|

市场调查报告书

商品编码

1684544

脉衝冲洗市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Pulse Lavage Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

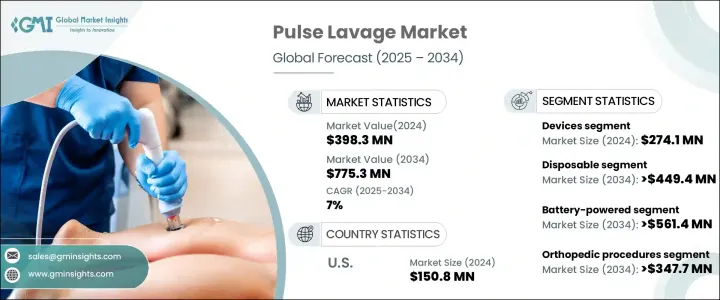

2024 年全球脉衝冲洗市场价值为 3.983 亿美元,预计将实现稳定成长,预计 2025 年至 2034 年的复合年增长率为 7%。脉衝冲洗装置是清洁、冲洗和清创伤口不可或缺的设备,在临床环境中发挥至关重要的作用。这些设备有助于预防感染、促进癒合并改善患者预后,特别是在骨科手术和一般伤口护理。

随着对有效、高效伤口管理的需求不断增长,脉衝冲洗市场在全球医疗保健环境中的应用越来越广泛。全球市场也受惠于微创手术日益增长的趋势,这种手术需要先进的便携式伤口护理技术。这些因素,加上医疗保健基础设施的改善和医疗设备的创新,使得脉衝冲洗市场成为医疗保健领域的重要参与者。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.983亿美元 |

| 预测值 | 7.753亿美元 |

| 复合年增长率 | 7% |

市场分为两个主要部分:设备和配件。 2024 年,设备部门创造了 2.741 亿美元的收入,占了大部分市场。脉衝冲洗设备包括手持装置、储液器和其他基本工具,已成为现代医疗保健中清洁伤口和控制感染不可或缺的设备。这些设备使用受控的加压液体有效地清洁伤口,有助于更快地恢復并最大限度地减少併发症。它们在骨科手术、感染管理和一般伤口护理中的应用使得它们在任何临床环境中都至关重要。随着医疗专业人员寻求更有效率、更便携的解决方案,对脉衝冲洗设备的需求持续成长。

按模式对脉衝冲洗市场进行进一步细分,显示出对电池供电设备的明显偏好。预计该领域将经历显着增长,预计复合年增长率为 7.2%,到 2034 年将达到 5.614 亿美元。其紧凑轻巧的设计增强了可用性,使其成为各种环境下医疗保健提供者的首选。向微创手术的转变以及对移动、易于使用的设备的需求将继续推动电池供电脉衝冲洗市场的成长。

在美国,脉衝冲洗市场在 2024 年的价值为 1.508 亿美元,预计未来十年的复合年增长率为 6.3%。由于对包括关节置换在内的骨科手术的需求不断增长,美国在全球市场占有相当大的份额。该国的医疗保健基础设施包括一些世界上最大的医疗设施,继续采用脉衝冲洗设备进行伤口护理和感染控制。政府对医疗保健的投资以及微创手术的日益增长的趋势进一步促进了美国市场的强劲增长

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 骨科疾病盛行率上升

- 伤口护理管理的进展

- 增加外科手术

- 政府改善医疗保健的倡议

- 产业陷阱与挑战

- 设备故障和可靠性问题

- 可用性和培训方面的挑战

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按产品类型,2021 - 2034 年

- 主要趋势

- 装置

- 配件

第六章:市场估计与预测:按可用性,2021 - 2034 年

- 主要趋势

- 一次性的

- 可重复使用的

第 7 章:市场估计与预测:按模式,2021 - 2034 年

- 主要趋势

- 电池供电

- 交流供电

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 整形外科手术

- 伤口护理

- 感染控制

- 其他应用

第 9 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 医院和诊所

- 门诊手术中心

- 其他最终用户

第 10 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- APEX

- Arthrex

- CLEAN

- ConMed

- deSoutter MEDICAL

- Fairmont MEDICAL

- Heraeus

- Judd

- Kaiser

- MicroAire Surgical Instruments

- Molnlycke

- NARANG MEDICAL LIMITED

- Smith & Nephew

- Stryker

- Zimmer Biomet

The Global Pulse Lavage Market, valued at USD 398.3 million in 2024, is poised for steady growth, with a projected CAGR of 7% from 2025 to 2034. This expansion is primarily driven by the increasing prevalence of orthopedic disorders and continuous advancements in wound care technologies. Pulse lavage devices, which are integral in cleaning, irrigating, and debriding wounds, play a critical role in clinical settings. These devices help prevent infections, promote healing, and improve patient outcomes, particularly in orthopedic surgeries and general wound care.

As the demand for effective, efficient wound management rises, the pulse lavage market is seeing greater adoption in healthcare environments worldwide. The global market is also benefiting from a growing trend towards minimally invasive surgeries, which require advanced, portable technologies for wound care. These factors, combined with improved healthcare infrastructure and innovation in medical devices, make the pulse lavage market a key player in the healthcare sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $398.3 Million |

| Forecast Value | $775.3 Million |

| CAGR | 7% |

The market is divided into two primary segments: devices and accessories. In 2024, the devices segment generated USD 274.1 million, accounting for the majority of the market share. Pulse lavage devices, which include hand-held units, fluid reservoirs, and other essential tools, have become indispensable in modern healthcare for cleaning wounds and managing infections. These devices use controlled, pressurized fluid to cleanse wounds effectively, aiding in faster recovery and minimizing complications. Their use in orthopedic procedures, infection management, and general wound care makes them vital in any clinical environment. As medical professionals seek more efficient and portable solutions, the demand for pulse lavage devices continues to grow.

Further segmentation of the pulse lavage market by mode shows a clear preference for battery-powered devices. This segment is expected to experience significant growth, with a projected CAGR of 7.2%, reaching USD 561.4 million by 2034. Battery-powered units are becoming increasingly popular due to their portability and convenience, offering healthcare providers a flexible solution for wound care, especially in settings like outpatient clinics or emergency care. Their compact and lightweight design enhances usability, making them the preferred choice for healthcare providers in various environments. The shift towards minimally invasive procedures and the need for mobile, easy-to-use devices will continue to drive growth in the battery-powered pulse lavage market.

In the United States, the pulse lavage market was valued at USD 150.8 million in 2024 and is expected to grow at a CAGR of 6.3% over the next decade. The U.S. holds a significant share of the global market, driven by the increasing demand for orthopedic surgeries, including joint replacements. The country's healthcare infrastructure, with some of the largest healthcare facilities worldwide, continues to adopt pulse lavage devices for wound care and infection control. Government investments in healthcare and the growing trend towards minimally invasive surgeries further contribute to the strong market growth in the U.S.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of orthopedic disorders

- 3.2.1.2 Advancements in wound care management

- 3.2.1.3 Increasing surgical procedures

- 3.2.1.4 Government initiatives for healthcare improvement

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Device malfunctions and reliability issues

- 3.2.2.2 Challenges in usability and training

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Devices

- 5.3 Accessories

Chapter 6 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Disposable

- 6.3 Reusable

Chapter 7 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Battery-powered

- 7.3 AC powered

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Orthopedic procedures

- 8.3 Wound care

- 8.4 Infection control

- 8.5 Other applications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgical centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 APEX

- 11.2 Arthrex

- 11.3 CLEAN

- 11.4 ConMed

- 11.5 deSoutter MEDICAL

- 11.6 Fairmont MEDICAL

- 11.7 Heraeus

- 11.8 Judd

- 11.9 Kaiser

- 11.10 MicroAire Surgical Instruments

- 11.11 Molnlycke

- 11.12 NARANG MEDICAL LIMITED

- 11.13 Smith & Nephew

- 11.14 Stryker

- 11.15 Zimmer Biomet