|

市场调查报告书

商品编码

1684560

马来酸氯苯那敏市场机会、成长动力、产业趋势分析与预测 2025 - 2034Chlorpheniramine Maleate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

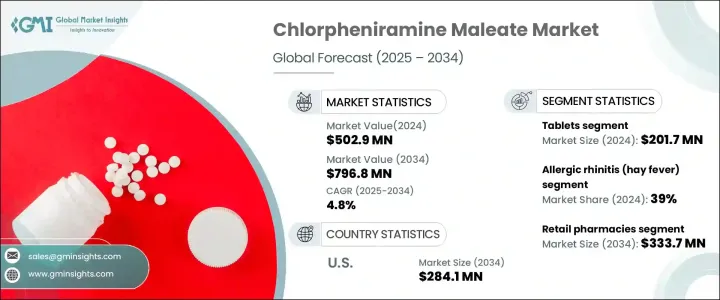

2024 年全球马来酸氯苯那敏市场价值为 5.029 亿美元,预计将实现稳步增长,预计 2025 年至 2034 年的复合年增长率为 4.8%。随着医疗保健系统的改善和抗过敏药物的普及,马来酸氯苯那敏的受欢迎程度持续上升。此外,抗组织胺配方的持续创新使治疗更加有效、更容易取得,扩大了马来酸氯苯那敏在治疗季节性和常年过敏症方面的使用范围。自我药疗的趋势日益增长,特别是在过敏性鼻炎和花粉症发病率高的市场,也刺激了对这种药物的需求。便利性、经济性和患者意识的提高进一步促进了其市场的扩张。

市场依剂型类型细分,注射剂、锭剂、糖浆和其他形式分别满足不同的消费者偏好。 2024 年平板电脑将占据市场主导地位,市场规模达 2.017 亿美元。由于其易于使用、经济高效以及广泛普及的便利性,它们成为治疗花粉症等疾病的个人的首选。此外,平板电脑的供应链成本相对较低,这也巩固了其在市场上的主导地位。製药公司热衷于开发改进的片剂配方,例如缓释版本,以增强治疗效果并提高患者的依从性。这些进步预计将进一步加强平板电脑领域的市场份额。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 5.029 亿美元 |

| 预测值 | 7.968 亿美元 |

| 复合年增长率 | 4.8% |

在应用方面,马来酸氯苯那敏市场分为过敏、过敏性鼻炎(花粉症)、普通感冒等。过敏性鼻炎领域在 2024 年占据最大份额,占市场份额的 39%。这种普遍的呼吸系统疾病影响着各个年龄层的人,其发病率的不断上升是推动对马来酸氯苯那敏等有效治疗药物的需求的主要因素。随着对这种疾病的认识不断提高,患者和医疗保健专业人员都开始使用这种抗组织胺来缓解症状。随着全球范围内花粉症和相关过敏症的发病率不断上升,越来越多的人寻求治疗,预计该领域将继续占据主导地位。

具体来看美国市场,预计马来酸氯苯那敏市场的复合年增长率为 4.7%,到 2034 年将达到 2.841 亿美元。美国约有 1,920 万成年人患有花粉症,对马来酸氯苯那敏等抗组织胺的需求持续存在。美国市场受益于非处方药(OTC)的优惠法规,加上强大的製药基础设施,确保这些产品在全国范围内易于获得。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球过敏症盛行率不断上升

- 已开发市场和新兴市场对抗组织胺药物的需求不断增加

- 扩大药品和非处方药 (OTC) 领域

- 产业陷阱与挑战

- 有副作用较少的替代抗组织胺药

- 影响产品发布和分销的严格监管要求

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:依配方类型,2021-2034 年

- 主要趋势

- 注射

- 平板电脑

- 糖浆

- 其他配方类型

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 过敏

- 过敏性鼻炎(花粉症)

- 普通感冒

- 其他应用

第 7 章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Aden Healthcare

- Alkem Laboratories

- Bayer

- Centaur Pharmaceuticals

- Cipla

- Dr. Reddy's Laboratories

- GlaxoSmithKline

- Glenmark Pharmaceuticals

- Merck & Co.

- Montage Laboratories

- Novalab Healthcare

- Pfizer

- Sun Pharmaceutical

The Global Chlorpheniramine Maleate Market, valued at USD 502.9 million in 2024, is poised to experience steady growth, with a projected CAGR of 4.8% from 2025 to 2034. The increasing prevalence of respiratory issues, including allergies, is a significant driver of this growth, as more people seek effective antihistamine treatments. As healthcare systems improve and greater access to allergy medications becomes available, chlorpheniramine maleate's popularity continues to rise. Additionally, ongoing innovations in antihistamine formulations are making treatments more effective and accessible, expanding the use of chlorpheniramine maleate for both seasonal and perennial allergies. The growing trend of self-medication, especially in markets with a high incidence of allergic rhinitis and hay fever, is also fueling the demand for this medication. The combination of convenience, affordability, and increased patient awareness is further promoting its market expansion.

The market is segmented based on formulation type, with injections, tablets, syrup, and other forms each serving distinct consumer preferences. Tablets led the market in 2024, accounting for USD 201.7 million. Their ease of use, cost-effectiveness, and the convenience of being widely available make them the preferred choice for individuals dealing with conditions like hay fever. Moreover, the relatively low supply chain costs associated with tablets have contributed to their dominant market position. Pharmaceutical companies are keen on developing improved tablet formulations, such as extended-release versions, to enhance therapeutic outcomes and improve patient compliance. These advancements are expected to further strengthen the tablet segment's market share.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $502.9 Million |

| Forecast Value | $796.8 Million |

| CAGR | 4.8% |

In terms of application, the chlorpheniramine maleate market is segmented into allergic conditions, allergic rhinitis (hay fever), common colds, and others. The allergic rhinitis segment held the largest share in 2024, representing 39% of the market. This widespread respiratory condition affects individuals of all ages, and its increasing incidence is a primary factor driving the demand for effective treatments like chlorpheniramine maleate. With growing awareness of the condition, both patients and healthcare professionals are turning to this antihistamine for relief. The segment is expected to continue its dominance as more individuals seek treatment for hay fever and related allergies, which are on the rise globally.

Looking specifically at the U.S. market, the chlorpheniramine maleate segment is forecast to grow at a CAGR of 4.7%, reaching USD 284.1 million by 2034. This growth is being driven by the increasing prevalence of allergies, particularly hay fever, among adults. With approximately 19.2 million adults in the U.S. affected by hay fever, there is a significant and ongoing demand for antihistamine treatments like chlorpheniramine maleate. The U.S. market benefits from favorable regulations surrounding over-the-counter (OTC) medications, coupled with a strong pharmaceutical infrastructure that ensures the easy availability of these products across the nation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of allergic conditions worldwide

- 3.2.1.2 Increasing demand for antihistamine medications in both developed and emerging markets

- 3.2.1.3 Expansion of pharmaceutical and over-the-counter (OTC) drug sectors

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of alternative antihistamines with fewer side effects

- 3.2.2.2 Strict regulatory requirements affecting product launches and distribution

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Formulation Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Injections

- 5.3 Tablets

- 5.4 Syrup

- 5.5 Other formulation types

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Allergic

- 6.3 Allergic rhinitis (hay fever)

- 6.4 Common cold

- 6.5 Other applications

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 Online pharmacies

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Aden Healthcare

- 9.2 Alkem Laboratories

- 9.3 Bayer

- 9.4 Centaur Pharmaceuticals

- 9.5 Cipla

- 9.6 Dr. Reddy’s Laboratories

- 9.7 GlaxoSmithKline

- 9.8 Glenmark Pharmaceuticals

- 9.9 Merck & Co.

- 9.10 Montage Laboratories

- 9.11 Novalab Healthcare

- 9.12 Pfizer

- 9.13 Sun Pharmaceutical

抗组织胺喷雾剂市场按产品类型、剂型、通路和最终用户划分-2026-2032年全球预测按产品类型、给药途径、分销管道、最终用户、处方状态和剂型分類的减充血剂市场-2025-2032年全球预测过敏性鼻炎治疗市场按分销管道、患者年龄层、剂型、给药途径和药物类别划分—全球预测 2025-2032

抗组织胺喷雾剂市场按产品类型、剂型、通路和最终用户划分-2026-2032年全球预测按产品类型、给药途径、分销管道、最终用户、处方状态和剂型分類的减充血剂市场-2025-2032年全球预测过敏性鼻炎治疗市场按分销管道、患者年龄层、剂型、给药途径和药物类别划分—全球预测 2025-2032 充血消除剂的全球市场:产品类型·处方区分·类别·用途·年龄层·流通管道·各地区 (~2035年)

充血消除剂的全球市场:产品类型·处方区分·类别·用途·年龄层·流通管道·各地区 (~2035年) 全球马来酸氯苯那敏市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球过敏性鼻炎市场规模(依过敏原类型、治疗类型、通路、区域覆盖范围和预测)

全球马来酸氯苯那敏市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球过敏性鼻炎市场规模(依过敏原类型、治疗类型、通路、区域覆盖范围和预测) 鼻减充血剂市场:按产品类型、按鼻减充血剂类型、按作用机制、按应用、按分销管道、按地区

鼻减充血剂市场:按产品类型、按鼻减充血剂类型、按作用机制、按应用、按分销管道、按地区 过敏性鼻炎药物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球抗组织胺市场按药物类别、剂型、适应症、给药途径、类型、分销管道和地区划分过敏性鼻炎治疗市场:依治疗类型、给药途径、通路及地区划分

过敏性鼻炎药物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测全球抗组织胺市场按药物类别、剂型、适应症、给药途径、类型、分销管道和地区划分过敏性鼻炎治疗市场:依治疗类型、给药途径、通路及地区划分