|

市场调查报告书

商品编码

1665072

汽车油管理模组市场机会、成长动力、产业趋势分析与预测 2025 - 2034Automotive Oil Management Module Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

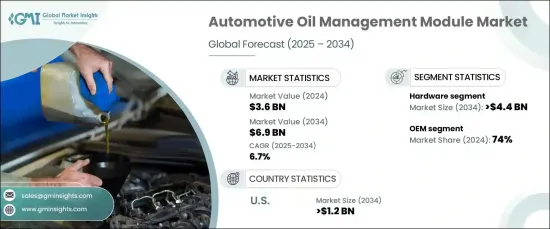

2024 年全球汽车油管理模组市场价值为 36 亿美元,预计将在 2025 年至 2034 年期间以 6.7% 的复合年增长率强劲增长。

随着各国政府实施更严格的排放标准以对抗空气污染和温室气体排放,汽车製造商越来越多地整合创新技术来遵守标准。高效的油管理系统对于优化引擎性能和减少排放至关重要,可帮助车辆满足严格的法规要求同时保持最佳效率。这些模组对于确保现代车辆的最佳引擎功能和可持续性至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 36亿美元 |

| 预测值 | 69亿美元 |

| 复合年增长率 | 6.7% |

市场按组件细分,包括硬体、软体和服务。 2024 年,硬体组件占据市场主导地位,占有 67% 的份额,预计到 2034 年将创造 44 亿美元的产值。这些部件在提高引擎性能、提高燃油效率和满足排放法规方面发挥着至关重要的作用,使其成为该行业的基石。

此外,市场根据最终用途分为OEM (原始设备製造商)和售后市场。 2024 年, OEM领域占据了 74% 的市场份额,反映出其重要地位。汽车製造过程中整合的油管理模组对于满足高品质标准、提高引擎性能和遵守监管要求至关重要。汽车製造商依靠这些系统来维护他们的声誉并为客户提供卓越的性能。

2024 年,美国汽车油管理模组市场表现出显着的主导地位,占据了该地区 87% 的份额,预计到 2034 年将超过 12 亿美元。对技术先进型汽车的需求不断增长以及在研发方面的大量投资进一步促进了市场成长。美国明确强调永续性和尖端解决方案,仍然是全球采用先进石油管理模组的主要推动力。

报告内容

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 技术提供者

- 零件供应商

- 製造商

- 原始设备製造商

- 供应商概况

- 利润率分析

- 技术与创新格局

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 增加汽车产量和车队规模

- 汽车零件的技术进步

- 越来越重视燃油效率

- 售后市场对维护和更换的需求不断增加

- 产业陷阱与挑战

- 先进石油管理系统的初始成本高

- 严格遵守法规

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第六章:市场估计与预测:依功能,2021 - 2034 年

- 主要趋势

- 油压管理

- 油过滤

- 油温控制

- 油流监控

- 油流管理

- 油品品质监控

- 综合油系统管理

第 7 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第 8 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第九章:公司简介

- Aisin Seiki Co. Ltd.

- BorgWarner Inc.

- Bosch Mobility Solutions

- Continental AG

- Cummins Inc.

- Delphi Technologies

- DENSO Corporation

- Eaton Corporation

- Hella GmbH & Co. KGaA

- Hengst SE

- Hitachi Astemo

- Hutchinson SA

- Magna International

- MAHLE GmbH

- MANN+HUMMEL

- Nidec Corporation

- Parker Hannifin

- Schaeffler Group

- Valeo

- ZF Friedrichshafen AG

The Global Automotive Oil Management Module Market, valued at USD 3.6 billion in 2024, is set to experience robust growth at a CAGR of 6.7% between 2025 and 2034. This expansion is fueled by the surging demand for passenger and commercial vehicles worldwide, creating a heightened need for advanced oil management systems.

As governments enforce stricter emission standards to combat air pollution and greenhouse gas emissions, automakers are increasingly integrating innovative technologies to comply. Efficient oil management systems are pivotal in optimizing engine performance and reducing emissions, helping vehicles meet stringent regulations while maintaining peak efficiency. These modules are indispensable for ensuring optimal engine functionality and sustainability in modern vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 6.7% |

The market is segmented by components, including hardware, software, and services. In 2024, hardware components dominated the market with a 67% share and are forecasted to generate USD 4.4 billion by 2034. Critical hardware elements such as oil pumps, sensors, filters, and valves are essential for regulating oil flow, pressure, filtration, and temperature control. These components play a vital role in enhancing engine performance, boosting fuel efficiency, and achieving compliance with emission regulations, making them a cornerstone of the industry.

Additionally, the market is categorized by end-use into OEM (Original Equipment Manufacturer) and aftermarket segments. The OEM segment captured 74% of the market in 2024, reflecting its prominence. Oil management modules integrated during vehicle manufacturing are instrumental in meeting high-quality standards, enhancing engine performance, and complying with regulatory requirements. Automakers rely on these systems to uphold their reputation and deliver superior performance to customers.

The U.S. automotive oil management module market showcased remarkable dominance in 2024, accounting for 87% of the regional share and is projected to surpass USD 1.2 billion by 2034. This leadership is attributed to the country's advanced automotive industry, strong focus on innovation, and stringent fuel economy standards. The rising demand for technologically advanced vehicles and significant investments in research and development further bolster market growth. With a clear emphasis on sustainability and cutting-edge solutions, the U.S. remains a key driver for the adoption of advanced oil management modules globally.

Report Content

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Technology providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 OEMs

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing vehicle production and fleet size

- 3.7.1.2 Technological advancements in automotive components

- 3.7.1.3 Growing focus on fuel efficiency

- 3.7.1.4 Increasing aftermarket demand for maintenance and replacement

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs of advanced oil management systems

- 3.7.2.2 Stringent regulatory compliance

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Function, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Oil pressure management

- 6.3 Oil filtration

- 6.4 Oil temperature control

- 6.5 Oil flow monitoring

- 6.6 Oil flow management

- 6.7 Oil quality monitoring

- 6.8 Integrated oil system management

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Aisin Seiki Co. Ltd.

- 9.2 BorgWarner Inc.

- 9.3 Bosch Mobility Solutions

- 9.4 Continental AG

- 9.5 Cummins Inc.

- 9.6 Delphi Technologies

- 9.7 DENSO Corporation

- 9.8 Eaton Corporation

- 9.9 Hella GmbH & Co. KGaA

- 9.10 Hengst SE

- 9.11 Hitachi Astemo

- 9.12 Hutchinson SA

- 9.13 Magna International

- 9.14 MAHLE GmbH

- 9.15 MANN+HUMMEL

- 9.16 Nidec Corporation

- 9.17 Parker Hannifin

- 9.18 Schaeffler Group

- 9.19 Valeo

- 9.20 ZF Friedrichshafen AG

电池管理系统硬体在环测试市场(按最终用途、车辆类型、组件类型、测试模式、应用和BMS类型划分),全球预测,2026-2032年

电池管理系统硬体在环测试市场(按最终用途、车辆类型、组件类型、测试模式、应用和BMS类型划分),全球预测,2026-2032年 汽车保固管理软体市场规模、份额和成长分析(按产品类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测

汽车保固管理软体市场规模、份额和成长分析(按产品类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测 全球汽车终端认证市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车终端认证市场规模、份额、趋势和成长分析报告(2026-2034) 汽车软体市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、应用、软体层级、地区及竞争格局划分,2021-2031年)高阶驾驶辅助系统的硬体在环测试市场,按测试类型、测试阶段、车辆类型和应用划分,全球预测(2026-2032年)

汽车软体市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、应用、软体层级、地区及竞争格局划分,2021-2031年)高阶驾驶辅助系统的硬体在环测试市场,按测试类型、测试阶段、车辆类型和应用划分,全球预测(2026-2032年) 汽车软体:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车软体:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 汽车软体市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车软体市场机会、成长要素、产业趋势分析及2026年至2035年预测 日本汽车软体市场按产品类型、车辆类型、应用和地区划分,2026-2034年

日本汽车软体市场按产品类型、车辆类型、应用和地区划分,2026-2034年 汽车软体市场规模、份额和成长分析(按软体类型、应用、最终用途、部署类型和地区划分)-2026-2033年产业预测

汽车软体市场规模、份额和成长分析(按软体类型、应用、最终用途、部署类型和地区划分)-2026-2033年产业预测 车载娱乐系统市场预测至2032年:按系统类型、组件、车辆类型、通路和地区分類的全球分析

车载娱乐系统市场预测至2032年:按系统类型、组件、车辆类型、通路和地区分類的全球分析