|

市场调查报告书

商品编码

1699381

高频高速覆铜板(CCL)市场机会、成长动力、产业趋势分析及2025-2034年预测High Frequency High Speed Copper Clad Laminate (CCL) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

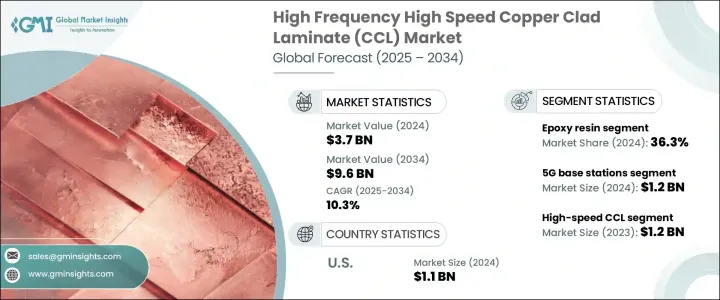

2024 年全球高频高速覆铜板市场规模达 37 亿美元,预估 2025 年至 2034 年期间复合年增长率将达到 10.3%。这一成长主要得益于 5G 技术的快速普及以及各行各业对先进电子设备的需求激增。随着对高速资料传输和增强连接性的需求不断增加,製造商越来越依赖高频和高速 CCL 等高性能材料。这些层压板在印刷电路板的生产中起着至关重要的作用,印刷电路板为现代电子设备、电信基础设施和高速计算系统提供动力。

人工智慧、物联网 (IoT) 和自动驾驶汽车的日益整合进一步扩大了对高效高速电子元件的需求。随着资料处理需求的不断发展,各行各业都开始关注需要坚固可靠的电路材料的下一代技术。此外,向紧凑、轻巧和节能设备的转变为製造商在材料成分方面进行创新创造了机会,提高了覆铜板的热阻、讯号完整性和整体性能。随着对半导体进步和无线通讯网路的大量投资,高频和高速 CCL 市场将在未来几年大幅扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 37亿美元 |

| 预测值 | 96亿美元 |

| 复合年增长率 | 10.3% |

市场主要分为高频 CCL 和高速 CCL,其中高频部分预计将占据主导地位,到 2024 年将达到 25 亿美元。对先进电信基础设施的日益依赖以及对不间断高速资料流日益增长的需求正在推动对高频 CCL 的需求。电信和消费性电子等产业正在经历前所未有的向更快、更可靠的电子元件的转变,这进一步加速了这些层压板的采用。

就树脂类型而言,高频高速覆铜板(CCL)市场分为酚醛树脂、环氧树脂、聚酰亚胺树脂和双马来酰亚胺-三嗪(BT)树脂。环氧树脂领域在 2024 年占据了 36.3% 的市场份额,这得益于其卓越的性能特点和增强 PCB 结构完整性的能力。环氧树脂配方的不断进步正在提高覆铜板的耐久性、热稳定性和电气性能,使其成为 PCB 製造商的首选。

预计到 2024 年,美国高频高速覆铜板 (CCL) 市场规模将达到 11 亿美元,这得益于 5G 基础设施的快速部署、电子产品的普及以及汽车行业的扩张。随着对更智慧、更有效率电子设备的需求不断增长,对高频和高速覆铜板等高性能材料的需求将在多个领域成长,从而加强其在未来数位转型中的关键作用。

目录

第一章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 5G技术扩展需求

- 电子设备需求不断成长

- 消费性电子产品需求激增

- 航太和国防技术的进步

- 产业陷阱与挑战

- 生产过程成本高

- 严格遵守环境法规

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 高频覆铜板

- 高速覆铜板

第六章:市场估计与预测:依树脂类型,2021-2034

- 主要趋势

- 环氧树脂

- 酚醛树脂

- 聚酰亚胺树脂

- 双马来酰亚胺-三嗪(BT)树脂

第七章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 5G基地台

- 汽车电子

- 消费性电子产品

- 智慧型手机

- 平板电脑

- 笔记型电脑

- 电信

- 路由器

- 开关

- 天线

- 航太和国防

- 雷达系统

- 通讯系统

- 其他的

第八章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AGC Inc. (Asahi Glass Co., Ltd.)

- Arlon Electronic Materials

- Doosan Corporation Electro-Materials

- Elite Material Co., Ltd. (EMC)

- Grace Electron

- Hanwha Advanced Materials

- Hitachi Chemical Co., Ltd.

- Isola Group

- ITEQ Corporation

- Kingboard Laminates Holdings Ltd.

- Mitsubishi Gas Chemical Company, Inc.

- Nan Ya Plastics Corporation

- Nelco Products (Park Electrochemical Corp.)

- Nippon Mektron, Ltd.

- Panasonic Corporation

- Rogers Corporation

- Shengyi Technology Co., Ltd.

- Shinko Electric Industries Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- SYTECH

- Taiwan Union Technology Corporation (TUC)

- TUC (Taiwan Union Technology Corporation)

- Ventec International Group

- Wazam New Materials

- Zhongying Science & Technology

The Global High Frequency High Speed Copper Clad Laminate Market reached USD 3.7 billion in 2024 and is expected to grow at a robust CAGR of 10.3% from 2025 to 2034. This growth is largely fueled by the rapid adoption of 5G technology and the surging demand for advanced electronic devices across various industries. With the increasing need for high-speed data transmission and enhanced connectivity, manufacturers are relying more on high-performance materials such as high-frequency and high-speed CCLs. These laminates play a crucial role in the production of printed circuit boards, which power modern electronic equipment, telecommunications infrastructure, and high-speed computing systems.

The growing integration of artificial intelligence, the Internet of Things (IoT), and autonomous vehicles is further amplifying the demand for efficient and high-speed electronic components. As data processing needs evolve, industries are focusing on next-generation technologies that require robust and reliable circuit materials. Additionally, the shift toward compact, lightweight, and energy-efficient devices is creating opportunities for manufacturers to innovate in material composition, improving the thermal resistance, signal integrity, and overall performance of copper clad laminates. With significant investments in semiconductor advancements and wireless communication networks, the market for high-frequency and high-speed CCLs is poised for substantial expansion in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.6 billion |

| CAGR | 10.3% |

The market is primarily categorized into high-frequency CCL and high-speed CCL, with the high-frequency segment projected to dominate, reaching USD 2.5 billion in 2024. The increasing reliance on advanced telecommunications infrastructure and the growing need for uninterrupted, high-speed data flow are driving the demand for high-frequency CCLs. Industries such as telecommunications and consumer electronics are witnessing an unprecedented shift toward faster, more reliable electronic components, further accelerating the adoption of these laminates.

In terms of resin types, the high frequency high-speed copper clad laminate (CCL) market is segmented into phenolic resin, epoxy resin, polyimide resin, and Bismaleimide-Triazine (BT) resin. The epoxy resin segment held a 36.3% market share in 2024, driven by its superior performance characteristics and ability to enhance the structural integrity of PCBs. Ongoing advancements in epoxy resin formulations are improving the durability, thermal stability, and electrical performance of copper clad laminates, making them a preferred choice among PCB manufacturers.

The U.S. high frequency high-speed copper clad laminate (CCL) market is forecasted to reach USD 1.1 billion in 2024, propelled by the rapid deployment of 5G infrastructure, increased electronics adoption, and the expansion of the automotive industry. As the demand for smarter, more efficient electronic devices continues to rise, the need for high-performance materials like high-frequency and high-speed CCLs is set to grow across multiple sectors, reinforcing their critical role in the future of digital transformation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Demand for 5G technology expansion

- 3.6.1.2 Increasing demand for electronic devices

- 3.6.1.3 Surge in consumer electronics demand

- 3.6.1.4 Advancements in aerospace and defense technologies

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs of production processes

- 3.6.2.2 Stringent environmental regulations compliance

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 High frequency CCL

- 5.3 High speed CCL

Chapter 6 Market Estimates & Forecast, By Resin Type, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Epoxy resin

- 6.3 Phenolic resin

- 6.4 Polyimide resin

- 6.5 Bismaleimide-Triazine (BT) resin

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 5G Base stations

- 7.3 Automotive electronics

- 7.4 Consumer electronics

- 7.4.1 Smartphones

- 7.4.2 Tablets

- 7.4.3 Laptops

- 7.5 Telecommunications

- 7.5.1 Routers

- 7.5.2 Switches

- 7.5.3 Antennas

- 7.6 Aerospace and defense

- 7.6.1 Radar systems

- 7.6.2 Communication systems

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AGC Inc. (Asahi Glass Co., Ltd.)

- 9.2 Arlon Electronic Materials

- 9.3 Doosan Corporation Electro-Materials

- 9.4 Elite Material Co., Ltd. (EMC)

- 9.5 Grace Electron

- 9.6 Hanwha Advanced Materials

- 9.7 Hitachi Chemical Co., Ltd.

- 9.8 Isola Group

- 9.9 ITEQ Corporation

- 9.10 Kingboard Laminates Holdings Ltd.

- 9.11 Mitsubishi Gas Chemical Company, Inc.

- 9.12 Nan Ya Plastics Corporation

- 9.13 Nelco Products (Park Electrochemical Corp.)

- 9.14 Nippon Mektron, Ltd.

- 9.15 Panasonic Corporation

- 9.16 Rogers Corporation

- 9.17 Shengyi Technology Co., Ltd.

- 9.18 Shinko Electric Industries Co., Ltd.

- 9.19 Sumitomo Bakelite Co., Ltd.

- 9.20 SYTECH

- 9.21 Taiwan Union Technology Corporation (TUC)

- 9.22 TUC (Taiwan Union Technology Corporation)

- 9.23 Ventec International Group

- 9.24 Wazam New Materials

- 9.25 Zhongying Science & Technology

COF级柔性铜箔基板市场报告:趋势、预测及竞争分析(至2031年)

COF级柔性铜箔基板市场报告:趋势、预测及竞争分析(至2031年) 全球高频高速 CCL 市场-市场占有率及排名、总收入、需求预测(2025-2031)

全球高频高速 CCL 市场-市场占有率及排名、总收入、需求预测(2025-2031) 全球覆铜板市场(2025 年)

全球覆铜板市场(2025 年) 覆铜板市场:按类型、增强材料、树脂类型、应用分类 - 全球预测 2025-2030

覆铜板市场:按类型、增强材料、树脂类型、应用分类 - 全球预测 2025-2030 覆铜板市场机会、成长动力、产业趋势分析与预测 2024 - 2032

覆铜板市场机会、成长动力、产业趋势分析与预测 2024 - 2032 高频高速CCL的全球市场:市场占有率排行榜,整体销售及需求预测(2024年~2030年)

高频高速CCL的全球市场:市场占有率排行榜,整体销售及需求预测(2024年~2030年) 全球覆铜板市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测覆铜板(CCL)市场规模、份额和趋势分析报告:按层压板类型、增强材料、树脂、应用、地区、细分市场预测,2024-2030年

全球覆铜板市场研究报告 - 2024 年至 2032 年产业分析、规模、份额、成长、趋势和预测覆铜板(CCL)市场规模、份额和趋势分析报告:按层压板类型、增强材料、树脂、应用、地区、细分市场预测,2024-2030年 2024-2028年全球覆铜板市场

2024-2028年全球覆铜板市场