|

市场调查报告书

商品编码

1665059

人类免疫缺乏病毒治疗市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Human Immunodeficiency Virus Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

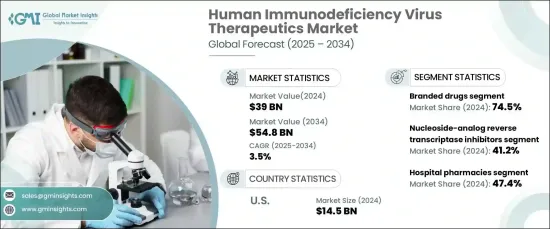

2024 年全球人类免疫缺乏病毒治疗市场估值达到 390 亿美元,预计 2025 年至 2034 年期间将以 3.5% 的复合年增长率稳步增长。 市场扩张主要得益于爱滋病毒感染率的上升、治疗方案的重大进步、政府的支持倡议以及有利的监管批准。这些因素结合起来在促进市场持续成长方面发挥着至关重要的作用。

市场主要依药品类型分为品牌药和仿製药。 2024 年,品牌药物凭藉其经过验证的疗效、长期的临床可靠性以及在爱滋病毒治疗中值得信赖的表现,占据了 74.5% 的大幅份额,占据市场主导地位。固定剂量组合越来越受欢迎,因为它们提供了简化的给药方案,从而提高了患者对治疗计划的依从性。它们在联合疗法中发挥的关键作用,特别是有效抑制病毒量,并继续推动市场需求,确保未来几年市场持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 390亿美元 |

| 预测值 | 548亿美元 |

| 复合年增长率 | 3.5% |

市场的分销管道进一步凸显了爱滋病毒治疗的覆盖范围和可及性。主要分销管道包括药局和零售药局、网路药局和医院药局。 2024 年,医院药局占最大的市场份额,达到 47.4%。医院药房设备齐全,可提供更广泛的专门爱滋病毒药物,包括先进的抗逆转录病毒疗法和需要精心管理的注射疗法。他们能够在医疗专业人员的监督下提供包括联合疗法在内的尖端治疗,这使得他们成为需要专门护理和关注的患者的首选。

在美国,爱滋病毒治疗市场在 2024 年创造了 145 亿美元的收入。医疗补助(Medicaid)和医疗保险(Medicare)等健康保险计划的广泛普及进一步保证了患者能够负担得起所需的救命治疗。此外,广泛的零售药局、医院设施和线上平台网路有助于促进爱滋病毒治疗药物的无缝分发和可用性,确保患者能够轻鬆获得所需的治疗。

2024 年全球人类免疫缺乏病毒(HIV) 治疗市场估值达到 390 亿美元,预计 2025 年至 2034 年期间将以 3.5% 的复合年增长率稳步增长。这些因素结合起来在促进市场持续成长方面发挥着至关重要的作用。

市场主要依药品类型分为品牌药和仿製药。 2024 年,品牌药物凭藉其经过验证的疗效、长期的临床可靠性以及在爱滋病毒治疗中值得信赖的表现,占据了 74.5% 的大幅份额,占据市场主导地位。固定剂量组合越来越受欢迎,因为它们提供了简化的给药方案,从而提高了患者对治疗计划的依从性。它们在联合疗法中发挥的关键作用,特别是有效抑制病毒量,并继续推动市场需求,确保未来几年市场持续成长。

市场的分销管道进一步凸显了爱滋病毒治疗的覆盖范围和可及性。主要分销管道包括药局和零售药局、网路药局和医院药局。 2024 年,医院药局占最大的市场份额,达到 47.4%。医院药房设备齐全,可提供更广泛的专门爱滋病毒药物,包括先进的抗逆转录病毒疗法和需要精心管理的注射疗法。他们能够在医疗专业人员的监督下提供包括联合疗法在内的尖端治疗,这使得他们成为需要专门护理和关注的患者的首选。

在美国,爱滋病毒治疗市场在 2024 年创造了 145 亿美元的收入。医疗补助(Medicaid)和医疗保险(Medicare)等健康保险计划的广泛普及进一步保证了患者能够负担得起所需的救命治疗。此外,零售药局、医院设施和

目录

第 1 章:方法论与范围

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 爱滋病毒感染率高

- 治疗方案的进展

- 透过政府措施和健康计划增加支持

- 有利的监管批准

- 产业陷阱与挑战

- 治疗费用高昂

- 与患者依从性和治疗连续性相关的担忧

- 成长动力

- 成长潜力分析

- 监管格局

- 差距分析

- 专利分析

- 技术格局

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略展望

第 5 章:市场估计与预测:按药物类型,2021 年至 2034 年

- 主要趋势

- 品牌药物

- 仿製药

第 6 章:市场估计与预测:按药物类别,2021 年至 2034 年

- 主要趋势

- 核苷类似物逆转录酶抑制剂

- 整合酶抑制剂

- 非核苷逆转录酶抑制剂

- 蛋白酶抑制剂

- 进入和融合抑制剂

- 辅助受体拮抗剂

第 7 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 药局和零售药局

- 网路药局

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AbbVie

- Aurobindo Pharma

- Boehringer Ingelheim International GmbH

- Bristol-Myers Squibb Company

- Cipla

- Dr. Reddy's Laboratories

- F. Hoffmann-La Roche

- Gilead Sciences

- Hetero Drugs

- Johnson & Johnson

- Merck & Co

- Mylan NV (Viatris)

- Sun Pharmaceutical Industries

- Teva Pharmaceutical Industries

- ViiV Healthcare

The Global Human Immunodeficiency Virus Therapeutics Market reached a valuation of USD 39 billion in 2024 and is projected to experience steady growth at a CAGR of 3.5% from 2025 to 2034. The market expansion is largely driven by the rising rates of HIV infections, significant advancements in treatment options, supportive government initiatives, and favorable regulatory approvals. These factors combined are playing a crucial role in fostering the market's ongoing growth trajectory.

The market is primarily segmented by drug type into branded and generic drugs. In 2024, branded drugs led the market with a substantial share of 74.5%, attributed to their proven efficacy, long-standing clinical reliability, and trusted performance in HIV treatment. Fixed-dose combinations have been gaining widespread popularity, as they offer simplified dosing regimens that enhance patient adherence to treatment plans. Their key role in combination therapies, particularly for effectively suppressing viral loads, continues to drive demand in the market, ensuring consistent market growth in the years to come.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39 Billion |

| Forecast Value | $54.8 Billion |

| CAGR | 3.5% |

The market's distribution channels further highlight the reach and accessibility of HIV therapeutics. The primary distribution segments include drug stores and retail pharmacies, online pharmacies, and hospital pharmacies. In 2024, hospital pharmacies held the largest share of the market, with a notable 47.4%. Hospital pharmacies are well-equipped to offer a broader selection of specialized HIV medications, including advanced antiretroviral therapies and injectable treatments that require careful administration. Their ability to provide cutting-edge treatments, including combination regimens, under the supervision of healthcare professionals makes them the preferred choice for patients who require specialized care and attention.

In the United States, the HIV therapeutics market generated USD 14.5 billion in 2024. The country benefits from a highly developed healthcare infrastructure that ensures widespread access to advanced HIV treatments, including clinical trials and long-acting injectable therapies. The widespread availability of health insurance programs, such as Medicaid and Medicare, further guarantees that patients can afford the life-saving therapies they need. Moreover, the extensive network of retail pharmacies, hospital facilities, and online platforms helps facilitate seamless distribution and availability of HIV therapeutics, ensuring that patients can easily access the treatments they require.

The global Human Immunodeficiency Virus (HIV) therapeutics market reached a valuation of USD 39 billion in 2024 and is projected to experience steady growth at a CAGR of 3.5% from 2025 to 2034. The market expansion is largely driven by the rising rates of HIV infections, significant advancements in treatment options, supportive government initiatives, and favorable regulatory approvals. These factors combined are playing a crucial role in fostering the market's ongoing growth trajectory.

The market is primarily segmented by drug type into branded and generic drugs. In 2024, branded drugs led the market with a substantial share of 74.5%, attributed to their proven efficacy, long-standing clinical reliability, and trusted performance in HIV treatment. Fixed-dose combinations have been gaining widespread popularity, as they offer simplified dosing regimens that enhance patient adherence to treatment plans. Their key role in combination therapies, particularly for effectively suppressing viral loads, continues to drive demand in the market, ensuring consistent market growth in the years to come.

The market's distribution channels further highlight the reach and accessibility of HIV therapeutics. The primary distribution segments include drug stores and retail pharmacies, online pharmacies, and hospital pharmacies. In 2024, hospital pharmacies held the largest share of the market, with a notable 47.4%. Hospital pharmacies are well-equipped to offer a broader selection of specialized HIV medications, including advanced antiretroviral therapies and injectable treatments that require careful administration. Their ability to provide cutting-edge treatments, including combination regimens, under the supervision of healthcare professionals makes them the preferred choice for patients who require specialized care and attention.

In the United States, the HIV therapeutics market generated USD 14.5 billion in 2024. The country benefits from a highly developed healthcare infrastructure that ensures widespread access to advanced HIV treatments, including clinical trials and long-acting injectable therapies. The widespread availability of health insurance programs, such as Medicaid and Medicare, further guarantees that patients can afford the life-saving therapies they need. Moreover, the extensive network of retail pharmacies, hospital facilities, and on

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High incidence of HIV infections

- 3.2.1.2 Advances in therapeutic treatment options

- 3.2.1.3 Growing support through government initiatives and health programs

- 3.2.1.4 Favorable regulatory approvals

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Concerns related to patient adherence and treatment continuity

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded drugs

- 5.3 Generic drugs

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Nucleoside-analog reverse transcriptase inhibitors

- 6.3 Integrase inhibitors

- 6.4 Non-nucleoside reverse transcriptase inhibitors

- 6.5 Protease inhibitors

- 6.6 Entry and fusion inhibitors

- 6.7 Coreceptor antagonists

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Drugs stores and retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Aurobindo Pharma

- 9.3 Boehringer Ingelheim International GmbH

- 9.4 Bristol-Myers Squibb Company

- 9.5 Cipla

- 9.6 Dr. Reddy's Laboratories

- 9.7 F. Hoffmann-La Roche

- 9.8 Gilead Sciences

- 9.9 Hetero Drugs

- 9.10 Johnson & Johnson

- 9.11 Merck & Co

- 9.12 Mylan N.V. (Viatris)

- 9.13 Sun Pharmaceutical Industries

- 9.14 Teva Pharmaceutical Industries

- 9.15 ViiV Healthcare

人类免疫力缺乏病毒(HIV)治疗市场:依药物类别、治疗方法、治疗阶段、给药途径、病患类型及通路划分-2026-2032年全球市场预测全球暴露前预防市场(按产品类型、剂型、分销管道和最终用户划分)预测(2026-2032年)按产品类型、分子类型、分销管道、最终用户和给药方法分類的肠外暴露前预防(PrEP)市场,全球预测,2026-2032年长效PrEP市场依产品类型、最终用户、给药方案及分销管道划分,全球预测(2026-2032年)

人类免疫力缺乏病毒(HIV)治疗市场:依药物类别、治疗方法、治疗阶段、给药途径、病患类型及通路划分-2026-2032年全球市场预测全球暴露前预防市场(按产品类型、剂型、分销管道和最终用户划分)预测(2026-2032年)按产品类型、分子类型、分销管道、最终用户和给药方法分類的肠外暴露前预防(PrEP)市场,全球预测,2026-2032年长效PrEP市场依产品类型、最终用户、给药方案及分销管道划分,全球预测(2026-2032年) HIV相关脂肪萎缩市场-全球产业规模、份额、趋势、机会及预测(按类型、给药途径、分销管道、地区和竞争格局划分,2021-2031年)

HIV相关脂肪萎缩市场-全球产业规模、份额、趋势、机会及预测(按类型、给药途径、分销管道、地区和竞争格局划分,2021-2031年) 人类免疫缺乏病毒治疗药的全球市场:成长,未来展望,竞争分析 (2025年~2033年)

人类免疫缺乏病毒治疗药的全球市场:成长,未来展望,竞争分析 (2025年~2033年) 口服抗病毒市场,按类型、给药途径、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测暴露前预防 (PrEP) 市场,按产品类型、按使用类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

口服抗病毒市场,按类型、给药途径、应用、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测暴露前预防 (PrEP) 市场,按产品类型、按使用类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测