|

市场调查报告书

商品编码

1982318

2026 年至 2035 年显微外科机器人市场机会、成长要素、产业趋势与预测。Microsurgery Robot Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

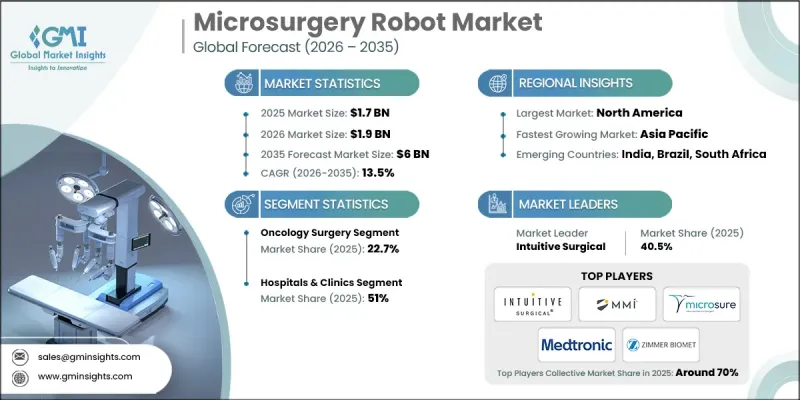

2025 年全球显微外科果冻市场价值为 17 亿美元,预计到 2035 年将达到 60 亿美元,年复合成长率为 13.5%。

市场扩张的驱动力来自对微创手术技术日益增长的需求、机器人辅助平台技术的快速发展,以及需要精准手术干预的慢性疾病数量的不断增加。已开发国家对先进机器人研发投入的增加,以及外科培训计画的扩展,正在推动其普及。持续的研发投入、医疗技术(MedTech)领域的合作,以及价格较亲民的机器人系统的出现,进一步加速了商业化进程。由于微创手术具有创伤小、恢復时间短、併发症风险低、病患满意度高等临床优势,全球医疗机构正转向微创手术。医院也优先采用机器人技术,以提高手术精度、规范复杂手术流程并优化长期治疗效果,这使得果冻机器人成为现代外科手术环境中的变革性解决方案。

| 市场范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 17亿美元 |

| 预测金额 | 60亿美元 |

| 复合年增长率 | 13.5% |

全球慢性疾病负担日益加重,需要手术治疗,这持续推动对机器人辅助果冻系统的需求。在复杂的多学科手术中,机器人平台所提供的更高操控性、更少的震颤和更佳的视野正发挥着不可估量的作用。随着手术复杂性的增加,机器人技术正被用来提高手术的精准度、一致性和整体效率,强化其在先进医疗服务体系中的作用。

预计到2025年,泌尿系统手术市场规模将达3.523亿美元。该领域持续做出重大贡献,主要得益于机器人系统在该专科领域的早期应用及其与常规手术流程的持续整合。推动成长的因素包括:向发展中地区的扩张、在技术先进的手术中应用日益广泛,以及旨在提升手术效果的专用手术机器人平台的推出。

到2025年,医院和诊所将占据51%的市场。大规模三级医疗机构和大学附属医院将成为机器人手术的主要应用对象,它们通常在不同的外科领域运行多个机器人系统。这些机构受惠于大量的手术量、完善的培训计画、支持性的报销机制以及采用先进技术所需的财力。

美国显微外科手术机器人市场预计2025年将达到8.988亿美元。日益增多的专业外科手术预计将推动市场持续成长。美国凭藉其先进的医疗基础设施、公共和私人保险公司提供的优惠报销政策、促进创新的清晰监管流程、强劲的跨专科手术需求以及完善的外科教育项目,继续引领市场。

目录

第一章:调查方法

- 研究途径

- 品质改进计划

- GMI人工智慧政策及对资料完整性的承诺

- 资讯来源一致性通讯协定

- GMI人工智慧政策及对资料完整性的承诺

- 调查过程和可靠性评分

- 研究路径的组成部分

- 评分组成部分

- 数据收集

- 主要来源部分列表

- 资料探勘资讯来源

- 付费资讯来源

- 区域资讯来源

- 付费资讯来源

- 基本估算和计算方法

- 基准年的计算

- 预测模型

- 量化市场影响分析

- 生长参数对预测的数学影响

- 量化市场影响分析

- 关于调查透明度的补充信息

- 资讯来源归属框架

- 品质保证指标

- 对信任的承诺

第二章执行摘要

第三章业界考察

- 生态系分析

- 影响产业的因素

- 促进因素

- 对微创手术的需求日益增长

- 技术进步

- 慢性病发生率增加

- 已开发国家加大对果冻机器人研发的资金投入

- 产业潜在风险与挑战

- 机器人系统相关的高成本

- 熟练医护人员短缺

- 机会

- 人工智慧和机器学习在预测性手术的应用

- 机器人手术器械小型化以实现精准手术

- 促进因素

- 成长潜力分析

- 监理情势

- 北美洲

- 欧洲

- 亚太地区

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格分析

- 救赎方案

- Start-Ups趋势

- 政策展望

- 波特的分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

第四章 竞争情势

- 介绍

- 企业矩阵分析

- 企业市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估计与预测:依应用领域划分,2022-2035年

- 外科肿瘤学

- 泌尿系统手术

- 妇产科手术

- 显微吻合术

- 重组手术

- 耳鼻喉科手术

- 胃肠外科手术

- 心血管外科

- 输尿管镜检查

- 神经血管外科

- 眼科手术

- 其他用途

第六章 市场估算与预测:依最终用途划分,2022-2035年

- 医院和诊所

- 门诊手术中心

- 研究机构

- 其他最终用户

第七章 市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第八章:公司简介

- ASENSUS SURGICAL

- CMR Surgical

- Distalmotion

- Intuitive Surgical

- Medical Micro Instruments(MMI)

- Medtronic

- meerecompany

- MicroSure

- Preceyes

- Siemens Healthineers

- Zimmer Biomet

The Global Microsurgery Robot Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 13.5% to reach USD 6 billion by 2035.

Market expansion is fueled by the growing preference for minimally invasive surgical techniques, rapid innovation in robotic-assisted platforms, and the increasing incidence of chronic health conditions that require precision-based surgical intervention. Rising financial support for advanced robotic development in developed economies, combined with expanding surgeon training initiatives, is strengthening adoption rates. Continuous R&D investments, MedTech collaborations, and the introduction of more affordable robotic systems are further accelerating the commercialization process. Healthcare providers worldwide are shifting toward minimally invasive approaches due to clinical advantages such as reduced trauma, shorter recovery durations, lower complication risks, and improved patient satisfaction. Hospitals are also prioritizing robotic integration to enhance surgical precision, standardize complex procedures, and optimize long-term treatment outcomes, positioning microsurgery robots as a transformative solution in modern operating environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $6 Billion |

| CAGR | 13.5% |

The increasing global burden of chronic disorders requiring surgical management continues to drive demand for robotic-assisted microsurgical systems. Complex procedures across multiple specialties benefit from enhanced dexterity, tremor filtration, and magnified visualization enabled by robotic platforms. As surgical complexity increases, robotic technologies are being utilized to improve accuracy, consistency, and overall procedural efficiency, strengthening their role in advanced healthcare delivery systems.

The urology surgery segment generated USD 352.3 million in 2025. This segment remains a strong contributor due to early adoption of robotic systems within the specialty and continued integration into routine surgical workflows. Growth momentum is expected to stem from expansion into developing regions, increasing use in technically demanding procedures, and the introduction of procedure-specific robotic platforms designed to enhance surgical performance.

The hospitals and clinics segment held 51% share in 2025. Large tertiary care institutions and academic medical centers account for a substantial portion of installations, often managing multiple robotic systems across diverse surgical disciplines. These facilities benefit from high procedural volumes, structured training ecosystems, supportive reimbursement frameworks, and the capital capacity required for advanced technology acquisition.

U.S. Microsurgery Robot Market was valued at USD 898.8 million in 2025. Rising volumes of specialized surgical procedures are anticipated to stimulate continued expansion. The country maintains leadership due to sophisticated healthcare infrastructure, favorable reimbursement support from public and private payers, well-defined regulatory pathways encouraging innovation, strong procedural demand across specialties, and comprehensive surgeon education programs.

Key companies operating in the Global Microsurgery Robot Market include Intuitive Surgical, Medtronic, Siemens Healthineers, Zimmer Biomet, CMR Surgical, ASENSUS SURGICAL, Distalmotion, Medical Micro Instruments (MMI), MicroSure, meerecompany, and Preceyes. Companies in the microsurgery robot market are strengthening their competitive positioning through sustained investment in next-generation robotic platforms and digital surgical ecosystems. Strategic partnerships with hospitals and academic institutions support training expansion and product validation. Manufacturers are prioritizing system miniaturization, improved haptic feedback, and AI-enabled imaging integration to enhance clinical precision. Portfolio diversification across multiple surgical specialties allows companies to broaden revenue streams. Many players are also expanding geographically through distribution alliances and localized manufacturing to improve accessibility.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for minimally invasive surgical procedures

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising incidences of chronic conditions

- 3.2.1.4 Increasing funding for development of microsurgery robots in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with robotic systems

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.3 Opportunities

- 3.2.3.1 Integration with AI and machine learning for predictive surgery

- 3.2.3.2 Miniaturization of robotic instruments for precise procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Reimbursement scenario

- 3.8 Start-up scenario

- 3.9 Policy outlook

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Gap analysis

- 3.13 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Oncology surgery

- 5.3 Urology surgery

- 5.4 Obstetrics and gynecology surgery

- 5.5 Micro anastomosis

- 5.6 Reconstructive surgery

- 5.7 ENT surgery

- 5.8 Gastrointestinal surgery

- 5.9 Cardiovascular surgery

- 5.10 Ureterorenoscopy

- 5.11 Neurovascular surgery

- 5.12 Ophthalmology surgery

- 5.13 Other applications

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals and clinics

- 6.3 Ambulatory surgical centers

- 6.4 Research institutes

- 6.5 Other end-users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 ASENSUS SURGICAL

- 8.2 CMR Surgical

- 8.3 Distalmotion

- 8.4 Intuitive Surgical

- 8.5 Medical Micro Instruments (MMI)

- 8.6 Medtronic

- 8.7 meerecompany

- 8.8 MicroSure

- 8.9 Preceyes

- 8.10 Siemens Healthineers

- 8.11 Zimmer Biomet

2026年全球显微外科机器人市场报告

2026年全球显微外科机器人市场报告 显微外科手术机器人市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测

显微外科手术机器人市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测 全球果冻机器人市场

全球果冻机器人市场 全球显微手术机器人市场:成长、未来展望与竞争分析(2024-2032 年)

全球显微手术机器人市场:成长、未来展望与竞争分析(2024-2032 年)