|

市场调查报告书

商品编码

1666966

宠物癌症治疗市场机会、成长动力、产业趋势分析与预测 2025 - 2034Pet Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

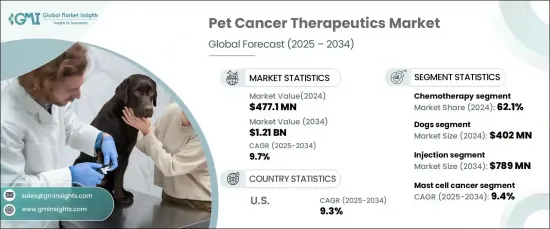

2024 年全球宠物癌症治疗市场规模达到 4.771 亿美元,预计 2025 年至 2034 年的复合年增长率为 9.7%。增强的诊断能力和尖端治疗方法(包括标靶治疗和免疫疗法)进一步提高了兽医癌症治疗的可及性和有效性。

宠物数量老化导致癌症发生率上升,大大增加了对肿瘤学解决方案的需求。消费者行为的演变,加上兽医学的不断进步,凸显了市场对宠物创新和延长寿命治疗的需求日益增长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 4.771亿美元 |

| 预测值 | 12.1亿美元 |

| 复合年增长率 | 9.7% |

市场按物种细分为狗、猫和其他动物。狗占据了最大的市场份额,2024 年的价值为 4.02 亿美元。犬肿瘤学对专科治疗的需求日益增长,持续推动了对有效治疗方案的需求。

根据治疗方法,市场包括化疗、免疫疗法、标靶治疗和联合治疗。化疗成为主要领域,到 2024 年将占据 62.1% 的份额。其在缓解方面的高成功率,尤其是对于常见的犬癌症,确保了其在兽医肿瘤学中持续占据重要地位。

2025 年至 2034 年期间,美国宠物癌症治疗市场复合年增长率为 9.3%。这种领导地位得益于该国强大的兽医医疗保健基础设施、高宠物拥有率以及对晚期癌症治疗的广泛认识。对兽医肿瘤学研究和技术的大量投资促进了创新疗法的发展,包括免疫疗法和标靶治疗,进一步加强了美国市场。

此外,老年宠物中癌症发生率的不断上升也持续推动了对高品质治疗方案的需求。随着人们对先进兽医护理的认识和采用的不断提高,宠物癌症治疗市场预计将在全球范围内实现强劲增长,北美将在塑造行业趋势方面发挥关键作用。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 增强宠物的人性化

- 宠物癌症发生率上升

- 兽医肿瘤诊断和治疗进展

- 提高认识和诊断能力

- 产业陷阱与挑战

- 治疗费用高

- 副作用和动物耐受性

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按物种,2021 – 2034 年

- 主要趋势

- 狗

- 猫

- 其他物种

第 6 章:市场估计与预测:按疗法,2021 – 2034 年

- 主要趋势

- 化疗

- 免疫疗法

- 标靶治疗

- 合併治疗

第 7 章:市场估计与预测:按管理路线,2021 年至 2034 年

- 主要趋势

- 口服

- 注射

第 8 章:市场估计与预测:按癌症类型,2021 年至 2034 年

- 主要趋势

- 淋巴瘤

- 肥大细胞癌

- 黑色素瘤

- 乳癌和鳞状细胞癌

- 其他癌症类型

第 9 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- AB Science

- Boehringer Ingelheim International

- CureLab Oncology

- Dechra Pharmaceuticals

- Elanco Animal Health

- ELIAS Animal Health

- NovaVive

- Qbiotics

- Pfizer

- Torigen

- Vibrac

- Vivesto

- Zoetis

The Global Pet Cancer Therapeutics Market reached USD 477.1 million in 2024 and is anticipated to grow at a CAGR of 9.7% from 2025 to 2034. This growth is primarily attributed to the rising trend of pet humanization, as pet owners increasingly prioritize advanced healthcare for their animals. Enhanced diagnostic capabilities and cutting-edge treatments, including targeted therapies and immunotherapies, are further boosting the accessibility and effectiveness of veterinary cancer care.

The aging pet population has led to a higher prevalence of cancer, significantly driving the demand for oncology solutions. This evolution in consumer behavior, combined with continual advancements in veterinary medicine, underlines the growing market need for innovative and life-prolonging treatments for pets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $477.1 Million |

| Forecast Value | $1.21 Billion |

| CAGR | 9.7% |

The market is segmented by species into dogs, cats, and other animals. Dogs held the largest market share, valued at USD 402 million in 2024. This dominance is attributed to the higher incidence of cancers such as lymphoma, osteosarcoma, and mammary tumors in dogs compared to other pets. The growing need for specialized treatments in canine oncology continues to propel the demand for effective therapeutic options.

By therapy, the market includes chemotherapy, immunotherapy, targeted therapy, and combination therapy. Chemotherapy emerged as the leading segment, generating a 62.1% share in 2024. Known for its efficacy in targeting and inhibiting the growth of cancer cells, chemotherapy remains a cornerstone of treatment for various cancers, particularly lymphoma and mast cell tumors. Its high success rates in remission, especially for common canine cancers, ensure its continued prominence in veterinary oncology.

U.S. pet cancer therapeutics market held a CAGR of 9.3% throughout 2025-2034. This leadership is driven by the country's robust veterinary healthcare infrastructure, high pet ownership rates, and widespread awareness of advanced cancer treatments. Significant investments in veterinary oncology research and technology enable the development of innovative therapies, including immunotherapy and targeted treatments, further strengthening the U.S. market.

Additionally, the increasing prevalence of cancer among aging pets continues to fuel the demand for high-quality therapeutic solutions. As awareness and adoption of advanced veterinary care rise, the pet cancer therapeutics market is expected to witness robust growth globally, with North America maintaining a pivotal role in shaping industry trends.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet humanization

- 3.2.1.2 Rising cancer incidence in pets

- 3.2.1.3 Advancements in veterinary oncology diagnosis and treatment

- 3.2.1.4 Growing awareness and diagnostic capabilities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Side effects and animal tolerance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Species, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

- 5.4 Other species

Chapter 6 Market Estimates and Forecast, By Therapy, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chemotherapy

- 6.3 Immunotherapy

- 6.4 Targeted therapy

- 6.5 Combination therapy

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injection

Chapter 8 Market Estimates and Forecast, By Cancer Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Lymphoma

- 8.3 Mast cell cancer

- 8.4 Melanoma

- 8.5 Mammary and squamous cell cancer

- 8.6 Other cancer types

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AB Science

- 10.2 Boehringer Ingelheim International

- 10.3 CureLab Oncology

- 10.4 Dechra Pharmaceuticals

- 10.5 Elanco Animal Health

- 10.6 ELIAS Animal Health

- 10.7 NovaVive

- 10.8 Qbiotics

- 10.9 Pfizer

- 10.10 Torigen

- 10.11 Vibrac

- 10.12 Vivesto

- 10.13 Zoetis