|

市场调查报告书

商品编码

1959624

军用帐篷及掩体市场机会、成长要素、产业趋势分析及预测(2026-2035年)Military Tent and Shelter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

2025 年全球军用帐篷和住所市场价值 10 亿美元,预计到 2035 年将达到 15 亿美元,年复合成长率为 4%。

市场成长的主要驱动力是全球国防预算增加导致军用掩体采购量上升。对远征任务快速部署解决方案的需求,以及模组化和智慧掩体技术的进步,进一步加速了其普及。此外,人们对可用于军事行动和紧急应变的掩体的兴趣日益浓厚,也扩大了市场范围。军方和政府部门越来越重视柔软性、节能且可快速部署的基础设施,以支援作战准备和人道主义任务。对军民两用场景的关注在2020年前后显着增强,并将持续影响2030年的筹资策略,因为军事和灾害应变机构正在整合物流计划,以提高作战韧性和危机应变能力。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 10亿美元 |

| 预测金额 | 15亿美元 |

| 复合年增长率 | 4% |

随着各国政府将预算分配给行动基础设施,以支持野战行动和灾害救援,不断增长的军事开支推动了对避难所的需求。模组化和智慧避难所设计技术的进步,为军事任务提供了节能高效且可快速部署的解决方案。同时,紧急应变和人道援助等双用途应用也拓展了市场潜力。货柜式和医疗避难所因其耐用性、适应性以及整合通讯系统、指挥中心和医疗基础设施的能力而备受关注。这些解决方案能够支援前沿部署行动、半永久性基地以及在偏远和衝突地区提供先进的医疗支持,从而提高任务效率和快速反应能力。

预计2026年至2035年间,货柜式掩体市场将以5.1%的复合年增长率成长。现代军事行动中对坚固耐用、防护性能卓越的基础设施的需求不断增长,推动了货柜式掩体的应用。货柜式掩体具有优异的隔热性和耐久性,并可整合指挥中心、医疗设施和通讯网路等系统。其对恶劣环境的适应性以及对半永久性和永久性用途的适用性,也支撑着市场的持续成长。

预计到2035年,医疗和野战医院领域将以5.3%的复合年增长率成长。对前沿部署医疗单元、灾害应变和军事医疗系统的投资增加是推动需求成长的主要因素。这些设施专为偏远和高风险地区的紧急治疗、隔离病房和手术室而设计。日益增长的人道主义援助和快速医疗响应需求正在加速这些解决方案的普及,这些解决方案提供技术先进的医疗基础设施,可快速部署用于军事和紧急用途。

预计到2025年,北美军用帐篷和掩体市场将占据39.9%的市场。该地区的成长主要得益于美加两国军方不断增加的国防预算以及对远征基础建设的日益重视。具备气候控制、电力供应和快速部署能力的模组化智慧掩体系统正在广泛应用。政府和国防相关企业持续投资研发用于军事行动和救援工作的下一代可部署掩体,不断推动技术进步。北美将持续引领创新,军事现代化计划、联合演习和作战需求将持续支撑市场成长至2035年。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段增加的价值

- 影响价值链的因素

- 中断

- 影响产业的因素

- 促进因素

- 由于全球国防预算增加,防空洞采购量也随之增加。

- 远征任务中对快速部署基础架构的需求

- 模组化智慧住所的技术进步

- 可用于军事和紧急用途的两用掩体

- 联合/盟军对互通性的需求

- 产业潜在风险与挑战

- 高昂的采购、维护和生命週期成本

- 偏远地区或恶劣环境下的复杂物流

- 市场机会

- 根据特定任务需求客製化模组化设计

- 将可再生能源系统整合到房屋中

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 定价策略

- 新兴经营模式

- 合规要求

- 专利和智慧财产权分析

- 地缘政治和贸易趋势

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 市场集中度分析

- 按地区

- 主要企业的竞争标竿分析

- 财务绩效比较

- 收入

- 利润率

- 研究与开发

- 产品系列比较

- 产品线的广度

- 科技

- 创新

- 地理位置比较

- 全球扩张分析

- 服务网路覆盖

- 按地区分類的市场渗透率

- 竞争定位矩阵

- 领导企业

- 挑战者

- 追踪者

- 小众玩家

- 战略展望矩阵

- 财务绩效比较

- 主要进展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/Start-Ups竞争对手的发展趋势

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 军用帐篷

- 部队住宿帐篷

- 轻型战斗帐篷

- 快速展开式充气帐篷

- 软墙模组化庇护所

- 框架支撑式织物庇护所

- 可扩充软墙系统

- 硬墙可部署式掩体

- 硬质板避难所

- 隔热硬墙避难所

- 货柜式避难所

- ISO货柜式遮篷(20英尺/40英尺)

- 可扩展货柜式避难所

- 车载式及拖车式遮蔽棚

- 移动指挥所

- 可移动任务庇护所

第六章 市场估算与预测:依部署类型划分,2022-2035年

- 快速部署

- 半永久性

- 便携式/可携式

第七章 市场估计与预测:依保护等级划分,2022-2035年

- 非保护性(仅限环境保护)

- 防弹

- 抗爆性

- 核生化防护

- 电磁脉衝/电磁干扰屏蔽

- 特征缩减

第八章 市场估算与预测:依材料类型划分,2022-2035年

- 织物底材

- 金属框架

- 复合材料基体

- 混合结构

第九章 市场估价与预测:依行动平台划分,2022-2035年

- 地面部署类型(可人工运输或飞机运输)

- 车上型

- 拖车式

- 容器化

第十章 市场估价与预测:依应用领域划分,2022-2035年

- 部队营房/基地营地

- 指挥与控制(C2)操作

- 医疗与野战医院

- 维护、维修和支援服务

- 通信、雷达和监视

- 弹药和装备储存

- 训练和模拟支持

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 主要企业

- HDT Global

- General Dynamics Mission Systems

- HTS TENTIQ GmbH

- Losberger De Boer

- AAR Mobility Systems

- 按地区分類的主要企业

- 北美洲

- UTS Systems LLC

- ADS Inc.(Advanced Deployable Systems)

- Celina Military Shelters(Celina Tent, Inc.)

- Outdoor Venture Corp

- 欧洲

- M. Schall

- Rekord Structures Company(RDS)

- Veldeman

- Tentora/New Tents Manufacturing

- 北美洲

- 特殊玩家/干扰者

- Weatherhaven

- Shelter Structures

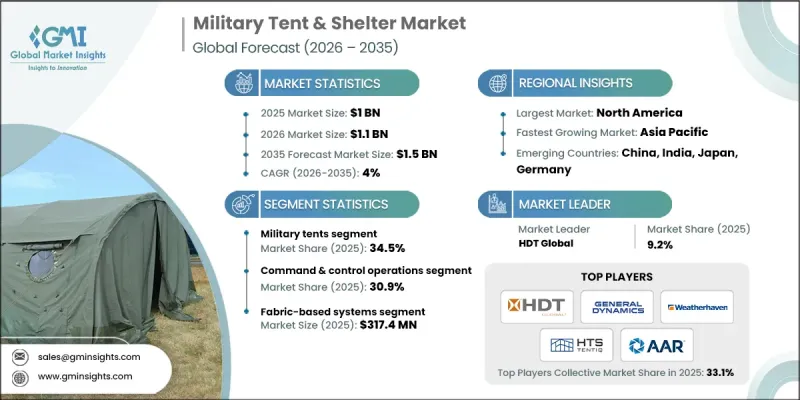

The Global Military Tent & Shelter Market was valued at USD 1 billion in 2025 and is estimated to grow at a CAGR of 4% to reach USD 1.5 billion in 2035.

Market growth is driven by rising global defense budgets, which are increasing the procurement of military shelters. The demand for rapidly deployable solutions for expeditionary missions and technological advances in modular and smart shelters is further accelerating adoption. Additionally, there is growing interest in shelters that serve dual purposes for military operations and emergency response, broadening the market scope. Military forces and governments are increasingly prioritizing flexible, energy-efficient, and quick-deployment infrastructure to support operational readiness and humanitarian missions. The focus on dual-use scenarios emerged strongly around 2020 and continues to shape procurement strategies through 2030, as military and disaster-response agencies integrate logistics planning to improve operational resilience and crisis response capabilities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1 Billion |

| Forecast Value | $1.5 Billion |

| CAGR | 4% |

Military expenditure growth is fueling the demand for shelters, as governments allocate budgets to mobile infrastructure to support field operations and disaster relief. Advances in modular and smart shelter designs are enabling energy-efficient, rapid-deployment solutions for military missions, while dual-use applications for emergency response and humanitarian aid are expanding market potential. Containerized and medical shelters are gaining traction for their durability, adaptability, and ability to integrate systems such as communications, command centers, and healthcare infrastructure. These solutions allow for forward-deployed operations, semi-permanent bases, and advanced medical support in remote or conflict-affected areas, enhancing mission effectiveness and rapid-response capabilities.

The containerized shelters segment is expected to grow at a CAGR of 5.1% during 2026-2035. The increasing need for robust, long-lasting, and protective infrastructure for modern military operations is driving adoption. Containerized shelters offer superior insulation, durability, and the ability to integrate systems such as command centers, medical facilities, and communication networks. Their adaptability to harsh environments and suitability for semi-permanent and permanent use are supporting sustained market growth.

The medical and field hospital shelters segment is projected to grow at a CAGR of 5.3% through 2035. Rising investments in forward-deployed medical units, disaster response, and military healthcare readiness are fueling demand. These shelters are designed for emergency treatment, isolation wards, and surgical units in remote or high-risk locations. Humanitarian missions and rapid-response healthcare requirements are accelerating adoption, as these solutions provide quickly deployable and technologically advanced medical infrastructure for military and emergency use.

North America Military Tent & Shelter Market held a 39.9% share in 2025. Growth in the region is driven by rising defense budgets and the U.S. and Canadian militaries' emphasis on expeditionary infrastructure development. Modular and smart shelter systems offering climate control, power, and rapid-deployment capabilities are gaining traction. Investments by governments and defense contractors in next-generation deployable shelters for both military and relief operations continue to drive technological advancement. North America remains at the forefront of innovation, with military modernization projects, joint exercises, and operational needs sustaining market growth through 2035.

Key companies operating in the Global Military Tent & Shelter Market include HDT Global, Shelter Structures, Celina Military Shelters (Celina Tent, Inc.), Rekord Structures Company (RDS), UTS Systems LLC, AAR Mobility Systems, ADS Inc. (Advanced Deployable Systems), Losberger De Boer, Tentora / New Tents Manufacturing, ZTS TENTIQ GmbH, Weatherhaven, Outdoor Venture Corp, M. Schall, Veldeman, and other prominent players. Companies in the Military Tent & Shelter Market are strengthening their foothold through innovation, product diversification, and strategic collaborations. They are developing modular, smart, and energy-efficient shelters that cater to both military and dual-use applications. Partnerships with governments and defense contractors ensure early adoption and long-term contracts. Investments in rapid-deployment technologies, climate-controlled solutions, and integrated communication systems enhance operational relevance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Deployment type trends

- 2.2.3 Protection level trends

- 2.2.4 Material type trends

- 2.2.5 Mobility platform trends

- 2.2.6 Application trends

- 2.2.7 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global defense budgets increasing shelter procurements

- 3.2.1.2 Need for rapid deployment infrastructure in expeditionary missions

- 3.2.1.3 Technological advancements in modular and smart shelters

- 3.2.1.4 Dual-use shelters for military and emergency applications

- 3.2.1.5 Interoperability demand from joint/coalition military forces

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High procurement, maintenance and lifecycle costs

- 3.2.2.2 Complex logistics in remote or harsh environments

- 3.2.3 Market opportunities

- 3.2.3.1 Custom modular designs for mission-specific needs

- 3.2.3.2 Integration of renewable energy systems into shelters

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Military tents

- 5.2.1 Troop accommodation tents

- 5.2.2 Lightweight combat tents

- 5.2.3 Rapid-deployment & inflatable tents

- 5.3 Soft-wall modular shelters

- 5.3.1 Frame-supported fabric shelters

- 5.3.2 Expandable soft-wall systems

- 5.4 Hard-wall deployable shelters

- 5.4.1 Rigid panel shelters

- 5.4.2 Insulated hard-wall shelters

- 5.5 Containerized shelters

- 5.5.1 ISO container shelters (20-ft / 40-ft)

- 5.5.2 Expandable containerized shelters

- 5.6 Vehicle-mounted & trailer-mounted shelters

- 5.6.1 Mobile command shelters

- 5.6.2 Transportable mission shelters

Chapter 6 Market Estimates and Forecast, By Deployment Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Rapid-deployment

- 6.3 Semi-permanent

- 6.4 Relocatable / mobile

Chapter 7 Market Estimates and Forecast, By Protection Level, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Non-protected (environmental protection only)

- 7.3 Ballistic-resistant

- 7.4 Blast-resistant

- 7.5 CBRN / NBC-protected

- 7.6 EMP / EMI-shielded

- 7.7 Signature-Reduction

Chapter 8 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Fabric-based

- 8.3 Metal-frame

- 8.4 Composite-based

- 8.5 Hybrid construction

Chapter 9 Market Estimates and Forecast, By Mobility Platform, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Ground-deployable (man-portable / air-portable)

- 9.3 Vehicle-mounted

- 9.4 Trailer-mounted

- 9.5 Container-transportable

Chapter 10 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 10.1 Troop accommodation & base camps

- 10.2 Command & control (C2) operations

- 10.3 Medical & field hospitals

- 10.4 Maintenance, repair & logistics

- 10.5 Communication, radar & surveillance

- 10.6 Ammunition & equipment storage

- 10.7 Training & simulation support

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 HDT Global

- 12.1.2 General Dynamics Mission Systems

- 12.1.3 HTS TENTIQ GmbH

- 12.1.4 Losberger De Boer

- 12.1.5 AAR Mobility Systems

- 12.2 Regional key players

- 12.2.1 North America

- 12.2.1.1 UTS Systems LLC

- 12.2.1.2 ADS Inc. (Advanced Deployable Systems)

- 12.2.1.3 Celina Military Shelters (Celina Tent, Inc.)

- 12.2.1.4 Outdoor Venture Corp

- 12.2.2 Europe

- 12.2.2.1 M. Schall

- 12.2.2.2 Rekord Structures Company (RDS)

- 12.2.2.3 Veldeman

- 12.2.2.4 Tentora / New Tents Manufacturing

- 12.2.1 North America

- 12.3 Niche Players/Disruptors

- 12.3.1 Weatherhaven

- 12.3.2 Shelter Structures