|

市场调查报告书

商品编码

1341917

泰国服装製造业:2023-2032Thailand Garment Manufacturing Industry Research Report 2023-2032 |

||||||

泰国是东南亚第二大经济体,人均GDP约6,600美元,定位为中高收入国家。 到2022年底,该国人口将达到7080万,劳动力成本低廉,劳动力充足。 15岁及以上的劳动人口超过4024万,最低日工资约为10美元。

泰国纺织业拥有广泛的价值链,有2000多家服装和纺织公司主要集中在曼谷和泰国东部。 该行业对泰国的国内生产总值和出口收入发挥着至关重要的作用。 泰国在家用纺织品的生产、设计和营销方面表现出色,作为丝绸和纱线製造国而享誉全球。 此外,我们在符合国际标准的环保整理、染色和印花服务方面表现出色,但仍有进一步改进的空间。

泰国纺织产品主要出口到美国、日本、英国、俄罗斯和中国。 由于COVID-19期间外部需求减少,作为国家经济促进力的纺织和服装行业在2020年经历了低迷。 大约 3,000 家工厂已转向生产口罩和个人防护装备,以应对经济危机。 然而,泰国纺织业在2021年復苏并恢復了全部製造能力,泰国的服装厂和纺织厂以100%的製造能力重新启动运营。 2021年和2022年,由于越南、柬埔寨、印度尼西亚、印度、欧洲和美国等服装生产地区的需求,泰国对美国的服装出口激增。

2021年,随着疫情影响消退,泰国开始放鬆监管措施。 因此,泰国纺织服装业出口在2021年和2022年迅速恢復。 历年纺织品服装出口额分别为65.26亿美元和68.5亿美元,比上年增长13.53%和4.96%。

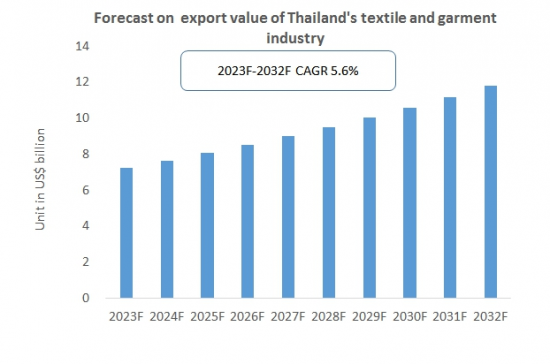

总体而言,在全球纺织服装行业向东南亚转移的推动下,全球服装市场蕴藏着巨大的商机,并处于稳步上升的轨道。 泰国纺织服装业在泰国政府的支持和推动下正在快速发展,前景广阔。 预计2032年泰国纺织品和服装出口额将增长至118亿美元,2023年至2032年復合年增长率为5.6%。

本报告对泰国服装製造业进行调查,分析泰国服装行业的经济和政策环境、市场影响因素和市场机会、市场规模趋势和预测,并对主要服装企业进行分析等进行总结。

目录

第 1 章泰国服装产业发展概况

- 定义和分类

- 主要产品分析

- COVID-19 感染对泰国服装业的影响

第 2 章泰国服装製造业分析:2018-2023

- 泰国服装业发展环境

- 经济环境

- 政策环境

- 社会环境

- 泰国服装供应分析:2018-2022

- 泰国服装行业主要外资来源分析

- 服装製造

- 泰国市场服装需求分析

- 服装的主要消费群体

- 泰国国内服装市场规模

第 3 章泰国纺织服装行业进出口分析

- 导入

- 原材料进口

- 主要进口来源

- 导出

- 泰国服装业出口分析

- 主要出口目的地

第 4 章泰国服装行业竞争状况

- 进入泰国服装业的壁垒

- 政府政策

- 销售渠道

- 品牌墙

- 泰国服装业的竞争结构

第 5 章泰国服装製造业成本与价格分析

- 泰国服装製造成本分析:2018-2022

- 原材料成本

- 人员成本分析

- 泰国服装价格分析

第 6 章泰国主要服装製造企业概况

- Toray Industries (Thailand) Co. Ltd. Toray Group

- NaRaYa

- Jaspal

- Thai Wacoal

- Disaya

第 7 章泰国服装製造业展望:2023-2032

- 影响泰国服装製造业发展的因素

- 促进因素/市场机会

- 威胁/挑战

- 展望/市场机会

- 预测竞争格局

- 供应预测

- 原材料进口预测

- 服装出口预测

- 需求预测

- 整体市场需求预测

- 需求预测:按不同类别

Thailand, as the second-largest economy in Southeast Asia, boasts a per capita GDP of approximately US$6,600, positioning it as a middle to high-income country. The country's population stood at 70.8 million by the end of 2022, and it possesses a robust labor force characterized by low labor costs. With over 40.24 million people aged 15 and above in the workforce, Thailand sustains a minimum daily wage of approximately US$10.

SAMPLE VIEW

The textile industry in Thailand encompasses a comprehensive value chain, with more than 2,000 apparel and textile companies operating, primarily concentrated in Bangkok and eastern Thailand. This sector plays a pivotal role in contributing to the country's GDP and export earnings. Thailand stands out for its proficiency in the production, design, and marketing of home textiles, earning a global reputation as a silk producer and yarn manufacturer. Moreover, the nation excels in eco-friendly finishing, dyeing, and printing services that meet international standards, although there is room for further improvement.

Thailand's textile exports are primarily directed towards the United States, Japan, the United Kingdom, Russia, and China. The country's two economic drivers, the textile and garment industry, experienced a downturn in 2020 due to reduced foreign demand during the COVID-19 pandemic. Approximately 3,000 factories pivoted to producing masks and PPE protective clothing to survive the economic challenges. However, the Thai textile industry rebounded in 2021, restoring production to full capacity, and Thai garment and textile factories resumed operations at 100% capacity. The years 2021 and 2022 witnessed a surge in Thailand's apparel exports to the United States, driven by demand from apparel-producing regions like Vietnam, Cambodia, Indonesia, India, Europe, and U.S. garment factories.

In 2021, Thailand began relaxing control measures as the pandemic's impact waned. This, in turn, led to a rapid recovery of Thailand's textile and apparel industry exports in 2021 and 2022. During these years, textile and apparel exports amounted to US$6,526 million and US$6,850 million, respectively, representing year-on-year increases of 13.53% and 4.96%.

Overall, the global garment market presents substantial opportunities, with a steady upward trajectory fueled by the relocation of the global textile and apparel industry to Southeast Asia. Thailand's textile and apparel sector is experiencing rapid growth, supported and promoted by the Thai government, suggesting a promising future. CRI anticipates that Thailand's textile and apparel exports will reach US$11.8 billion by 2032, with a Compound Annual Growth Rate (CAGR) of 5.6% from 2023 to 2032.

Topics covered:

- Thailand Garment Industry Overview

- The economic and policy environment of the Thai garment industry

- What is the impact of COVID-19 on the Thai garment industry?

- Thailand Garment Industry Market Size 2018-2022

- Analysis of major Thai garment companies

- Key Drivers and Market Opportunities in Thailand's Garment Industry

- What are the key drivers, challenges and opportunities for the Thai garment industry during the forecast period 2023-2032?

- Which are the key players in the Thailand Garment Industry market and what are their competitive advantages?

- What is the expected revenue of Thailand Garments Industry market during the forecast period of 2023-2032?

- What strategies have been adopted by the key players in the market to increase their market share in the industry?

- Which segment of the Thailand Garment Industry market is expected to dominate the market by 2032?

- What are the major unfavorable factors facing the Thai garment industry?

Table of Contents

1 Overview of the Development of Thailand's Garment Industry

- 1.1 Definitions and Classifications

- 1.2 Analysis of Major Products

- 1.3 Impact of COVID-19 on Thailand's Garment Manufacturing Industry

2 Analysis on Garment Manufacturing Industry in Thailand, 2018-2023

- 2.1 Development Environment of Thailand's Garment Industry

- 2.1.1 Economic Environment

- 2.1.2 Policy Environment

- 2.1.3 Social Environment

- 2.2 Thailand Garment Supply Analysis 2018-2022

- 2.2.1 Analysis of Major Foreign Investment Sources in Thailand's Garment Manufacturing Industry

- 2.2.2 Clothing Production

- 2.3 Thailand Market Demand Analysis for Garment

- 2.3.1 Major Consumer Groups of Clothing

- 2.3.2 Size of Thailand's Domestic Garment Market

3 Thailand Textile and Clothing Industry Import and Export Analysis

- 3.1 Imports

- 3.1.1 Import of Raw Materials

- 3.1.2 Main Sources of Imports

- 3.2 Exports

- 3.2.1 Export Analysis of Thailand's Garment Industry

- 3.2.2 Main Export Destinations

4 Competition Status of Garment Manufacturing Industry in Thailand

- 4.1 Barriers to Entry in Thailand's Clothing Industry

- 4.1.1 Government Policies

- 4.1.2 Sales Channels

- 4.1.3 Brand Barriers

- 4.2 Competitive Structure of Thailand's Garment Manufacturing Industry

- 4.2.1 Bargaining Power of Raw Material Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Competition within the Garment Industry

- 4.2.4 Potential Entrants

- 4.2.5 Alternatives

5 Analysis on Cost and Price in Garment Manufacturing Industry in Thailand

- 5.1 Thailand Garment Manufacturing Cost Analysis 2018-2022

- 5.1.1 Cost of Raw Materials

- 5.1.2 Labor Cost Analysis of Thailand's Garment Manufacturing Industry

- 5.2 Thailand Clothing Price Analysis

6 Overview of Major Garment Manufacturing Companies in Thailand

- 6.1 Toray Industries (Thailand) Co. Ltd. Toray Group

- 6.1.1 Business Profile

- 6.1.2 Main Products

- 6.1.3 Modes of Operation

- 6.2 NaRaYa

- 6.2.1 Business Profile

- 6.2.2 Main Products

- 6.2.3 Modes of Operation

- 6.3 Jaspal

- 6.3.1 Business Profile

- 6.3.2 Main Products

- 6.3.3 Modes of Operation

- 6.4 Thai Wacoal

- 6.4.1 Business Profile

- 6.4.2 Main Products

- 6.4.3 Modes of Operation

- 6.5 Disaya

- 6.5.1 Business Profile

- 6.5.2 Main Products

- 6.5.3 Modes of Operation

7 Thailand Garment Manufacturing Outlook, 2023-2032

- 7.1 Factors Influencing the Development of Thailand's Garment Manufacturing Industry

- 7.1.1 Drivers and Market Opportunities in Thailand Garment Manufacturing Industry

- 7.1.2 Threats and Challenges Facing Thailand's Garment Manufacturing Industry

- 7.1.3 Industry Prospects and Market Opportunities

- 7.2 Competitive Landscape Forecast for Thailand Garment Manufacturing Industry

- 7.3 Supply Forecast of Garment Manufacturing in Thailand, 2023-2032

- 7.3.1 Thailand Garment Manufacturing Raw Material Import Forecast 2023-2032

- 7.3.2 Thailand's Garment Export Forecast 2023-2032

- 7.4 Thailand Garment Manufacturing Market Demand Forecast 2023-2032

- 7.4.1 Overall Market Demand Forecast for Garment Manufacturing in Thailand, 2023-2032

- 7.4.2 Demand Forecast for Thailand Garment Manufacturing Segment 2023-2032

List of Charts

- Chart Classification of Garment Manufacturing

- Chart Garment Manufacturing Industry Chain Analysis

- Chart Garment Manufacturing Raw Materials Source Analysis

- Chart Thailand's Textile and Garment Exports, 2018-2022

- Chart Product Sales Revenue of Textile Industry in Thailand 2018-2022

- Chart 2018-2022 Textile Fiber Production in Thailand

- Chart 2018-2022 Thailand Garment Manufacturing Apparent Consumption Analysis

- Chart Toray Industries (Thailand) Co. Ltd. Toray Group Basic Information

- Chart NaRaYa Basic Information

- Chart Jaspal Basic Information

- Chart Thai Wacoal Basic Information

- Chart Disaya Basic Information

- Chart 2023-2032 Thailand Cotton Import Forecasts

- Chart 2023-2032 Forecast of Thailand's Garment Exports