|

市场调查报告书

商品编码

1667017

多参数患者监测市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测Multiparameter Patient Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

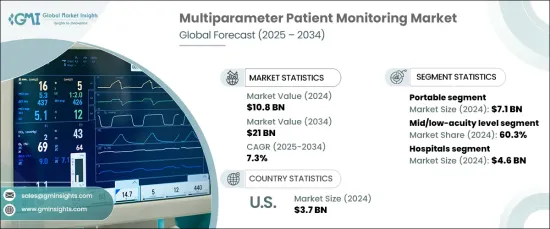

2024 年全球多参数患者监测市场价值为 108 亿美元,预计 2025 年至 2034 年的复合年增长率为 7.3%。

随着全球医疗保健系统转向以患者为中心的方式,对可靠、即时监测解决方案的需求激增。这些系统不仅提供生命征象的深入分析,还使临床医生能够采取主动措施,预防併发症的恶化。随着远距医疗的普及、慢性病的发生率的上升以及许多地区老年人口的不断增加,市场有望进一步成长。人工智慧 (AI) 和机器学习的进步有望进一步提高这些系统的有效性,实现更个人化和精确的医疗干预。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 108亿美元 |

| 预测值 | 210亿美元 |

| 复合年增长率 | 7.3% |

市场分为便携式和固定係统,其中便携式设备在创收方面占据市场领先地位。这种成长主要得益于对远距病人监控日益增长的需求,尤其是在家庭医疗环境中。便携式设备具有无与伦比的灵活性,允许在医院外持续监测患者。对于需要持续观察的慢性病患者来说,这尤其有益。即时追踪生命征象的能力赋予了病人更多自主权,同时也能确保医疗保健提供者及时了解其病情的任何重大变化。这种便利性导致需求大幅增加,预计这种趋势将持续整个预测期。

市场进一步分为高敏感度和中/低敏感度类别,其中中/低敏感度部分在 2024 年占据相当大的市场份额。这些领域需要基本但有效的监测解决方案,可以检测到患者病情的细微变化,从而及时触发医疗反应。随着医疗保健越来越注重早期干预和预防性护理,中/低敏锐度监测系统的采用预计会增加。

在美国,多参数患者监测市场在 2024 年创造了 37 亿美元的收入。美国医疗保健系统越来越多地采用人工智慧和机器学习等先进技术,推动监测系统的创新并提高其功能。对医院和家庭护理监测解决方案的需求不断增长,并继续支持该地区的市场成长。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 慢性病发生率上升

- 提高对多参数监测仪的认识

- 便携式家用多参数患者监护设备的普及率不断提高

- 多参数监测仪中先进技术的集成

- 产业陷阱与挑战

- 严格的监管框架

- 多参数监测设备成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 我们

- 欧洲

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按设备类型,2021 – 2034 年

- 主要趋势

- 便携的

- 固定的

第六章:市场估计与预测:依敏锐度水平,2021 年至 2034 年

- 主要趋势

- 高敏锐度

- 中/低敏感度

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 家庭护理设置

- 门诊手术中心

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Baxter International

- BPL Medical Technologies

- Dragerwerk

- GE Healthcare

- Koninklijke Philips

- Medion

- Medtronic

- Mindray

- Murata Vios

- Nihon Kohden Corporation

- Opto Circuits

- OSI Systems

- Schiller Healthcare

- Skanray Technologies

- Zoll Medical

The Global Multiparameter Patient Monitoring Market, valued at USD 10.8 billion in 2024, is projected to expand at a CAGR of 7.3% from 2025 to 2034. This market involves the continuous or periodic tracking of multiple vital physiological parameters simultaneously, using sophisticated monitoring systems that integrate advanced technology to improve accuracy, precision, and early detection of various health conditions.

As healthcare systems worldwide move towards more patient-centric approaches, the demand for reliable and real-time monitoring solutions has surged. These systems not only provide in-depth analysis of vital signs but also enable clinicians to take proactive measures, preventing complications before they escalate. The market is poised to grow even further with the rising adoption of telemedicine, the increasing prevalence of chronic diseases, and an expanding geriatric population in many regions. Advances in artificial intelligence (AI) and machine learning are expected to further elevate the effectiveness of these systems, enabling even more personalized and precise healthcare interventions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.8 Billion |

| Forecast Value | $21 Billion |

| CAGR | 7.3% |

The market is segmented into portable and fixed systems, with portable devices leading the market in terms of revenue generation. This growth is primarily driven by the increasing demand for remote patient monitoring, especially in home healthcare environments. Portable devices offer unparalleled flexibility, allowing patients to be monitored continuously outside of hospital settings. This is particularly beneficial for individuals with chronic conditions who require ongoing observation. The ability to track vital signs in real time gives patients more autonomy, while also ensuring that healthcare providers are kept informed of any significant changes in their condition. This convenience has led to a substantial surge in demand, which is expected to continue throughout the forecast period.

The market is further divided into high-acuity and mid/low-acuity categories, with the mid/low-acuity segment capturing a substantial market share in 2024. This segment is anticipated to experience significant growth as healthcare providers focus on enhancing patient safety and well-being across various settings, including general hospital wards and step-down units. These areas need basic yet effective monitoring solutions that can detect even subtle shifts in a patient's condition, which can then trigger timely medical responses. As healthcare becomes increasingly focused on early intervention and preventative care, the adoption of mid/low-acuity monitoring systems is expected to rise.

In the U.S., the multiparameter patient monitoring market generated USD 3.7 billion in 2024. This growth is largely attributed to an aging population, rising chronic disease rates, and the increasing acceptance of cutting-edge healthcare technologies. U.S. healthcare systems are increasingly incorporating advanced technologies such as AI and machine learning, driving innovation in monitoring systems and improving their functionality. The rising demand for both hospital-based and home care monitoring solutions continues to support market growth in the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of chronic diseases

- 3.2.1.2 Increasing awareness regarding multiparameter monitors

- 3.2.1.3 Growing adoption of portable home multiparameter patient monitoring device

- 3.2.1.4 Integration of advanced technology within the multiparameter monitors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of multiparameter monitoring device

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Portable

- 5.3 Fixed

Chapter 6 Market Estimates and Forecast, By Acuity Level, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 High-acuity level

- 6.3 Mid/low-acuity level

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital

- 7.3 Homecare settings

- 7.4 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Baxter International

- 9.2 BPL Medical Technologies

- 9.3 Dragerwerk

- 9.4 GE Healthcare

- 9.5 Koninklijke Philips

- 9.6 Medion

- 9.7 Medtronic

- 9.8 Mindray

- 9.9 Murata Vios

- 9.10 Nihon Kohden Corporation

- 9.11 Opto Circuits

- 9.12 OSI Systems

- 9.13 Schiller Healthcare

- 9.14 Skanray Technologies

- 9.15 Zoll Medical

多参数探头市场:按便携性、应用和销售管道,全球预测(2026-2032年)携带式通风量计市场(按设备类型、电源、应用、最终用户和销售管道),全球预测(2026-2032年)

多参数探头市场:按便携性、应用和销售管道,全球预测(2026-2032年)携带式通风量计市场(按设备类型、电源、应用、最终用户和销售管道),全球预测(2026-2032年) 2026年全球多参数病患监测设备市场报告2026年全球手持式多参数监测设备市场报告床边多功能患者监护仪市场按行动端性别、技术、设备类型、最终用户和应用划分 - 全球预测(2026-2032 年)

2026年全球多参数病患监测设备市场报告2026年全球手持式多参数监测设备市场报告床边多功能患者监护仪市场按行动端性别、技术、设备类型、最终用户和应用划分 - 全球预测(2026-2032 年) 多参数监测市场规模、份额和成长分析(按设备、严重程度、年龄层、应用和地区划分)—产业预测(2026-2033 年)

多参数监测市场规模、份额和成长分析(按设备、严重程度、年龄层、应用和地区划分)—产业预测(2026-2033 年) 手持终端机:全球市场占有率和排名、总收入和需求预测(2025-2031年)多参数病患监测系统市场:按便携性、最终用户、技术和应用划分-2025-2032年全球预测

手持终端机:全球市场占有率和排名、总收入和需求预测(2025-2031年)多参数病患监测系统市场:按便携性、最终用户、技术和应用划分-2025-2032年全球预测 多参数病患监测系统市场规模、份额和趋势分析报告:按设备、严重程度、年龄组、最终用途、地区和细分市场预测,2025 年至 2033 年

多参数病患监测系统市场规模、份额和趋势分析报告:按设备、严重程度、年龄组、最终用途、地区和细分市场预测,2025 年至 2033 年 手持式多参数监测设备市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035)

手持式多参数监测设备市场-全球产业分析、规模、份额、成长、趋势及预测(2025-2035)