|

市场调查报告书

商品编码

1666619

无人交通管理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Unmanned Traffic Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

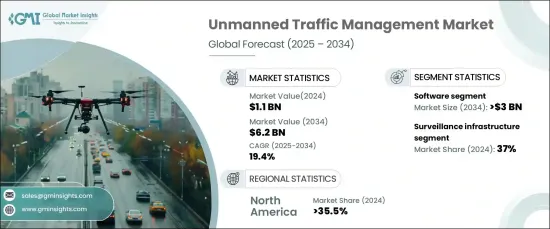

2024 年全球无人交通管理市场规模达到 11 亿美元,预计 2025 年至 2034 年期间将以 19.4% 的强劲复合年增长率成长。随着无人机成为这些领域运作不可或缺的一部分,对先进空中交通管理系统的需求激增,以确保无人机安全且有效率地融入共享空域。随着城市地区越来越多地采用无人机进行最后一英里的配送和智慧城市应用,其营运管理变得更加复杂,需要可扩展且可靠的 UTM 解决方案。

此外,不断变化的法规和对无人机技术不断增加的投资正在催化市场的扩张。政府和私人组织正在合作建立无人机(UAV)运作框架,促进该领域的创新和发展。在解决空域拥塞挑战的同时,专注于提高安全性和效率,预计将进一步推动市场发展。无人机相关技术的不断进步,包括延长电池寿命、提高有效载荷能力和即时监控系统,正在塑造 UTM 系统的未来。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 11亿美元 |

| 预测值 | 62亿美元 |

| 复合年增长率 | 19.4% |

市场的成长也受到突破性技术进步的支持。自主飞行系统、增强型感测器、人工智慧 (AI) 驱动的决策和下一代通讯网路的创新正在显着提高无人机的能力。这些发展不仅简化了无人机的操作,而且迫切需要强大的 UTM 解决方案,以确保遵守不断发展的航空标准,同时保持安全和营运效率。

UTM 市场大致分为硬体、软体和服务。软体在2024 年成为主导领域,占据 48% 的市场份额,预计到 2034 年将创造 30 亿美元的市场价值。这些系统在确保法规合规、追踪无人机交通以及促进无人机和空中交通管制之间的安全通讯方面发挥关键作用。软体解决方案的不可或缺性使这一领域成为市场成长的主要驱动力。

根据应用,市场分为导航基础设施、监控基础设施、通讯基础设施和其他类别。 2024 年,监控基础设施占据了 37% 的市场份额。先进的监视系统对于防止碰撞、缓解空域拥塞和确保共享空域的顺利运作至关重要。

从地区来看,北美 UTM 市场占据主导地位,到 2024 年将占有 35.5% 的份额,这得益于该地区的技术领导地位、支持性监管框架以及无人机技术的早期采用。美国是商业和政府无人机营运的全球领导者,在推动 UTM 解决方案方面发挥关键作用。该地区积极主动地将无人机纳入国家领空,巩固了其在全球市场的重要参与者地位。

目录

第 1 章:方法论与范围

- 研究设计

- 研究部分

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- UTM解决方案供应商

- 无人机製造商和营运商

- 电信和连接供应商

- 数据分析和云端服务供应商

- 导航和感测器技术供应商

- 最终用途

- 利润率分析

- 技术与创新格局

- 使用案例

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 城市空中交通的成长

- UTM 系统的技术进步

- 改善监管框架和标准

- 公共和私营部门对无人机领域的投资不断增加

- 高效率交通管理的需求

- 产业陷阱与挑战

- 隐私和安全问题

- 实施成本高

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第六章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 执着的

- 非持久性

第 7 章:市场估计与预测:按部署,2021 - 2034 年

- 主要趋势

- 本地

- 云

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 导航基础设施

- 监控基础设施

- 通讯基础设施

- 其他的

第 9 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 商业的

- 政府

- 私人的

第 10 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Aeris

- Airbus

- Airspace Link

- Altitude Angel

- Anra Technologies

- DroneUp

- Droniq

- Frequentis

- InnovATM

- L3Harris Technologies

- Leonardo

- Lockheed Martin

- Onesky Technology

- PrecisionHawk

- Terra Drone

- Thales

- Unifly

- Unmanned Experts

The Global Unmanned Traffic Management Market reached USD 1.1 billion in 2024 and is projected to grow at a robust CAGR of 19.4% from 2025 to 2034. This impressive growth trajectory is primarily fueled by the rapid adoption of drones across diverse industries such as delivery, agriculture, and surveillance. With drones becoming an integral part of operations in these sectors, the need for advanced air traffic management systems has surged to ensure safe and efficient drone integration into shared airspace. As urban areas increasingly adopt drones for last-mile deliveries and smart city applications, managing their operations has grown more complex, necessitating scalable and reliable UTM solutions.

Furthermore, evolving regulations and increasing investments in drone technology are catalyzing the market's expansion. Governments and private organizations are collaborating to establish frameworks for unmanned aerial vehicle (UAV) operations, fostering innovation and development in the sector. The focus on enhancing safety and efficiency while addressing the challenges of airspace congestion is expected to further drive the market. The ongoing advancements in drone-related technologies, including improved battery life, payload capacity, and real-time monitoring systems, are shaping the future of UTM systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 19.4% |

The market growth is also underpinned by groundbreaking technological advancements. Innovations in autonomous flight systems, enhanced sensors, artificial intelligence (AI)-driven decision-making, and next-generation communication networks are significantly improving drone capabilities. These developments are not only streamlining drone operations but are also creating a pressing need for robust UTM solutions to ensure compliance with evolving aviation standards while maintaining safety and operational efficiency.

The UTM market is broadly categorized into hardware, software, and services. Software emerged as the dominant segment in 2024, capturing 48% of the market share, and is anticipated to generate USD 3 billion by 2034. Software forms the backbone of the UTM ecosystem, enabling seamless management of drone operations through efficient flight path optimization and real-time data processing. These systems play a critical role in ensuring regulatory compliance, tracking drone traffic, and facilitating secure communication between drones and air traffic control. The indispensable nature of software solutions positions this segment as a key driver of market growth.

In terms of application, the market is segmented into navigation infrastructure, surveillance infrastructure, communication infrastructure, and other categories. Surveillance infrastructure accounted for 37% of the market share in 2024. This segment is essential for maintaining safety and efficiency, particularly as drone operations increase in densely populated urban environments. Advanced surveillance systems are crucial for preventing collisions, mitigating airspace congestion, and ensuring smooth operations in shared airspace.

Regionally, the North American UTM market dominated with a 35.5% share in 2024, driven by the region's technological leadership, supportive regulatory framework, and early adoption of drone technologies. The United States, a global leader in commercial and governmental drone operations, has played a pivotal role in advancing UTM solutions. The region's proactive approach to integrating drones into national airspace has cemented its position as a key player in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research Component

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360º synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 UTM solution providers

- 3.2.2 Drone manufacturers and operators

- 3.2.3 Telecommunication and connectivity providers

- 3.2.4 Data analytics and cloud service providers

- 3.2.5 Navigation and sensor technology providers

- 3.2.6 End Use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Use cases

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Growth of urban air mobility

- 3.8.1.2 Technological advancements in UTM systems

- 3.8.1.3 Improving regulatory frameworks and standards

- 3.8.1.4 Rising public and private sector investments in drone sector

- 3.8.1.5 Demand for efficient traffic management

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Privacy and security concerns

- 3.8.2.2 High implementation costs

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Persistent

- 6.3 Non-persistent

Chapter 7 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 On-premise

- 7.3 Cloud

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Navigation infrastructure

- 8.3 Surveillance infrastructure

- 8.4 Communication infrastructure

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Commercial

- 9.3 Government

- 9.4 Private

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aeris

- 11.2 Airbus

- 11.3 Airspace Link

- 11.4 Altitude Angel

- 11.5 Anra Technologies

- 11.6 DroneUp

- 11.7 Droniq

- 11.8 Frequentis

- 11.9 InnovATM

- 11.10 L3Harris Technologies

- 11.11 Leonardo

- 11.12 Lockheed Martin

- 11.13 Onesky Technology

- 11.14 PrecisionHawk

- 11.15 Terra Drone

- 11.16 Thales

- 11.17 Unifly

- 11.18 Unmanned Experts