|

市场调查报告书

商品编码

1951132

全球防务光电瞄准器(EOD)市场(2026-2036)Global Defense Electro-Optical Directors (EOD) Market 2026-2036 |

||||||

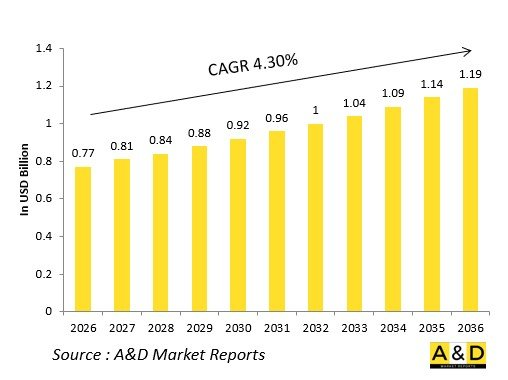

全球防务光电瞄准器(EOD)市场预计在2026年达到7.7亿美元,预计到2036年将达到11.9亿美元,2026年至2036年的复合年增长率(CAGR)为4.30%。

引言

随着全球国防机构采用先进的感测器系统来提高目标追踪、监视和火力控制的精度,全球防务光电瞄准器(EOD)市场持续稳定成长。 光电瞄准系统(EOD)整合了成像感测器、红外线探测器和雷射指示器,可在各种环境条件下实现高精度目标捕获。这些系统正越来越多地部署在海军、陆地和空中平台上,以支援一体化指挥控制行动。随着自动化探测和多感测器融合的日益重要,EOD 在以网路为中心的战术架构中的作战角色正在被重新定义。主要国防机构的现代化专案强调模组化、软体可升级的系统,这些系统能够与先进武器平台整合。随着威胁日益复杂,交战精准度变得愈发关键,光电瞄准具(EOD)对于态势感知、精确打击和威胁识别至关重要,并已成为全球智慧作战和监视系统发展的关键推动因素。

科技对光电瞄准具(EOD)的影响

持续的技术创新正在重新定义光电瞄准具(EOD)的功能和应用范围。 现代电子爆炸物处理 (EOD) 系统配备了先进的成像感测器、高解析度热像仪和多光谱探测能力,即使在低能见度和交战环境下也能实现卓越的目标追踪。人工智慧和机器学习的整合增强了自动目标识别、资料关联和动态威胁优先排序,从而减轻了操作员的工作负荷并缩短了回应时间。数位稳定技术和高速万向节支架提高了平台移动时的成像精度,使其成为海空作战的关键装备。开放式架构设计支援与雷达系统、雷射导引系统和通讯网路的互通性,从而增强了多域协作。人工智慧驱动的分析功能可实现预测性监控和自适应校准,以优化感测器效能。总而言之,技术整合正在将 EOD 系统从传统的光学追踪器转变为多感测器认知资产,这对于现代国防行动中的即时态势感知和精确打击至关重要。

电子光学瞄准镜 (EOD) 的主要驱动因素

多种战略和战斗因素正在推动电子光学瞄准镜 (EOD) 市场的成长。 对精确作战的日益依赖以及在非对称威胁环境下增强识别能力的需求,正推动着爆炸物处理(EOD)系统在海军舰艇、装甲车辆和飞机上的部署。对感测器融合和网路化目标架构的投入不断增加,正在强化光电技术在监视和火力控制中的作用。国防现代化工作致力于取代过时的光机系统,这推动了对紧凑、轻巧且全数位化EOD解决方案的需求。海上和边境安全行动频率的增加也促进了昼夜成像系统采购的扩大。此外,全球向无人和远端操作平台的转变,正在拓宽光电目标处理(EOD)系统在有人和自主系统中的应用。随着现代作战系统不断整合多域感测器,EOD能力正成为下一代防御态势的核心组成部分。

光电瞄准(EOD)的区域趋势

由于国防战略、工业基础和安全优先事项的差异,各地区对光电瞄准(EOD)系统的需求各不相同。北美在先进EOD技术的研究、开发和部署方面继续处于领先地位,这些技术与精确导引武器和海军火控系统整合。欧洲国家则强调联合感测器规划和模组化设计,以增强多国国防平台之间的互通性。受领土安全需求、海上监视和国内产业成长的驱动,亚太地区正在迅速扩大对光电瞄准器(EOD)的采购。

本报告分析了全球国防光电瞄准器(EOD)市场,提供了影响该市场的技术资讯、未来十年的预测以及区域趋势。

目录

国防光电瞄准器(EOD)市场报告定义

国防光电瞄准器(EOD)市场细分

依地区

依平台

依安装方式

依波长

未来十年国防光电瞄准器(EOD)市场分析

国防光电瞄准器 (EOD) 市场技术

全球国防光电瞄准器 (EOD) 市场预测

区域国防光电瞄准器 (EOD) 市场趋势与预测

北美

驱动因素、限制因素与挑战

PEST 分析

市场预测与情境分析

主要公司

供应商层级概览

公司基准分析

欧洲

中东

亚太地区

南美洲

国防光电瞄准器 (EOD) 市场国家分析

美国

国防项目

最新消息

专利

当前市场技术成熟度

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

德国

澳洲

南非

印度

中国

俄罗斯

南非

韩国日本

马来西亚

新加坡

巴西

国防光电瞄准器 (EOD) 市场机会矩阵

专家对国防光电瞄准器 (EOD) 市场报告的意见

结论

关于航空和国防市场报告

The Global Defense electro-optical directors (EOD) market is estimated at USD 0.77 billion in 2026, projected to grow to USD 1.19 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.30% over the forecast period 2026-2036.

Introduction:

The Global Defense electro-optical directors (EOD) market is experiencing steady expansion as defense forces worldwide adopt advanced sensor systems to enhance target tracking, surveillance, and fire control accuracy. Electro-optical directors integrate imaging sensors, infrared detectors, and laser designators to provide high-precision target acquisition under diverse environmental conditions. These systems are increasingly deployed across naval, land, and airborne platforms, supporting integrated command and control operations. The growing emphasis on automated detection and multi-sensor fusion is reshaping the operational role of EODs within network-centric warfare architectures. Modernization programs across major defense forces emphasize modular, software-upgradable systems capable of integrating with advanced weapon platforms. As threats become more complex and engagements demand greater accuracy, electro-optical directors have become indispensable for situational awareness, precision engagement, and threat identification, positioning them as a key enabler in the evolution of smart combat and surveillance systems globally.

Technology Impact in Electro-Optical Directors (EOD)

Continuous technological advancement is redefining the performance and application scope of electro-optical directors. Modern EOD systems feature advanced imaging sensors, high-resolution thermal cameras, and multispectral detection capabilities, enabling superior target tracking in low-visibility and contested environments. Integration of artificial intelligence and machine learning enhances automated target recognition, data correlation, and dynamic threat prioritization, reducing operator workload and response times. Digital stabilization technologies and high-speed gimballed mounts improve imaging accuracy during platform motion, making them essential for both naval and airborne missions. Open architecture design supports interoperability with radar systems, laser guidance units, and communication networks, reinforcing coordination across multiple domains. AI-powered analytics now allow predictive monitoring and adaptive calibration for optimal sensor performance. Overall, technology integration is transforming EOD systems from traditional optical trackers into multi-sensor, cognitive assets critical for real-time situational awareness and precision engagement in modern defense operations.

Key Drivers in Electro-Optical Directors (EOD)

Multiple strategic and operational factors are propelling growth within the electro-optical directors market. Increasing reliance on precision warfare and the need for enhanced identification in asymmetric threat environments drive the deployment of EOD systems across naval vessels, armored vehicles, and aircraft. Rising investment in sensor fusion and networked targeting architectures strengthens the role of electro-optical technology in both surveillance and fire control. Defense modernization initiatives, focused on replacing legacy opto-mechanical systems, are fueling demand for compact, lightweight, and fully digital EOD solutions. The growing frequency of maritime and border security operations also contributes to increased procurement of day-and-night imaging systems. Furthermore, the global shift toward unmanned and remotely operated platforms is expanding applications of electro-optical directors across both manned and autonomous systems. As modern combat systems continue to integrate multi-domain sensors, EOD capabilities have become central to next-generation defense readiness.

Regional Trends in Electro-Optical Directors (EOD)

Regional demand for electro-optical directors varies with differing defense strategies, industrial capabilities, and security priorities. North America continues to lead in research, development, and deployment of advanced EOD technologies integrated with precision-guided weapons and naval fire control systems. European nations emphasize collaborative sensor programs and modular designs to enhance interoperability across multinational defense platforms. The Asia-Pacific region is rapidly expanding its electro-optical director acquisitions, driven by territorial security needs, maritime surveillance, and indigenous industrial growth. In the Middle East, modernization of naval and air assets stimulates demand for EOD systems capable of operating in harsh desert and maritime conditions. Emerging economies in Latin America and Africa are gradually adopting these capabilities through partnerships with global defense suppliers. Across all regions, investment in electro-optical technology reflects a strategic commitment to maintaining visual dominance and improving target engagement reliability in evolving threat environments.

Key Electro-Optical Directors (EOD) Programs

Several key defense programs across the globe underscore the strategic importance of electro-optical directors in modern warfare. Leading defense contractors are developing next-generation EOD systems featuring multi-spectral imaging, AI-enabled processing, and real-time data fusion for integration into advanced combat platforms. Naval programs increasingly incorporate EOD solutions within fire control suites to enhance shipborne engagement precision and situational awareness. Land-based initiatives focus on compact sensor packages compatible with armored vehicles and autonomous surveillance systems. Concurrently, air forces are upgrading targeting pods with improved electro-optical tracking and laser designation systems. Many nations are investing in indigenous EOD technologies through joint ventures and defense-industrial partnerships aimed at strengthening local production capabilities. These programs collectively highlight the transition toward intelligent, networked optical systems designed to meet the demands of high-speed, information-centric warfare across multiple operational domains.

Table of Contents

Defense Electro-Optical Directors (EOD) Market - Table of Contents

Defense Electro-Optical Directors (EOD) Market Report Definition

Defense Electro-Optical Directors (EOD) Market Segmentation

By Region

By Platform

By Mounting

By Wavelength

Defense Electro-Optical Directors (EOD) Market Analysis for next 10 Years

The 10-year Defense Electro-Optical Directors (EOD) Market analysis would give a detailed overview of Defense Electro-Optical Directors (EOD) Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Electro-Optical Directors (EOD) Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Electro-Optical Directors (EOD) Market Forecast

The 10-year Defense Electro-Optical Directors (EOD) Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Electro-Optical Directors (EOD) Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Electro-Optical Directors (EOD) Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Electro-Optical Directors (EOD) Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Electro-Optical Directors (EOD) Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Mounting, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Platform, 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Mounting, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Platform, 2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Region, 2026-2036

List of Figures

- Figure 1: Global Defense Electro-Optical Directors (EOD) Market Forecast, 2026-2036

- Figure 2: Global Defense Electro-Optical Directors (EOD) Market Forecast, By Mounting, 2026-2036

- Figure 3: Global Defense Electro-Optical Directors (EOD) Market Forecast, By Platform, 2026-2036

- Figure 4: Global Defense Electro-Optical Directors (EOD) Market Forecast, By Region, 2026-2036

- Figure 5: North America, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 6: Europe, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 7: Middle East, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 8: APAC, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 9: South America, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 10: United States, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 11: United States, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 12: Canada, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 13: Canada, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 14: Italy, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 15: Italy, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 16: France, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 17: France, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 18: Germany, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 19: Germany, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 21: Netherlands, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 22: Belgium, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 23: Belgium, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 24: Spain, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 25: Spain, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 26: Sweden, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 27: Sweden, Defense Electro-Optical Directors (EOD) Market, Forecast, 2026-2036

- Figure 28: Brazil, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 29: Brazil, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 30: Australia, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 31: Australia, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 32: India, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 33: India, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 34: China, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 35: China, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 38: South Korea, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 39: South Korea, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 40: Japan, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 41: Japan, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 43: Malaysia, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 44: Singapore, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 45: Singapore, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense Electro-Optical Directors (EOD) Market, Technology Maturation, 2026-2036

- Figure 47: United Kingdom, Defense Electro-Optical Directors (EOD) Market, Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense Electro-Optical Directors (EOD) Market, By Mounting (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense Electro-Optical Directors (EOD) Market, By Mounting (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense Electro-Optical Directors (EOD) Market, By (Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense Electro-Optical Directors (EOD) Market, By Platform(CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense Electro-Optical Directors (EOD) Market, By Region (Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense Electro-Optical Directors (EOD) Market, By Region (CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense Electro-Optical Directors (EOD) Market, Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense Electro-Optical Directors (EOD) Market, Global Market, 2026-2036

- Figure 56: Scenario 1, Defense Electro-Optical Directors (EOD) Market, Total Market, 2026-2036

- Figure 57: Scenario 1, Defense Electro-Optical Directors (EOD) Market, By Mounting, 2026-2036

- Figure 58: Scenario 1, Defense Electro-Optical Directors (EOD) Market, By Platform, 2026-2036

- Figure 59: Scenario 1, Defense Electro-Optical Directors (EOD) Market, By Region, 2026-2036

- Figure 60: Scenario 2, Defense Electro-Optical Directors (EOD) Market, Total Market, 2026-2036

- Figure 61: Scenario 2, Defense Electro-Optical Directors (EOD) Market, By Mounting, 2026-2036

- Figure 62: Scenario 2, Defense Electro-Optical Directors (EOD) Market, By Platform, 2026-2036

- Figure 63: Scenario 2, Defense Electro-Optical Directors (EOD) Market, By Region, 2026-2036

- Figure 64: Company Benchmark, Defense Electro-Optical Directors (EOD) Market, 2026-2036