|

市场调查报告书

商品编码

1684531

牙科印模系统市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Dental Impression Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

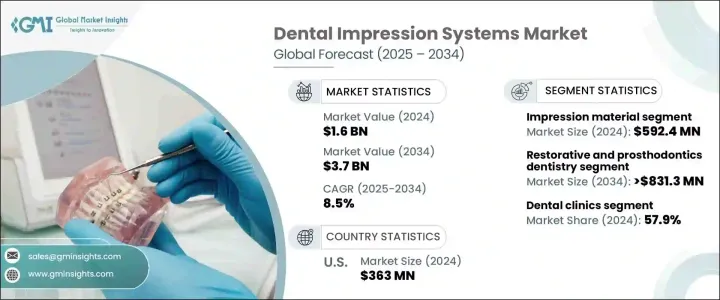

2024 年全球牙科印模系统市场规模达到 16 亿美元,预计 2025 年至 2034 年期间将以 8.5% 的强劲复合年增长率增长。随着人口老化和口腔健康意识的不断增强,越来越多的人寻求先进的牙科治疗,从而推动对可靠、精确的印模系统的需求。此外,牙科技术的发展彻底改变了传统的实践,提供了更好的治疗效果和患者满意度。

数位化牙科的创新进步,例如 3D 列印、CAD/CAM 系统和口内扫描仪,正在改变印模技术。这些技术显着提高了牙科印模的准确性、效率和患者的舒适度。透过减少错误、简化工作流程和提供精确的结果,数位印模系统正在成为现代牙科实践中不可或缺的工具。向数位化解决方案的转变不仅优化了临床结果,而且符合人们对微创手术和客製化牙科假体的日益增长的偏好,进一步推动了全球的采用率。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 16亿美元 |

| 预测值 | 37亿美元 |

| 复合年增长率 | 8.5% |

市场按产品类型分类,包括口内扫描器、印模材料、印模托盘、 CAD/CAM 系统和相关产品。仅印模材料一项,2024 年就创造了 5.924 亿美元的收入,反映了它们在为各种牙科手术提供高品质印模方面的重要作用。硅基、聚醚和水胶体材料可满足不同的处理需求,其中乙烯基聚硅氧烷 (VPS) 因其出色的尺寸稳定性和精度而脱颖而出。 VPS 材料广泛用于生产牙冠、牙桥和假牙等精密修復体,凸显了其需求日益增长。

在应用方面,修復和假牙牙科领域占据市场主导地位,预计复合年增长率为 9.4%,到 2034 年达到 8.313 亿美元。先进技术的不断应用在修復治疗中进一步推动了这一领域的扩张。

2024 年,美国牙科印模系统市场规模将达到 3.63 亿美元,到 2034 年的复合年增长率为 8.2%。微创治疗和客製化假牙的需求不断上升,推动了全国对精准、高效的牙科印模系统的需求。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 牙齿修復和假牙的需求不断增长

- 数位化牙科和口内扫描仪的采用率不断提高

- 牙齿疾病和牙齿脱落的盛行率不断上升

- CAD/CAM 系统的技术进步

- 产业陷阱与挑战

- 数位化牙科印模系统成本高

- 发展中地区数位系统采用有限

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按产品类型,2021 年至 2034 年

- 主要趋势

- 印模材料

- 聚乙烯硅氧烷 (PVS)

- 聚醚

- 硅酮

- 海藻酸盐

- 其他印模材料

- 口内扫描仪

- 印模托盘

- CAD/CAM 系统

- 其他产品类型

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 修復和口腔修復学

- 正畸

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 牙医诊所

- 医院

- 其他最终用户

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- 3shape

- AMANN GIRRBACH

- Carestream DENTAL

- Dentsply Sirona

- GC America

- HENRY SCHEIN

- ivoclar

- KULZER

- MEDIT

- PLANMECA

- solventum

- straumann

- VITA Zahnfabrik

- VOCO

- Zirkonzahn

The Global Dental Impression Systems Market reached USD 1.6 billion in 2024 and is anticipated to grow at a robust CAGR of 8.5% between 2025 and 2034. This growth is fueled by the increasing prevalence of dental diseases, such as tooth decay, periodontal diseases, and tooth loss, as well as the rising demand for dental restorations. With the aging population and the growing awareness of oral health, more individuals are seeking advanced dental treatments, driving demand for reliable and precise impression systems. Furthermore, the evolution of dental technologies has revolutionized traditional practices, offering improved outcomes and patient satisfaction.

Innovative advancements in digital dentistry, such as 3D printing, CAD/CAM systems, and intraoral scanners, are transforming impression-taking techniques. These technologies have significantly enhanced the accuracy, efficiency, and patient comfort of dental impressions. By reducing errors, streamlining workflows, and delivering precise results, digital impression systems are becoming indispensable tools in modern dental practices. The shift toward digital solutions not only optimizes clinical outcomes but also aligns with the increasing preference for minimally invasive procedures and customized dental prosthetics, further driving adoption rates worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.7 Billion |

| CAGR | 8.5% |

The market is categorized by product type, intraoral scanners, encompassing impression materials, impression trays, CAD/CAM systems, and related products. Impression materials alone generated USD 592.4 million in 2024, reflecting their essential role in delivering high-quality impressions for various dental procedures. Silicone-based, polyether, and hydrocolloid materials cater to diverse treatment needs, with vinyl polysiloxane (VPS) standing out for its exceptional dimensional stability and precision. VPS materials are widely favored for producing accurate restorations such as crowns, bridges, and dentures, underscoring their growing demand.

In terms of application, the restorative and prosthodontic dentistry segment dominates the market and is projected to grow at a CAGR of 9.4%, reaching USD 831.3 million by 2034. This segment's growth is attributed to the rising demand for crowns, bridges, dentures, and implants, which require precise dental impressions for optimal fit and functionality. The increasing adoption of advanced technologies for restorative treatments further propels this segment's expansion.

The U.S. dental impression systems market reached USD 363 million in 2024, growing at a CAGR of 8.2% through 2034. The adoption of digital impression technologies, including CAD/CAM systems and intraoral scanners, is driving growth as dental practices embrace these tools to improve workflow efficiency and accuracy. The demand for minimally invasive treatments and tailored prosthetics continues to rise, bolstering the need for precise and efficient dental impression systems across the country.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for dental restorations and prosthetics

- 3.2.1.2 Increasing adoption of digital dentistry and intraoral scanners

- 3.2.1.3 Rising prevalence of dental disorders and tooth loss

- 3.2.1.4 Technological advancements in CAD/CAM systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of digital dental impression systems

- 3.2.2.2 Limited adoption of digital systems in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Impression materials

- 5.2.1 Polyvinyl Siloxane (PVS)

- 5.2.2 Polyether

- 5.2.3 Silicone

- 5.2.4 Alginate

- 5.2.5 Other impression materials

- 5.3 Intraoral scanners

- 5.4 Impression trays

- 5.5 CAD/CAM systems

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Restorative and prosthodontics dentistry

- 6.3 Orthodontics

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Dental clinics

- 7.3 Hospitals

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3shape

- 9.2 AMANN GIRRBACH

- 9.3 Carestream DENTAL

- 9.4 Dentsply Sirona

- 9.5 GC America

- 9.6 HENRY SCHEIN

- 9.7 ivoclar

- 9.8 KULZER

- 9.9 MEDIT

- 9.10 PLANMECA

- 9.11 solventum

- 9.12 straumann

- 9.13 VITA Zahnfabrik

- 9.14 VOCO

- 9.15 Zirkonzahn

全球牙科印模材料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球牙科印模材料市场规模、份额、趋势和成长分析报告(2026-2034年) 位元组註册材料市场:按材料类型、分销管道、应用和最终用户划分 - 2026-2032 年全球预测

位元组註册材料市场:按材料类型、分销管道、应用和最终用户划分 - 2026-2032 年全球预测 牙科印模材料系统市场规模、份额及成长分析(按产品、应用、最终用户和地区划分)—产业预测(2026-2033 年)

牙科印模材料系统市场规模、份额及成长分析(按产品、应用、最终用户和地区划分)—产业预测(2026-2033 年) 牙科印模材料市场-全球产业规模、份额、趋势、机会和预测,依材料类型、应用、最终用途、地区和竞争格局划分,2020-2030年预测

牙科印模材料市场-全球产业规模、份额、趋势、机会和预测,依材料类型、应用、最终用途、地区和竞争格局划分,2020-2030年预测 牙科印模系统市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测(2025-2033 年)

牙科印模系统市场规模、份额和趋势分析报告:按产品、应用、最终用途、地区和细分市场预测(2025-2033 年) 2025年全球牙科印模材料市场报告2025年全球牙科印模系统市场报告

2025年全球牙科印模材料市场报告2025年全球牙科印模系统市场报告 全球牙科印模材料市场全球牙科印模系统市场聚乙烯硅氧烷印模材料市场按产品类型、固化时间、销售管道、最终用户应用划分 - 2025 年至 2030 年的全球预测

全球牙科印模材料市场全球牙科印模系统市场聚乙烯硅氧烷印模材料市场按产品类型、固化时间、销售管道、最终用户应用划分 - 2025 年至 2030 年的全球预测