|

市场调查报告书

商品编码

1928944

资料中心液冷市场机会、成长要素、产业趋势分析及2026年至2035年预测Data Center Liquid Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

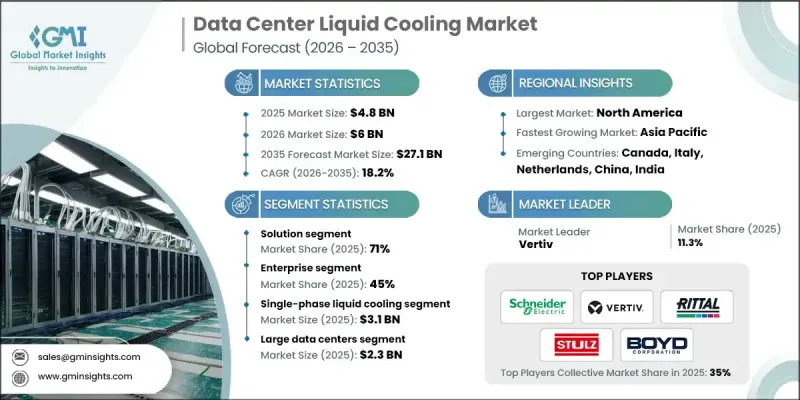

全球资料中心液冷市场预计到 2025 年将达到 48 亿美元,到 2035 年将达到 271 亿美元,年复合成长率为 18.2%。

能源成本不断上涨,加上日益严格的永续性要求,正在加速资料中心采用液冷技术。与传统风冷设施的1.4至1.8相比,液冷系统的电源使用效率 (PUE) 显着降低,仅1.05至1.15,直接降低电力消耗并减少二氧化碳排放。欧盟能源效率指令、德国能源效率法案(目标是到2027年将PUE降至1.3)以及加州能源效率标准等监管要求,正推动营运商采用先进的冷却解决方案。此外,液冷系统能够回收废热用于区域供热或工业流程,使资料中心成为循环能源经济的贡献者,帮助企业实现净零排放目标,并提升营运的永续性。北美地区持续引领资料中心液冷市场,这主要得益于该地区高度集中的超大规模云端营运商、半导体製造商和系统整合商,他们部署了高密度人工智慧和高效能运算基础设施。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 48亿美元 |

| 预测金额 | 271亿美元 |

| 复合年增长率 | 18.2% |

预计到2025年,解决方案领域将占据71%的市场份额,并在2026年至2035年间以15%的复合年增长率成长。晶片级直接冷却是成长最快的技术,它使用直接连接到处理器、GPU或记忆体的冷板或微通道冷却器,在热量散发到大气之前将其去除60-80%。这些系统在晶片表面循环冷却剂,例如含有抑制剂的水或乙二醇混合物,从而实现低至0.01-0.05 度C/W的热阻。

预计2025年,单相液冷系统市场规模将达31亿美元。这类系统在整个循环过程中保持冷却剂处于液态,透过传导和对流传递热量,无需发生相变。依设计不同,冷却剂在18-50°C(60-122°F)的温度下循环流经冷板、浸没式水箱或热交换器,然后由冷却器、干式冷却器或冷却塔将热量从循环迴路中排出。

2025 年美国资料中心液冷市场价值 12.9 亿美元。推动公共部门资料中心采用液冷技术的关键因素包括联邦政府的各项倡议,例如人工智慧和高效能运算计画、CHIPS 法案下的半导体资金,以及包含人工智慧的国防现代化计划。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 元件供应商

- 製造商

- 系统整合商

- 管道路径分析

- 云端服务供应商

- 最终用户

- 成本结构

- 利润率

- 每个阶段的附加价值

- 影响供应链的因素

- 颠覆者

- 供应商情况

- 影响因素

- 司机

- 人工智慧和高效能运算工作负载的指数级增长

- 能源成本上涨和对永续性的需求

- 超大规模和託管资料中心基础架构扩展

- 边缘运算和分散式架构的兴起

- 产业潜在风险与挑战

- 初始投资高且复杂

- 技术风险和操作问题

- 市场机会

- 对现有资料中心设施维修和现代化改造

- 混合冷却架构的开发

- 市场上冷气即服务和託管服务模式的兴起

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国能源政策法案(PUE 标准)

- 加州第24号能源效率法规

- NERC关键基础设施保护(冷却可靠性)

- 欧洲

- 欧盟能源效率指令(EED)

- 德国能源保护法(PUE<=1.3)

- 英国能源产品政策框架

- 气候中和资料中心协议

- 法国资料中心能源报告法规

- 亚太地区

- 中国 GB 50174 PUE 标准(要求 PUE 值低于 1.3)

- 数位印度效率指南

- 新加坡绿色资料中心蓝图

- 日本地震冷却标准

- 澳洲资料中心能源监管

- 拉丁美洲

- 巴西ANATEL能源效率标准

- 墨西哥数据中心永续性指南

- 智利绿色资料中心激励措施

- 中东和非洲

- 阿联酋2030年绿色议程

- 沙乌地阿拉伯2030年资料效率愿景

- 南非关键基础建设法规

- 北美洲

- 波特的分析

- PESTEL 分析

- 技术与创新展望

- 当前技术趋势

- 新兴技术

- 成本細項分析

- 按机架密度等级分類的每千瓦冷却成本

- 新安装与维修之间的成本差异

- 总拥有成本 (TCO)

- 专利分析

- 案例研究

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 架构分析

- 晶片级液冷

- 浸没式冷却

- 空气冷却至液体冷却过渡分析

- 资料中心功率密度趋势

- 对高效能运算的需求日益增长

- 加速边缘运算

- 先进的冷却技术

- 空间优化

- 客製化工作负载解决方案

- 建立关係和加强伙伴关係

- 策略整合伙伴关係模式

- 联合工程服务

- 联合製定综合标准

- 联合竞标超大规模资料中心计划

- 试办合作机会

- 与超大规模资料中心业者营运商的示范计划

- 企业维修中的策略实施

- 策略整合伙伴关係模式

- 与现有基础设施的整合和效率优化

- 整合策略

- 维修之路

- 利用现有冷水系统进行晶片直接贴装

- 后门热交换器直接安装改装

- 模组化添加浸入式舱

- 混合整合

- 空气冷却+液体冷却区

- 部分机架液体辅助(GPU机架)

- 适应新环境

- 如果是校园的一部分,则需与现有系统进行整合设计。

- 隔离式液冷二次迴路

- 效率优化方法

- 热效率

- 机架级散热优化

- 整合式冷热通道封闭系统

- 最大限度减少再循环和旁通气流

- 整合策略

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- LATAM

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金筹措

- 整合与维修的基准

- 在现有机架上安装液冷系统所需时间

- 维修期间停机的影响

- 与现有中央空调/中央空调或附属机组相容

- 扩展营运复杂性

第五章 按组件分類的市场估算与预测,2022-2035年

- 解决方案

- 直接到尖端

- 冷板

- 微通道冷却器

- 身临其境型

- IT底盘

- 浴缸/开放式浴缸

- 后门热交换器

- 主动式(泵浦驱动)

- 被动元件

- 直接到尖端

- 服务

- 託管服务

- 远端监控

- 效能最佳化

- 维护和支援服务

- 专业服务

- 咨询与设计

- 安装与实施

- 託管服务

第六章 依冷却机制分類的市场估计与预测,2022-2035年

- 单相液体冷却

- 两相液冷

7. 冷媒市场估算与预测,2022-2035年

- 水性冷却剂

- 介电液

- 合成流体

- 矿物油

- 生物基/天然系冷却剂

第八章 资料中心市场估算与预测,2022-2035年

- 小规模资料中心

- 中型资料中心

- 大型资料中心

第九章 按应用领域分類的市场估算与预测,2022-2035年

- 伺服器冷却

- CPU散热

- GPU/AI加速器冷却

- 储冷

- 网路冷却

- 其他的

第十章 依最终用途分類的市场估计与预测,2022-2035年

- 对于企业

- BFSI

- 零售与电子商务

- 政府

- 卫生保健

- 製造业

- IT相关服务(ITeS)

- 其他的

- 通讯服务供应商

- 云端服务供应商

第十一章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 波兰

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 哥伦比亚

- 阿根廷

- 智利

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- Global leaders

- Alfa Laval

- Asetek

- Boyd

- CoolIT Systems

- Green Revolution Cooling(GRC)

- LiquidStack

- Rittal

- Schneider Electric

- Stulz

- Vertiv

- 区域玩家

- Asperitas

- DCX Liquid Cooling Systems

- Delta Electronics

- DUG Technology

- Iceotope Technologies

- Kaori Heat Treatment

- Submer Technologies

- 新兴企业

- Accelsius

- Chilldyne

- JETCOOL Technologies

- LiquidCool Solutions

- Midas Green Technologies

- Seguente

- ZutaCore

The Global Data Center Liquid Cooling Market was valued at USD 4.8 billion in 2025 and is estimated to grow at a CAGR of 18.2% to reach USD 27.1 billion by 2035.

Rising energy costs, coupled with stringent sustainability requirements, are accelerating the adoption of liquid cooling technologies across data centers. Liquid cooling systems offer significantly lower Power Usage Effectiveness (PUE) ratios ranging from 1.05 to 1.15 compared to 1.4-1.8 for traditional air-cooled facilities, which directly lowers electricity consumption and reduces carbon emissions. Regulatory mandates, including the EU Energy Efficiency Directive, Germany's Energy Efficiency Act targeting PUE 1.3 by 2027, and California's energy efficiency standards, are pushing operators toward advanced cooling solutions. Furthermore, the ability of liquid cooling systems to recover waste heat for district heating or industrial processes transforms data centers into contributors to circular energy economies, supporting corporate net-zero initiatives and enhancing operational sustainability. North America continues to lead the data center liquid cooling market, driven by a dense concentration of hyperscale cloud operators, semiconductor manufacturers, and systems integrators deploying high-density AI and HPC infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.8 Billion |

| Forecast Value | $27.1 Billion |

| CAGR | 18.2% |

The solution segment held a 71% share in 2025 and is forecast to grow at a CAGR of 15% from 2026 to 2035. Direct-to-chip cooling is the fastest-growing technology, employing cold plates and micro-channel coolers attached directly to processors, GPUs, and memory to remove 60-80% of heat before it enters the air. These systems circulate coolants such as water with inhibitors or glycol mixtures across chip surfaces, achieving thermal resistances as low as 0.01-0.05°C/W.

The single-phase liquid cooling systems segment reached USD 3.1 billion in 2025. These systems maintain coolant in liquid form throughout the cycle, transferring heat via conduction and convection without phase change. Coolants circulate through cold plates, immersion tanks, or heat exchangers at 18-50°C, depending on design, while facility chillers, dry coolers, or towers remove heat from the loop.

U.S. Data Center Liquid Cooling Market captured USD 1.29 billion in 2025. Federal initiatives, including AI and HPC programs, semiconductor funding under the CHIPS Act, and defense modernization projects incorporating AI, are key drivers of liquid cooling adoption in public sector data centers.

Leading companies in the Data Center Liquid Cooling Market include Alfa Laval, Asetek, Boyd, CoolIT Systems, Green Revolution Cooling, LiquidStack, Rittal, Schneider Electric (Motivair), Stulz, and Vertiv. Key strategies adopted by companies in the Data Center Liquid Cooling Market focus on technological innovation, such as developing high-efficiency immersion and direct-to-chip cooling solutions for next-generation processors and GPUs. Firms are forming strategic partnerships with hyperscale cloud providers, semiconductor manufacturers, and HPC integrators to expand deployment. Investments in R&D for energy-efficient, modular, and scalable systems strengthen product differentiation. Companies are also emphasizing geographic expansion into emerging markets, supporting sustainability initiatives, and integrating IoT-enabled monitoring tools to optimize performance, enhance reliability, and maintain long-term client relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022-2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cooling mechanism

- 2.2.4 Coolant

- 2.2.5 Data center

- 2.2.6 Application

- 2.2.7 End use

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component suppliers

- 3.1.1.2 Manufacturers

- 3.1.1.3 System integrators

- 3.1.1.4 Distribution channel analysis

- 3.1.1.5 Cloud service providers

- 3.1.1.6 End user

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Exponential growth in AI and high-performance computing workloads

- 3.2.1.2 Increasing energy costs and sustainability mandates

- 3.2.1.3 Expansion of hyperscale and colocation data center infrastructure

- 3.2.1.4 Proliferation of edge computing and distributed architecture

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment and complexity

- 3.2.2.2 Technical risks and operational concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Retrofit and modernization of existing data center facilities

- 3.2.3.2 Development of hybrid cooling architecture

- 3.2.3.3 Emergence of cooling-as-a-service and managed service models markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Energy Policy Act (PUE Standards)

- 3.4.1.2 California Title 24 Energy Efficiency Regulations

- 3.4.1.3 NERC Critical Infrastructure Protection (Cooling Reliability)

- 3.4.2 Europe

- 3.4.2.1 EU Energy Efficiency Directive (EED)

- 3.4.2.2 German Energy Efficiency Act (PUE ≤1.3)

- 3.4.2.3 UK Energy-related Products Policy Framework

- 3.4.2.4 Climate Neutral Data Centre Pact

- 3.4.2.5 French Data Center Energy Reporting Decree

- 3.4.3 Asia Pacific

- 3.4.3.1 China GB 50174 PUE Standards (≤1.3 Mandate)

- 3.4.3.2 India Digital India Efficiency Guidelines

- 3.4.3.3 Singapore Green Data Centre Roadmap

- 3.4.3.4 Japan Seismic Cooling Standards

- 3.4.3.5 Australia Data Centre Energy Regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazil ANATEL Energy Efficiency Norms

- 3.4.4.2 Mexico Data Center Sustainability Guidelines

- 3.4.4.3 Chile Green Data Center Incentives

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE Green Agenda 2030

- 3.4.5.2 Saudi Arabia Vision Data Efficiency 2030

- 3.4.5.3 South Africa Critical Infrastructure Regulations

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Cost per kW cooled across rack density tiers

- 3.8.2 Greenfield vs retrofit cost delta

- 3.8.3 Total Cost of Ownership (TCO)

- 3.9 Patent analysis

- 3.10 Case studies

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Architecture analysis

- 3.12.1 Direct to chip liquid cooling

- 3.12.2 Immersive cooling

- 3.13 Analysis of shift from air cooling to liquid cooling

- 3.14 Power density trends in data centers

- 3.14.1 Increasing demands for high-performance computing

- 3.14.2 Acceleration of edge computing

- 3.14.3 Advanced cooling technologies

- 3.14.4 Optimization of space

- 3.14.5 Customized workload solutions

- 3.15 Relationship and partnership build-out

- 3.15.1 Strategic integration partnership models

- 3.15.1.1 Joint engineering services

- 3.15.1.2 Co-development of integration standards

- 3.15.1.3 Co-bidding for hyperscale dc projects

- 3.15.2 Pilot deployment collaboration opportunities

- 3.15.2.1 Demonstration projects with hyperscalers

- 3.15.2.2 Strategic adoption in enterprise retrofits

- 3.15.1 Strategic integration partnership models

- 3.16 Integration with existing infrastructure & efficiency optimization

- 3.16.1 Integration strategies

- 3.16.1.1 Retrofit pathways

- 3.16.1.2 Direct-to-chip implementation with existing chilled water

- 3.16.1.3 Rear-door heat exchanger drop-in retrofits

- 3.16.1.4 Immersion pod modular addition

- 3.16.2 Hybrid integration

- 3.16.2.1 Air cooling + liquid cooling zones

- 3.16.2.2 Partial rack liquid assist (GPU racks)

- 3.16.3 Greenfield adaptation

- 3.16.3.1 Design-to-integrate with existing systems if part of campus

- 3.16.3.2 Secondary loop for isolated liquid cooling

- 3.16.4 Efficiency optimization approaches

- 3.16.4.1 Thermal efficiency

- 3.16.4.2 Rack-level heat removal optimization

- 3.16.4.3 Hot/cold aisle containment integration

- 3.16.4.4 Minimizing recirculation and bypass airflow

- 3.16.1 Integration strategies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Integration & retrofit benchmarking

- 4.7.1 Time-to-deploy liquid cooling in existing racks

- 4.7.2 Downtime impact during retrofits

- 4.7.3 Compatibility with existing CRAH/CRAC or in-row units

- 4.7.4 Operational complexity scaling

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Direct to chip

- 5.2.1.1 Cold plates

- 5.2.1.2 Micro-channel coolers

- 5.2.2 Immersive

- 5.2.2.1 IT chassis

- 5.2.2.2 Tub/Open bath

- 5.2.3 Rear-door heat exchangers

- 5.2.3.1 Active (pumped)

- 5.2.3.2 Passive

- 5.2.1 Direct to chip

- 5.3 Service

- 5.3.1 Managed service

- 5.3.1.1 Remote monitoring

- 5.3.1.2 Performance optimization

- 5.3.1.3 Maintenance & support services

- 5.3.2 Professional service

- 5.3.2.1 Consultation & design

- 5.3.2.2 Installation & deployment

- 5.3.1 Managed service

Chapter 6 Market Estimates & Forecast, By Cooling Mechanism, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Single-phase liquid cooling

- 6.3 Two-phase liquid cooling

Chapter 7 Market Estimates & Forecast, By Coolant, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Water-based coolants

- 7.3 Dielectric fluids

- 7.4 Synthetic fluids

- 7.5 Mineral oils

- 7.6 Bio-based/Natural coolants

Chapter 8 Market Estimates & Forecast, By Data Center, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Small data centers

- 8.3 Medium data centers

- 8.4 Large data centers

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Server cooling

- 9.2.1 CPU cooling

- 9.2.2 GPU/AI accelerator cooling

- 9.3 Storage cooling

- 9.4 Networking cooling

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Enterprise

- 10.2.1 BFSI

- 10.2.2 Retail & e-commerce

- 10.2.3 Government

- 10.2.4 Healthcare

- 10.2.5 Manufacturing

- 10.2.6 IT enabled services (ITeS)

- 10.2.7 Others

- 10.3 Telecom service provider

- 10.4 Cloud service provider

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.2.3 Mexico

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Poland

- 11.3.7 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Colombia

- 11.5.3 Argentina

- 11.5.4 Chile

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global leaders

- 12.1.1 Alfa Laval

- 12.1.2 Asetek

- 12.1.3 Boyd

- 12.1.4 CoolIT Systems

- 12.1.5 Green Revolution Cooling (GRC)

- 12.1.6 LiquidStack

- 12.1.7 Rittal

- 12.1.8 Schneider Electric

- 12.1.9 Stulz

- 12.1.10 Vertiv

- 12.2 Regional players

- 12.2.1 Asperitas

- 12.2.2 DCX Liquid Cooling Systems

- 12.2.3 Delta Electronics

- 12.2.4 DUG Technology

- 12.2.5 Iceotope Technologies

- 12.2.6 Kaori Heat Treatment

- 12.2.7 Submer Technologies

- 12.3 Emerging players

- 12.3.1 Accelsius

- 12.3.2 Chilldyne

- 12.3.3 JETCOOL Technologies

- 12.3.4 LiquidCool Solutions

- 12.3.5 Midas Green Technologies

- 12.3.6 Seguente

- 12.3.7 ZutaCore

资料中心自主液冷系统市场:依产品、类型、资料中心类型、最终用途及部署方式划分,全球预测(2026-2032年)

资料中心自主液冷系统市场:依产品、类型、资料中心类型、最终用途及部署方式划分,全球预测(2026-2032年) 资料中心液冷:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

资料中心液冷:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球资料中心液冷市场报告液冷资料中心基础设施产品市场(按组件、冷却技术、流速类型、流体类型、部署类型、机架密度和最终用户划分)-2026-2032年全球预测资料中心液冷设备市场按技术类型、冷却介质、容量范围、应用和最终用户产业划分,全球预测(2026-2032年)

2026年全球资料中心液冷市场报告液冷资料中心基础设施产品市场(按组件、冷却技术、流速类型、流体类型、部署类型、机架密度和最终用户划分)-2026-2032年全球预测资料中心液冷设备市场按技术类型、冷却介质、容量范围、应用和最终用户产业划分,全球预测(2026-2032年) 全球资料中心液冷市场评估:按组件、规模、类型、终端用户产业、地区、机会和预测(2018-2032 年)

全球资料中心液冷市场评估:按组件、规模、类型、终端用户产业、地区、机会和预测(2018-2032 年) 资料中心液冷市场规模、份额及成长分析(按产品、资料中心类型、资料中心规模、冷却模式、基础设施、应用、分销通路和地区划分)-2026-2033年产业预测

资料中心液冷市场规模、份额及成长分析(按产品、资料中心类型、资料中心规模、冷却模式、基础设施、应用、分销通路和地区划分)-2026-2033年产业预测 资料中心液冷市场 - 全球产业规模、份额、趋势、机会和预测(按组件、冷却类型、最终用户、地区和竞争格局划分,2020-2030 年预测)资料中心液体冷却市场(按冷却技术、组件、技术、层级类型、应用、资料中心规模和最终用户划分)—2025-2030 年全球预测

资料中心液冷市场 - 全球产业规模、份额、趋势、机会和预测(按组件、冷却类型、最终用户、地区和竞争格局划分,2020-2030 年预测)资料中心液体冷却市场(按冷却技术、组件、技术、层级类型、应用、资料中心规模和最终用户划分)—2025-2030 年全球预测 2025-2029年全球人工智慧资料中心液体冷却市场

2025-2029年全球人工智慧资料中心液体冷却市场