|

市场调查报告书

商品编码

1822602

自我血糖监测设备市场机会、成长动力、产业趋势分析及2025-2034年预测Self-Monitoring Blood Glucose Monitoring Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

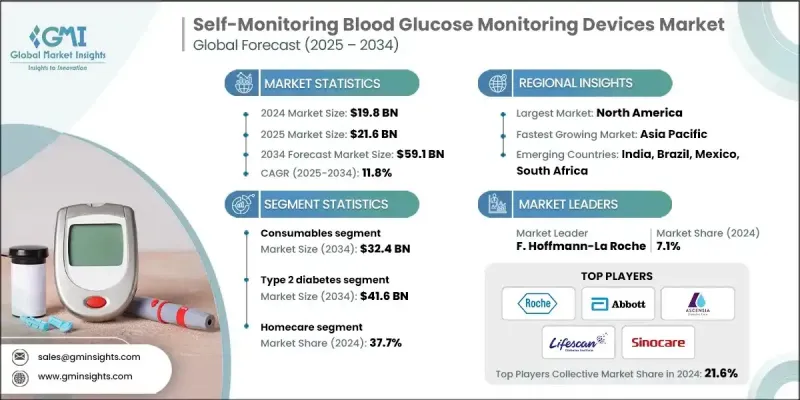

根据 Global Market Insights Inc. 发布的最新报告,全球自我监测血糖监测设备市场规模在 2024 年估计为 198 亿美元,预计将从 2025 年的 216 亿美元增长到 2034 年的 591 亿美元,复合年增长率为 11.8%。

全球1型和第2型糖尿病病例激增,尤其是在新兴市场,这推动了对便利可靠的SMBG设备的需求,这些设备可用于日常血糖监测。久坐的生活方式、不健康的饮食以及不断上升的肥胖率导致糖尿病发病率上升,越来越多的人被诊断出糖尿病,并且患病年龄越来越小,人群分布也越来越广泛。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 198亿美元 |

| 预测值 | 591亿美元 |

| 复合年增长率 | 11.8% |

消耗品需求不断成长

2024年,耗材市场在试纸、采血针和质控液的推动下占据了显着份额。由于这些产品是日常监测的必需品,其需求持续高企,推动了市场稳定成长。由于试纸更换週期频繁,其在耗材销售中占据主导地位。随着消费者追求更准确、更便利的检测,各公司不断创新,生产出只需少量血液样本即可快速获得结果的试纸。耗材市场的扩张对于维持患者依从性至关重要,并且持续吸引旨在确保长期客户忠诚度的行业参与者的大量投资。

2型糖尿病盛行率上升

2024年,第2型糖尿病细分市场收入可观,这反映了全球生活型态相关糖尿病病例的上升。 2型糖尿病患者通常需要定期监测血糖,以便在饮食和药物治疗的同时有效管理病情。随着人们对疾病管理的认识不断提高,以及医疗保健提供者强调血糖控制在预防併发症方面的重要性,这个细分市场正在快速成长。 SMBG设备价格实惠且易于使用,使其成为第2型糖尿病患者不可或缺的工具。

家庭护理将获得青睐

受以患者为中心和远距医疗管理趋势的推动,家庭护理领域在2024年占据了显着份额。越来越多的人选择在家中舒适地监测血糖水平,这得益于便利性、隐私性以及远距医疗服务的不断扩展。该领域受益于技术进步,包括相容于智慧型手机的设备和能够与医疗专业人员即时共享资料的数位健康平台。家庭护理的普及也与临床环境之外对慢性病管理的日益重视相契合。

区域洞察

北美将成为利润丰厚的地区

2024年,北美自我血糖监测设备市场占据了显着份额。强大的医疗基础设施、高糖尿病盛行率以及广泛的保险覆盖,共同推动了此类设备的强劲需求。该地区消费者註重准确性、便利性以及与数位健康生态系统的融合,这推动了製造商的快速创新。此外,主要行业参与者的参与和完善的监管环境确保了产品的高品质标准和可靠性。

自我监测血糖监测设备市场的主要参与者有 All Medicus、DarioHealth、B. Braun Melsungen、Ypsomed Holding、Sanofi、Bionime Corporation、AgaMatrix、Nova Biomedical、LifeScan、Arkray、Omnis Health、Sinocare、Abbott Laboratories、F. Hoffmann-Laabetes 和 Ascens。

为了巩固市场地位,自我血糖监测设备市场的公司正大力关注创新、合作伙伴关係和患者参与。产品开发注重准确性、易用性和连接性,许多製造商推出了支援应用程式的血糖仪,可与更广泛的数位健康平台整合。与医疗保健提供者和保险公司的策略合作,正在透过报销计划和捆绑式医疗方案扩大设备的可及性。公司也正在投资教育项目,以提高患者的认知度和依从性,尤其是在新兴市场。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 全球糖尿病盛行率不断上升

- 政府采取措施提高民众意识

- 已开发国家自我监测血糖监测设备的技术进步

- 产业陷阱与挑战

- 发展中国家先进设备和配件成本高昂

- 严格的监管要求

- 市场机会

- 新兴市场的扩张

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 技术进步

- 当前的技术趋势

- 新兴技术

- 供应链和分销分析

- 报销场景

- 2024年定价分析

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略仪表板

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 自我监测血糖仪

- 耗材

- 测试条

- 刺血针

第六章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 1型糖尿病

- 2型糖尿病

- 妊娠糖尿病

第七章:市场估计与预测:依最终用途,2021 - 2034

- 主要趋势

- 医院

- 门诊手术中心

- 诊断中心

- 居家护理

- 其他最终用途

第八章:市场估计与预测:按国家/地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 荷兰

- 瑞典

- 比利时

- 丹麦

- 芬兰

- 挪威

- 立陶宛

- 拉脱维亚

- 爱沙尼亚

- 俄罗斯

- 波兰

- 瑞士

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 台湾

- 印尼

- 越南

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 智利

- 秘鲁

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

- 埃及

- 以色列

- 科威特

- 卡达

第九章:公司简介

- Abbott Laboratories

- AgaMatrix

- All Medicus

- Arkray

- Ascensia Diabetes Care Holdings

- B. Braun Melsungen

- Bionime Corporation

- DarioHealth

- F. Hoffmann-La Roche

- LifeScan

- Nova Biomedical

- Omnis Health

- Sanofi

- Sinocare

- Ypsomed Holding

The global self-monitoring blood glucose monitoring devices market was estimated at USD 19.8 billion in 2024 and is expected to grow from USD 21.6 billion in 2025 to USD 59.1 billion in 2034, at a CAGR of 11.8%, according to the latest report published by Global Market Insights Inc.

The global surge in type 1 and type 2 diabetes cases, particularly in emerging markets, is driving demand for convenient and reliable SMBG devices for daily glucose tracking. As sedentary lifestyles, unhealthy diets, and rising obesity rates contribute to a higher incidence of diabetes, more individuals are being diagnosed at younger ages and across wider demographics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.8 Billion |

| Forecast Value | $59.1 Billion |

| CAGR | 11.8% |

Rising Demand for Consumables

The consumables segment held a notable share in 2024, driven by test strips, lancets, and control solutions. As these items are essential for daily monitoring, their demand remains consistently high, driving steady market growth. Test strips dominate consumables sales due to their frequent replacement cycles. As consumers seek more accurate and convenient testing, companies are innovating to produce strips that require smaller blood samples and deliver faster results. The consumables segment's expansion is critical for maintaining patient adherence, and it continues to attract substantial investment from industry players aiming to secure long-term customer loyalty.

Rising Prevalence of Type 2 Diabetes

The type 2 diabetes segment generated significant revenues in 2024, reflecting the global rise in lifestyle-related diabetes cases. Patients with type 2 diabetes often require regular glucose monitoring to manage their condition effectively alongside diet and medication. This segment is growing rapidly as awareness about disease management improves and healthcare providers emphasize the importance of glycemic control in preventing complications. The affordability and ease of use of SMBG devices for type 2 diabetes patients make them indispensable tools.

Homecare to Gain Traction

The homecare segment held a significant share in 2024, driven by the trend toward patient-centered and remote healthcare management. More individuals prefer monitoring their blood glucose levels from the comfort of their homes, motivated by convenience, privacy, and the ongoing expansion of telehealth services. This segment benefits from technological advancements, including smartphone-compatible devices and digital health platforms that enable real-time data sharing with healthcare professionals. Homecare adoption also aligns with the increasing emphasis on chronic disease management outside clinical settings.

Regional Insights

North America to Emerge as a Lucrative Region

North America self-monitoring blood glucose monitoring devices market generated a notable share in 2024. Strong healthcare infrastructure, high diabetes prevalence, and widespread insurance coverage contribute to robust demand for these devices. Consumers in this region prioritize accuracy, convenience, and integration with digital health ecosystems, which has pushed manufacturers to innovate rapidly. Additionally, the presence of major industry players and a well-established regulatory environment ensures high-quality standards and product reliability.

Major players in the self-monitoring blood glucose monitoring devices market are All Medicus, DarioHealth, B. Braun Melsungen, Ypsomed Holding, Sanofi, Bionime Corporation, AgaMatrix, Nova Biomedical, LifeScan, Arkray, Omnis Health, Sinocare, Abbott Laboratories, F. Hoffmann-La Roche, and Ascensia Diabetes Care Holdings.

To strengthen their market foothold, companies in the self-monitoring blood glucose monitoring devices market are focusing heavily on innovation, partnerships, and patient engagement. Product development emphasizes accuracy, ease of use, and connectivity, with many manufacturers launching app-enabled meters that integrate with broader digital health platforms. Strategic collaborations with healthcare providers and insurance companies are expanding device accessibility through reimbursement schemes and bundled care programs. Companies are also investing in educational initiatives to improve patient literacy and adherence, especially in emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of diabetes worldwide

- 3.2.1.2 Government initiatives for increasing awareness among people

- 3.2.1.3 Technological advancements of self-monitoring blood glucose monitoring devices in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced devices and accessories in developing countries

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain and distribution analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Self-monitoring blood glucose meters

- 5.3 Consumables

- 5.3.1 Testing strips

- 5.3.2 Lancets

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Type 1 diabetes

- 6.3 Type 2 diabetes

- 6.4 Gestational diabetes

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital

- 7.3 Ambulatory surgical centers

- 7.4 Diagnostic centers

- 7.5 Homecare

- 7.6 Other end use

Chapter 8 Market Estimates and Forecast, By Country, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 UK

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.3.7 Sweden

- 8.3.8 Belgium

- 8.3.9 Denmark

- 8.3.10 Finland

- 8.3.11 Norway

- 8.3.12 Lithuania

- 8.3.13 Latvia

- 8.3.14 Estonia

- 8.3.15 Russia

- 8.3.16 Poland

- 8.3.17 Switzerland

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Taiwan

- 8.4.7 Indonesia

- 8.4.8 Vietnam

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Colombia

- 8.5.5 Chile

- 8.5.6 Peru

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Turkey

- 8.6.5 Egypt

- 8.6.6 Israel

- 8.6.7 Kuwait

- 8.6.8 Qatar

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AgaMatrix

- 9.3 All Medicus

- 9.4 Arkray

- 9.5 Ascensia Diabetes Care Holdings

- 9.6 B. Braun Melsungen

- 9.7 Bionime Corporation

- 9.8 DarioHealth

- 9.9 F. Hoffmann-La Roche

- 9.10 LifeScan

- 9.11 Nova Biomedical

- 9.12 Omnis Health

- 9.13 Sanofi

- 9.14 Sinocare

- 9.15 Ypsomed Holding

2026年全球血糖值自我监测(SMBG)设备市场报告

2026年全球血糖值自我监测(SMBG)设备市场报告 日本血糖自我监测设备市场报告(按组件(血糖仪、试纸、采血针)和地区划分,2026-2034 年)

日本血糖自我监测设备市场报告(按组件(血糖仪、试纸、采血针)和地区划分,2026-2034 年) 自我监测血糖市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、最终用户、地区和竞争细分,2020-2030 年)

自我监测血糖市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、最终用户、地区和竞争细分,2020-2030 年) 自我监测血糖设备市场(按产品类型、按技术、按检测地点、按患者类型、按最终用户、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

自我监测血糖设备市场(按产品类型、按技术、按检测地点、按患者类型、按最终用户、按国家和地区)-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 自我血糖监测设备 (SMBG) 的全球市场 - 2024 年至 2029 年预测血糖自我监测 (SMBG) 设备的全球市场:到 2033 年的机会和策略

自我血糖监测设备 (SMBG) 的全球市场 - 2024 年至 2029 年预测血糖自我监测 (SMBG) 设备的全球市场:到 2033 年的机会和策略