|

市场调查报告书

商品编码

1665403

智慧尾门市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Smart Tailgate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

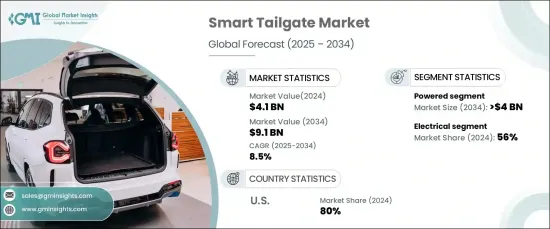

2024 年全球智慧尾门市场价值为 41 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 8.5%。汽车製造商正在不断增强车辆介面以融入创新技术。具有自动开启和关闭功能的智慧尾门系统可提供免持功能,这对于管理重物的使用者特别有用。强调使用者友善、技术先进的解决方案符合消费者对现代车辆更大便利性的偏好。

此外,SUV和跨界车等大型车辆的日益普及,大大推动了智慧尾门的普及。安全性和安保功能的增强也推动了市场的成长,因为这些系统透过整合感测器来检测障碍物,从而降低了受伤或损坏的风险。车辆安全功能的不断发展凸显了这些技术在提高功能性和使用者满意度方面的重要性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 41亿美元 |

| 预测值 | 91亿美元 |

| 复合年增长率 | 8.5% |

该市场分为手动、电动和免持三种选择,其中电动部分将在 2024 年占据超过 50% 的市场份额。电动智慧尾门与车辆的整合体现了汽车製造商为满足不断变化的期望和增强竞争优势而做出的努力。

智慧尾门的机制包括电动系统、液压系统和气动系统。受消费者对易于操作和节能解决方案的需求推动,电气系统在 2024 年占据了 56% 的市场份额。这些系统透过按钮操作开启和关闭等功能简化了后挡板控制。无缝、无线操作提高了效率和可及性,同时也满足了人们对智慧、环保汽车日益增长的偏好。无钥匙进入和遥控器等先进技术的加入进一步提高了使用者的便利性,增强了电动智慧尾门系统的吸引力。

在北美,美国在区域智慧尾门市场占据主导地位,2024 年的份额高达 80%。消费者在购买汽车时优先考虑的是便利性和安全性,因此智慧尾门成为一种有价值的附加功能。这些系统方便人们轻鬆进入后车箱,满足旅途中个人的需求。户外生活方式和长途公路旅行的转变继续推动智慧尾门系统在该地区的普及。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 零件供应商

- 製造商

- 配销通路

- 最终用户

- 供应商概况

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻及倡议

- 监管格局

- 成本分析

- 衝击力

- 成长动力

- 提高车辆舒适性

- 消费者对便利性的期望不断提高

- 车辆技术进步

- 不断成长的豪华汽车市场

- 产业陷阱与挑战

- 製造成本高

- 技术复杂性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按供应量,2021 - 2034 年

- 主要趋势

- 手动的

- 供电

- 免持

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 掀背车

- 轿车

- SUV

第 7 章:市场估计与预测:按机制,2021 - 2034 年

- 主要趋势

- 电力

- 油压

- 气动

第 8 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳新银行

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第九章:公司简介

- Aisin Seiki

- Aptiv

- Bosch

- Brose

- Continental

- Ficosa

- Hella

- Huf Holding

- Johnson

- Kiekert

- Lear

- Magna

- Mitsuba

- Stabilus

- Zhejiang

The Global Smart Tailgate Market, valued at USD 4.1 billion in 2024, is projected to grow at a CAGR of 8.5% from 2025 to 2034. This expansion is largely driven by the increasing demand for advanced in-vehicle automation and convenience features. Automotive manufacturers are continuously enhancing vehicle interfaces to incorporate innovative technologies. Smart tailgate systems with automated opening and closing functions offer hands-free access, making them particularly useful for users managing heavy loads. The emphasis on user-friendly, tech-forward solutions aligns with consumer preferences for greater convenience in modern vehicles.

Additionally, the rising popularity of larger vehicles, such as SUVs and crossovers, has significantly boosted the adoption of smart tailgates. Safety and security enhancements also propel market growth, as these systems reduce the risk of injury or damage by integrating sensors to detect obstacles. The ongoing evolution of vehicle safety features highlights the importance of these technologies in improving functionality and user satisfaction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 8.5% |

The market, segmented by offering into manual, powered, and hands-free options, saw the powered segment dominate with over 50% of the market share in 2024. By 2034, this segment is anticipated to surpass USD 4 billion, reflecting the growing consumer appetite for convenient, high-tech vehicle features. The integration of powered smart tailgates into vehicles demonstrates automakers' efforts to meet evolving expectations and enhance their competitive edge.

Mechanisms for smart tailgates include electrical, hydraulic, and pneumatic systems. Electrical systems held a 56% market share in 2024, driven by consumer demand for easily operable and energy-efficient solutions. These systems simplify tailgate control with features like button-operated opening and closing. The seamless, cordless operation improves efficiency and accessibility while aligning with the growing preference for smart, eco-friendly vehicles. The incorporation of advanced technologies like keyless entry and remote control further enhances user convenience and reinforces the appeal of electrical smart tailgate systems.

In North America, the United States dominated the regional smart tailgate market with an impressive 80% share in 2024. The rise in outdoor recreational activities, including camping and road trips, has led to increased demand for vehicles equipped with advanced features. Consumers prioritize convenience and safety when purchasing vehicles, making smart tailgates a valuable addition. These systems facilitate effortless access to the trunk, catering to the needs of individuals on the go. The shift towards outdoor-oriented lifestyles and longer road trips continues to drive the penetration of smart tailgate systems across the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Distribution channel

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing vehicle comfort features

- 3.9.1.2 Rising consumer convenience expectations

- 3.9.1.3 Technological advancements in vehicles

- 3.9.1.4 Growing automotive luxury segment

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High manufacturing costs

- 3.9.2.2 Technical complexity

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Powered

- 5.4 Hands-Free

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Hatchback

- 6.3 Sedan

- 6.4 SUVs

Chapter 7 Market Estimates & Forecast, By Mechanism, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Electrical

- 7.3 Hydraulic

- 7.4 Pneumatic

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 ANZ

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Aisin Seiki

- 9.2 Aptiv

- 9.3 Bosch

- 9.4 Brose

- 9.5 Continental

- 9.6 Ficosa

- 9.7 Hella

- 9.8 Huf Holding

- 9.9 Johnson

- 9.10 Kiekert

- 9.11 Lear

- 9.12 Magna

- 9.13 Mitsuba

- 9.14 Stabilus

- 9.15 Zhejiang

碳纤维传动轴市场规模、份额和成长分析:按类型、材质、应用、製造流程、终端用户产业和地区划分-2026-2033年产业预测

碳纤维传动轴市场规模、份额和成长分析:按类型、材质、应用、製造流程、终端用户产业和地区划分-2026-2033年产业预测 碳纤维引擎盖市场规模、份额和成长分析:按产品类型、材质类型、车辆类型、製造流程、分销管道和地区划分-2026-2033年产业预测

碳纤维引擎盖市场规模、份额和成长分析:按产品类型、材质类型、车辆类型、製造流程、分销管道和地区划分-2026-2033年产业预测 碳纤维扰流板市场规模、份额和成长分析:按产品类型、车辆类型、最终用户、销售管道、价格范围和地区划分-2026-2033年产业预测

碳纤维扰流板市场规模、份额和成长分析:按产品类型、车辆类型、最终用户、销售管道、价格范围和地区划分-2026-2033年产业预测 2026-2034年全球汽车用碳纤维热塑性塑胶市场规模、份额、趋势及成长分析报告

2026-2034年全球汽车用碳纤维热塑性塑胶市场规模、份额、趋势及成长分析报告 全球汽车碳纤维传动轴市场(按车辆类型、动力类型、传动系统、轴设计和分销管道划分)预测(2026-2032年)汽车预浸料市场:按树脂类型、纤维类型、製程、产品形式、应用和车辆类型划分-2026-2032年全球预测

全球汽车碳纤维传动轴市场(按车辆类型、动力类型、传动系统、轴设计和分销管道划分)预测(2026-2032年)汽车预浸料市场:按树脂类型、纤维类型、製程、产品形式、应用和车辆类型划分-2026-2032年全球预测 汽车碳纤维复合材料市场规模、份额及成长分析(按产品、製造流程、应用、最终用户及地区划分)-2026-2033年产业预测

汽车碳纤维复合材料市场规模、份额及成长分析(按产品、製造流程、应用、最终用户及地区划分)-2026-2033年产业预测 全球汽车酰胺纤维市场按类型、应用和地区划分-预测至2030年汽车碳纤维市场(按应用、车型、原料和纤维等级)—2025-2032 年全球预测

全球汽车酰胺纤维市场按类型、应用和地区划分-预测至2030年汽车碳纤维市场(按应用、车型、原料和纤维等级)—2025-2032 年全球预测 2025年全球汽车碳纤维复合材料零件市场报告

2025年全球汽车碳纤维复合材料零件市场报告