|

市场调查报告书

商品编码

2023796

2026-2036年全球航太和国防工业铜需求:Global Copper demand in Aerospace & Defense Industry 2026-2036 |

||||||

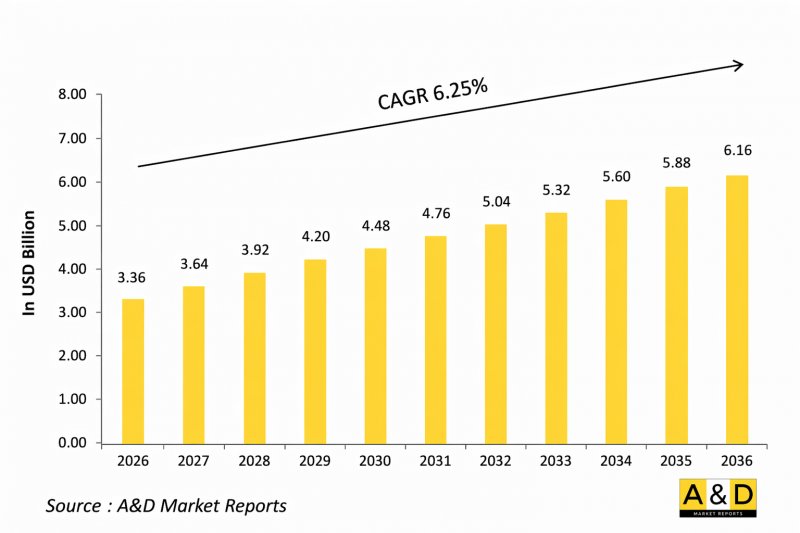

全球航太和国防工业对铜的需求

2026 年全球航太和国防工业对铜的需求量估计为 33.6 亿美元,预计在 2026 年至 2036 年的预测期内,将以 6.25% 的复合年增长率增长,到 2036 年达到 61.6 亿美元。

1. 引言

全球航太和国防工业对铜的需求对于现代军事和航空系统至关重要。铜因其卓越的导电性、导热性和耐腐蚀性而备受青睐,是飞机、船舰、地面系统和先进国防电子设备的关键材料。随着航太平台电气化和数位化程度的不断提高,对铜基组件的依赖性也持续增长。从线束和航空电子设备到雷达系统和通讯网络,铜在确保可靠性和性能方面发挥基础性作用。此外,向先进材料和下一代国防技术的转型进一步提升了高品质导电材料的重要性。人们对能源效率、轻量化和提升作战能力的日益关注也进一步推动了铜的使用。随着全球国防现代化和航太创新的加速发展,铜的需求预计将继续成为支撑高性能军事和航空系统发展的关键要素。

2. 科技对全球航太和国防工业铜需求的影响

航太和国防系统的技术进步正显着影响着各种应用领域对铜的需求。随着更多电气化和全电动飞机概念的采用,对高性能布线和配电系统的需求激增,而铜凭藉其卓越的导电性,仍然是首选材料。先进的航空电子设备、雷达系统和通讯技术高度依赖铜基组件,以确保稳定的讯号传输和系统效率。此外,人工智慧、感测器网路和电子战系统的整合也增加了对强大电力基础设施的需求,进一步推动了铜的消耗。

此外,定向能量武器、高功率运算系统和下一代推进技术的出现,对高效的温度控管解决方案提出了更高的要求,而铜的散热性能在其中至关重要。轻质铜合金和复合材料的创新使製造商能够在性能和重量减轻之间取得平衡,这在航太设计中是一个关键考虑因素。随着国防平台技术日趋复杂和互联互通,铜在整个现代军事生态系统中继续发挥核心作用,确保可靠、快速和节能的运作。

3.航太和国防工业对全球铜需求的主要驱动因素

推动航太和国防领域铜需求成长的关键因素有很多。其中一个主要因素是飞机和国防平台的电气化程度不断提高,这需要大规模的布线系统和电气元件。随着航空电子设备、通讯系统和关键任务电子设备的日益复杂,对可靠导电材料的需求也进一步增长。此外,各国国防现代化计画都致力于用先进的电子系统升级现有平台,也增加了铜的消耗量。

太空探勘计画和卫星部署的扩展是另一个重要因素,因为这些系统在电力传输和温度控管高度依赖铜基组件。此外,无人机和自动驾驶车辆等无人系统的兴起,也增加了对紧凑高效电气系统的需求。航太设计中对能源效率和永续性的日益重视,也推动了铜的应用,因为铜具有可回收性和性能优势。这些因素共同作用,预计将使不断发展的航太和国防领域对铜的需求保持强劲。

4.航太和国防工业全球铜需求的区域趋势

航太和国防工业对铜的需求区域趋势受技术进步、国防费用和工业产能差异的影响。北美凭藉其强大的航太製造业基础和对先进国防技术的持续投资,仍然是主要需求区域。欧洲也是重要的需求来源,其成熟的航太工业和联合国防倡议推动了对铜基系统的稳定需求。

亚太地区正经历快速成长,这主要得益于航太能力的提升、国防预算的增加以及对国内製造业项目的投资成长。印度和中国等国家正致力于发展先进的军事平台并扩大航空业,这推动了铜需求的成长。中东地区也逐步增加对国防和航太基础设施的投资,从而促进了该地区铜需求的成长。同时,拉丁美洲和非洲作为新兴市场,随着先进技术的逐步应用和现代化进程的推进,航太和国防应用领域对铜的需求也缓慢增长。

5.航太和国防工业领域全球铜需求的主要趋势

影响航太和国防工业铜需求的关键项目与现代化倡议、先进飞机研发以及下一代国防系统密切相关。世界各国政府和国防机构都在投资研发「全电」飞机,这类飞机高度依赖铜基电气系统来实现高效率的电力分配。军用飞机升级项目,例如为老旧机型加装先进的航空电子设备、通讯系统和电子战设备,也在推动铜的需求。

海军现代化项目,包括先进军舰和潜水艇的研发,由于电气系统和电源管理技术的广泛应用,进一步推高了对铜的需求。此外,太空探勘专案和卫星部署工作也为高效能环境下的铜应用创造了新的机会。无人驾驶航空器系统和自主防御平台的研发是另一个铜需求不断成长的重要领域。这些项目共同凸显了铜在实现下一代航太和国防能力方面所发挥的战略性重要作用。

目录

航太和国防市场中的铜製部件 - 目录

航太和国防市场报告中铜部件的定义

航太与国防市场细分

按组件

透过流程

按地区

合金

未来十年航太与国防市场铜零件分析

本章详细分析了过去十年航太和国防领域的铜部件市场,说明了其成长、发展趋势、技术采用和市场吸引力。

门禁控制技术市场

本节将说明预计将对该市场产生影响的十大技术及其对整个市场的潜在影响。

全球门禁控制市场预测

上述各细分市场对该市场未来 10 年的门禁控制市场预测进行了详细说明。

区域门禁控制市场趋势与预测

本部分将说明区域门禁管制市场的趋势、驱动因素、限制因素、挑战以及政治、经济、社会和技术方面的问题。此外,还将提供详细的区域市场预测和情境分析。区域分析的最后一部分将介绍主要企业概况、供应商格局和公司基准。目前市场规模是基于典型情境估算的。

北美洲

促进因素、阻碍因素、挑战

害虫

市场预测与情境分析

主要企业

供应商层级状态

企业标竿管理

欧洲

中东

亚太地区

南美洲

各国门禁控制市场分析

本章将说明该市场的主要国防项目,以及该市场的最新新闻和专利申请。此外,还将说明针对特定国家的十年市场预测和情境分析。

我们

国防计划

最新消息

专利

该市场目前的技术成熟度水平

市场预测与情境分析

加拿大

义大利

法国

德国

荷兰

比利时

西班牙

瑞典

希腊

澳洲

南非

印度

中国

俄罗斯

韩国

日本

马来西亚

新加坡

巴西

门禁控制市场机会矩阵

机会矩阵帮助读者了解该市场中具有高机会的细分市场。

专家对门禁控制市场报告的意见

我们总结了专家们对该市场分析潜力的意见。

结论

关于航空航太和国防市场报告

Global Copper Demand in Aerospace & Defense Industry

The Global Copper demand in Aerospace & Defense Industry is estimated at USD 3.36 billion in 2026, projected to grow to USD 6.16 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 6.25% over the forecast period 2026-2036.

1. Introduction

The global copper demand in the aerospace and defense industry represents a vital component of modern military and aviation systems. Copper is widely valued for its excellent electrical conductivity, thermal efficiency, and corrosion resistance, making it indispensable in aircraft, naval vessels, ground systems, and advanced defense electronics. As aerospace platforms become increasingly electrified and digitally integrated, the reliance on copper-based components continues to expand. From wiring harnesses and avionics to radar systems and communication networks, copper plays a foundational role in ensuring reliability and performance. Additionally, the shift toward advanced materials and next-generation defense technologies has reinforced the importance of high-quality conductive materials. The growing emphasis on energy efficiency, lightweight systems, and enhanced operational capabilities further drives copper utilization. As global defense modernization and aerospace innovation accelerate, copper demand is expected to remain a critical factor in supporting the evolution of high-performance military and aviation systems.

2. Technology Impact in Global Copper Demand in Aerospace & Defense Industry

Technological advancements in aerospace and defense systems are significantly influencing the demand for copper across various applications. The increasing adoption of more-electric and all-electric aircraft concepts has led to a surge in demand for high-performance wiring and power distribution systems, where copper remains a preferred material due to its superior conductivity. Advanced avionics, radar systems, and communication technologies rely heavily on copper-based components to ensure stable signal transmission and system efficiency. Furthermore, the integration of artificial intelligence, sensor networks, and electronic warfare systems has expanded the need for robust electrical infrastructure, further strengthening copper consumption.

In addition, the emergence of directed energy weapons, high-power computing systems, and next-generation propulsion technologies requires efficient thermal management solutions, where copper's heat dissipation properties are critical. Innovations in lightweight copper alloys and composite materials are also enabling manufacturers to balance performance with weight reduction, a key consideration in aerospace design. As defense platforms become more technologically sophisticated and interconnected, copper continues to play a central role in enabling reliable, high-speed, and energy-efficient operations across modern military ecosystems.

3. Key Drivers in Global Copper Demand in Aerospace & Defense Industry

Several key factors are driving the demand for copper in the aerospace and defense sector. One of the primary drivers is the increasing electrification of aircraft and defense platforms, which requires extensive wiring systems and electrical components. The growing complexity of avionics, communication systems, and mission-critical electronics has further amplified the need for reliable conductive materials. Additionally, defense modernization programs across various countries are focusing on upgrading existing platforms with advanced electronic systems, thereby boosting copper consumption.

The expansion of space exploration initiatives and satellite deployment is another significant driver, as these systems depend heavily on copper-based components for power transmission and thermal management. Furthermore, the rise of unmanned systems, including drones and autonomous vehicles, has increased the demand for compact and efficient electrical systems. The emphasis on energy efficiency and sustainability in aerospace design is also encouraging the use of copper due to its recyclability and performance advantages. These combined factors are expected to sustain strong demand for copper in the evolving aerospace and defense landscape.

4. Regional Trends in Global Copper Demand in Aerospace & Defense Industry

Regional trends in copper demand within the aerospace and defense industry are shaped by varying levels of technological advancement, defense spending, and industrial capabilities. North America remains a leading region due to its strong aerospace manufacturing base and continuous investment in advanced defense technologies. Europe is also a significant contributor, with established aerospace industries and collaborative defense initiatives driving steady demand for copper-based systems.

The Asia-Pacific region is experiencing rapid growth, fueled by expanding aerospace capabilities, increasing defense budgets, and rising investments in indigenous manufacturing programs. Countries such as India and China are focusing on developing advanced military platforms and expanding their aviation sectors, which in turn boosts copper demand. The Middle East is gradually increasing its investments in defense and aerospace infrastructure, contributing to regional demand growth. Meanwhile, Latin America and Africa are emerging markets, with gradual adoption of advanced technologies and modernization efforts supporting incremental demand for copper in aerospace and defense applications.

5. Key Global Copper Demand in Aerospace & Defense Industry Program

Key programs influencing copper demand in the aerospace and defense industry are closely tied to modernization initiatives, advanced aircraft development, and next-generation defense systems. Governments and defense organizations worldwide are investing in the development of more-electric aircraft, which rely heavily on copper-based electrical systems for efficient power distribution. Military aircraft upgrade programs are also driving demand, as older platforms are retrofitted with advanced avionics, communication systems, and electronic warfare capabilities.

Naval modernization programs, including the development of advanced warships and submarines, further contribute to copper demand due to the extensive use of electrical systems and power management technologies. Additionally, space exploration programs and satellite deployment initiatives are creating new opportunities for copper utilization in high-performance environments. The development of unmanned aerial systems and autonomous defense platforms is another key area where copper demand is increasing. These programs collectively highlight the strategic importance of copper in enabling the next generation of aerospace and defense capabilities.

Table of Contents

Copper Component In The Aerospace And Defense Market - Table of Contents

Copper Component In The Aerospace And Defense Market Report Definition

Copper Component In The Aerospace And Defense Market Segmentation

By Component

By Process

By Region

By Alloy

Copper Component In The Aerospace And Defense Market Analysis for next 10 Years

The 10-year Copper Component In The Aerospace And Defense market analysis would give a detailed overview of Copper Component In The Aerospace And Defense market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Access Control Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Access Control Market Forecast

The 10-year access control market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Access Control Market Trends & Forecast

The regional access control market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Access Control Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Access Control Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Access Control Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2026-2036

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2026-2036

- Table 18: Scenario Analysis, Scenario 1, By Alloy 2026-2036

- Table 19: Scenario Analysis, Scenario 1, By Process, 2026-2036

- Table 20: Scenario Analysis, Scenario 2, By Region, 2026-2036

- Table 21: Scenario Analysis, Scenario 2, By Alloy2026-2036

- Table 22: Scenario Analysis, Scenario 2, By Process, 2026-2036

List of Figures

- Figure 1: Global Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market Forecast, 2026-2036

- Figure 2: Global Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market Forecast, By Region, 2026-2036

- Figure 3: Global Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market Forecast, By Alloy2026-2036

- Figure 4: Global Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market Forecast, By Process, 2026-2036

- Figure 5: North America, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 6: Europe, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 7: Middle East, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 8: APAC, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 9: South America, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 10: United States, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 11: United States, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 12: Canada, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 13: Canada, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 14: Italy, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 15: Italy, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 16: France, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 17: France, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 18: Germany, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 19: Germany, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 20: Netherlands, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 21: Netherlands, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 22: Belgium, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 23: Belgium, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 24: Spain, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 25: Spain, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 26: Sweden, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 27: Sweden, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 28: Brazil, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 29: Brazil, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 30: Australia, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 31: Australia, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 32: India, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 33: India, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 34: China, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 35: China, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 36: Saudi Arabia, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 37: Saudi Arabia, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 38: South Korea, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 39: South Korea, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 40: Japan, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 41: Japan, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 42: Malaysia, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 43: Malaysia, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 44: Singapore, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 45: Singapore, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 46: United Kingdom, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Region Maturation, 2026-2036

- Figure 47: United Kingdom, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Market Forecast, 2026-2036

- Figure 48: Opportunity Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Region (Cumulative Market), 2026-2036

- Figure 49: Opportunity Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Region (CAGR), 2026-2036

- Figure 50: Opportunity Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Alloy Cumulative Market), 2026-2036

- Figure 51: Opportunity Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Alloy CAGR), 2026-2036

- Figure 52: Opportunity Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Process(Cumulative Market), 2026-2036

- Figure 53: Opportunity Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Process(CAGR), 2026-2036

- Figure 54: Scenario Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Cumulative Market, 2026-2036

- Figure 55: Scenario Analysis, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Global Market, 2026-2036

- Figure 56: Scenario 1, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Total Market, 2026-2036

- Figure 57: Scenario 1, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Region, 2026-2036

- Figure 58: Scenario 1, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Alloy 2026-2036

- Figure 59: Scenario 1, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Process, 2026-2036

- Figure 60: Scenario 2, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , Total Market, 2026-2036

- Figure 61: Scenario 2, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Region, 2026-2036

- Figure 62: Scenario 2, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Alloy 2026-2036

- Figure 63: Scenario 2, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , By Process, 2026-2036

- Figure 64: Company Benchmark, Defense COPPER COMPONENT IN THE AEROSPACE AND DEFENSE Market , 2026-2036

吡硫翁铜市场:依产品类型、纯度等级、应用及通路划分-2026-2032年全球市场预测铜提炼市场:依原料、製程、产品及最终用途划分-2026-2032年全球市场预测

吡硫翁铜市场:依产品类型、纯度等级、应用及通路划分-2026-2032年全球市场预测铜提炼市场:依原料、製程、产品及最终用途划分-2026-2032年全球市场预测 铜:全球市场份额和排名、总收入和需求预测(2026-2032年)数控主轴市场:2026-2032年全球市场预测(依冷却方式、转速、功率范围、加工材料、安装方式、应用及最终用途产业划分)铜市场:2026-2032年全球市场预测(按形状、产品类型、应用和最终用途行业划分)铜型材市场:依产品类型、铜牌、製造流程、表面处理及最终用途产业划分,全球预测,2026-2032年铜矿开采市场:2026-2032年全球预测,依开采方法、矿石类型、产品类型、通路和应用划分

铜:全球市场份额和排名、总收入和需求预测(2026-2032年)数控主轴市场:2026-2032年全球市场预测(依冷却方式、转速、功率范围、加工材料、安装方式、应用及最终用途产业划分)铜市场:2026-2032年全球市场预测(按形状、产品类型、应用和最终用途行业划分)铜型材市场:依产品类型、铜牌、製造流程、表面处理及最终用途产业划分,全球预测,2026-2032年铜矿开采市场:2026-2032年全球预测,依开采方法、矿石类型、产品类型、通路和应用划分 2026年全球铜磷合金市场研究报告数控车床主轴市场:依主轴类型、轴配置、转速范围、轴承类型、安装方向、最终用户划分,全球预测,2026-2032年

2026年全球铜磷合金市场研究报告数控车床主轴市场:依主轴类型、轴配置、转速范围、轴承类型、安装方向、最终用户划分,全球预测,2026-2032年 无机铜化学品市场规模、份额和成长分析:按产品类型、配方类型、最终用途产业、销售管道和地区划分-2026-2033年产业预测

无机铜化学品市场规模、份额和成长分析:按产品类型、配方类型、最终用途产业、销售管道和地区划分-2026-2033年产业预测