|

市场调查报告书

商品编码

1936051

全球国防引擎燃油帮浦市场:2026-2036Global Defense Engine Fuel Pumps Market 2026-2036 |

||||||

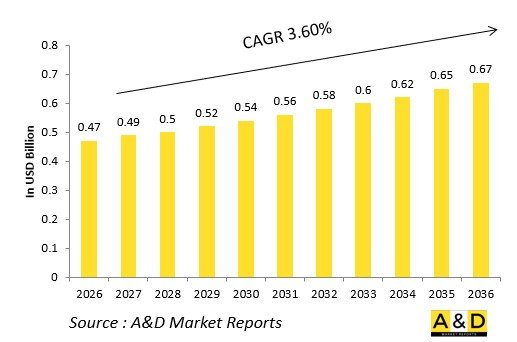

据估计,2026年全球国防发动机燃油泵市场规模为4.7亿美元,预计到2036年将达到6.7亿美元,2026年至2036年的复合年增长率(CAGR)为3.60%。

简介

全球国防引擎燃油帮浦市场透过齿轮驱动的容积式和离心式增压器,在从怠速到全加力燃烧室等各种严苛的动态工况下,为燃烧室提供精确的煤油流量。 主帮浦透过引擎上的过滤器计量燃油,紧急系统确保引擎熄火后能够重新启动。

市场发展与自适应循环引擎密切相关,这类引擎需要根据旁通比进行可变供油。核心技术包括双剪切齿轮、电液伺服机构和用于有效防止高空空化的气相分离进气口。注重弹性设计以支援无人纵深打击任务。

地缘政治上的空中优势竞争正在推动研发,优先考虑与合成燃料和定向能提取技术相容的泵。模组化组件无需拆卸引擎即可进行现场更换。抗污染涂层和高压密封件是供应链的关键考虑因素。派克、伊顿和伍德沃德先锋电气公司正在竞相引领电动主泵的研发。

国防引擎燃油帮浦的技术影响

电动燃油帮浦将燃油传输与引擎转速解耦,能够利用不受辅助齿轮箱故障影响的无刷直流马达实现精确计量。变速控制可在瞬态工况下预先调整流量,以防止燃油浓度异常波动。

整合式健康监测系统包含压力感知器和流量感知器,可为全权限数位引擎控制系统 (FADEC) 的预测性维护提供资讯。碎屑分析可侦测齿轮磨损。碳复合材料叶轮显着降低了惯性负荷,同时也能抵抗异物损伤。静电集尘器可在燃油进入帮浦入口前捕捉亚微米级污染物。

自适应控制律可补偿气候变迁造成的燃油热膨胀,并维持喷射品质。双通道冗余设计可交叉验证燃油输送与燃烧室需求。具有多孔金属筛网的耐蒸气入口可在上升过程中分离气体。

级联式结构将助推级和主级分层,优化每一级的压升。 3D列印的螺旋齿轮可实现客製化齿形,最大限度地减少剪切热。数位孪生技术利用战损引擎验证泵浦的特性。这些创新确保即使在9G机动下也能维持燃烧稳定性。

国防引擎燃油帮浦的关键驱动因素

自适应循环引擎需要与涡轮转速无关的可变流量,这推动了电动帮浦相对于变速箱驱动设计的应用。第六代无人平台需要独立于启动盒的重启能力。

维护成本有利于无需定期更换的启动盒设计。出口市场要求合成燃料与联盟相容。在超音速巡航过渡期间,即时、无喘振的燃料供应至关重要。

预算限制优先考虑采用军用加固的商用衍生产品。供应链的韧性可以应付稀土磁体短缺的问题。 互通性标准使得不同引擎系列能够使用通用歧管。

高压增压等级对于定向能武器的抽取至关重要。这些要求使得泵浦成为燃烧技术的基础。

国防引擎燃油帮浦的区域发展趋势

在北美,F-35 的维修保养正在推动短距起降(STOVL)机型采用电动主帮浦。

在欧洲,为了适应阵风/颱风战斗机的分散部署,变速控制升级正在进行中。

在亚太地区,高空启动泵浦的国产化研发正在加速。例如印度的 Kaveri 和中国的 WS-15。

在中东,人们正在研发具有先进过滤能力的防沙设计。

俄罗斯正在研发高过载泵,以提高苏-57 的机动性。

韩国正将其整合到KF-21出口套件中。

无刷电气化发展趋势强劲,亚太地区的生产占有率也不断扩大。

主要国防引擎燃油帮浦专案

F135燃油系统采用电助力来测量短距起降(STOVL)升力风扇过渡和加力燃烧室喘振。

新一代战斗机(NGAD)的适配型燃油帮浦计画交付,并采用第三流量调变技术。

EJ200升级套件采用双容积式燃油泵,可实现超音速巡航流量。

印度的Kaveri引擎采用干湿混合配置,配备国产齿轮帮浦。

F119燃油帮浦可实现低蒸汽吸入,进而维持隐身性能。

阵风M88引擎整合了紧急电启动功能。

苏-57的AL-41F1帮浦可解决三维推力向量控制过程中的瞬态问题。

T-50的FADEC控制流量系统可防止压缩机失速。

目录

国防引擎燃油帮浦市场 - 目录

国防引擎燃油帮浦市场报告定义

国防引擎燃油帮浦市场细分

依平台

依泵浦类型

依驱动系统

依燃油种类

未来十年国防引擎燃油帮浦市场分析

本章将对未来十年国防引擎燃油泵市场进行分析,详细概述市场成长、趋势变化、技术应用情况以及整体市场吸引力。

国防引擎燃油帮浦市场技术概览

本部分讨论了预计将影响该市场的十大技术,以及这些技术可能对整体市场产生的影响。

全球国防引擎燃油帮浦市场预测

以上各部分详细涵盖了该市场未来十年的预测。

区域国防引擎燃油帮浦市场趋势及预测

本部分涵盖了区域反无人机市场的趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术因素。此外,还提供了详细的区域市场预测和情境分析。区域分析最后对主要公司、供应商格局和公司基准进行了概述。目前市场规模是基于 "一切照旧" 情境估算的。

北美

驱动因素、限制因素与挑战

PEST分析

市场预测与情境分析

主要公司

供应商层级结构

公司标竿分析

欧洲

中东

亚太地区

南美洲

国防引擎燃油帮浦市场国家分析

本章涵盖该市场的主要国防项目以及最新的市场动态和专利申请资讯。此外,本章也提供未来十年各国的市场预测和情境分析。

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

南非

韩国

日本

马来西亚

新加坡

巴西

国防引擎燃油帮浦市场机会矩阵

机会矩阵帮助读者了解该市场中高机会细分领域。

国防引擎燃油帮浦市场报告专家意见

本报告总结了我们专家对此市场分析潜力的意见。

结论

关于航空与国防市场报告

The Global Defense Engine Fuel Pumps Market is estimated at USD 0.47 billion in 2026, projected to grow to USD 0.67 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.60% over the forecast period 2026-2036.

Introduction

The global Defense Engine Fuel Pumps market delivers precise kerosene flow to combustors under extreme dynamics, from idle to full afterburner via gear-driven positive displacement and centrifugal boosters. Main pumps meter fuel through engine-mounted filters, while emergency systems ensure restart capability post-flameout.

Market evolution tracks adaptive cycle engines requiring variable delivery across bypass ratios. Core technologies include dual-shear gears, electro-hydraulic servos, and vapor-separating inlets preventing cavitation at altitude. Emphasis on fault-tolerant designs supports unmanned deep-strike missions.

Geopolitical air superiority competitions drive development, prioritizing pumps compatible with synthetic fuels and directed-energy power extraction. Modular cartridges enable field replacement without engine teardown. Supply chains focus on contamination-resistant coatings and high-pressure seals. Competition features Parker, Eaton, and Woodward pioneering electric main pumps.

Technology Impact in Defense Engine Fuel Pumps

Electric fuel pumps decouple delivery from engine speed, enabling precise metering via brushless DC motors independent of accessory gearbox failures. Variable speed controllers adjust flow preemptively during transients, preventing rich/lean excursions.

Integrated health monitoring embeds pressure transducers and flow sensors feeding FADEC prognostics, detecting gear wear via debris analysis. Carbon composite impellers resist foreign object damage while slashing inertial loads. Electrostatic precipitators capture submicron contaminants before pump faces.

Adaptive control laws compensate for fuel thermal expansion across climates, maintaining spray quality. Dual-channel redundancy cross-checks delivery against combustor demands. Vapor tolerant inlets with porous metal screens separate gas during climbs.

Cascaded architectures layer boost then main stages, each optimized for pressure rise. 3D-printed helical gears enable custom tooth profiles minimizing shear heating. Digital twins validate pump signatures against battle-damaged engines. These innovations ensure combustion stability under 9g maneuvers.

Key Drivers in Defense Engine Fuel Pumps

Adaptive cycle engines demand variable flow independent of spool speeds, driving electric pump adoption over gearbox slaves. Sixth-generation unmanned platforms require restart capability without starter cart dependency.

Sustainment economics favor cartridge designs eliminating scheduled removals. Export markets need synthetic fuel compatibility across coalitions. Supercruise transitions mandate instantaneous delivery without surge.

Budget pressures prioritize commercial derivatives with military hardening. Supply chain resilience counters rare-earth magnet shortages. Interoperability standards enable common manifolds across engine families.

Directed-energy weapons extraction requires high-pressure boost stages. These imperatives position pumps as combustion enablers.

Regional Trends in Defense Engine Fuel Pumps

North America leads with F-35 sustainment driving electric main pumps for STOVL profiles.

Europe upgrades Rafale/Typhoon with variable speed controllers for dispersed basing.

Asia-Pacific accelerates indigenous development-India's Kaveri, China's WS-15-for high-altitude startups.

Middle East pursues sand-tolerant designs with advanced filtration.

Russia advances high-g tolerant pumps for Su-57 agility.

South Korea integrates with KF-21 export packages.

Trends favor brushless electric; Asia-Pacific gains manufacturing share.

Key Defense Engine Fuel Pumps Programs

F135 fuel system meters STOVL lift fan transitions and afterburner surges via electric boost.

NGAD adaptive pumps schedule delivery with third-stream modulation.

EJ200 upgrades deliver supercruise flow through dual positive displacement.

India's Kaveri equips dry/wet variants with indigenous gear pumps.

F119 pumps sustain stealth missions with low-vapor inlets.

Rafale M88 integrates emergency electric restart capability.

Su-57 AL-41F1 pumps handle 3D thrust vectoring transients.

T-50 FADEC-driven metering prevents compressor stalls.

Table of Contents

Defense Engine Fuel Pumps Market - Table of Contents

Defense Engine Fuel Pumps Market Report Definition

Defense Engine Fuel Pumps Market Segmentation

By Platform

By Pump Type

By Drive Method

By Fuel Type

Defense Engine Fuel Pumps Market Analysis for next 10 Years

The 10-year Defense Engine Fuel Pumps market analysis would give a detailed overview of Defense Engine Fuel Pumps market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Engine Fuel Pumps Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Engine Fuel Pumps Market Forecast

The 10-year Defense Engine Fuel Pumps market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Engine Fuel Pumps Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Engine Fuel Pumps Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Engine Fuel Pumps Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Engine Fuel Pumps Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Pump Type, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Fuel Type, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Pump Type, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Fuel Type, 2026-2036

List of Figures

- Figure 1: Global Defense Engine Fuel Pumps Market Forecast, 2026-2036

- Figure 2: Global Defense Engine Fuel Pumps Market Forecast, By Pump Type, 2026-2036

- Figure 3: Global Defense Engine Fuel Pumps Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Engine Fuel Pumps Market Forecast, By Fuel Type, 2026-2036

- Figure 5: North America, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 9: South America, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 10: United States, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Engine Fuel Pumps Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 28: Brazil, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Engine Fuel Pumps Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Engine Fuel Pumps Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Engine Fuel Pumps Market, By Pump Type (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Engine Fuel Pumps Market, By Pump Type (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Engine Fuel Pumps Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Engine Fuel Pumps Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Engine Fuel Pumps Market, By Fuel Type (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Engine Fuel Pumps Market, By Fuel Type (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Engine Fuel Pumps Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Engine Fuel Pumps Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Engine Fuel Pumps Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Engine Fuel Pumps Market, By Pump Type, 2026-2036

- Figure 58: Scenario 1, Defense Engine Fuel Pumps Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Engine Fuel Pumps Market, By Fuel Type, 2026-2036

- Figure 60: Scenario 2, Defense Engine Fuel Pumps Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Engine Fuel Pumps Market, By Pump Type, 2026-2036

- Figure 62: Scenario 2, Defense Engine Fuel Pumps Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Engine Fuel Pumps Market, By Fuel Type, 2026-2036

- Figure 64: Company Benchmark, Defense Engine Fuel Pumps Market, 2026-2036

全球国防燃油输送/增压帮浦市场:2026-2036全球国防用发动机驱动液压帮浦市场(2026-2036 年)

全球国防燃油输送/增压帮浦市场:2026-2036全球国防用发动机驱动液压帮浦市场(2026-2036 年) 全球油气泵市场:市场规模、占有率、成长、依类型和应用划分的产业分析、区域洞察及预测(2026-2034)

全球油气泵市场:市场规模、占有率、成长、依类型和应用划分的产业分析、区域洞察及预测(2026-2034) 2026年全球油气帮浦市场报告

2026年全球油气帮浦市场报告 燃油泵市场-全球产业规模、份额、趋势、机会、预测:按技术、应用、地区和竞争格局划分,2021-2031年

燃油泵市场-全球产业规模、份额、趋势、机会、预测:按技术、应用、地区和竞争格局划分,2021-2031年 无刷燃油泵市场按电压、帮浦控制、燃油类型、帮浦类型、应用、最终用途和销售管道,全球预测,2026-2032年

无刷燃油泵市场按电压、帮浦控制、燃油类型、帮浦类型、应用、最终用途和销售管道,全球预测,2026-2032年 混合动力燃油帮浦市场规模、份额和成长分析(按车辆类型、技术和地区划分)-2026-2033年产业预测

混合动力燃油帮浦市场规模、份额和成长分析(按车辆类型、技术和地区划分)-2026-2033年产业预测 石油和天然气泵市场按泵类型、应用、最终用户和地区划分全球油气泵市场-2025-2030年预测燃油帮浦市场-2025年至2030年预测

石油和天然气泵市场按泵类型、应用、最终用户和地区划分全球油气泵市场-2025-2030年预测燃油帮浦市场-2025年至2030年预测