|

市场调查报告书

商品编码

1936042

全球AESA雷达市场:2026-2036Global AESA Radar Market 2026-2036 |

||||||

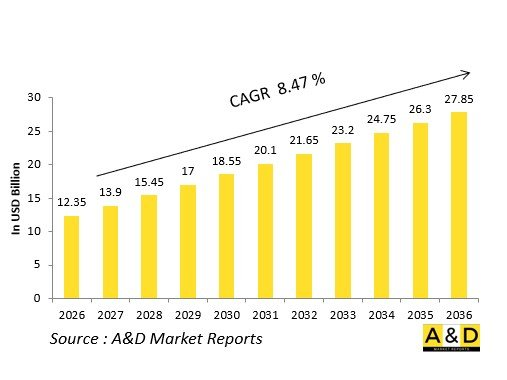

2026年全球AESA雷达市场规模估计为123.5亿美元,预计到2036年将达到278.5亿美元,2026年至2036年的年复合成长率(CAGR)为8.47%。

引言

全球AESA雷达市场是现代空中优势的基础,它利用固态相控阵雷达为战斗机火控、海军监视和陆基飞弹防御提供支援。数千个收发模组(TRM)可实现快速波束稳定、同步空对空追踪和地面测绘,其可靠性和多功能性超越了机械雷达。

市场发展反映了机队现代化进程,现有平台透过 AESA 升级扩展,而新设计则采用氮化镓(GaN)实现紧凑型电源。关键特性包括频率捷变、低旁瓣和电子对抗,支持用于视场作战和合成孔径成像的交错模式。

地缘政治紧张局势推动采购,各国空军都在寻求适用于多用途战斗机和无人机的可扩展架构。互通性标准促进了出口,而开放式系统设计则便于升级。在半导体短缺的情况下,供应链致力于高可靠性半导体。基于 GaN 的模组领域,现有企业正与新兴企业竞争。

该市场体现了感测器融合在网路化战争中的作用。

AESA雷达的技术影响

AESA技术透过电子波束控制革新了雷达性能,无需机械万向节即可实现瞬时方位角和仰角变化。基于GaN的TRM提高了功率和效率,可以缩小阵列尺寸,同时扩展对隐身目标和高超音速飞行器的侦测范围。

多功能性使其能够在噪音环境下同时追踪数十个目标,并同时进行追踪和扫描以进行飞弹导引。自适应波形支援跳频,避免干扰并超越敌方反应时间。低捕获机率模式使用扩频讯号来掩蔽被动侦测器的无线电辐射。

数位波束成形技术可产生用于精确探测的窄波束或用于搜寻的宽扇形波束,最佳化地面模式下的合成孔径解析度。非合作目标识别透过分析微多普勒特征来区分敌我。与电子战系统的整合可利用定向噪音抑制威胁。

感知演算法能够自我最佳化以应对噪音和欺骗,而数位孪生技术则加速了模式的发展。舰载版本足够坚固,能够承受舰船运动,并支援广域搜索和视野扩展。这些进步缩短了杀伤链,并在对抗空域中实现了 "先发制人" 的优势。

AESA雷达的主要驱动因素

战斗机机队的现代化推动AESA雷达的采用,因为老旧飞机需要进行改装以应对隐身威胁和饱和攻击。海军航空兵需要在对抗激烈的深海环境中为多用途航空母舰配备小型机头雷达。

高超音速和低可侦测性武器的扩散需要超越机械扫描极限的敏捷追踪能力。出口市场对能够结合可扩展的追踪参考模型(TRM)数量以适应不同平台并采用偏移生产的解决方案的需求蓬勃发展。

互通性需求推动联合作战通用架构的发展。向氮化镓(GaN)的过渡显着降低了尺寸、重量和功耗,能够实现无人机群和忠诚僚机的协同作战。日益频繁的电子战促使人们选择抗电子对抗(ECCM)的设计。

预算压力促使人们倾向于选择长寿命的固态元件,而不是维护成本高的真空管。城市空战理论优先考虑多模式弹性。供应链本地化有助于解决脆弱性问题。

透过高效能模组实现永续性符合绿色采购原则。这些因素巩固了 AESA 作为 C4ISR 基础的地位。

AESA 雷达依地区划分的发展趋势

北美在成熟的GaN 专案方面处于领先地位,这些专案用于 F-35 系列战机和宙斯盾舰的升级,并强调多域融合。

在欧洲,共同开发用于欧洲战斗机和阵风战斗机的可扩展阵列,以符合北约在东线的标准。

在亚太地区,为应对岛屿和喜马拉雅地区的威胁,本土研发加速推进,例如印度的Uttam计画用于Tejas,中国的歼-20系列战机。

在中东,西方进口产品正与本地组装相结合,以确保空中优势。

俄罗斯研发能够抵抗电子战饱和的砷化镓阵列。

韩国和日本优先发展用于海上拒止的小型舰载主动相控阵雷达。

在拉丁美洲,各国正致力于进口陆基系统用于领土监视。

数位主动相控阵雷达和人工智慧处理技术的发展趋势融合,使亚太地区在大规模生产方面具有优势。

主要AESA雷达专案

战斗机计画是AESA发展的基础 - AN/APG-81为隐身平台提供空对空/空对地互通性和抗干扰能力。

阵风RBE2-AA为出口机队提供小型氮化镓(GaN)功率。

欧洲战斗机Captor-E扩展了目标参考模型(TRM),使其角色更有弹性。

印度自主研发的Uttam阵列为LCA的后继机型提供多模式机动性支援。

海军的AN/SPY-6可扩展,适用于驱逐舰广域搜寻。

陆基AN/TPY-4移动阵列用来引导飞弹防御。

改良型无人机(UAV),例如MQ-9 "掠夺者" ,将扩展远程侦察和监视(ISR)能力。

数位化主动相控阵雷达(AESA)路线图将整合量子处理器以支援认知模式。

将使用共同开发的样机进行高超音速追踪测试。

出口组件将与导弹整合,以实现全面杀伤力。

这些努力将重新定义雷达,使其成为一种动态效应装置。

目录

AESA雷达市场 - 目录

AESA雷达市场报告定义

AESA雷达市场区隔

依地区

依应用

依平台

未来十年AESA雷达市场分析

本章透过对未来十年AESA雷达市场的分析,详细概述了AESA雷达市场的成长、趋势变化、技术应用概况以及整体市场吸引力。

AESA雷达市场技术

本部分讨论了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的潜在影响。

全球AESA雷达市场预测

以上各细分市场详细阐述了未来十年AESA雷达市场的预测。

AESA雷达市场区域趋势及预测

本部分涵盖各区域AESA雷达市场的趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术因素。此外,也提供详细的区域市场预测和情境分析。最终的区域分析包括主要公司概况、供应商格局和公司基准分析。目前市场规模是基通常情况估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级结构

公司标竿分析

欧洲

中东

亚太地区

南美洲

(市场名称)国家分析

本章 涵盖该市场的主要国防项目以及最新的新闻和专利申请。此外,本章 也提供国家层级的十年市场预测和情境分析。

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

AESA雷达市场机会矩阵

机会矩阵帮助读者了解该市场中高机会细分领域。

AESA雷达市场报告专家意见

本报告总结了专家对此市场分析潜力的意见。

结论

关于航空与国防市场报告

The Global AESA Radar Market is estimated at USD 12.35 billion in 2026, projected to grow to USD 27.85 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 8.47% over the forecast period 2026-2036.

Introduction

The global AESA Radar market anchors modern air dominance, powering fighter fire control, naval surveillance, and ground-based missile defense with solid-state phased arrays. Thousands of transmit-receive modules (TRMs) enable rapid beam agility, simultaneous air-to-air tracking, and ground mapping, surpassing mechanical radars in reliability and versatility.

Market evolution reflects fleet modernization, where AESA retrofits extend legacy platforms while new designs incorporate gallium nitride for compact power. Core features include frequency agility, low sidelobes, and electronic counter-countermeasures, supporting interleaved modes for beyond-visual-range engagements and synthetic aperture imaging.

Geopolitical tensions drive procurement, with air forces seeking scalable architectures for multirole fighters and UAVs. Interoperability standards facilitate exports, while open-system designs ease upgrades. Supply chains focus on resilient semiconductors amid chip constraints. Competition pits established primes against emerging players in GaN-based modules.

This market exemplifies sensor fusion's role in networked warfare.

Technology Impact in AESA Radar

AESA technology revolutionizes radar performance through electronic beam steering, eliminating mechanical gimbals for instantaneous azimuth and elevation shifts. GaN-based TRMs boost power output and efficiency, shrinking arrays while extending detection against stealthy targets and hypersonics.

Multi-function capabilities track dozens of contacts simultaneously, cueing missiles via track-while-scan amid clutter. Adaptive waveforms evade jamming, hopping frequencies faster than adversaries react. Low-probability-of-intercept modes use spread-spectrum signals, concealing emissions from passive detectors.

Digital beamforming shapes narrow pencil beams for precision or wide fans for search, optimizing synthetic aperture resolution in ground modes. Non-cooperative target recognition analyzes micro-Doppler signatures for friend-foe decisions. Integration with EW suites suppresses threats via directed noise.

Cognitive algorithms self-optimize against clutter or deception, while digital twins accelerate mode development. Naval variants ruggedize for ship motion, supporting volume search and horizon extension. These strides compress kill chains, enabling first-look-first-kill advantages in contested airspace.

Key Drivers in AESA Radar

Fighter fleet modernization propels AESA adoption, retrofitting legacy airframes to counter stealthy threats and saturation attacks. Naval aviation demands compact nose radars for multirole carriers amid blue-water rivalries.

Proliferating hypersonic and low-observable munitions necessitate agile tracking beyond mechanically scanned limits. Export markets thrive on scalable TRM counts suiting diverse platforms, bundled with offset production.

Interoperability mandates drive common architectures for coalition ops. GaN transitions slash size-weight-power, enabling UAV and loyal wingman swarms. Electronic warfare escalation favors ECCM-hardened designs.

Budget pressures favor long-life solid-state over maintenance-heavy tubes. Urban air combat doctrines prioritize multi-mode flexibility. Supply chain localization counters vulnerabilities.

Sustainability via efficient modules aligns with green procurement. These forces embed AESA as C4ISR cornerstone.

Regional Trends in AESA Radar

North America leads with mature GaN programs for F-35 derivatives and Aegis upgrades, emphasizing multi-domain fusion.

Europe collaborates on scalable arrays for Eurofighter and Rafale, harmonizing via NATO standards for eastern flanks.

Asia-Pacific accelerates indigenous development-India's Uttam for Tejas, China's J-20 suites-tailored to island and Himalayan threats.

Middle East integrates Western imports with local assembly for air superiority.

Russia advances gallium arsenide arrays resilient to EW saturation.

South Korea and Japan prioritize compact naval AESA for sea denial.

Latin America focuses ground-based imports for territorial vigilance.

Trends converge on digital AESA with AI processing, Asia-Pacific gaining via volume production.

Key AESA Radar Programs

Fighter programs anchor AESA evolution: AN/APG-81 equips stealth platforms with interleaved A2A/A2G modes and jamming resistance.

Rafale RBE2-AA delivers compact GaN power for export fleets.

Eurofighter Captor-E scales TRMs for role flexibility.

India's Uttam indigenous array powers LCA successors with multimode agility.

Naval AN/SPY-6 scales for destroyer volume search.

Ground-based AN/TPY-4 mobile arrays cue missile defenses.

UAV variants like MQ-9 Predator upgrades extend endurance ISR.

Digital AESA roadmaps fuse quantum processors for cognitive modes.

Collaborative prototypes test hypersonic tracking.

Export packages bundle with missiles for holistic lethality.

These initiatives redefine radar as dynamic effectors.

Table of Contents

AESA Radar Market - Table of Contents

AESA Radar Market Report Definition

AESA Radar Market Segmentation

By Region

By Fit

By Platform

AESA Radar Market Analysis for next 10 Years

The 10-year AESA radar market analysis would give a detailed overview of AESA radar market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of AESA Radar Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global AESA Radar Market Forecast

The 10-year AESA radar market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional AESA Radar Market Trends & Forecast

The regional AESA radar market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of (Market name)

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for AESA Radar Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on AESA Radar Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Fit , 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Fit , 2026-2036

List of Figures

- Figure 1: Global AESA Radar Market Forecast, 2026-2036

- Figure 2: Global AESA Radar Market Forecast, By Region, 2026-2036

- Figure 3: Global AESA Radar Market Forecast, By Platform, 2026-2036

- Figure 4: Global AESA Radar Market Forecast, By Fit , 2026-2036

- Figure 5: North America, AESA Radar Market, Forecast, 2026-2036

- Figure 6: Europe, AESA Radar Market, Forecast, 2026-2036

- Figure 7: Middle East, AESA Radar Market, Forecast, 2026-2036

- Figure 8: APAC, AESA Radar Market, Forecast, 2026-2036

- Figure 9: South America, AESA Radar Market, Forecast, 2026-2036

- Figure 10: United States, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 11: United States, AESA Radar Market, Forecast, 2026-2036

- Figure 12: Canada, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 13: Canada, AESA Radar Market, Forecast, 2026-2036

- Figure 14: Italy, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 15: Italy, AESA Radar Market, Market Forecast, 2026-2036

- Figure 16: France, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 17: France, AESA Radar Market, Market Forecast, 2026-2036

- Figure 18: Germany, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 19: Germany, AESA Radar Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, AESA Radar Market, Market Forecast, 2026-2036

- Figure 22: Belgium, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, AESA Radar Market, Market Forecast, 2026-2036

- Figure 24: Spain, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 25: Spain, AESA Radar Market, Market Forecast, 2026-2036

- Figure 26: Sweden, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, AESA Radar Market, Market Forecast, 2026-2036

- Figure 28: Brazil, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, AESA Radar Market, Market Forecast, 2026-2036

- Figure 30: Australia, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 31: Australia, AESA Radar Market, Market Forecast, 2026-2036

- Figure 32: India, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 33: India, AESA Radar Market, Market Forecast, 2026-2036

- Figure 34: China, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 35: China, AESA Radar Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, AESA Radar Market, Market Forecast, 2026-2036

- Figure 38: South Korea, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, AESA Radar Market, Market Forecast, 2026-2036

- Figure 40: Japan, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 41: Japan, AESA Radar Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, AESA Radar Market, Market Forecast, 2026-2036

- Figure 44: Singapore, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, AESA Radar Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, AESA Radar Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, AESA Radar Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, AESA Radar Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, AESA Radar Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, AESA Radar Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, AESA Radar Market, By Platform (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, AESA Radar Market, By Fit (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, AESA Radar Market, By Fit (CAGR), 2026-2036

- Figure 54: Scenario Analysis, AESA Radar Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, AESA Radar Market, Global Market, 2026-2036

- Figure 56: Scenario 1, AESA Radar Market, Total Market, 2026-2036

- Figure 57: Scenario 1, AESA Radar Market, By Region, 2026-2036

- Figure 58: Scenario 1, AESA Radar Market, By Platform, 2026-2036

- Figure 59: Scenario 1, AESA Radar Market, By Fit , 2026-2036

- Figure 60: Scenario 2, AESA Radar Market, Total Market, 2026-2036

- Figure 61: Scenario 2, AESA Radar Market, By Region, 2026-2036

- Figure 62: Scenario 2, AESA Radar Market, By Platform, 2026-2036

- Figure 63: Scenario 2, AESA Radar Market, By Fit , 2026-2036

- Figure 64: Company Benchmark, AESA Radar Market, 2026-2036

固态雷达市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材质、部署类型、最终用户及功能划分

固态雷达市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材质、部署类型、最终用户及功能划分 2026年全球军用相位阵列天线市场报告2026年全球犬类GPS电子产品市场报告

2026年全球军用相位阵列天线市场报告2026年全球犬类GPS电子产品市场报告 60 GHz 雷达市场:按技术、产品类型、部署模式、组件、销售管道、最终用户和应用划分 - 全球预测,2026-2032 年双极化主动相控相位阵列雷达市场:按技术、频段、工作模式、组件、类型、平台、最终用户和应用划分-全球预测,2026-2032年数位主动相控阵雷达市场依架构类型、频段、距离分类、平台类型及最终用户划分,全球预测(2026-2032年)

60 GHz 雷达市场:按技术、产品类型、部署模式、组件、销售管道、最终用户和应用划分 - 全球预测,2026-2032 年双极化主动相控相位阵列雷达市场:按技术、频段、工作模式、组件、类型、平台、最终用户和应用划分-全球预测,2026-2032年数位主动相控阵雷达市场依架构类型、频段、距离分类、平台类型及最终用户划分,全球预测(2026-2032年) 雷达侦测器市场规模、份额和成长分析(按产品类型、技术、应用和地区划分)-2026-2033年产业预测

雷达侦测器市场规模、份额和成长分析(按产品类型、技术、应用和地区划分)-2026-2033年产业预测 雷达安防市场-全球产业规模、份额、趋势、机会及预测(按监控类型、范围、应用、地区和竞争格局划分,2020-2030 年预测)

雷达安防市场-全球产业规模、份额、趋势、机会及预测(按监控类型、范围、应用、地区和竞争格局划分,2020-2030 年预测) 安全雷达感测器:全球市场份额和排名、总收入和需求预测(2025-2031年)60GHz毫米波雷达-全球市占率及排名、总营收及需求预测(2025-2031年)

安全雷达感测器:全球市场份额和排名、总收入和需求预测(2025-2031年)60GHz毫米波雷达-全球市占率及排名、总营收及需求预测(2025-2031年)