|

市场调查报告书

商品编码

1822613

听力学设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Audiology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

根据 Global Market Insights Inc. 发布的最新报告,全球听力设备市场规模在 2024 年估计为 116 亿美元,预计将从 2025 年的 121 亿美元增长到 2034 年的 207 亿美元,复合年增长率为 6.1%。

全球听力损失发生率的不断上升是听力设备市场的主要驱动力。随着预期寿命的延长和全球人口老化的加剧,与年龄相关的听力障碍(也称为老年性耳聋)也变得越来越普遍。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 116亿美元 |

| 预测值 | 207亿美元 |

| 复合年增长率 | 6.1% |

助听器需求不断成长

2024年,助听器市场占据了显着份额,这得益于持续的技术创新以及对低调、用户友好型产品日益增长的需求。现代助听器如今拥有蓝牙连接、基于人工智慧的声音增强、降噪和可充电电池等先进功能。这些功能吸引了那些追求与数位生活方式无缝融合的科技消费者。

成年人获得关注

由于与年龄相关的听力损失盛行率高,2024年成人听力市场收入可观。随着越来越多的成年人寻求支持积极生活方式的解决方案,对高性能、低维护、音质自然、电池续航时间长的设备的需求日益增长。成年人也更有可能定期进行听力评估,从而提高诊断和治疗率。製造商正瞄准这一人群,并专注于独立性、沟通能力和生活品质。

神经性听力损失盛行率不断上升

2024年,感音神经性听损细分市场实现了永续的收入。这种疾病通常由内耳或听觉神经损伤引起,往往不可逆,需要长期的设备支持。助听器和人工耳蜗是主要的解决方案,其设备性能可根据不同严重程度进行客製化。各公司正在大力投入研发,以生产能够更好地模拟自然听觉并适应复杂声音环境的设备。语音辨识和即时声音处理的创新正在帮助使用者在嘈杂的环境中体验到更清晰、更舒适的聆听体验。

区域洞察

北美将成为推动力地区

2024年,北美听力设备市场占据了相当大的份额,这得益于其先进的医疗基础设施、优惠的报销政策以及浓厚的早期听力损失诊断文化。美国在该区域市场占据主导地位,其市场规模超过30亿美元,由于人口老化和消费者意识的提升,市场规模每年都在稳步增长。各大公司正在透过扩展听力诊所网路、增强线上零售平台以及将远距医疗解决方案融入听力保健领域来巩固其在北美的地位。

听力学设备市场的主要参与者有 EARGO、Demant、NUROTRON、ENVOY MEDICAL、WS Audiology、Medtronic、GN Store Nord、MAICO、RION、EARTECHNIC、MED-EL Medical、Starkey、Cochlear、American Diagnostic Corporation 和 Sonova。

为了巩固其地位,听力设备市场的领先公司正在采取多管齐下的策略。创新仍然是核心,并持续投资于微型化、基于人工智慧的音讯处理和无线连接,以满足不断变化的用户期望。许多公司正在与远距医疗服务提供者和零售连锁药局建立策略联盟,以扩大其分销网络。此外,他们透过个人化验配技术、用于装置控制的行动应用程式以及终身服务计划,将客户体验放在首位。

目录

第一章:方法论与范围

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球听力损失盛行率不断上升

- 对电子商务通路的偏好日益增长

- 听力学设备的技术进步

- 已开发国家优惠的报销政策

- 产业陷阱与挑战

- 先进听力设备成本高昂

- 低收入国家缺乏认识

- 市场机会

- 人工智慧和机器学习在助听设备中的集成

- 对远距听力学和远距听力服务的需求不断增长

- 成长动力

- 成长潜力分析

- 监管格局

- 我们

- 欧洲

- 技术格局

- 报销场景

- 按地区进行定价分析

- 消费者途径

- 传统途径

- 需要新的途径

- 混合途径

- 消费者洞察

- 政策格局

- 差距分析

- 风险管理分析

- 研究与开发

- 营运

- 行销和销售

- 品质

- 智慧财产

- 监管

- 资讯科技

- 气候

- 金融的

- 波特的分析

- PESTEL分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 按地区

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 助听器

- 按类型

- 耳背式(BTE)

- 耳内接收器/耳道接收器(RITE/RIC)

- 完全耳道式/隐形耳道式(CIC/IIC)

- 耳内式 (ITE)

- 耳道内(ITC)

- 按配销通路

- 实体店面

- 电子商务

- 按类型

- 人工耳蜗

- 单侧植入物

- 双侧植入物

- 诊断设备

- 鼓室压力计

- 听力计

- 耳镜

- 骨锚式助听器(BAHA)

- 中耳植入物(MEI)

第六章:市场估计与预测:按患者,2021 - 2034 年

- 主要趋势

- 成人

- 儿科

第七章:市场估计与预测:按听力损失,2021 - 2034 年

- 主要趋势

- 感音神经性听损

- 传导性听力损失

- 混合性听力损失

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- American Diagnostic Corporation

- Cochlear

- Demant

- EARGO

- EARTECHNIC

- ENVOY MEDICAL

- GN Store Nord

- MAICO

- MED-EL Medical

- Medtronic

- NUROTRON

- RION

- sonova

- Starkey

- WS Audiology

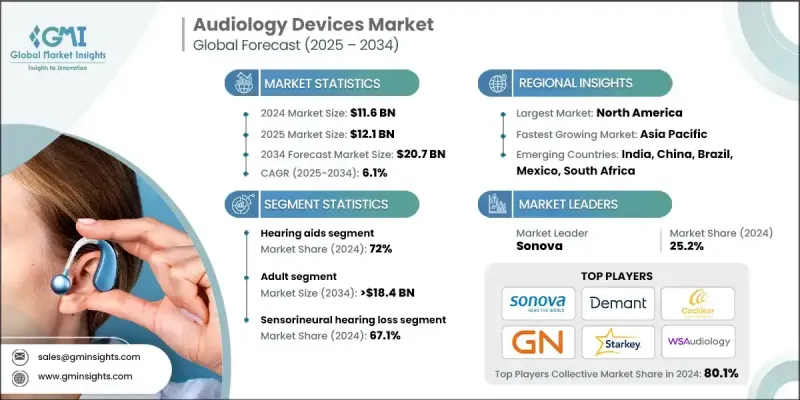

The global audiology devices market was estimated at USD 11.6 billion in 2024 and is expected to grow from USD 12.1 billion in 2025 to USD 20.7 billion by 2034, at a CAGR of 6.1%, according to the latest report published by Global Market Insights Inc.

The growing incidence of hearing loss worldwide is a primary driver of the audiology devices market. Age-related hearing impairment, also known as presbycusis, is becoming increasingly common as life expectancy rises and the global population continues to age.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.6 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 6.1% |

Rising Demand for Hearing Aids

The hearing aids segment held a notable share in 2024, driven by continuous technological innovation and rising demand for discreet, user-friendly products. Modern hearing aids now feature advanced functionalities such as Bluetooth connectivity, AI-based sound enhancement, noise cancellation, and rechargeable batteries. These features appeal to tech-savvy consumers looking for seamless integration with digital lifestyles.

Adults to Gain Traction

The adult segment generated significant revenues in 2024, owing to the high prevalence of age-related hearing loss. As more adults seek solutions that support active lifestyles, there is a growing demand for high-performance, low-maintenance devices that offer natural sound quality and long battery life. Adults are also more likely to engage in regular hearing assessments, leading to higher diagnosis and treatment rates. Manufacturers are targeting this demographic with marketing that emphasizes independence, communication, and quality of life.

Increasing Prevalence of Sensorineural Hearing Loss

The sensorineural hearing loss segment generated sustainable revenues in 2024. This condition, typically caused by damage to the inner ear or auditory nerve, is often irreversible and requires long-term device support. Hearing aids and cochlear implants are the primary solutions, with device performance tailored to different degrees of severity. Companies are investing heavily in research and development to produce devices that better mimic natural hearing and adapt to complex sound environments. Innovations in speech recognition and real-time sound processing are helping users experience improved clarity and comfort in noisy settings.

Regional Insights

North America to Emerge as a Propelling Region

North America audiology devices market held a sizeable share in 2024, driven by advanced healthcare infrastructure, favorable reimbursement policies, and a strong culture of early hearing loss diagnosis. The United States dominates the regional market, with a value exceeding USD 3 billion and steady annual growth fueled by the aging population and rising consumer awareness. Companies are strengthening their position in North America by expanding audiology clinic networks, enhancing online retail platforms, and integrating telehealth solutions into the hearing care journey.

Major players in the audiology devices market are EARGO, Demant, NUROTRON, ENVOY MEDICAL, WS Audiology, Medtronic, GN Store Nord, MAICO, RION, EARTECHNIC, MED-EL Medical, Starkey, Cochlear, American Diagnostic Corporation, and Sonova.

To solidify their presence, leading companies in the audiology devices market are adopting a multi-pronged approach. Innovation remains central, with ongoing investments in miniaturization, AI-based audio processing, and wireless connectivity to meet evolving user expectations. Many companies are entering strategic alliances with telehealth providers and retail pharmacy chains to broaden their distribution footprint. Additionally, customer experience is prioritized through personalized fitting technology, mobile apps for device control, and lifetime service plans.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Patient trends

- 2.2.4 Hearing loss trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of hearing loss globally

- 3.2.1.2 Growing preference for e-commerce channels

- 3.2.1.3 Technological advancements in audiology devices

- 3.2.1.4 Favorable reimbursement policies in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced audiology devices

- 3.2.2.2 Lack of awareness in low-income countries

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and machine learning in hearing devices

- 3.2.3.2 Growing demand for tele-audiology and remote hearing services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis, by region

- 3.8 Consumer pathway

- 3.8.1 Conventional pathway

- 3.8.2 Need for new pathway

- 3.8.3 Hybrid pathway

- 3.9 Consumer insights

- 3.10 Policy landscape

- 3.11 Gap analysis

- 3.12 Risk management analysis

- 3.12.1 Research and development

- 3.12.2 Operations

- 3.12.3 Marketing and sales

- 3.12.4 Quality

- 3.12.5 Intellectual property rights

- 3.12.6 Regulatory

- 3.12.7 Information technology

- 3.12.8 Climate

- 3.12.9 Financial

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Future market trends

- 3.16 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Latin America

- 4.3.1.5 MEA

- 4.3.1 By region

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Hearing aids

- 5.2.1 By Type

- 5.2.1.1 Behind-the-ear (BTE)

- 5.2.1.2 Receiver in the ear/receiver in canal (RITE/RIC)

- 5.2.1.3 Completely-in-the-canal/invisible-in-canal (CIC/IIC)

- 5.2.1.4 In-the-ear (ITE)

- 5.2.1.5 In-the-canal (ITC)

- 5.2.2 By Distribution Channel

- 5.2.2.1 Brick and mortar

- 5.2.2.2 E-commerce

- 5.2.1 By Type

- 5.3 Cochlear implants

- 5.3.1 Unilateral implants

- 5.3.2 Bilateral implants

- 5.4 Diagnostic devices

- 5.4.1 Tympanometers

- 5.4.2 Audiometer

- 5.4.3 Otoscopes

- 5.5 Bone-anchored hearing aids (BAHA)

- 5.6 Middle ear implants (MEI)

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Hearing Loss, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Sensorineural hearing loss

- 7.3 Conductive hearing loss

- 7.4 Mixed hearing loss

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 American Diagnostic Corporation

- 9.2 Cochlear

- 9.3 Demant

- 9.4 EARGO

- 9.5 EARTECHNIC

- 9.6 ENVOY MEDICAL

- 9.7 GN Store Nord

- 9.8 MAICO

- 9.9 MED-EL Medical

- 9.10 Medtronic

- 9.11 NUROTRON

- 9.12 RION

- 9.13 sonova

- 9.14 Starkey

- 9.15 WS Audiology

2026年全球助听设备市场报告2026年全球听力服务市场报告

2026年全球助听设备市场报告2026年全球听力服务市场报告 听力测试间市场按类型、技术、应用、最终用户和分销管道划分-全球预测(2026-2032 年)

听力测试间市场按类型、技术、应用、最终用户和分销管道划分-全球预测(2026-2032 年) 助听器市场规模、份额和成长分析(按技术、年龄层、产品、听力损失类型、销售管道和地区划分)-2026-2033年产业预测助听器市场按产品类型、分销管道、最终用户、技术类型、电池类型和年龄组别划分-2025-2032年全球预测

助听器市场规模、份额和成长分析(按技术、年龄层、产品、听力损失类型、销售管道和地区划分)-2026-2033年产业预测助听器市场按产品类型、分销管道、最终用户、技术类型、电池类型和年龄组别划分-2025-2032年全球预测 听力学设备市场-全球产业规模、份额、趋势、机会和预测(按技术、产品、销售通路、地区和竞争细分,2020-2030 年)

听力学设备市场-全球产业规模、份额、趋势、机会和预测(按技术、产品、销售通路、地区和竞争细分,2020-2030 年) 听力测试设备市场规模、份额、趋势分析报告:按技术、年龄层、产品、销售管道、细分预测,2025-2030 年

听力测试设备市场规模、份额、趋势分析报告:按技术、年龄层、产品、销售管道、细分预测,2025-2030 年 听觉设备:市场洞察·竞争环境·市场预测 (~2030年)

听觉设备:市场洞察·竞争环境·市场预测 (~2030年) 全球助听器市场,2024-2028

全球助听器市场,2024-2028 诊断助听器的全球市场

诊断助听器的全球市场