|

市场调查报告书

商品编码

1982366

功能性印刷市场:成长机会、成长要素、产业趋势分析及2026-2035年预测Functional Printing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

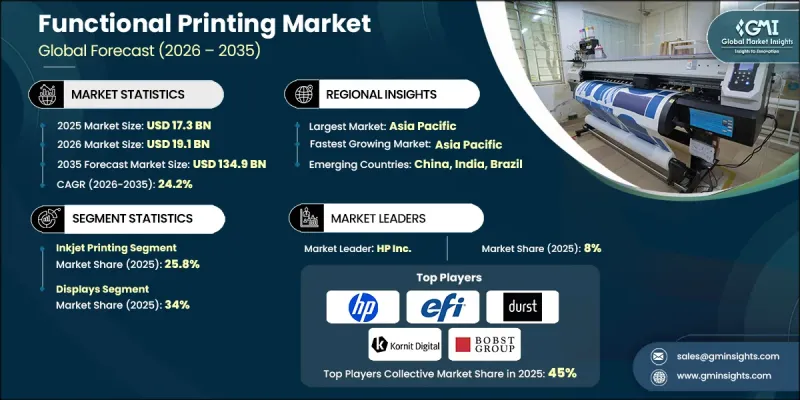

全球功能性印刷市场预计到 2025 年将达到 173 亿美元,预计到 2035 年将达到 1,349 亿美元,年复合成长率为 24.2%。

该市场的发展动力源于先进材料、导电油墨以及喷墨、丝网印刷和凹版印刷等新一代印刷技术的持续创新。功能性印刷因其高度客製化、减少废弃物和缩短产品开发週期等优势,在高价值应用中日益受到青睐。从光刻和标准PCB製造等传统减材製造方法朝向积层製造和数数位化生产的转变,代表着製造理念的重大模式转移。透过併购和技术合作实现的策略整合正在加速市场成长,使导电油墨、软式电路板和印刷感测器技术领域的主要企业能够建立整合解决方案。随着行业对柔软性、小批量生产和多品种生产的需求日益增长,功能性印刷正在成为电子、包装和智慧型装置等领域的关键驱动力。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 173亿美元 |

| 预测金额 | 1349亿美元 |

| 复合年增长率 | 24.2% |

喷墨列印领域占25.8%的市场份额,预计2025年市场规模将达44亿美元。喷墨列印之所以引领市场,是因为它能够灵活应用于印刷电子产品、高解析度功能层和智慧包装等领域。奈米导电油墨、软式电路板和低温烧结技术的快速创新正在推动市场成长。喷墨列印适用于按需生产和多品种小批量生产,使其成为电子、纺织品和先进包装应用的理想选择。

预计到2025年,显示器产业将占据34%的市场份额,这主要得益于软性显示器、OLED面板、触控介面和印刷背板的日益普及。卷轴式製造流程和透明导电材料的应用将进一步推动这一成长。包括喷墨、网版印刷和凹版印刷在内的功能性印刷技术,能够製造柔性且复杂的显示结构,从而促进便携式电子产品、能源解决方案和楼宇整合技术(BIT)等领域的应用。

到2025年,美国功能性印刷市占率将达到64.4%。印刷电子、软性显示器数位化包装的普及是推动市场成长的主要动力。电子商务、医疗保健和家用电子电器等行业对智慧标籤、印刷感测器、RFID追踪和增材电子的需求激增。除了采用结合柔版印刷和喷墨技术的混合印刷平台外,人工智慧驱动的印刷优化、在线连续检测和预测性维护等技术也提高了原始设备製造商 (OEM) 和加工商在工业应用领域的可靠性。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 劳动力短缺加剧和製造业回流

- 人工智慧、衍生设计和软体集成

- IT/OT在印刷作业中的集成

- 产业潜在风险与挑战

- 高阶整合的复杂性

- 资料隐私和网路安全

- 机会

- Printing-as-a-Service(PaaS)

- 印刷电子和智慧包装的成长

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 透过技术

- 监理情势

- 标准和合规要求

- 区域法律规范

- 认证标准

- 波特的分析

- PESTEL 分析

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依材料划分,2022-2035年

- 基板

- 玻璃

- 塑胶

- 纸

- 碳化硅

- 氮化镓

- 其他的

- 墨水

- 导电油墨

- 介电油墨

- 石墨烯墨水

- 其他的

第六章 市场估计与预测:依技术划分,2022-2035年

- 喷墨列印

- 网版印刷

- 柔版印刷

- 凹版印刷

- 其他的

第七章 市场估计与预测:依应用领域划分,2022-2035年

- 展示

- 感应器

- 太阳能

- 照明

- 电池

- RFID标籤

- 其他的

第八章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第九章:公司简介

- Bobst Group

- Comexi Group

- Domino

- Durst Group

- EFI

- HP Inc.

- Kornit Digital

- KYMC

- Mark Andy

- Mimaki Engineering

- PCMC

- Roland DG

- SPGPrints

- Thieme

- Uteco Converting

The Global Functional Printing Market was valued at USD 17.3 billion in 2025 and is estimated to grow at a CAGR of 24.2% to reach USD 134.9 billion by 2035.

The market is driven by continuous innovations in advanced materials, conductive inks, and next-generation printing technologies such as inkjet, screen, and gravure printing. Functional printing is increasingly preferred in high-value applications due to its ability to enable high customization, low waste, and faster product development cycles. The shift from traditional subtractive manufacturing methods, like lithography and standard PCB fabrication, toward additive and digitalized production represents a major paradigm shift in manufacturing philosophy. Strategic consolidations through mergers, acquisitions, and technology partnerships are accelerating market growth, allowing key players in conductive inks, flexible substrates, and printed sensor technologies to build integrated solutions. As industries increasingly demand flexible, low-volume, and high-mix production, functional printing is emerging as a critical enabler across sectors like electronics, packaging, and smart devices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $17.3 Billion |

| Forecast Value | $134.9 Billion |

| CAGR | 24.2% |

The inkjet printing segment held 25.8% share, valued at USD 4.4 billion in 2025. Inkjet dominates due to its adaptability for printed electronics, high-resolution functional layers, and smart packaging. Rapid innovations in nanoparticle conductive inks, flexible substrates, and low-temperature sintering are supporting growth. Its suitability for on-demand, high-mix, and low-volume production makes it ideal for electronics, textiles, and advanced packaging applications.

In 2025, the displays segment held a 34% share, driven by the increasing adoption of flexible displays, OLED panels, touch interfaces, and printed backplanes. Roll-to-roll manufacturing and the use of transparent conductive materials further support growth. Functional printing technologies, including inkjet, screen, and gravure, enable the production of flexible and complex display structures, serving applications in portable electronics, energy solutions, and building-integrated technologies.

U.S. Functional Printing Market held 64.4% share in 2025. Strong adoption of printed electronics, flexible displays, and digitized packaging fuels the market. Rapid growth in demand for smart labels, printed sensors, RFID tracking, and additive electronics is being driven by sectors such as e-commerce, healthcare, and consumer electronics. The use of hybrid printing platforms combining flexo and inkjet technologies, coupled with AI-driven print optimization, inline inspection, and predictive maintenance, strengthens reliability for OEMs and converters across industrial applications.

Key players in the Global Functional Printing Market include Bobst Group, Comexi Group, Domino, Durst Group, EFI, HP Inc., Kornit Digital, KYMC, Mark Andy, Mimaki Engineering, PCMC, Roland DG, SPGPrints, Thieme, and Uteco Converting. Companies in the Global Functional Printing Market are strengthening their position by investing heavily in R&D to develop high-precision, high-speed, and energy-efficient printing technologies. They focus on expanding their product portfolios with hybrid printing solutions and customizable applications to meet diverse industry needs. Strategic partnerships, joint ventures, and acquisitions help them integrate complementary technologies, enhance scale, and expand geographic reach. Companies also leverage AI, IoT, and predictive maintenance tools to improve reliability, minimize downtime, and optimize print quality. Expanding into emerging markets, targeting high-growth verticals like flexible electronics and smart packaging, and offering service and support solutions help players enhance customer loyalty and maintain a competitive advantage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Application

- 2.2.4 Technology

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Labor Shortages & Manufacturing Reshoring

- 3.2.1.2 AI, Generative Design & Software Integration

- 3.2.1.3 IT/OT Convergence in Printing Operations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High Integration Complexity

- 3.2.2.2 Data Privacy & Cybersecurity

- 3.2.3 Opportunities

- 3.2.3.1 Printing-as-a-Service (PaaS)

- 3.2.3.2 Growth in Printed Electronics & Smart Packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Technology

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Substrate

- 5.2.1 Glass

- 5.2.2 Plastic

- 5.2.3 Paper

- 5.2.4 Silicon Carbide

- 5.2.5 Gallium Nitride

- 5.2.6 Others

- 5.3 Inks

- 5.3.1 Conductive Inks

- 5.3.2 Dielectric Inks

- 5.3.3 Graphene Inks

- 5.3.4 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Inkjet Printing

- 6.3 Screen Printing

- 6.4 Flexographic Printing

- 6.5 Gravure Printing

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Displays

- 7.3 Sensors

- 7.4 Photovoltaics

- 7.5 Lighting

- 7.6 Batteries

- 7.7 RFID Tags

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bobst Group

- 9.2 Comexi Group

- 9.3 Domino

- 9.4 Durst Group

- 9.5 EFI

- 9.6 HP Inc.

- 9.7 Kornit Digital

- 9.8 KYMC

- 9.9 Mark Andy

- 9.10 Mimaki Engineering

- 9.11 PCMC

- 9.12 Roland DG

- 9.13 SPGPrints

- 9.14 Thieme

- 9.15 Uteco Converting