|

市场调查报告书

商品编码

1667057

汽车手势辨识市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Automotive Gesture Recognition Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

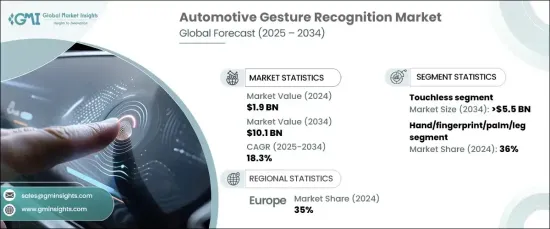

2024 年全球汽车手势辨识市场价值为 19 亿美元,预计 2025 年至 2034 年的复合年增长率为 18.3%。随着消费者越来越追求更智慧的汽车,手势识别技术已成为关键的解决方案,使驾驶员无需实际接触任何按钮或萤幕即可控制资讯娱乐、导航和气候控制等各种功能。透过利用自然的手部动作,该技术可以无缝融入日常驾驶,使汽车体验更加直觉和人性化。向更先进的手势识别系统的转变反映了汽车介面自动化和简化的持续趋势,满足了对驾驶体验有更多期望的现代消费者的需求。

市场分为两种主要技术类别:触控式系统和非触控式系统。非接触式手势辨识在 2024 年占据了市场主导地位,占总份额的 55%,预计到 2034 年将达到 55 亿美元。由于该技术使驾驶员无需身体接触即可与车辆控制装置进行交互,因此它有助于保持对道路的注意力,同时仍提供无缝操作。简单的手势可以让驾驶员控制各种功能,例如调整音量或更改导航设置,从而进一步改善驾驶体验,因为驾驶员无需将视线从道路上移开。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 19亿美元 |

| 预测值 | 101亿美元 |

| 复合年增长率 | 18.3% |

在身份验证方面,汽车手势识别市场细分为手/指纹/手掌/腿、脸部、视觉、语音和混合系统。 2024 年,手/指纹/手掌/腿部身份验证部分占据了 36% 的市场份额。透过生物辨识身分验证,钥匙卡或 PIN 码等传统方法被安全、唯一的识别码所取代,使车辆进入和引擎启动更快、更安全。此外,该技术还可以根据特定驾驶员的资料自订车辆的设定(例如座椅位置和首选驾驶模式),从而提高整体的便利性和舒适性。

欧洲在塑造汽车手势识别市场方面发挥了重要作用,到 2024 年将占据 35% 的市场份额。随着欧洲监管机构推动提高车辆安全性并减少道路事故,製造商越来越多地整合手势控制和生物识别系统以满足这些高标准。由于这些技术在提高安全性和使用者体验方面发挥着至关重要的作用,欧洲汽车手势辨识市场将在未来几年继续扩大。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 零件供应商

- 软体开发者

- 技术提供者

- 售后市场供应商

- 最终用途

- 供应商概况

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻及倡议

- 监管格局

- 定价分析

- 成本明细分析

- 衝击力

- 成长动力

- 对先进车辆安全功能的需求不断增加

- 越来越注重改善驾驶和乘客的体验

- 监管支援和安全标准正在推动驾驶员监控系统的采用

- 自动驾驶和网路连线汽车的普及率不断提高

- 产业陷阱与挑战

- 实施成本高

- 在不同驾驶条件下实现准确识别存在挑战

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按技术,2021 - 2034 年

- 主要趋势

- 触控式

- 无接触

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 轿车

- 掀背车

- SUV

- 商用车

- 轻型商用车 (LCV)

- 重型商用车 (HCV)

第 7 章:市场估计与预测:按认证,2021 - 2034 年

- 主要趋势

- 手/指纹/手掌/腿

- 脸

- 想像

- 嗓音

- 杂交种

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 多媒体/资讯娱乐/导航

- 照明系统

- 气候控制

- 车窗和天窗操作

- 驾驶员监控系统

- 其他的

第 9 章:市场估计与预测:按销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第 10 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Apple

- Aptiv

- Bosch

- Cognitec Systems

- Continental

- Eyesight Technologies

- Gestigon

- Harman

- Intel

- Magna

- Melexis

- Navtek Solutions

- Neonode

- NXP Semiconductors

- Qualcomm

- Renesas Electronics

- Synaptics

- Texas Instruments

- Valeo

- Visteon

The Global Automotive Gesture Recognition Market, valued at USD 1.9 billion in 2024, is set to experience a CAGR of 18.3% from 2025 to 2034. This surge is largely driven by the growing demand for innovative in-car technologies that offer enhanced convenience, better user experiences, and improved vehicle safety. With consumers increasingly seeking smarter vehicles, gesture recognition technology has emerged as a key solution that allows drivers to control a variety of functions such as infotainment, navigation, and climate control without needing to physically touch any buttons or screens. By leveraging natural hand movements, this technology seamlessly integrates into daily driving, making the car experience more intuitive and user-friendly. The shift toward more advanced gesture recognition systems reflects an ongoing trend towards automating and streamlining car interfaces, meeting the needs of modern consumers who expect more from their driving experience.

The market is split into two primary technology categories: touch-based and touchless systems. The touchless segment dominated the market in 2024, accounting for 55% of the total share, and is projected to reach USD 5.5 billion by 2034. The appeal of touchless gesture recognition lies in its ability to enhance driver safety by minimizing distractions. Since the technology enables drivers to interact with vehicle controls without physical contact, it helps maintain focus on the road while still providing seamless operation. Simple hand gestures allow drivers to control various features, such as adjusting volume or changing navigation settings, further improving the driving experience by eliminating the need to look away from the road.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 18.3% |

In terms of authentication, the automotive gesture recognition market is segmented into hand/fingerprint/palm/leg, face, vision, voice, and hybrid systems. The hand/fingerprint/palm/leg authentication segment represented 36% of the market share in 2024. This biometric system offers not only increased security but also the potential for a more personalized user experience. With biometric authentication, traditional methods like key fobs or PIN codes are replaced by secure, unique identifiers that make vehicle access and engine starting faster and safer. Furthermore, this technology can tailor the vehicle's settings-such as seat position and preferred driving mode-based on the specific driver's data, enhancing overall convenience and comfort.

Europe played a significant role in shaping the automotive gesture recognition market, holding 35% of the market share in 2024. Stringent automotive safety and environmental regulations in the region are accelerating the adoption of advanced technologies like gesture recognition. With European regulators pushing for safer vehicles and fewer road accidents, manufacturers are increasingly integrating gesture control and biometric systems to meet these high standards. As these technologies play a crucial role in improving both safety and user experience, the European market for automotive gesture recognition is poised for continued expansion in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Software developers

- 3.1.4 Technology providers

- 3.1.5 Aftermarket providers

- 3.1.6 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for advanced vehicle safety features

- 3.10.1.2 Growing focus on improving driver and passenger experiences

- 3.10.1.3 Regulatory support and safety standards are driving the adoption of driver monitoring systems

- 3.10.1.4 Increasing adoption of autonomous and connected vehicles

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High implementation costs

- 3.10.2.2 Challenges exist in achieving accurate recognition in different driving conditions

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Touch-based

- 5.3 Touchless

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Technology)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light Commercial Vehicles (LCV)

- 6.3.2 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Authentication, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Hand/Fingerprint/Palm/Leg

- 7.3 Face

- 7.4 Vision

- 7.5 Voice

- 7.6 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Multimedia/infotainment/navigation

- 8.3 Lighting system

- 8.4 Climate control

- 8.5 Window and sunroof operation

- 8.6 Driver monitoring systems

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn,Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Apple

- 11.2 Aptiv

- 11.3 Bosch

- 11.4 Cognitec Systems

- 11.5 Continental

- 11.6 Eyesight Technologies

- 11.7 Gestigon

- 11.8 Harman

- 11.9 Intel

- 11.10 Magna

- 11.11 Melexis

- 11.12 Navtek Solutions

- 11.13 Neonode

- 11.14 NXP Semiconductors

- 11.15 Qualcomm

- 11.16 Renesas Electronics

- 11.17 Synaptics

- 11.18 Texas Instruments

- 11.19 Valeo

- 11.20 Visteon

手势姿态辨识与非接触式感测市场:依技术、组件、应用、终端用户产业及外形规格-2025-2032年全球预测手势姿态辨识市场(按技术、产品、部署模式、应用和最终用户划分)—全球预测 2025-2032

手势姿态辨识与非接触式感测市场:依技术、组件、应用、终端用户产业及外形规格-2025-2032年全球预测手势姿态辨识市场(按技术、产品、部署模式、应用和最终用户划分)—全球预测 2025-2032 2025年手势姿态辨识与非接触式感应全球市场报告

2025年手势姿态辨识与非接触式感应全球市场报告 2032 年基于二维材料的电子市场预测:按产品类型、材料类型、製造技术、应用和地区进行的全球分析

2032 年基于二维材料的电子市场预测:按产品类型、材料类型、製造技术、应用和地区进行的全球分析 手势姿态辨识和非接触式感应市场规模、份额和成长分析(按技术、组织规模、应用、最终用户和地区):产业预测(2025-2032)

手势姿态辨识和非接触式感应市场规模、份额和成长分析(按技术、组织规模、应用、最终用户和地区):产业预测(2025-2032) 手势辨识和非接触式感测市场,按产品类型、按技术、按最终用户、按国家和地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测

手势辨识和非接触式感测市场,按产品类型、按技术、按最终用户、按国家和地区划分 - 2025 年至 2032 年全球产业分析、市场规模、市场份额及预测 手势辨识市场规模、份额、趋势及预测(依技术、最终用途产业及地区),2025 年至 2033 年

手势辨识市场规模、份额、趋势及预测(依技术、最终用途产业及地区),2025 年至 2033 年 智慧型电视手势姿态辨识市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032)

智慧型电视手势姿态辨识市场:全球产业分析、市场规模、份额、成长、趋势与未来预测(2025-2032) 全球手势感应控制市场

全球手势感应控制市场 零售中的手势姿态辨识:市场份额分析、行业趋势、统计数据和成长预测(2025-2030)

零售中的手势姿态辨识:市场份额分析、行业趋势、统计数据和成长预测(2025-2030)