|

市场调查报告书

商品编码

1936049

全球国防全权限数位引擎控制 (FADEC) 市场:2026-2036 年Global Defense Full Authority Digital Engine Control (FADEC) Market 2026-2036 |

||||||

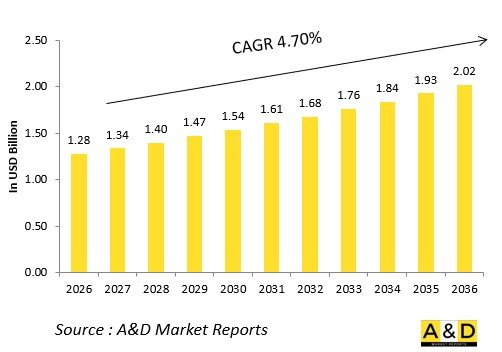

全球国防全权限数位引擎控制 (FADEC) 市场预计将从 2026 年的 12.8 亿美元成长到 2036 年的 20.2 亿美元,2026 年至 2036 年的复合年增长率 (CAGR) 为 4.70%。

引言

全球国防 FADEC 市场透过电子发动机控制器管理军用涡轮扇发动机和涡轴发动机的性能,这些控制器处理油门输入以及压力、温度和马赫数数据。双通道架构无需机械备援即可执行燃油计量、固定翼、引气阀和加力燃烧室顺序控制,从而将完全控制权交给软体。

市场发展与第六代战机的需求相符,全权限数位引擎控制系统 (FADEC) 正在与飞行控制系统整合,以优化极端瞬态条件下的推力。核心功能包括突波保护、过热保护和自动重燃,同时最大限度地提高整个飞行包线的效率。健康监测功能会将诊断讯息传送到地面站。

地缘政治空中优势竞争正在推动发展,优先考虑用于网路化战争的抗网路攻击控制器。模组化软体能够快速更新以应对威胁。供应链正专注于抗辐射处理器。在竞争格局中,BAE系统公司、霍尼韦尔公司和赛峰集团是基于模型控制技术的先驱。

国防全权限数位引擎控制系统 (FADEC) 的技术影响

基于人工智慧的模型预测控制可在性能下降之前预测压缩机失速,并在快速机动过程中主动调整叶片。双通道投票持续比较感测器套件,透过硬体隔离和多样化的软体路径,在微秒内隔离故障。

网路安全隔离分区将关键推力指令和预测诊断资料链路分开。开放式系统架构支援第三方应用程式进行特定任务调度(超音速巡航与待机)。整合式飞行器管理系统将 FADEC 输出与飞行律融合,以实现绝对稳定性。

抗量子加密保护参数表免受国家级威胁。数位孪生技术支援对引擎变化的控制律进行飞行前验证。容错设计支援灵活的性能下降控制,并可过渡到单通道紧急返回模式。

高温碳化硅处理器确保即使在发生不可控故障的情况下也能持续运作。区块链记录不可篡改的健康数据,用于任务后审计。自适应燃料调度可自动补偿性能下降的组件。这些创新显着减轻了飞行员的工作负荷,同时安全地扩展了作战范围。

国防全权限数位引擎控制系统 (FADEC) 的关键驱动因素

第六代整合需要将 FADEC 与任务系统整合,以实现自主协作。超音速巡航优化需要超越人类反应能力的即时可变控制。

维护经济性强调预测性维护,以避免例行更换。出口市场需要可设定软体,以相容于各种引擎。日益激烈的网路战推动了实体隔离控制器的采用。

预算压力促使优先采用军用级商用衍生产品。供应链韧性使国内製造能够应对处理器短缺问题。互通性标准实现了盟军之间的资料共享。

无人机需要轻型控制器,且无需驾驶舱介面。这些需求推动了全权限数位引擎控制系统(FADEC)作为推进系统智慧系统的应用。

本报告分析了全球国防全权限数位引擎控制系统(FADEC)市场,并总结了关键趋势、市场影响因素、关键技术及其影响、主要地区和国家的趋势以及市场机会分析。

目录

国防全权限数位引擎控制系统 (FADEC) 市场:目录

国防全权限数位引擎控制系统 (FADEC) 市场:报告定义

国防全权限数位引擎控制系统 (FADEC) 市场:细分

依平台

依地区

依引擎类型

未来十年国防全权限数位引擎控制系统 (FADEC) 市场分析

国防全权限数位引擎控制系统 (FADEC) 市场成长、趋势变化、技术应用概要及市场吸引力详情

国防全权限数位引擎控制系统 (FADEC) 市场:技术

预计将影响市场的十大技术及其对整体市场的潜在影响

全球国防全权限数位引擎控制系统 (FADEC) 市场:预测

未来十年本报告详细涵盖了上述各细分市场中国防全权限数位电子控制系统 (FADEC) 的市场预测。

国防全权限数位电子控制系统 (FADEC) 市场趋势与预测:依地区划分

本报告涵盖市场趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术因素。报告还提供了详细的区域市场预测和情境分析。区域分析最后包括主要公司概况、供应商状况和公司基准分析。目前市场规模是基于一切照旧情境估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级概览

公司标竿分析

欧洲

中东

亚太地区

南美洲

国防全权限数位引擎控制系统(FADEC)市场:国家分析

美国

国防项目

最新资讯

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

国防 FADEC 市场:机会矩阵

国防 FADEC 市场:专家意见报告

结论

关于航空航太与国防市场报告

The Global Defense Full Authority Digital Engine Control (FADEC) Market is estimated at USD 1.28 billion in 2026, projected to grow to USD 2.02 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.70% over the forecast period 2026-2036.

Introduction

The global Defense FADEC market governs military turbofan and turboshaft performance through electronic engine controllers processing throttle inputs alongside pressures, temperatures, and Mach data. Dual-channel architectures command fuel metering, stator vanes, bleed valves, and afterburner sequencing without mechanical backups, placing full authority in software.

Market evolution tracks sixth-generation demands, where FADEC fuses with flight controls for optimized thrust under extreme transients. Core capabilities include surge prevention, overtemperature protection, and automatic relights, all while maximizing efficiency across flight envelopes. Health monitoring streams diagnostics to ground stations.

Geopolitical air superiority races drive development, prioritizing cyber-hardened controllers for networked warfare. Modular software enables rapid threat response updates. Supply chains focus on radiation-tolerant processors. Competition features BAE Systems, Honeywell, and Safran pioneering model-based controls.

Technology Impact in Defense FADEC

AI-driven model predictive control anticipates compressor stalls before degradation, adjusting vanes proactively during aggressive maneuvers. Dual-channel voting compares sensor suites continuously, isolating faults within microseconds via hardware separation and diverse software paths.

Cyber-hardened partitions segregate critical thrust commands from prognostic data links. Open-system architectures enable third-party apps for mission-specific scheduling-supercruise versus loiter. Integrated vehicle management fuses FADEC outputs with flight laws for canardless stability.

Quantum-resistant encryption secures parameter tables against nation-state threats. Digital twins validate control laws pre-flight against engine variants. Fault-tolerant designs degrade gracefully, reverting to single-channel limp-home modes.

High-temperature silicon carbide processors survive uncontained failures. Blockchain logs immutable health data for post-mission audits. Adaptive fuel schedules counter degraded components automatically. These innovations slash pilot workload while expanding operational envelopes safely.

Key Drivers in Defense FADEC

Sixth-generation integration mandates FADEC fusion with mission systems for autonomous teaming. Super cruise optimization requires real-time variable geometry beyond human response times.

Sustainment economics favor prognostics eliminating scheduled removals. Export markets demand configurable software for diverse engines. Cyber warfare escalation drives air-gapped controllers.

Budget pressures prioritize commercial derivatives with military hardening. Supply chain resilience counters processor shortages via domestic fabs. Interoperability standards enable coalition data sharing.

Unmanned loyal wingmen need lightweight controllers without cockpit interfaces. These imperatives embed FADEC as propulsion intelligence.

Regional Trends in Defense FADEC

North America pioneers AI-augmented controls for NGAD adaptive engines.

Europe standardizes via FCAS frameworks, harmonizing dual-channel architectures.

Asia-Pacific accelerates indigenous development-India's Kaveri FADEC, China's WS-15-for high-altitude intercepts.

Middle East pursues hardened controllers for desert over temps.

Russia advances fault-tolerant designs for Su-57 agility.

South Korea integrates with KF-21 export packages.

Trends favor model-based controls; Asia-Pacific gains software talent.

Key Defense FADEC Programs

F135 FADEC governs STOVL lift fan transitions and afterburner sequencing across variants.

NGAD digital engine control fuses with AI wingmen for formation thrust.

EJ200 upgrades enable dry super cruise via predictive scheduling.

India's GTRE FADEC powers Kaveri derivatives with stall protection.

WS-15 controller manages high-temperature materials autonomously.

Rafale M88 FADEC integrates carrier catapult profiles.

Su-57 AL-41F1S FADEC enables 3D thrust vectoring safely.

T-50 FADEC handles super maneuverability envelope protection.

Table of Contents

Defense Full Authority Digital Engine Control (FADEC) Market- Table of Contents

Defense Full Authority Digital Engine Control (FADEC) Market Report Definition

Defense Full Authority Digital Engine Control (FADEC) Market Segmentation

By Platform

By Region

By Engine Type

Defense Full Authority Digital Engine Control (FADEC) Market Analysis for next 10 Years

The 10-year Defense Full Authority Digital Engine Control (FADEC) Market analysis would give a detailed overview of Defense Full Authority Digital Engine Control (FADEC) Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Aircraft Braking Systems Market Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Full Authority Digital Engine Control (FADEC) Market Forecast

The 10-year Defense Full Authority Digital Engine Control (FADEC) Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Full Authority Digital Engine Control (FADEC) Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Aircraft Braking Systems Market Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Aircraft Braking Systems Market Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Full Authority Digital Engine Control (FADEC) Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Engine Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Engine Type, 2026-2036

List of Figures

- Figure 1: Global Full Authority Digital Engine Control (FADEC) Market Forecast, 2026-2036

- Figure 2: Global Full Authority Digital Engine Control (FADEC) Market Forecast, By Region, 2026-2036

- Figure 3: Global Full Authority Digital Engine Control (FADEC) Market Forecast, By Platform, 2026-2036

- Figure 4: Global Full Authority Digital Engine Control (FADEC) Market Forecast, By Engine Type, 2026-2036

- Figure 5: North America, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 6: Europe, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 7: Middle East, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 8: APAC, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 9: South America, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 10: United States, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 11: United States, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 12: Canada, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 13: Canada, Full Authority Digital Engine Control (FADEC) Market , Forecast, 2026-2036

- Figure 14: Italy, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 15: Italy, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 16: France, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 17: France, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 18: Germany, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 19: Germany, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 21: Netherlands, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 23: Belgium, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 24: Spain, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 25: Spain, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 27: Sweden, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 29: Brazil, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 30: Australia, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 31: Australia, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 32: India, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 33: India, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 34: China, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 35: China, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 39: South Korea, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 40: Japan, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 41: Japan, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 43: Malaysia, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 45: Singapore, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Full Authority Digital Engine Control (FADEC) Market , Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Full Authority Digital Engine Control (FADEC) Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Full Authority Digital Engine Control (FADEC) Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Full Authority Digital Engine Control (FADEC) Market , By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Full Authority Digital Engine Control (FADEC) Market , By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Full Authority Digital Engine Control (FADEC) Market , By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Full Authority Digital Engine Control (FADEC) Market , By Engine Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Full Authority Digital Engine Control (FADEC) Market , By Engine Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Full Authority Digital Engine Control (FADEC) Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Full Authority Digital Engine Control (FADEC) Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Full Authority Digital Engine Control (FADEC) Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Full Authority Digital Engine Control (FADEC) Market , By Region, 2026-2036

- Figure 58: Scenario 1, Full Authority Digital Engine Control (FADEC) Market , By Platform, 2026-2036

- Figure 59: Scenario 1, Full Authority Digital Engine Control (FADEC) Market , By Engine Type, 2026-2036

- Figure 60: Scenario 2, Full Authority Digital Engine Control (FADEC) Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Full Authority Digital Engine Control (FADEC) Market , By Region, 2026-2036

- Figure 62: Scenario 2, Full Authority Digital Engine Control (FADEC) Market , By Platform, 2026-2036

- Figure 63: Scenario 2, Full Authority Digital Engine Control (FADEC) Market , By Engine Type, 2026-2036

- Figure 64: Company Benchmark, Full Authority Digital Engine Control (FADEC) Market , 2026-2036