|

市场调查报告书

商品编码

1665280

混合动力飞机市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Hybrid Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

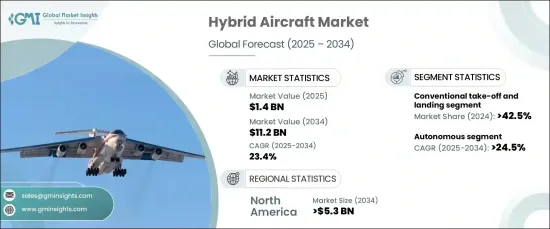

预计到 2034 年,全球混合动力飞机市场规模将达到 14 亿美元,2025 年至 2034 年期间的复合年增长率将达到惊人的 23.4%。

电力推进和储能係统的技术进步在塑造混合动力飞机的未来方面发挥关键作用。这些混合电力推进系统旨在透过降低碳排放和提高燃油效率来减少航空对环境的影响。製造商越来越多地将这些系统整合到区域和短途飞机中,并且根据未来电池技术的改进,有可能实现长途应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 14亿美元 |

| 预测值 | 112亿美元 |

| 复合年增长率 | 23.4% |

根据升力技术,市场分为不同的类别,包括常规起降(CTOL)、短距起降(STOL)和垂直起降(VTOL)飞机。 2024 年,CTOL 领域占据最大的市场份额,为 42.5%,预计将继续保持强劲成长。混合型 CTOL 飞机尤其具有吸引力,因为它们可以利用现有的航空基础设施,例如跑道和维护设施,使其成为未来航空业的实用且可持续的选择。

根据运行模式,市场也细分为有人驾驶飞机和自动驾驶飞机。自动驾驶领域将经历快速成长,预计到 2034 年复合年增长率将达到 24.5%。这将提高安全性和效率,特别是在货物运输、监视和灾难应变等领域,无人机提供了经济高效且可靠的解决方案。

北美目前是混合动力飞机市场的主导地区,预计将继续成长,到 2034 年市场价值达到 53 亿美元。大型航太公司和新兴新创公司正在大力投资电动和混合电动推进技术,主要关注区域和短途混合动力飞机。这些解决方案在燃油效率和减少排放方面具有显着优势,推动了市场的发展。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 对环保航空解决方案的需求不断增加

- 电动垂直起降 (eVTOL) 解决方案的成长

- 日益关注高效能混合动力引擎的开发

- 对于混合电力推进系统的能量储存和效率改进的需求日益增加。

- 公营和私营部门对混合动力飞机研究的资金投入不断增加

- 产业陷阱与挑战

- 开发成本高

- 电池限制

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依飞机类型,2021-2034 年

- 主要趋势

- 区域运输飞机

- 公务机

- 轻型和超轻型飞机

- 无人机

- 先进的空中机动性

第 6 章:市场估计与预测:按升降技术,2021 年至 2034 年

- 主要趋势

- 常规起飞和着陆

- 短距起飞和降落

- 垂直起飞和降落

第 7 章:市场估计与预测:按燃料类型,2021-2034 年

- 主要趋势

- 燃料混合动力

- 氢混合动力

第 8 章:市场估计与预测:按范围,2021 年至 2034 年

- 主要趋势

- < 100 公里

- 101公里至500公里

- > 501 公里

第 9 章:市场估计与预测:按营运模式 2021-2034

- 主要趋势

- 试航

- 自主

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Airbus

- Ampaire

- Electric Aviation Group

- Embraer

- Faradair Aerospace

- General Electric

- Heart Aerospace

- Pipistrel

- RTX

- Safran

- Voltaero

- XTI Aircraft

The Global Hybrid Aircraft Market is projected to reach USD 1.4 billion by 2034, growing at an impressive CAGR of 23.4% from 2025 to 2034. This significant growth is being driven by the increasing demand for more sustainable aviation solutions as industries and governments prioritize reducing carbon emissions and improving fuel efficiency.

Technological advancements in electric propulsion and energy storage systems are playing a pivotal role in shaping the future of hybrid aircraft. These hybrid-electric propulsion systems are designed to reduce the environmental impact of aviation by lowering carbon emissions and boosting fuel efficiency. Manufacturers are increasingly integrating these systems into regional and short-haul aircraft, with the potential for long-haul applications depending on future improvements in battery technology.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $11.2 Billion |

| CAGR | 23.4% |

The market is divided into different categories based on lift technology, including conventional take-off and landing (CTOL), short take-off and landing (STOL), and vertical take-off and landing (VTOL) aircraft. In 2024, the CTOL segment held the largest share of the market at 42.5%, and it is expected to continue growing at a strong pace. Hybrid CTOL aircraft are particularly attractive because they can utilize existing aviation infrastructure, such as runways and maintenance facilities, making them a practical and sustainable choice for the future of aviation.

The market is also segmented based on the mode of operation into piloted and autonomous aircraft. The autonomous segment is set to experience rapid growth, with a projected CAGR of 24.5% through 2034. Breakthroughs in artificial intelligence, sensor technologies, and flight automation systems are enabling aircraft to operate independently, avoid obstacles, and perform essential system checks without human intervention. This is leading to greater safety and efficiency, particularly in sectors such as cargo transport, surveillance, and disaster response, where unmanned aircraft offer cost-effective and reliable solutions.

North America is currently the dominant region in the hybrid aircraft market and is expected to continue its growth, reaching a market value of USD 5.3 billion by 2034. The United States is at the forefront of hybrid aircraft development, with a strong emphasis on sustainable aviation solutions. Major aerospace companies, alongside emerging startups, are heavily investing in electric and hybrid-electric propulsion technologies, focusing primarily on regional and short-haul hybrid aircraft. These solutions offer significant advantages in terms of fuel efficiency and reduced emissions, driving the market forward.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for eco-friendly aviation solutions

- 3.6.1.2 Growth in electric vertical takeoff and landing (eVTOL) solutions

- 3.6.1.3 Rising focus on the development of efficient hybrid engines

- 3.6.1.4 Increasing demand for improved energy storage and efficiency for hybrid-electric propulsion.

- 3.6.1.5 Growing funding from public and private sectors for hybrid aircraft research

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development costs

- 3.6.2.2 Battery limitations

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Regional transport aircraft

- 5.3 Business jets

- 5.4 Light and ultralight aircraft

- 5.5 Unmanned aerial vehicles

- 5.6 Advanced air mobility

Chapter 6 Market Estimates & Forecast, By Lift Technology, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Conventional Take-off and landing

- 6.3 Short Take-off and landing

- 6.4 Vertical Take-off and landing

Chapter 7 Market Estimates & Forecast, By Fuel Type, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Fuel hybrid

- 7.3 Hydrogen hybrid

Chapter 8 Market Estimates & Forecast, By Range, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 < 100 km

- 8.3 101 km to 500 km

- 8.4 > 501 km

Chapter 9 Market Estimates & Forecast, By Mode of Operation 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Piloted

- 9.3 Autonomous

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Airbus

- 11.2 Ampaire

- 11.3 Electric Aviation Group

- 11.4 Embraer

- 11.5 Faradair Aerospace

- 11.6 General Electric

- 11.7 Heart Aerospace

- 11.8 Pipistrel

- 11.9 RTX

- 11.10 Safran

- 11.11 Voltaero

- 11.12 XTI Aircraft

混合动力飞机市场规模、份额、成长分析及产业预测(按飞机类型、动力来源、运行模式、航程、升力技术、系统和地区)- 2025 年至 2032 年

混合动力飞机市场规模、份额、成长分析及产业预测(按飞机类型、动力来源、运行模式、航程、升力技术、系统和地区)- 2025 年至 2032 年 混合无人机市场按类型、作战范围、作战模式、有效载荷容量、组件、最终用户和最终用户产业划分——2025-2030 年全球预测混合无人机引擎市场(按引擎类型、平台整合、功率、应用和最终用途)—2025-2030 年全球预测

混合无人机市场按类型、作战范围、作战模式、有效载荷容量、组件、最终用户和最终用户产业划分——2025-2030 年全球预测混合无人机引擎市场(按引擎类型、平台整合、功率、应用和最终用途)—2025-2030 年全球预测 混合无人机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

混合无人机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球混合动力飞机市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测

全球混合动力飞机市场研究报告 - 产业分析、规模、份额、成长、趋势及 2025 年至 2033 年预测 2025年全球混合动力飞机市场报告混合动力飞机市场:按技术、按应用划分 - 2025-2030 年全球预测

2025年全球混合动力飞机市场报告混合动力飞机市场:按技术、按应用划分 - 2025-2030 年全球预测