|

市场调查报告书

商品编码

1665352

汽车动能回收系统 (KERS) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Kinetic Energy Recovery System (KERS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

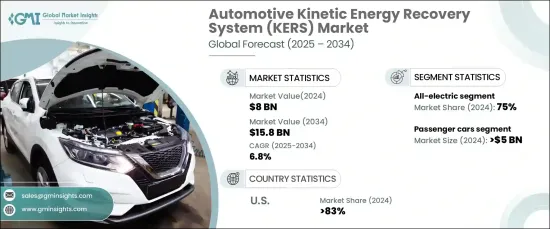

2024 年全球汽车动能回收系统市场价值为 80 亿美元,预计 2025 年至 2034 年的复合年增长率为 6.8%。这项创新技术最大限度地减少了对传统燃料的依赖,与全球永续发展目标完美契合。汽车製造商越来越多地将 KERS 纳入混合动力和电动车中,以增强节能效果、提升性能并确保符合严格的排放标准。

城市化进程的加速和智慧城市计画的兴起正在推动对生态友善交通解决方案的需求。 KERS 正在成为城市交通的基石,优化了大都市中常见的走走停停交通中的能源使用。对电动车基础设施和公共交通系统电气化的投资不断增加,进一步推动了 KERS 技术的应用。这使得 KERS 成为永续城市交通系统不可或缺的一部分,促进全球市场成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 80亿美元 |

| 预测值 | 158亿美元 |

| 复合年增长率 | 6.8% |

根据车辆类型,市场分为商用车和乘用车。 2024 年,乘用车将占据市场主导地位,创造 50 亿美元的收入。这种领先地位归功于混合动力和电动技术在乘用车中的广泛应用,其中 KERS 显着提高了燃油效率并减少了排放。消费者对环境可持续和节能的交通解决方案的偏好日益增长,这继续扩大了对配备 KERS 的车辆的需求,从而推动了市场的扩张。

根据推进方式,市场进一步分为全电动、PHEV、HEV 和 FCEV。受益于与能量回收系统的无缝集成,全电动领域在 2024 年占据 75% 的份额。 KERS 透过捕捉和重复利用煞车能量,在提高能源效率方面发挥关键作用,从而延长了电动车的行驶里程。政府对电动车应用的支持性激励措施,加上严格的排放法规,正在加强 KERS 技术的应用。轻量化零件的进步也促进了全电动推进系统日益占据主导地位。

在混合动力和电动车普及的强劲推动下,美国汽车动能回收系统 (KERS) 市场将在 2024 年占据令人印象深刻的 83% 的份额。更严格的排放标准和燃油经济法规正在鼓励汽车製造商实施 KERS 等节能技术。联邦激励措施和对永续创新的大量投资进一步加速了市场成长。凭藉强大的研发基础设施和领先汽车製造商的高度集中,美国继续引领 KERS 技术进步,巩固其全球市场领先地位。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- 原物料供应商

- 零件供应商

- 製造商

- 服务提供者

- 经销商

- 最终用途

- 利润率分析

- 定价分析

- 成本明细分析

- 技术与创新格局

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 严格的排放法规推动了采用

- 混合动力汽车和电动车的整合度不断提高

- 轻质材料的进步提高了效率

- 更加重视燃油效率和永续性

- 产业陷阱与挑战

- 先进KERS技术成本高昂

- 低成本汽车领域采用有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 其他的

- 商用车

- 轻型

- 中型

- 重负

第六章:市场估计与预测:按系统,2021 - 2034 年

- 主要趋势

- 飞轮

- 电池

- 超级电容器

第 7 章:市场估计与预测:按推进方式,2021 - 2034 年

- 主要趋势

- 全电动

- 插电式混合动力汽车

- 油电混合车

- 燃料电池汽车

第 8 章:市场估计与预测:按 KERS,2021 - 2034 年

- 主要趋势

- 机械的

- 机电

- 油压

- 电子的

第 9 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 东南亚

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东及非洲

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- Advics

- Aisin

- Bosch

- Brembo

- Continental

- Denso

- Haldex

- Hitachi Astemo

- Hyundai Mobis

- Magna International

- Mando

- Nidec

- PHINIA

- Schaeffler

- Skeleton Technologies

- Tenneco

- Torotrak

- TRW Automotive

- Valeo

- ZF Friedrichshafen

The Global Automotive Kinetic Energy Recovery System Market was valued at USD 8 billion in 2024 and is projected to grow at a CAGR of 6.8% from 2025 to 2034. The integration of KERS with regenerative braking systems is revolutionizing energy efficiency in vehicles by converting braking energy into reusable power. This innovative technology minimizes reliance on conventional fuels, aligning seamlessly with global sustainability goals. Automakers are increasingly incorporating KERS into hybrid and electric vehicles, enhancing energy savings, boosting performance, and ensuring compliance with stringent emission standards.

The surge in urbanization and the rise of smart city initiatives are fueling demand for eco-friendly transportation solutions. KERS is emerging as a cornerstone of urban mobility, optimizing energy use in stop-and-go traffic common in metropolitan areas. The growing investments in electric mobility infrastructure and the electrification of public transit systems are further propelling the adoption of KERS technology. This positions KERS as an indispensable component of sustainable urban transportation systems, catalyzing global market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8 Billion |

| Forecast Value | $15.8 Billion |

| CAGR | 6.8% |

By vehicle type, the market is segmented into commercial vehicles and passenger cars. Passenger cars dominated the market in 2024, generating USD 5 billion in revenue. This leadership is attributed to the widespread adoption of hybrid and electric technologies in passenger vehicles, where KERS significantly enhances fuel efficiency and reduces emissions. The growing consumer preference for environmentally sustainable and energy-efficient transportation solutions continues to amplify demand for KERS-equipped vehicles, driving the market's expansion.

The market is further categorized by propulsion into all-electric, PHEV, HEV, and FCEV. The all-electric segment held a commanding 75% share in 2024, benefiting from seamless integration with energy recovery systems. KERS plays a pivotal role in improving energy efficiency by capturing and reusing braking energy, which extends the driving range of electric vehicles. Supportive government incentives for EV adoption, coupled with stringent emission regulations, are reinforcing the adoption of KERS technology. Advancements in lightweight components are also contributing to the growing dominance of all-electric propulsion systems.

The U.S. automotive kinetic energy recovery system (KERS) market accounted for an impressive 83% share in 2024, driven by a strong commitment to hybrid and electric vehicle adoption. Stricter emission standards and fuel economy regulations are encouraging automakers to implement energy-efficient technologies like KERS. Federal incentives and substantial investments in sustainable innovations are further accelerating market growth. With a robust research and development infrastructure and a high concentration of leading automakers, the U.S. continues to lead advancements in KERS technology, solidifying its position as a global market leader.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component supplier

- 3.2.3 Manufacturer

- 3.2.4 Service provider

- 3.2.5 Distributor

- 3.2.6 End-use

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Cost breakdown analysis

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Adoption driven by stringent emission regulations

- 3.9.1.2 Rising integration in hybrid and electric vehicles

- 3.9.1.3 Advancements in lightweight materials for better efficiency

- 3.9.1.4 Increasing focus on fuel efficiency and sustainability

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High costs associated with advanced KERS technologies

- 3.9.2.2 Limited adoption in low-cost vehicle segments

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.2.4 Others

- 5.3 Commercial vehicle

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By System, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Flywheel

- 6.3 Battery

- 6.4 Super capacitor

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 All-electric

- 7.3 PHEV

- 7.4 HEV

- 7.5 FCEV

Chapter 8 Market Estimates & Forecast, By KERS, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mechanical

- 8.3 Electro-mechanical

- 8.4 Hydraulic

- 8.5 Electronic

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Argentina

- 9.5.3 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Advics

- 10.2 Aisin

- 10.3 Bosch

- 10.4 Brembo

- 10.5 Continental

- 10.6 Denso

- 10.7 Haldex

- 10.8 Hitachi Astemo

- 10.9 Hyundai Mobis

- 10.10 Magna International

- 10.11 Mando

- 10.12 Nidec

- 10.13 PHINIA

- 10.14 Schaeffler

- 10.15 Skeleton Technologies

- 10.16 Tenneco

- 10.17 Torotrak

- 10.18 TRW Automotive

- 10.19 Valeo

- 10.20 ZF Friedrichshafen

动能回收健身器材市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、安装类型、设备及解决方案划分动能撷取穿戴式装置市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材质、设备、功能及安装类型划分

动能回收健身器材市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、最终用户、安装类型、设备及解决方案划分动能撷取穿戴式装置市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材质、设备、功能及安装类型划分 新能源汽车一体化马达控制单元市场(按马达类型、车辆类型、额定功率、整合度和应用划分)-2026年至2032年全球预测

新能源汽车一体化马达控制单元市场(按马达类型、车辆类型、额定功率、整合度和应用划分)-2026年至2032年全球预测 汽车能源回收系统市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车能源回收系统市场机会、成长要素、产业趋势分析及2026年至2035年预测 能源回收技术市场-全球产业规模、份额、趋势、机会及预测(依技术、能源来源、最终用户、地区及竞争细分,2020-2030 年)

能源回收技术市场-全球产业规模、份额、趋势、机会及预测(依技术、能源来源、最终用户、地区及竞争细分,2020-2030 年) 2032 年动能开关市场预测:按产品类型、工作范围、频率范围、技术、应用、最终用户和地区进行的全球分析

2032 年动能开关市场预测:按产品类型、工作范围、频率范围、技术、应用、最终用户和地区进行的全球分析 全球汽车能量回收系统市场规模、份额、产业分析报告(按推进系统、子系统、车辆、地区、展望和预测),2025 年至 2032 年

全球汽车能量回收系统市场规模、份额、产业分析报告(按推进系统、子系统、车辆、地区、展望和预测),2025 年至 2032 年 2025年全球汽车能量回收系统市场报告动能回收系统市场分析与预测(至 2034 年):类型、产品、服务、技术、组件、应用、最终用户、功能

2025年全球汽车能量回收系统市场报告动能回收系统市场分析与预测(至 2034 年):类型、产品、服务、技术、组件、应用、最终用户、功能 汽车动能回收系统市场,按产品类型、按应用、按车辆类型、按组件、按推进类型、按国家和地区 - 2025 年至 2032 年的全球行业分析、市场规模、市场份额和预测

汽车动能回收系统市场,按产品类型、按应用、按车辆类型、按组件、按推进类型、按国家和地区 - 2025 年至 2032 年的全球行业分析、市场规模、市场份额和预测