|

市场调查报告书

商品编码

1667187

化学锅炉市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Chemical Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

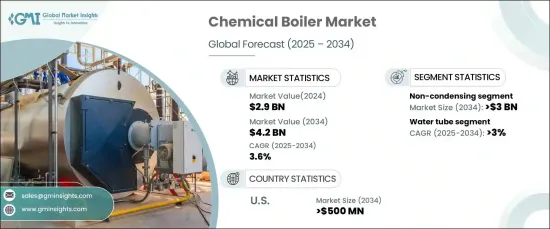

2024 年全球工锅炉市场规模达到 29 亿美元,预计将实现稳步增长,2025 年至 2034 年的复合年增长率预计为 3.6%。 这一扩张得益于工业基础设施的不断进步、日益增多的节能倡议以及各个行业对更高效供热技术日益增长的需求。随着全球各地的产业越来越注重永续性,人们开始明显转向符合全球环境目标的低排放供暖系统。以现代的、更有效率的模型取代过时的传统系统的需求进一步推动了化学锅炉的采用。随着各行各业越来越意识到其对环境的影响,对符合严格的政府能源效率和碳排放法规的锅炉的需求也日益增加。

预计到 2034 年,非冷凝化工锅炉市场的规模将超过 30 亿美元。非冷凝化学锅炉由于其功能增强而变得越来越受欢迎,这得益于智慧控制和远端监控等功能。这些改进使非冷凝锅炉成为现代工业应用的重要组成部分,而现代工业应用中需要高性能、低排放的加热解决方案。随着越来越多的行业采用这些先进技术,该领域将实现显着扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 29亿美元 |

| 预测值 | 42亿美元 |

| 复合年增长率 | 3.6% |

预计水管化学锅炉市场将稳步成长,到 2034 年复合年增长率将达到 3%。改良的绝缘技术、先进的燃烧系统和热回收解决方案等技术进步正在重塑格局,为水管化学锅炉的采用开闢新的机会。随着各行各业不断寻求提高营运效率和降低能源成本的方法,这些锅炉的市场预计将稳定成长。

在美国,化学锅炉市场预计到 2034 年将创收 5 亿美元。随着立法者采用更严格的标准,对低排放和超低排放锅炉系统的需求正在迅速增长。物联网控制等智慧技术的整合进一步提高了化学锅炉的运作效率和可靠性,使其成为实现国家能源和环境目标的重要组成部分。

在亚太地区,化工锅炉市场正在快速扩张,这得益于该地区蓬勃发展的化学工业和对老化基础设施进行现代化改造的努力。各国政府正在强调永续能源解决方案并鼓励采用更清洁的燃料替代品。环保、生物基化学製程的研究和开发也促进了市场的成长。因此,该地区将在全球化学锅炉市场中发挥关键作用,并成为向更永续、更有效率的供热解决方案过渡的领导者。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依产能,2021 – 2034 年

- 主要趋势

- < 10 百万英热单位/小时

- 10-25百万英热单位/小时

- 25-50 百万英热单位/小时

- 50-75 百万英热单位/小时

- 75-100 百万英热单位/小时

- 100-175 百万英热单位/小时

- 175-250 百万英热单位/小时

- > 250 百万英热单位/小时

第 6 章:市场规模及预测:依产品,2021 – 2034 年

- 主要趋势

- 火管

- 水管

第 7 章:市场规模与预测:依技术,2021 – 2034 年

- 主要趋势

- 冷凝

- 无凝结

第 8 章:市场规模与预测:按燃料,2021 – 2034 年

- 主要趋势

- 天然气

- 油

- 煤炭

- 其他的

第 9 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 法国

- 英国

- 波兰

- 义大利

- 西班牙

- 奥地利

- 德国

- 瑞典

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 菲律宾

- 日本

- 韩国

- 澳洲

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 伊朗

- 阿联酋

- 奈及利亚

- 南非

- 拉丁美洲

- 阿根廷

- 智利

- 巴西

第十章:公司简介

- Babcock & Wilcox Enterprises

- Babcock Wanson

- Boilermech Holdings Berhad

- Clayton Industries

- Cleaver-Brooks

- Cochran

- FERROLI SpA

- Forbes Marshalls

- Fulton

- Hurst Boiler & Welding

- John Cockerill

- Maxima Boilers

- Miura America

- Rentech Boiler Systems

- Robert Bosch

- Thermax

- Thermodyne Boilers

- Vapor Power International

- Viessmann

- York-Shipley

The Global Chemical Boiler Market reached USD 2.9 billion in 2024 and is expected to experience steady growth, with a projected CAGR of 3.6% from 2025 to 2034. This expansion is fueled by ongoing advancements in industrial infrastructure, growing energy-saving initiatives, and the rising demand for more efficient heating technologies across various sectors. As industries worldwide increasingly focus on sustainability, there is a notable shift toward low-emission heating systems that align with global environmental goals. The need to replace outdated, conventional systems with modern, more efficient models is further driving the adoption of chemical boilers. With industries becoming more conscious of their environmental impact, the demand for boilers that meet stringent government regulations related to energy efficiency and carbon emissions is intensifying.

The non-condensing chemical boiler segment is expected to surpass USD 3 billion by 2034. The chemical sector's growth, paired with rising government pressure to reduce greenhouse gas emissions, is amplifying the need for these types of boilers. Non-condensing chemical boilers are becoming more popular due to their enhanced functionality, driven by features like smart controls and remote monitoring. These improvements are making non-condensing boilers a vital component in modern industrial applications, where high-performance, low-emission heating solutions are in demand. As more industries embrace these advanced technologies, the segment is set to see significant expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.2 Billion |

| CAGR | 3.6% |

The water tube chemical boiler market is predicted to grow at a steady pace, registering a CAGR of 3% through 2034. Energy efficiency continues to be a top priority, with manufacturers focusing on innovative designs that maximize heat transfer and minimize energy losses. Technological advancements, such as improved insulation, advanced combustion systems, and heat recovery solutions, are reshaping the landscape, opening up new opportunities for the adoption of water tube chemical boilers. As industries seek ways to improve operational efficiency and lower energy costs, the market for these boilers is expected to grow steadily.

In the U.S., the chemical boiler market is poised to generate USD 500 million by 2034. This growth is driven by increasing environmental awareness, as well as the implementation of stricter emission regulations across various states. As lawmakers adopt more stringent standards, the demand for low-emission and ultra-low-emission boiler systems is growing rapidly. The integration of smart technologies, such as IoT-enabled controls, is further enhancing the operational efficiency and reliability of chemical boilers, making them an essential component in meeting the nation's energy and environmental goals.

In the Asia Pacific region, the chemical boiler market is experiencing rapid expansion, driven by the region's booming chemical industry and efforts to modernize aging infrastructure. Governments are emphasizing sustainable energy solutions and encouraging the adoption of cleaner fuel alternatives. Research and development in eco-friendly, bio-based chemical processes are also contributing to market growth. As a result, the region is set to play a key role in the global chemical boiler market, positioning itself as a leader in the transition to more sustainable and efficient heating solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 5.1 Key trends

- 5.2 < 10 MMBTU/hr

- 5.3 10-25 MMBTU/hr

- 5.4 25-50 MMBTU/hr

- 5.5 50-75 MMBTU/hr

- 5.6 75-100 MMBTU/hr

- 5.7 100-175 MMBTU/hr

- 5.8 175-250 MMBTU/hr

- 5.9 > 250 MMBTU/hr

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 6.1 Key trends

- 6.2 Fire-tube

- 6.3 Water-tube

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 7.1 Key trends

- 7.2 Condensing

- 7.3 Non-condensing

Chapter 8 Market Size and Forecast, By Fuel, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 8.1 Key trends

- 8.2 Natural gas

- 8.3 Oil

- 8.4 Coal

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (Units, MMBTU/hr & USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 France

- 9.3.2 UK

- 9.3.3 Poland

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Austria

- 9.3.7 Germany

- 9.3.8 Sweden

- 9.3.9 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Philippines

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.4.6 Australia

- 9.4.7 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 Iran

- 9.5.3 UAE

- 9.5.4 Nigeria

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Argentina

- 9.6.2 Chile

- 9.6.3 Brazil

Chapter 10 Company Profiles

- 10.1 Babcock & Wilcox Enterprises

- 10.2 Babcock Wanson

- 10.3 Boilermech Holdings Berhad

- 10.4 Clayton Industries

- 10.5 Cleaver-Brooks

- 10.6 Cochran

- 10.7 FERROLI S.p.A

- 10.8 Forbes Marshalls

- 10.9 Fulton

- 10.10 Hurst Boiler & Welding

- 10.11 John Cockerill

- 10.12 Maxima Boilers

- 10.13 Miura America

- 10.14 Rentech Boiler Systems

- 10.15 Robert Bosch

- 10.16 Thermax

- 10.17 Thermodyne Boilers

- 10.18 Vapor Power International

- 10.19 Viessmann

- 10.20 York-Shipley