|

市场调查报告书

商品编码

1666916

陶瓷基复合材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Ceramic Matrix Composites Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

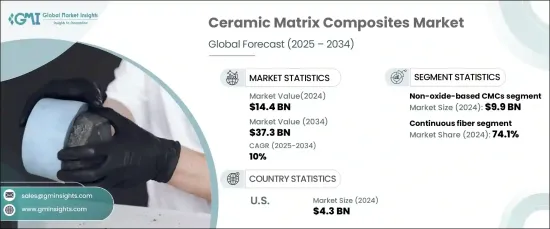

全球陶瓷基复合材料市场正在经历强劲增长,到 2024 年将达到 144 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 10%。 陶瓷基复合材料因其出色的强度重量比、优异的耐高温性和无与伦比的耐用性而正在彻底改变行业。这些先进的材料在极端条件下的性能至关重要的应用中是不可或缺的,包括航太、国防和能源领域。人们越来越重视传统金属和合金的轻质、高强度替代品,这使得 CMC 成为提高燃油效率和减少碳排放的关键组成部分。它们在各种应用领域的广泛应用凸显了它们在现代工程和技术中的重要性。

航太和国防工业是 CMC 需求的最前沿,依靠这些材料来製造涡轮叶片、排气系统以及飞机和太空船的结构加固等高性能零件。随着全球提高燃油效率和实现永续发展目标的努力不断加强,CMC的独特性能使其成为必不可少的材料选择。它们能够显着减轻重量,同时保持卓越的机械强度和耐热性,确保满足尖端航空航天技术的严格要求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 144亿美元 |

| 预测值 | 373亿美元 |

| 复合年增长率 | 10% |

从基质材料来看,CMC市场又分为氧化物基复合材料和非氧化物基复合材料。非氧化物基 CMC 占据市场主导地位,2024 年创造 99 亿美元的收入。这些特性使它们在航太、汽车和能源等行业特别有价值,这些行业中的材料必须承受极端条件而不影响性能。

按纤维类型细分的市场显示出对连续纤维增强陶瓷基复合材料(CF-CMC)的强烈偏好,占了 74.1% 的市场份额。 CF-CMC因其优异的强度、热稳定性和抗损伤能力而备受追捧。透过在陶瓷基体中嵌入连续纤维(陶瓷或碳),这些复合材料具有无与伦比的抵抗热衝击和机械应力的能力。这种弹性使 CF-CMC 成为高性能应用的首选材料,包括先进的推进系统和关键行业的结构部件。

美国引领北美陶瓷基复合材料市场,2024 年的收入航太43 亿美元。航空、能源等产业对轻质、高强度材料的需求不断增长,确保美国市场在 CMC 技术创新和应用方面始终处于领先地位。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 航太和国防领域需求旺盛

- 轻量化汽车零件日益受到关注

- 再生能源应用的成长

- 产业陷阱与挑战

- 生产和材料成本高

- 来自替代复合材料的竞争

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场规模及预测:依基质材料,2021-2034 年

- 主要趋势

- 氧化物基 CMC

- 非氧化物基 CMC

第 6 章:市场规模与预测:依纤维类型,2021-2034 年

- 主要趋势

- 连续纤维

- 不连续/碳化硅晶须

第 7 章:市场规模与预测:依最终用途,2021-2034 年

- 主要趋势

- 航太和国防

- 汽车

- 能源与电力

- 工业的

- 其他的

第 8 章:市场规模与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Applied Thin Films, Inc.

- CeramTec GmbH

- COI Ceramics, Inc.

- CoorsTek, Inc.

- General Electric Company

- Kyocera Corporation

- Lancer Systems

- Morgan Advanced Materials

- Reinhold Industries, Inc.

- Renegade Materials Corporation

- Rolls-Royce plc

The Global Ceramic Matrix Composites Market is experiencing robust growth, reaching USD 14.4 billion in 2024, with projections to expand at a CAGR of 10% from 2025 to 2034. Ceramic matrix composites are revolutionizing industries due to their exceptional strength-to-weight ratio, superior high-temperature tolerance, and unparalleled durability. These advanced materials are indispensable in applications where performance under extreme conditions is paramount, including aerospace, defense, and energy sectors. The increasing emphasis on lightweight, high-strength alternatives to traditional metals and alloys has positioned CMCs as a critical component in the quest for greater fuel efficiency and reduced carbon emissions. Their growing adoption across a diverse range of applications underscores their importance in modern engineering and technology.

The aerospace and defense industries are at the forefront of CMC demand, relying on these materials for high-performance components such as turbine blades, exhaust systems, and structural reinforcements for aircraft and spacecraft. As global efforts to enhance fuel efficiency and achieve sustainability targets intensify, the unique properties of CMCs have made them an essential material choice. Their ability to significantly reduce weight while maintaining superior mechanical strength and thermal resistance ensures they meet the stringent requirements of cutting-edge aviation and space technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.4 Billion |

| Forecast Value | $37.3 Billion |

| CAGR | 10% |

In terms of matrix materials, the CMC market is divided into oxide-based and non-oxide-based composites. Non-oxide-based CMCs dominate the market, generating USD 9.9 billion in revenue in 2024. These composites, predominantly comprising silicon carbide (SiC) and carbon, are celebrated for their remarkable mechanical intensity, thermal resistivity, and wear properties. These attributes make them particularly valuable in industries such as aerospace, automotive, and energy, where materials must endure extreme conditions without compromising performance.

The market segmentation by fiber type reveals a strong preference for continuous fiber-reinforced ceramic matrix composites (CF-CMCs), which account for 74.1% of the market share. CF-CMCs are highly sought after due to their superior strength, thermal stability, and damage tolerance. By embedding continuous fibers, either ceramic or carbon, within the ceramic matrix, these composites deliver unmatched resistance to thermal shocks and mechanical stresses. This resilience positions CF-CMCs as the material of choice for high-performance applications, including advanced propulsion systems and structural components in critical industries.

The U.S. leads the North American ceramic matrix composites market, generating USD 4.3 billion in revenue in 2024. The country's dominance stems from its robust aerospace and defense sectors, substantial R&D investments, and the presence of major manufacturers. The increasing demand for lightweight, high-strength materials across industries like aviation and energy ensures that the U.S. market remains at the forefront of innovation and adoption in CMC technology.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 High demand in aerospace and defense

- 3.6.1.2 Rising focus on lightweight automotive components

- 3.6.1.3 Growth in renewable energy applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production and material costs

- 3.6.2.2 Competition from alternative composite materials

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Matrix Material, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Oxide-based CMCs

- 5.3 Non-oxide-based CMCs

Chapter 6 Market Size and Forecast, By Fiber Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 continuous fiber

- 6.3 Discontinuous/SiC whisker

Chapter 7 Market Size and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Aerospace & defense

- 7.3 Automotive

- 7.4 Energy & power

- 7.5 Industrial

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Applied Thin Films, Inc.

- 9.2 CeramTec GmbH

- 9.3 COI Ceramics, Inc.

- 9.4 CoorsTek, Inc.

- 9.5 General Electric Company

- 9.6 Kyocera Corporation

- 9.7 Lancer Systems

- 9.8 Morgan Advanced Materials

- 9.9 Reinhold Industries, Inc.

- 9.10 Renegade Materials Corporation

- 9.11 Rolls-Royce plc

陶瓷基复合材料 (CMC) 市场(按基质类型、增强类型、製造技术、应用、最终用途行业和分销渠道)- 全球预测,2025-2032 年

陶瓷基复合材料 (CMC) 市场(按基质类型、增强类型、製造技术、应用、最终用途行业和分销渠道)- 全球预测,2025-2032 年 全球陶瓷基复合材料市场(按纤维类型、纤维材料、基体类型、最终用途行业和地区划分)- 预测至 2030 年

全球陶瓷基复合材料市场(按纤维类型、纤维材料、基体类型、最终用途行业和地区划分)- 预测至 2030 年 2025年陶瓷基复合材料全球市场报告

2025年陶瓷基复合材料全球市场报告 全球陶瓷基复合材料市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球陶瓷基复合材料市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 陶瓷基复合材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030)

陶瓷基复合材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030) 日本陶瓷基复合材料市场报告(依复合材料类型、纤维类型、纤维材料、应用和地区)2025-2033

日本陶瓷基复合材料市场报告(依复合材料类型、纤维类型、纤维材料、应用和地区)2025-2033 压电陶瓷复合材料市场报告:趋势、预测与竞争分析(至2031年)

压电陶瓷复合材料市场报告:趋势、预测与竞争分析(至2031年) 陶瓷基复合材料市场规模、份额、趋势分析报告:按产品、应用、地区、细分市场、预测,2025-2030 年2025 年至 2033 年陶瓷基复合材料市场(按复合材料类型、纤维类型、纤维材料、应用和地区划分)

陶瓷基复合材料市场规模、份额、趋势分析报告:按产品、应用、地区、细分市场、预测,2025-2030 年2025 年至 2033 年陶瓷基复合材料市场(按复合材料类型、纤维类型、纤维材料、应用和地区划分) 陶瓷基质材料市场规模、份额和增长分析(按纤维类型、基体类型、纤维材料、最终用途行业和地区)- 行业预测 2025-2032

陶瓷基质材料市场规模、份额和增长分析(按纤维类型、基体类型、纤维材料、最终用途行业和地区)- 行业预测 2025-2032