|

市场调查报告书

商品编码

1665290

太空经济市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Space Economy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

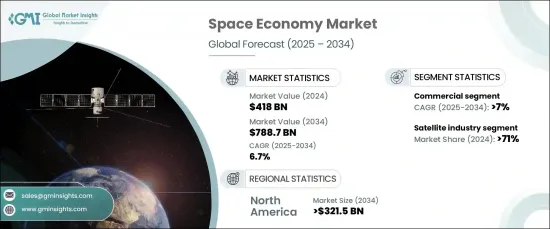

2024 年全球太空经济市场价值为 4,180 亿美元,预计将经历强劲增长,2025 年至 2034 年的复合年增长率为 6.7%。

卫星和火箭的技术创新使得进入太空变得更加容易且更具成本效益,从而推动了市场扩张。这些进步透过提供即时追踪、全球通讯和先进的天气监测等功能,使交通、物流和灾害管理等行业受益。随着企业不断整合以空间为基础的解决方案,市场将释放更多的成长和营运效率潜力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 4180亿美元 |

| 预测值 | 7,887 亿美元 |

| 复合年增长率 | 6.7% |

太空经济市场主要分为三个关键部分:卫星产业、非卫星产业和太空永续活动。 2024 年卫星产业将占据市场主导地位,占有 71% 的份额。随着电信、导航和地球观测领域对卫星服务的需求不断增长,预计这种主导地位将持续下去。公司越来越关注在低地球轨道(LEO)部署小型卫星,这对于增强全球互联网连接、收集资料和支援无缝通讯至关重要。卫星技术在农业、物流和灾难应变等各个领域也发挥着至关重要的作用,使组织能够做出数据驱动的决策,进而提高营运效率。

从最终用户来看,太空经济市场分为商业部门及政府及防务部门。预计到 2034 年,商业领域的复合年增长率将达到 7%。不断扩大的低地球轨道卫星星座正在改善网路覆盖范围和响应时间,从而实现更可靠的通讯和先进的遥感能力。这些技术突破对于缺乏传统基础设施的地区尤其有利,加速了各行业对卫星服务的采用。

预计到 2034 年,北美的太空经济市场收入将达到 3,215 亿美元。卫星部署的关键发展和发射成本的降低正在加速市场的扩张。美国继续在建立用于全球宽频服务的卫星网路、推动服务不足地区的连结性改善以及促进科技领域创新方面发挥领导作用。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 太空科技的技术进步

- 通讯、地球观测和全球定位的卫星应用激增

- 太空商业化日益发展

- 国际合作与投资不断增加

- 增加政府对太空探索的资助

- 产业陷阱与挑战

- 成本高,投资风险大

- 环境和永续性议题

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 卫星产业

- 卫星发射

- 卫星服务

- 卫星製造

- 卫星地面设备

- 非卫星产业

- 政府太空预算

- 商业载人航太

- 空间可持续性活动

第 6 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 商业的

- 政府和国防

第 7 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- AeroVironment

- Airbus

- BAE Systems

- Blue Origin

- Boeing

- Elbit Systems

- General Dynamics

- Indian Space Research Organisation

- Israel Aerospace Industries

- Lockheed Martin

- Maxar Technologies

- Northrop Grumman

- Raytheon Technologies

- SpaceX

- Thales

- Viasat

The Global Space Economy Market was valued at USD 418 billion in 2024 and is projected to experience robust growth, expanding at a CAGR of 6.7% from 2025 to 2034. This growth is driven by the increasing adoption of space technologies across various industries, which is revolutionizing operations and opening up new revenue opportunities.

Technological innovations in satellites and rockets are making space more accessible and cost-effective, fueling market expansion. These advancements are benefiting industries such as transportation, logistics, and disaster management by providing capabilities like real-time tracking, global communication, and advanced weather monitoring. As businesses continue to integrate space-based solutions, the market is poised to unlock even more potential for growth and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $418 billion |

| Forecast Value | $788.7 billion |

| CAGR | 6.7% |

The space economy market is primarily divided into three key segments: the satellite industry, the non-satellite industry, and space sustainability activities. The satellite industry dominated the market in 2024, accounting for a significant 71% share. This dominance is expected to continue as demand for satellite services in telecommunications, navigation, and Earth observation continues to rise. Companies are increasingly focusing on deploying small satellites in Low Earth Orbit (LEO), which are crucial for enhancing global internet connectivity, gathering data, and supporting seamless communication. Satellite technology also plays a vital role in various sectors, including agriculture, logistics, and disaster response, empowering organizations to make data-driven decisions that enhance operational effectiveness.

When it comes to end users, the space economy market is divided into the commercial sector and the government and defense sector. The commercial segment is projected to grow at a CAGR of 7% through 2034. This surge is driven by a growing demand for satellite-based services, particularly for global broadband and IoT connectivity. Expanding LEO satellite constellations are improving network coverage and response times, enabling more reliable communication and advanced remote sensing capabilities. These technological breakthroughs are especially beneficial for regions lacking traditional infrastructure, accelerating the adoption of satellite services across industries.

North America is expected to generate USD 321.5 billion in space economy market revenue by 2034. The U.S. is at the forefront of this growth, bolstered by substantial government funding and private-sector involvement. Key developments in satellite deployment and reduced launch costs are accelerating the expansion of the market. The U.S. continues to lead the way in building satellite networks for global broadband services, driving improved connectivity in underserved regions, and fostering innovation in the tech sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Technological advancements in space technologies

- 3.6.1.2 Surge in satellite applications for communication, Earth observation, and global positioning

- 3.6.1.3 Growing commercialization of space

- 3.6.1.4 Rising international collaboration and investments

- 3.6.1.5 Increasing government funding for space exploration

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs and investment risks

- 3.6.2.2 Environmental and sustainability issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Satellite industry

- 5.2.1 Satellite launch

- 5.2.2 Satellite services

- 5.2.3 Satellite manufacturing

- 5.2.4 Satellite ground equipment

- 5.3 Non-Satellite Industry

- 5.3.1 Government space budgets

- 5.3.2 Commercial human spaceflight

- 5.4 Space sustainability activities

Chapter 6 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Commercial

- 6.3 Government & defense

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AeroVironment

- 8.2 Airbus

- 8.3 BAE Systems

- 8.4 Blue Origin

- 8.5 Boeing

- 8.6 Elbit Systems

- 8.7 General Dynamics

- 8.8 Indian Space Research Organisation

- 8.9 Israel Aerospace Industries

- 8.10 Lockheed Martin

- 8.11 Maxar Technologies

- 8.12 Northrop Grumman

- 8.13 Raytheon Technologies

- 8.14 SpaceX

- 8.15 Thales

- 8.16 Viasat