|

市场调查报告书

商品编码

1666917

皮肤病学设备市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Dermatology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

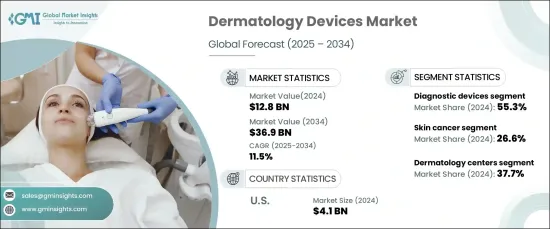

2024 年全球皮肤病设备市场价值为 128 亿美元,预计 2025 年至 2034 年期间复合年增长率将达到 11.5%。此外,皮肤病学设备的技术进步在该市场的扩张中发挥关键作用,而已开发地区对美容手术的需求日益增加。随着消费者继续重视皮肤健康和美容治疗,市场将持续成长。

市场分为诊断和治疗设备,它们在解决全球日益增多的皮肤相关健康问题方面发挥关键作用。诊断设备对于早期和准确的检测至关重要,包括影像系统、皮肤镜和活检工具。同时,治疗设备包括光疗系统、雷射、微晶换肤仪、冷冻疗法工具、电外科设备和抽脂设备。 2024年,诊断设备占据市场主导地位,占总份额的55.3%。这是因为人们越来越需要及时识别湿疹和皮肤癌等疾病,因为早期发现是成功治疗的关键。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 128亿美元 |

| 预测值 | 369亿美元 |

| 复合年增长率 | 11.5% |

在应用方面,皮肤科设备广泛应用于治疗皮肤癌、皮肤嫩肤、除毛、身体塑形、牛皮癣和其他各种皮肤病。 2024 年,皮肤癌领域占据市场主导地位,占 26.6% 的显着份额。这是由于全球皮肤癌病例的增加,推动了对可靠的诊断和治疗工具的需求。先进的皮肤病学设备对于识别癌症和癌前病变至关重要,有助于早期介入并改善患者的治疗效果。

美国皮肤科设备市场规模到 2024 年将达到 41 亿美元,仍是全球最大的皮肤科设备市场。这种主导地位是由于美国黑色素瘤和非黑色素瘤皮肤癌的高发生率,加上广泛的宣传计划和皮肤癌预防措施。此外,美国FDA批准先进的皮肤病学设备,增强了尖端诊断和治疗解决方案的可用性,促进了市场的持续成长和创新。随着皮肤病护理需求的日益加剧,美国仍将在这个快速扩张的市场中发挥关键作用。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球皮肤相关疾病和皮肤癌发生率不断上升

- 发展中国家皮肤护理支出增加

- 护肤设备的技术进步

- 已开发国家对整容手术的需求不断增长

- 产业陷阱与挑战

- 设备成本过高

- 严格的监管环境

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 专利分析

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略展望

第 5 章:市场估计与预测:按产品类型,2021 年至 2034 年

- 主要趋势

- 诊断设备

- 影像设备

- 皮肤镜

- 切片设备

- 治疗设备

- 光疗设备(LED 疗法)

- 雷射器

- 微晶磨皮设备

- 冷冻治疗设备

- 电外科设备

- 抽脂设备

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 皮肤癌

- 皮肤年轻化

- 除毛

- 塑身和紧緻肌肤

- 牛皮癣

- 其他应用

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 皮肤科中心

- 医院

- 诊所

- 其他最终用途

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Alma Lasers (Fosun Pharma)

- Ambicare Health

- Bausch Health Companies

- Biolitec

- Bruker Corporation

- Candela Corporation

- Canfield Scientific

- Carl Zeiss

- Cutera

- Cynosure Lutronic

- Genesis Biosystems

- Heine Optotechnik

- Hologic

- Image Derm

- Leica Microsystems

- Lumenis

- Michelson Diagnostics (VivoSight)

- Olympus Corporation

The Global Dermatology Devices Market was valued at USD 12.8 billion in 2024 and is expected to grow at an impressive CAGR of 11.5% from 2025 to 2034. This growth is primarily driven by the increasing prevalence of skin diseases, including skin cancer, as well as the rising focus on skincare in emerging economies. Additionally, technological advancements in dermatology devices are playing a key role in the expansion of this market, while developed regions are seeing heightened demand for cosmetic procedures. As consumers continue to prioritize skin health and aesthetic treatments, the market is set for sustained growth.

The market is categorized into diagnostic and treatment devices, both of which serve critical roles in addressing the increasing incidence of skin-related health concerns globally. Diagnostic devices are essential for early and accurate detection and include imaging systems, dermatoscopes, and biopsy tools. Meanwhile, treatment devices encompass light therapy systems, lasers, microdermabrasion units, cryotherapy tools, electrosurgical equipment, and liposuction devices. In 2024, diagnostic devices dominated the market, accounting for 55.3% of the total share. This is attributed to the growing need for timely identification of conditions such as eczema and skin cancer, as early detection is key to successful treatment outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.8 Billion |

| Forecast Value | $36.9 Billion |

| CAGR | 11.5% |

In terms of application, dermatology devices are widely used in the treatment of skin cancer, skin rejuvenation, hair removal, body contouring, psoriasis, and various other dermatological conditions. The skin cancer segment led the market in 2024, commanding a significant 26.6% share. This is due to the global rise in skin cancer cases, driving the demand for reliable diagnostic and treatment tools. Advanced dermatology devices are indispensable in identifying both cancerous and precancerous lesions, allowing for early intervention and improved patient outcomes.

The U.S. dermatology devices market, with a valuation of USD 4.1 billion in 2024, remains the largest in the world. This dominance is driven by the high rates of melanoma and non-melanoma skin cancers in the U.S., combined with extensive awareness programs and skin cancer prevention initiatives. Furthermore, the approval of advanced dermatology devices by the U.S. FDA has bolstered the availability of cutting-edge diagnostic and treatment solutions, contributing to the market's continued growth and innovation. As the demand for dermatological care intensifies, the U.S. will remain a key player in this rapidly expanding market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of skin associated diseases and skin cancer worldwide

- 3.2.1.2 Increasing expenditure on skin care in developing countries

- 3.2.1.3 Technological advancements in skincare devices

- 3.2.1.4 Growing demand for cosmetic procedures in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Excessive equipment cost

- 3.2.2.2 Stringent regulatory landscape

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Patent analysis

- 3.7 Future market trends

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy outlook

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diagnostic devices

- 5.2.1 Imaging devices

- 5.2.2 Dermatoscopes

- 5.2.3 Biopsy devices

- 5.3 Treatment devices

- 5.3.1 Light therapy devices (LED therapy)

- 5.3.2 Lasers

- 5.3.3 Microdermabrasion devices

- 5.3.4 Cryotherapy devices

- 5.3.5 Electrosurgical equipment

- 5.3.6 Liposuction devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Skin cancer

- 6.3 Skin rejuvenation

- 6.4 Hair removal

- 6.5 Body contouring and skin tightening

- 6.6 Psoriasis

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dermatology centers

- 7.3 Hospitals

- 7.4 Clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alma Lasers (Fosun Pharma)

- 9.2 Ambicare Health

- 9.3 Bausch Health Companies

- 9.4 Biolitec

- 9.5 Bruker Corporation

- 9.6 Candela Corporation

- 9.7 Canfield Scientific

- 9.8 Carl Zeiss

- 9.9 Cutera

- 9.10 Cynosure Lutronic

- 9.11 Genesis Biosystems

- 9.12 Heine Optotechnik

- 9.13 Hologic

- 9.14 Image Derm

- 9.15 Leica Microsystems

- 9.16 Lumenis

- 9.17 Michelson Diagnostics (VivoSight)

- 9.18 Olympus Corporation

2025年全球皮肤内视镜市场报告2025年全球皮肤内视镜设备市场报告2025年全球皮肤科设备市场报告

2025年全球皮肤内视镜市场报告2025年全球皮肤内视镜设备市场报告2025年全球皮肤科设备市场报告 皮肤镜市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035)

皮肤镜市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035) 全球皮肤病诊断设备市场规模(按类型、最终用户、区域范围)预测(至 2025 年)

全球皮肤病诊断设备市场规模(按类型、最终用户、区域范围)预测(至 2025 年) 皮肤病学影像全球市场:产业分析、规模、份额、成长、趋势和预测(2025-2032 年)

皮肤病学影像全球市场:产业分析、规模、份额、成长、趋势和预测(2025-2032 年) 皮肤科设备市场:全球 2025-2029视讯电子皮肤镜市场 - 全球产业规模、份额、趋势、机会和预测,按类型、按应用、按地区和竞争细分,2020-2030 年预测

皮肤科设备市场:全球 2025-2029视讯电子皮肤镜市场 - 全球产业规模、份额、趋势、机会和预测,按类型、按应用、按地区和竞争细分,2020-2030 年预测 皮肤科设备市场报告:趋势、预测和竞争分析(至 2031 年)全球皮肤病学设备市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年

皮肤科设备市场报告:趋势、预测和竞争分析(至 2031 年)全球皮肤病学设备市场研究报告 - 产业分析、规模、份额、成长、趋势和预测 2025 年至 2033 年