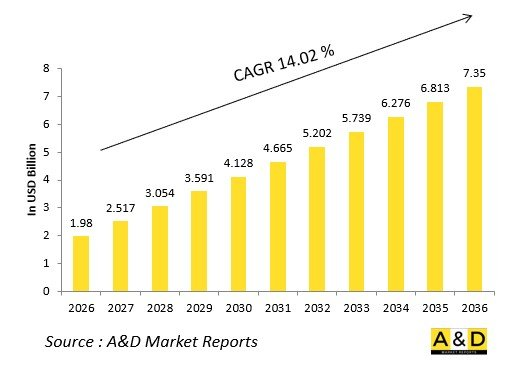

据估计,2026年全球繫留气球系统市场规模为19.8亿美元,预计到2036年将达到73.5亿美元,2026年至2036年的复合年增长率(CAGR)为14.02%。

引言

全球系留气球系统市场提供了一种经济高效的长期监视平台,能够实现地面系统无法达到的广泛感测器覆盖范围。系留式飞艇透过使雷达、光电摄影机和通讯节点保持在空中进行持续监测,从而为军事情报、监视与侦察 (ISR)、边境安全和关键基础设施保护做出贡献。

市场扩张的驱动力在于对繫留式飞艇的需求不断增长,这种飞艇弥合了无人机和卫星之间的差距。采用太阳能蒙皮的混合氦气包层延长了续航时间,稳定的万向节即使在强风中也能保持感测器锁定。模组化有效载荷可在各种任务之间无缝更换,从禁毒执法到电子战支援。

地缘政治边界和城市威胁正在推动部署,并加强与无人机群和地面网路的整合。 TCOM 和洛克希德马丁等供应商正在创新用于行动作业的系留管理技术。供应链优先考虑用于恶劣环境的耐用材料,与固定翼飞机相比,更快的重新配置速度是一项竞争优势。

繫留式飞艇正在重新定义空中持续监视能力。

技术对繫留气球系统的影响

技术进步使繫留气球系统实现了前所未有的续航力和精准度。先进的蒙皮材料(凯夫拉层压板和奈米复合材料)具有抗撕裂性,可最大限度地减少氦气洩漏,并支持数週的定点观测。自主繫泊绞车可在数分钟内从拖车上展开,从而支援灵活的前沿作战。

多光谱有效载荷结合了主动相控阵雷达 (AESA)、中波红外线 (IR) 和高光谱成像仪,用于昼夜威胁识别,探测低空飞行的无人机和船隻。人工智慧演算法处理机载数据,并透过即时下行链路向执行器发送讯号。太阳能光电阵列和燃料电池支援持续作战,并减少地面后勤保障。

网路整合使繫留气球能够融入杀伤网,将资料中继给战斗机和飞弹。稳定平台可抵消强风引起的湍流,并维持万向节精度。预测性维护感测器能够预测包络应力,从而显着减少停机时间。

混合繫绳整合了电源、资料和光纤,可实现高频宽 5G 中继。集群控制协调多个系留气球,使其覆盖范围重迭。这些进步增强了战场态势感知能力,并将繫留气球转变为纵深防御的倍增器。

繫留气球系统的关键驱动因素

日益增长的边境威胁正在推动系留气球的普及应用,与有人巡逻相比,系留气球能够以更经济的方式对广阔的边境地区进行持续监视。情报、监视与侦察 (ISR) 预算的调整也倾向于选择能够填补近太空空白的低成本平台。

军事理论要求全天候 (24/7) 覆盖反无人机系统 (UAS) 和海上态势感知,而繫留气球在持久性方面表现出色。国土安全部门正在扩大其在禁毒和基础设施监控方面的作用。

技术成熟使得有效载荷能够快速更换,并可适应不断发展的传感器而无需重新认证飞机。日益紧张的地缘政治局势正在推动出口,而补偿贸易则支持本地生产。

与整合网路的整合正在推动对通讯浮标的需求。透过氦气回收和太阳能发电实现的可持续性确保了符合环境法规。放宽的民用空域法规正在促进部署。

与卫星和直升机相比,成本优势持续增强。这些驱动因素使得繫留气球成为确保不对称优势的关键。

本报告探讨并分析了全球系留气球系统市场,提供了影响市场的技术资讯、未来十年的预测以及区域趋势。

目录

繫留气球系统市场报告定义

繫留气球系统市场细分

依推进方式

依地区

依类型

未来十年系留气球系统市场分析

繫留气球系统市场技术

全球系留气球系统市场预测

区域系留气球系统市场趋势及预测

北美

驱动因素、限制因素与挑战

PEST分析

市场预测及情境分析

主要公司

供应商层级现况

公司基准分析

欧洲

中东

亚太地区

南美洲

繫留气球系统市场国家分析

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测及情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

繫留气球系统市场机会矩阵

专家对繫留气球系统市场报告的意见

结论

关于航空与国防市场报告

The Global Aerostat Systems Market is estimated at USD 1.98 billion in 2026, projected to grow to USD 7.35 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 14.02% over the forecast period 2026-2036.

Introduction

The global Aerostat Systems market delivers cost-effective, long-endurance surveillance platforms, elevating sensors for wide-area coverage unattainable by ground systems. Tethered aerostats serve military ISR, border patrol, and critical infrastructure protection, carrying radars, electro-optical cameras, and communication nodes aloft for continuous monitoring.

Market expansion stems from heightened security needs, with aerostats filling gaps between drones and satellites. Hybrid helium envelopes with photovoltaic skins extend loiter times, while stabilized gimbals maintain sensor lock amid winds. Modular payloads swap seamlessly for missions from drug interdiction to electronic warfare support.

Geopolitical borders and urban threats drive deployments, integrated with UAV swarms and ground networks. Vendors like TCOM and Lockheed innovate tether management for mobile ops. Supply chains emphasize resilient materials against harsh environments. Competition favors rapid reconfigurability over fixed-wing alternatives.

Aerostats redefine persistent eyes in the sky.

Technology Impact in Aerostat Systems

Technological evolution empowers aerostat systems with unprecedented persistence and precision. Advanced envelope fabrics-kevlar laminates and nanocomposites-resist tears while minimizing helium leakage, enabling weeks-long stations. Autonomous tether winches deploy from trailers in minutes, supporting mobile forward ops.

Multi-spectral payloads fuse AESA radars, mid-wave IR, and hyperspectral imagers for day-night threat ID, detecting low-flying drones or vessels. AI algorithms process feeds onboard, cueing effectors via real-time downlink. Photovoltaic arrays and fuel cells power perpetual ops, reducing ground logistics.

Network integration meshes aerostats into kill webs, relaying data to fighters or missiles. Stabilized platforms counter turbulence up to gale forces, preserving gimbal accuracy. Predictive maintenance sensors forecast envelope stress, slashing downtime.

Hybrid tethers bundle power, data, and fiber optics, enabling high-bandwidth 5G relays. Swarm coordination links multiple aerostats for overlapping coverage. These strides amplify battlespace awareness, transforming aerostats into force multipliers for layered defense.

Key Drivers in Aerostat Systems

Escalating border threats propel aerostat adoption, offering economical persistent surveillance over vast frontiers versus manned patrols. ISR budget shifts favor low-operating-cost platforms filling near-space gaps.

Military doctrines demand 24/7 coverage for counter-UAS and maritime domain awareness, where aerostats excel in endurance. Homeland security expands roles in drug interdiction and infrastructure watch.

Technological maturity enables rapid payload swaps, adapting to evolving sensors without airframe requalification. Geopolitical tensions boost exports, with offsets spurring local production.

Integration with joint networks drives demand for communication buoys. Sustainability via helium recycling and solar power aligns with green mandates. Regulatory easing for commercial airspace eases deployments.

Cost advantages over satellites or helos sustain momentum. These drivers position aerostats as indispensable for asymmetric edges.

Regional Trends in Aerostat Systems

North America dominates with mature ISR programs, deploying tethered radars for continental defense and southern borders.

Europe integrates aerostats into NATO air pictures for eastern flanks and Mediterranean patrols.

Asia-Pacific accelerates amid territorial disputes, with India advancing Akashdeep for Himalayan vigilance and China scaling maritime sentinels.

Middle East leverages for desert frontiers and Gulf shipping lanes.

South America employs against narco-routes.

Africa adopts for peacekeeping perimeters.

Trends emphasize hybrid tethers and AI payloads, with Asia-Pacific emerging fastest via infrastructure spends.

Key Aerostat Systems Programs

US Army's Persistent Surveillance Systems-Tethered (PSS-T) modernizes aerostats for wide-area ISR, with Leidos, QinetiQ, and TCOM competing on sensor-laden tethers filling near-space voids.

India's Akashdeep, Nakshatra, and Chakshu develop indigenous aerostats for border radars.

JLENS trials balloon-borne fire-control radars cueing Patriot intercepts.

TCOM's LP-17 series equips forward bases with EO/IR relays.

Border Star systems patrol US-Mexico frontiers.

European Sky Shield incorporates aerostats for layered air defense.

Poland acquires PSS-T equivalents for eastern borders.

Maritime aerostats enhance littoral surveillance.

These initiatives blend legacy persistence with next-gen smarts.

Table of Contents

Aerostat Systems Market - Table of Contents

Aerostat Systems Market Report Definition

Aerostat Systems Market Segmentation

By Propulsion

By Region

By Type

Aerostat Systems Market Analysis for next 10 Years

The 10-year Aerostat Systems Market analysis would give a detailed overview of Aerostat Systems Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Aerostat Systems Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Aerostat Systems Market Forecast

The 10-year Aerostat Systems Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Aerostat Systems Market Trends & Forecast

The regional Aerostat Systems Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Aerostat Systems Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Aerostat Systems Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Aerostat Systems Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Range, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Application, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Range, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Application, 2026-2036

List of Figures

- Figure 1: Global Aerostat Systems Market Forecast, 2026-2036

- Figure 2: Global Aerostat Systems Market Forecast, By Region, 2026-2036

- Figure 3: Global Aerostat Systems Market Forecast, By Range, 2026-2036

- Figure 4: Global Aerostat Systems Market Forecast, By Application, 2026-2036

- Figure 5: North America, Aerostat Systems Market, Forecast, 2026-2036

- Figure 6: Europe, Aerostat Systems Market, Forecast, 2026-2036

- Figure 7: Middle East, Aerostat Systems Market, Forecast, 2026-2036

- Figure 8: APAC, Aerostat Systems Market, Forecast, 2026-2036

- Figure 9: South America, Aerostat Systems Market, Forecast, 2026-2036

- Figure 10: United States, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 11: United States, Aerostat Systems Market, Forecast, 2026-2036

- Figure 12: Canada, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Aerostat Systems Market, Forecast, 2026-2036

- Figure 14: Italy, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 16: France, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 17: France, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 18: Germany, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 24: Spain, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 30: Australia, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 32: India, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 33: India, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 34: China, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 35: China, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 40: Japan, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Aerostat Systems Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Aerostat Systems Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Aerostat Systems Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Aerostat Systems Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Aerostat Systems Market, By Range (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Aerostat Systems Market, By Range (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Aerostat Systems Market, By Application (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Aerostat Systems Market, By Application (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Aerostat Systems Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Aerostat Systems Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Aerostat Systems Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Aerostat Systems Market, By Region, 2026-2036

- Figure 58: Scenario 1, Aerostat Systems Market, By Range, 2026-2036

- Figure 59: Scenario 1, Aerostat Systems Market, By Application, 2026-2036

- Figure 60: Scenario 2, Aerostat Systems Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Aerostat Systems Market, By Region, 2026-2036

- Figure 62: Scenario 2, Aerostat Systems Market, By Range, 2026-2036

- Figure 63: Scenario 2, Aerostat Systems Market, By Application, 2026-2036

- Figure 64: Company Benchmark, Aerostat Systems Market, 2026-2036

轻型航具系统市场规模、份额和成长分析(按产品类型、推进系统、等级和地区划分):产业预测(2026-2033 年)

轻型航具系统市场规模、份额和成长分析(按产品类型、推进系统、等级和地区划分):产业预测(2026-2033 年) 全球轻型航具系统市场(按平台类型、有效载荷能力、高度范围、应用和最终用户)预测 2025-2032

全球轻型航具系统市场(按平台类型、有效载荷能力、高度范围、应用和最终用户)预测 2025-2032 轻型航具系统市场分析与预测(至 2034 年):类型、产品、服务、技术、组件、应用、材料类型、部署、最终用户

轻型航具系统市场分析与预测(至 2034 年):类型、产品、服务、技术、组件、应用、材料类型、部署、最终用户 轻型航具系统的全球市场:各类型,各用途,各终端用户,各地区,机会,预测,2018年~2032年

轻型航具系统的全球市场:各类型,各用途,各终端用户,各地区,机会,预测,2018年~2032年 2026 年至 2032 年轻型航具系统市场(按应用、产品类型、组件和地区划分)

2026 年至 2032 年轻型航具系统市场(按应用、产品类型、组件和地区划分) 浮空器系统市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

浮空器系统市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 浮空器系统市场 - 全球产业规模、份额、趋势、机会和预测,按产品类型、推进类型、类别类型、地区和竞争细分,2019-2029F

浮空器系统市场 - 全球产业规模、份额、趋势、机会和预测,按产品类型、推进类型、类别类型、地区和竞争细分,2019-2029F 轻型航具系统全球市场2024-2028浮空器系统市场:2024-2034

轻型航具系统全球市场2024-2028浮空器系统市场:2024-2034