|

市场调查报告书

商品编码

1666962

特种聚苯乙烯树脂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Specialty Polystyrene Resin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

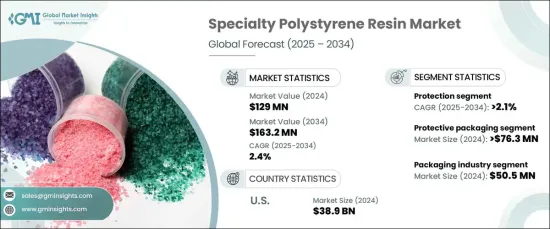

2024 年全球特种聚苯乙烯树脂市场价值为 1.29 亿美元,预计将稳定成长,预计 2025 年至 2034 年的复合年增长率为 2.4%。 特种聚苯乙烯树脂因其卓越的性能特性而受到认可,包括增强的衝击强度、耐热性和持久的耐用性。与标准聚苯乙烯不同,这些树脂适用于需要卓越功能的应用,使其成为电子、医疗设备和高性能包装等领域的首选材料。随着各行各业继续优先考虑满足严格性能要求的材料,特种聚苯乙烯树脂的市场将会扩大。製造技术的进步、材料效率意识的提高以及各种应用中轻量化、经济高效的解决方案的兴起进一步推动了这一增长。

特种聚苯乙烯树脂市场保护部分的估值在 2024 年达到 5,700 万美元,预计预测期间的复合年增长率为 2.1%。本部分强调了材料在需要增加耐用性、抗衝击性和热稳定性的应用中的价值。从敏感电子设备的保护外壳到汽车领域的零件,特种聚苯乙烯树脂满足了运输、搬运和储存过程中可靠保护的关键需求。其重量轻且具有成本效益进一步增强了它们的吸引力,使其成为寻求优化性能和成本的行业的首选。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.29亿美元 |

| 预测值 | 1.632亿美元 |

| 复合年增长率 | 2.4% |

保护性包装产业的价值将于 2024 年达到 7,630 万美元,预计未来十年的复合年增长率为 2.1%。对轻质、耐用且经济高效的包装解决方案的需求不断增长,推动了特种聚苯乙烯树脂的采用。这些材料具有出色的减震和隔热性能,对于包装电子产品和易腐烂物品等易碎物品来说是必不可少的。随着电子商务的快速扩张,特别是在消费性电子和医疗保健行业的快速扩张,对坚固保护包装的需求日益加剧。特种聚苯乙烯树脂正在成为这一增长的基石,提供平衡强度、可靠性和成本的解决方案。

2024 年,美国特种聚苯乙烯树脂市场价值为 3,890 万美元,预计 2025 年至 2034 年的复合年增长率为 2.5%。包装行业,尤其是食品包装,显着受益于该材料的透明度和保护性能。此外,随着消费者和製造商越来越重视环保解决方案,对永续性和可回收性的日益关注正在影响市场动态。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 对环保材料的需求不断增长

- 扩大电子领域的应用

- 材料技术的进步

- 产业陷阱与挑战

- 环境问题

- 回收挑战

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按功能,2021 年至 2034 年

- 主要趋势

- 保护

- 绝缘

- 轻的

- 耐用性

- 透明度

- 其他的

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 保护性包装

- 建筑与施工

- 汽车与运输

- 电气和电子产品

- 卫生保健

- 其他的

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 包装产业

- 电子业

- 汽车产业

- 建筑业

- 医疗保健产业

- 其他的

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Asahi Kasei

- BASF

- Braskem

- China Petrochemical Corporation

- ExxonMobil

- Formosa Plastics Corporation

- INEOS Styrolution

- LG Chem

- Mitsubishi Chemical Corporation

- SABIC

- Sinopec

- Styron (Dow)

- TotalEnergies

The Global Specialty Polystyrene Resin Market, valued at USD 129 million in 2024, is poised for steady growth, with projections indicating a CAGR of 2.4% from 2025 to 2034. Specialty polystyrene resin is recognized for its exceptional performance attributes, including enhanced impact strength, heat resistance, and long-lasting durability. Unlike standard polystyrene, these resins cater to applications that require superior functionality, making them a preferred material in sectors such as electronics, medical devices, and high-performance packaging. As industries continue to prioritize materials that meet stringent performance demands, the market for specialty polystyrene resin is set to expand. This growth is further fueled by advancements in manufacturing technologies, increasing awareness of material efficiency, and the rising trend of lightweight, cost-effective solutions across various applications.

The protection segment of the specialty polystyrene resin market achieved a valuation of USD 57 million in 2024, with expectations of a 2.1% CAGR over the forecast period. This segment underscores the material's value in applications necessitating added durability, impact resistance, and thermal stability. From protective casings for sensitive electronics to components in the automotive sector, specialty polystyrene resins address the critical need for reliable protection during shipping, handling, and storage. Their lightweight nature and cost-effectiveness further enhance their appeal, positioning them as a top choice for industries seeking to optimize both performance and cost.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $129 million |

| Forecast Value | $163.2 million |

| CAGR | 2.4% |

The protective packaging sector, valued at USD 76.3 million in 2024, is projected to grow at a CAGR of 2.1% over the next decade. The increasing demand for lightweight, durable, and cost-efficient packaging solutions drives the adoption of specialty polystyrene resins. These materials excel at shock absorption and thermal insulation, making them indispensable for packaging delicate items such as electronics and perishables. With the rapid expansion of e-commerce, particularly in the consumer electronics and healthcare industries, the need for robust protective packaging is intensifying. Specialty polystyrene resins are emerging as a cornerstone of this growth, delivering solutions that balance strength, reliability, and cost.

The U.S. specialty polystyrene resin market generated USD 38.9 million in 2024, with projections of a 2.5% CAGR from 2025 to 2034. The market's expansion in the U.S. is driven by the broad application of specialty polystyrene resins across industries, including packaging, electronics, automotive, and healthcare. The packaging sector, especially food packaging, benefits significantly from the material's clarity and protective properties. Furthermore, the rising focus on sustainability and recyclability is influencing market dynamics, as consumers and manufacturers increasingly prioritize environmentally friendly solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing demand for eco-friendly materials

- 3.6.1.2 Expanding applications in electronics

- 3.6.1.3 Advancements in material technology

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental concerns

- 3.6.2.2 Recycling challenges

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Function, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Protection

- 5.3 Insulation

- 5.4 Lightweight

- 5.5 Durability

- 5.6 Transparency

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Protective packaging

- 6.3 Building & construction

- 6.4 Automotive & transportation

- 6.5 Electrical & electronics

- 6.6 Healthcare

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging industry

- 7.3 Electronics industry

- 7.4 Automotive industry

- 7.5 Construction industry

- 7.6 Healthcare industry

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Asahi Kasei

- 9.2 BASF

- 9.3 Braskem

- 9.4 China Petrochemical Corporation

- 9.5 ExxonMobil

- 9.6 Formosa Plastics Corporation

- 9.7 INEOS Styrolution

- 9.8 LG Chem

- 9.9 Mitsubishi Chemical Corporation

- 9.10 SABIC

- 9.11 Sinopec

- 9.12 Styron (Dow)

- 9.13 TotalEnergies

特种聚苯乙烯树脂市场(依产品类型、树脂形式、聚合类型、分子量和应用)-全球预测 2025-2032聚苯乙烯市场按类型、形态、应用和製程划分-2025-2032年全球预测

特种聚苯乙烯树脂市场(依产品类型、树脂形式、聚合类型、分子量和应用)-全球预测 2025-2032聚苯乙烯市场按类型、形态、应用和製程划分-2025-2032年全球预测 2025-2033 年发泡聚苯乙烯市场报告(依产品(白色、灰色、黑色)、最终用途产业(建筑、包装、汽车等)及地区)

2025-2033 年发泡聚苯乙烯市场报告(依产品(白色、灰色、黑色)、最终用途产业(建筑、包装、汽车等)及地区) 2025-2029年全球发泡聚苯乙烯市场

2025-2029年全球发泡聚苯乙烯市场 全球发泡聚苯乙烯市场:市场规模、份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033)

全球发泡聚苯乙烯市场:市场规模、份额、趋势分析(按产品、应用和地区)、细分市场预测(2025-2033) 聚苯乙烯的全球市场:类别树脂,各用途,各地区,机会,预测,2018年~2032年

聚苯乙烯的全球市场:类别树脂,各用途,各地区,机会,预测,2018年~2032年 2025-2029年全球发泡聚苯乙烯(EPS)包装市场

2025-2029年全球发泡聚苯乙烯(EPS)包装市场 聚苯乙烯(PS)市场需求、产能、产量及价格范围及预测报告(截至2034年)聚苯乙烯市场规模、份额、趋势分析报告:按树脂类型、应用、地区、细分市场预测,2025-2030 年

聚苯乙烯(PS)市场需求、产能、产量及价格范围及预测报告(截至2034年)聚苯乙烯市场规模、份额、趋势分析报告:按树脂类型、应用、地区、细分市场预测,2025-2030 年 2032年溴化聚苯乙烯市场预测:按产品、形态、应用和地区分類的全球分析

2032年溴化聚苯乙烯市场预测:按产品、形态、应用和地区分類的全球分析