|

市场调查报告书

商品编码

1684194

实验室真空帮浦市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Laboratory Vacuum Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

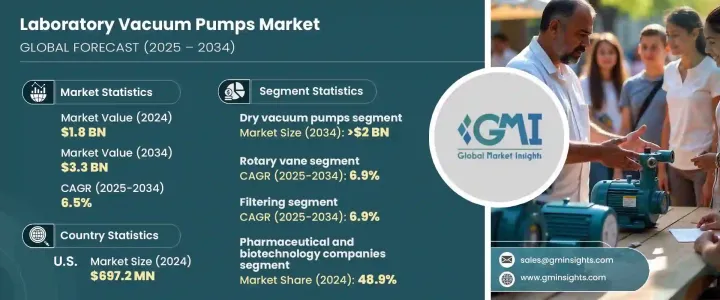

2024 年全球实验室真空帮浦市场价值为 18 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 6.5%。这些产业的实验室依靠真空帮浦来进行药物开发、灭菌和干燥等关键应用。随着全球慢性病盛行率不断上升,对诊断工具和实验室设备的需求也不断增加,进一步推动了真空帮浦市场的扩张。此外,随着医疗保健计划推动更准确的诊断和更有效率的药物开发过程,实验室真空帮浦在确保实现这些进步方面发挥着至关重要的作用。

技术创新,特别是无油和节能真空帮浦的技术创新也推动了市场的成长。随着人们对永续性的认识不断提高以及对实验室设备的严格规定,製造商现在专注于创造高性能、环保的解决方案。这种向绿色技术的转变不仅满足了监管要求,而且扩大了真空帮浦在不同实验室环境中的应用范围。因此,真空帮浦在实验室环境中变得越来越重要,可以提高效率、永续性和性能。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 18亿美元 |

| 预测值 | 33亿美元 |

| 复合年增长率 | 6.5% |

市场按产品类型细分,包括湿式真空帮浦、真空帮浦和干式真空帮浦。干式真空帮浦领域预计将实现最高成长,预计复合年增长率为 6.8%,到 2034 年将达到 20 亿美元。它们的无油设计在纯度至关重要的环境中至关重要,使其非常适合干燥和过滤等应用。

就技术而言,实验室真空帮浦市场分为旋片式、旋转式螺桿式、旋转爪式和其他技术。旋片真空帮浦市场将占据主导地位,预计复合年增长率为 6.9%,到 2034 年达到 15 亿美元。 这些帮浦以其在过滤、干燥和蒸馏等应用中的可靠性和多功能性而闻名。其耐用的设计确保了稳定的真空水平,使其成为製药和工业实验室必不可少的工具。

在美国,实验室真空帮浦市场规模在 2024 年达到 6.972 亿美元,预计将继续推动市场成长,预计 2025 年至 2034 年的复合年增长率为 5.9%。 这一增长得益于美国在製药和生物技术领域的领导地位,对先进实验室的需求不断增加,以支持新的医疗保健计划和创新。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 医疗保健领域对诊断实验室的需求不断增加

- 製药和生物技术研究活动的成长

- 需要真空技术的先进医疗设备日益普及

- 扩大生物製药产业和疫苗生产

- 产业陷阱与挑战

- 某些真空帮浦的维护挑战和营运成本

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 干式真空帮浦

- 湿式真空帮浦

- 组合真空帮浦

第六章:市场估计与预测:按技术,2021 - 2034 年

- 主要趋势

- 旋片式

- 旋转螺桿

- 旋爪

- 其他技术

第 7 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 滤

- 烘干

- 蒸馏

- 其他应用

第 8 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 製药和生物技术公司

- 医院和诊断实验室

- 学术和研究机构

- 其他最终用户

第 9 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Agilent

- Atlas Copco

- BUSCH

- DEKKER

- Ebara Technologies

- EDWARDS

- gast

- Graham

- KNF

- Leybold

- PFEIFFER

- SHIMADZU

- ULVAC

- VACUUBRAND

- WELCH

The Global Laboratory Vacuum Pumps Market was valued at USD 1.8 billion in 2024 and is projected to experience a CAGR of 6.5% from 2025 to 2034. This growth is primarily attributed to the booming pharmaceutical and biotechnology sectors, increasing investment in research and development (R&D), and the escalating need for advanced diagnostic solutions. Laboratories in these industries depend on vacuum pumps for critical applications such as drug development, sterilization, and drying. As the global prevalence of chronic diseases continues to rise, so does the demand for diagnostic tools and laboratory equipment, further driving the vacuum pump market expansion. Additionally, as healthcare initiatives push for more accurate diagnostics and efficient drug development processes, laboratory vacuum pumps play an essential role in ensuring these advancements can be achieved.

Technological innovations, particularly in oil-free and energy-efficient vacuum pumps, are also fueling market growth. With heightened awareness around sustainability and stringent regulations on laboratory equipment, manufacturers are now focusing on creating high-performance, eco-friendly solutions. This shift toward green technologies not only meets regulatory demands but also expands the range of applications for vacuum pumps in diverse laboratory environments. As such, vacuum pumps are becoming increasingly integral to laboratory settings, enhancing efficiency, sustainability, and performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 6.5% |

The market is segmented by product type, including wet vacuum pumps, vacuum pumps, and dry vacuum pumps. The dry vacuum pumps segment is expected to see the highest growth, projected to grow at a CAGR of 6.8%, reaching USD 2 billion by 2034. These pumps are especially favored in industries like pharmaceuticals and biotechnology for their contamination-free operation and low maintenance needs. Their oil-free design is critical in environments where purity is paramount, making them highly suitable for applications such as drying and filtration.

Regarding technology, the laboratory vacuum pumps market is divided into rotary vane, rotary screw, rotary claw, and other technologies. The rotary vane vacuum pump segment is set to dominate, expected to grow at a CAGR of 6.9%, reaching USD 1.5 billion by 2034. These pumps are renowned for their reliability and versatility in applications such as filtration, drying, and distillation. Their durable design ensures stable vacuum levels, making them an essential tool in both pharmaceutical and industrial laboratories.

In the U.S., the laboratory vacuum pumps market reached USD 697.2 million in 2024 and is projected to continue driving market growth, with an expected CAGR of 5.9% from 2025 to 2034. This growth is fueled by the nation's leadership in the pharmaceutical and biotechnology sectors, with increasing demand for advanced laboratory equipment to support new healthcare initiatives and innovative drug development.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for diagnostic laboratories in the healthcare sector

- 3.2.1.2 Growth in pharmaceutical and biotechnology research activities

- 3.2.1.3 Rising adoption of advanced medical devices requiring vacuum technology

- 3.2.1.4 Expanding biopharmaceutical industry and vaccine production

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Maintenance challenges and operational costs of certain vacuum pumps

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dry vacuum pumps

- 5.3 Wet vacuum pumps

- 5.4 Combination vacuum pumps

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Rotary vane

- 6.3 Rotary screw

- 6.4 Rotary claw

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Filtering

- 7.3 Drying

- 7.4 Distillation

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pharmaceutical and biotechnology companies

- 8.3 Hospitals and diagnostic labs

- 8.4 Academic and research institutes

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Agilent

- 10.2 Atlas Copco

- 10.3 BUSCH

- 10.4 DEKKER

- 10.5 Ebara Technologies

- 10.6 EDWARDS

- 10.7 gast

- 10.8 Graham

- 10.9 KNF

- 10.10 Leybold

- 10.11 PFEIFFER

- 10.12 SHIMADZU

- 10.13 ULVAC

- 10.14 VACUUBRAND

- 10.15 WELCH