|

市场调查报告书

商品编码

1936043

全球机载对抗系统市场:2026-2036Global Airborne Countermeasures System Market 2026-2036 |

||||||

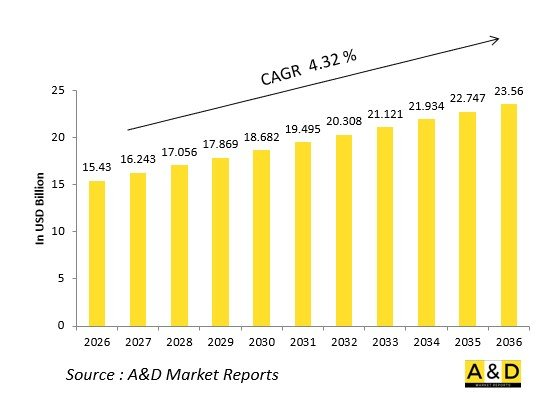

全球机载对抗系统市场预计将从2026年的154.3亿美元成长到2036年的235.6亿美元,2026年至2036年的复合年增长率(CAGR)为4.32%。

引言

全球机载对抗系统市场旨在保护固定翼和旋翼飞机免受不断演变的飞弹威胁,将雷达警告接收机、飞弹逼近告警系统和对抗措施投放器整合到无缝的自卫系统中。这些系统能够探测并识别红外线、雷达和雷射导引武器,并使用箔条、干扰弹和电子干扰将其抵消。

市场成长反映了防空密度的不断提高,因为系统正从被动式投放器发展到人工智慧驱动的定向效应器。核心组件包括吊舱式干扰器、拖曳式诱饵和可编程投放器,这些设备可相容于从隐形战斗机到VIP专机的各种平台。强调减少附带损害的城市作战正在推动调製红外线对抗措施的发展。

日益紧张的地缘政治局势正在加速系统升级,并优先考虑联盟任务中的互通性。开放式架构能够快速更新威胁库,而定向能武器的扩散正在推动供应链转型为高可靠性电子设备。竞争日趋激烈,BAE系统公司和萨博公司等主要厂商正引领光纤拖曳阵列的研发。

该市场表明,飞机的生存能力是任务成功的关键。

科技对机载对抗系统的影响

技术融合将机载对抗系统转变为主动防御系统。多波长飞弹逼近警报系统(紫外线、红外线和雷射)可侦测来自各个方向的飞弹发射,并透过基于全球交战资料训练的人工智慧威胁分类器,在微秒级时间内引导效应器。

定向红外线对抗(DIRCM)雷射利用调製光束使导引系统失效,无需消耗品即可干扰先进的成像导引飞弹。光纤拖曳诱饵可模拟飞机特征,同时能承受超音速发射,进而扩大干扰范围。智慧投放器可根据光谱分析优化箔条和曳光弹的投放。

网路化架构支援整个编队共享威胁数据,从而实现编队级防御。配备氮化镓放大器的紧凑型干扰器能够承受集中干扰。量子级联雷射瞄准高光谱导引头。数位射频记忆体(DRFM)产生与真实发射器无法区分的虚假目标。

与AESA雷达整合可提供融合态势感知。这些技术在飞行中部署带有微型干扰器的诱饵,可降低目标被解锁的机率,扩大无逃逸区,并突破综合防空系统。

机载对抗系统的关键驱动因素

便携式防空飞弹系统(MANPADS)的扩散增加了对高价值飞机的威胁,因此需要多层防护。先进的成像飞弹可对抗传统的干扰弹,推动空军采用DIRCM(远距离红外线导引飞弹对抗)。

舰队维护计画优先考虑提高在衝突地区作战的老旧运输机和加油机的生存能力。出口市场需要能够应付各种威胁库的交钥匙系统。

盟军互通性标准正在加速通用架构的采用。城市地区的近距离空中支援理论要求使用能够最大限度减少附带损害的精确导引设备。定向能武器的扩散使得雷射警告接收器的普及势在必行。

本报告对全球机载对抗系统市场进行了深入分析,全面阐述了关键趋势、市场影响因素、关键技术及其影响、主要地区和国家的趋势以及市场机会。

目录

机载对抗系统市场:目录

机载对抗系统市场:报告定义

机载对抗系统市场:细分

依应用

依地区

依类型

未来十年机载对抗系统市场分析

机载对抗系统市场成长、趋势变化及技术详情:应用概况及市场吸引力

机载对抗系统市场:技术

预计将影响市场的十大技术及其对整体市场的潜在影响

全球机载对抗系统市场: 预测

机载对抗系统市场趋势及预测:依地区划分

本报告涵盖市场趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术因素。报告还提供详细的区域市场预测和情境分析。区域分析最后包括主要公司概况、供应商状况和公司基准分析。目前市场规模是基于一切照旧情境估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级概览

公司标竿分析

欧洲

中东

亚太地区

南美洲

机载对抗系统市场:国家分析

美国

国防项目

最新资讯

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

机载对抗系统市场:机会矩阵

机载对抗系统市场:专家意见

结论

关于航空与国防市场报告

The Global Airborne Countermeasures System Market is estimated at USD 15.43 billion in 2026, projected to grow to USD 23.56 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.32% over the forecast period 2026-2036.

Introduction

The global Airborne Countermeasures System market safeguards fixed-wing and rotary aircraft against evolving missile threats, integrating radar warning receivers, missile approach warners, and countermeasure dispensers into seamless self-protection suites. These systems detect, identify, and neutralize infrared, radar, and laser-guided munitions via chaff, flares, and electronic jamming.

Market growth mirrors rising air defense densities, with suites evolving from reactive dispensers to AI-driven directional effectors. Core components include podded jammers, towed decoys, and programmable dispensers compatible across platforms from stealth fighters to VIP transports. Emphasis on low-collateral urban ops drives modulated infrared countermeasures.

Geopolitical flashpoints accelerate retrofits, prioritizing interoperability for coalition missions. Open architectures enable rapid threat library updates. Supply chains focus on resilient electronics amid directed-energy proliferation. Competition features primes like BAE and Saab pioneering fiber-optic towed arrays.

This market underscores aircraft survivability as mission enabler.

Technology Impact in Airborne Countermeasures System

Technological fusion transforms Airborne Countermeasures Systems into proactive shields. Multi-spectral missile approach warners-UV, IR, and laser-based-detect launches from all quadrants, cueing effectors in microseconds via AI threat classifiers trained on global engagement data.

Directional Infrared Countermeasures (DIRCM) lasers dazzle seeker heads with modulated beams, defeating advanced imaging missiles without expendables. Fiber-optic towed decoys extend jamming envelopes, mimicking aircraft signatures while surviving supersonic ejections. Smart dispensers sequence chaff and flares optimally, minimizing signatures via spectral analysis.

Networked architectures share threat data across formations, enabling formation-wide defenses. GaN amplifiers power compact jammers resisting barrage jamming. Quantum cascade lasers target hyperspectral seekers. Digital radio frequency memory (DRFM) creates false targets indistinguishable from real emitters.

Integration with AESA radars provides fused situational awareness. Expendable decoys deploy micro-jammers mid-flight. These innovations slash break-lock probabilities, extend no-escape zones, and enable deep-strike penetrations against integrated air defenses.

Key Drivers in Airborne Countermeasures System

Proliferating man-portable air defense systems expose high-value aircraft to top-attack profiles, mandating layered countermeasures. Advanced imaging missiles counter legacy flares, driving DIRCM adoption across air forces.

Fleet sustainment programs prioritize survivability upgrades for legacy transports and tankers operating in contested zones. Export markets demand turnkey suites compatible with diverse threat libraries.

Coalition interoperability standards accelerate common architectures. Urban close air support doctrines require precision effectors minimizing collateral. Directed-energy weapon proliferation necessitates laser warning receivers.

Budget imperatives favor podded solutions over airframe redesigns. Training revolutions leverage virtual threat injectors. Supply chain resilience counters sanctions via diversified electronics.

Sustainability via reusable lasers reduces expendable logistics. These dynamics position countermeasures as airpower prerequisites.

Regional Trends in Airborne Countermeasures System

North America pioneers DIRCM suites for strategic airlift and fifth-generation fighters, emphasizing towed decoys.

Europe standardizes via NATO frameworks, equipping multirole fleets with fiber-optic jammers for eastern corridors.

Asia-Pacific surges with indigenous development-India's digital RWR, China's modular pods-for maritime patrols.

Middle East fortifies VIP transports against shoulder-fired threats.

Russia advances plasma-based decoys resilient to multimode seekers.

South Korea integrates with K9 howitzers' air cover.

Latin America protects counter-narcotics helos.

Trends favor AI-driven autonomy, Asia-Pacific gaining manufacturing share.

Key Airborne Countermeasures System Programs

AN/ALE-47 dispensers equip coalition fighters with adaptive sequencing against IR/RF threats.

Saab's CMDS integrates with Gripen for sequenced expendables.

BAE's DIRCM suites dazzle advanced seekers on C-130J.

AN/ALQ-214 podded jammers defend legacy platforms.

Next-gen fiber decoys tow behind F-35s.

European MBDA Talios fuses RWR with laser warning.

India's digital integrated RF suite upgrades Su-30MKI.

VIP aircraft receive commercial DIRCM variants.

Export packages bundle with missile warners.

Table of Contents

Airborne Countermeasures System Market - Table of Contents

Airborne Countermeasures System Market Report Definition

Airborne Countermeasures System Market Segmentation

By Application

By Region

By Type

Airborne Countermeasures System Market Analysis for next 10 Years

The 10-year Airborne Countermeasures System Market analysis would give a detailed overview of Airborne Countermeasures System Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Airborne Countermeasures System Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Airborne Countermeasures System Market Forecast

The 10-year Airborne Countermeasures System Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Airborne Countermeasures System Market Trends & Forecast

The regional Airborne Countermeasures System Market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Airborne Countermeasures System Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Airborne Countermeasures System Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Airborne Countermeasures System Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Application , 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Type , 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Application , 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Type , 2026-2036

List of Figures

- Figure 1: Global Airborne Countermeasures System Market Forecast, 2026-2036

- Figure 2: Global Airborne Countermeasures System Market Forecast, By Region, 2026-2036

- Figure 3: Global Airborne Countermeasures System Market Forecast, By Application , 2026-2036

- Figure 4: Global Airborne Countermeasures System Market Forecast, By Type , 2026-2036

- Figure 5: North America, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 6: Europe, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 7: Middle East, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 8: APAC, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 9: South America, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 10: United States, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 11: United States, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 12: Canada, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Airborne Countermeasures System Market, Forecast, 2026-2036

- Figure 14: Italy, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 16: France, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 17: France, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 18: Germany, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 24: Spain, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 30: Australia, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 32: India, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 33: India, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 34: China, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 35: China, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 40: Japan, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Airborne Countermeasures System Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Airborne Countermeasures System Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Airborne Countermeasures System Market, By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Airborne Countermeasures System Market, By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Airborne Countermeasures System Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Airborne Countermeasures System Market, By Application (CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Airborne Countermeasures System Market, By Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Airborne Countermeasures System Market, By Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Airborne Countermeasures System Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Airborne Countermeasures System Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Airborne Countermeasures System Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Airborne Countermeasures System Market, By Region, 2026-2036

- Figure 58: Scenario 1, Airborne Countermeasures System Market, By Application , 2026-2036

- Figure 59: Scenario 1, Airborne Countermeasures System Market, By Type , 2026-2036

- Figure 60: Scenario 2, Airborne Countermeasures System Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Airborne Countermeasures System Market, By Region, 2026-2036

- Figure 62: Scenario 2, Airborne Countermeasures System Market, By Application , 2026-2036

- Figure 63: Scenario 2, Airborne Countermeasures System Market, By Type , 2026-2036

- Figure 64: Company Benchmark, Airborne Countermeasures System Market, 2026-2036