|

市场调查报告书

商品编码

1684713

双人自行车市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Tandem Bike Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

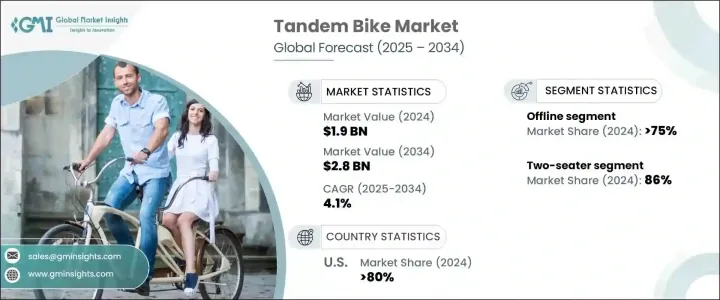

2024 年全球双人自行车市场价值为 19 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 4.1%。这些自行车为不同技术水平的骑乘者提供独特、愉快的体验,成为家庭、情侣和团体的热门选择。随着越来越多的人寻求在城市公园、风景小径和旅游目的地享受令人兴奋的户外体验,双人自行车的普及率持续上升。

此外,人们越来越注重健康生活方式和对休閒骑行的日益偏好也促进了市场扩张。越来越多的人选择骑自行车来增强体质,同时与亲人共度美好时光,因此双人自行车成为共享户外探险的有吸引力的选择。这一增长背后的另一个驱动力是环保型交通替代品的兴起。随着世界各地的城市加大对自行车基础设施和永续发展计画的投资,双人自行车正成为可行且环保的选择。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 19亿美元 |

| 预测值 | 28亿美元 |

| 复合年增长率 | 4.1% |

双人自行车市场按分销管道分类,到 2024 年,线下销售将占总市场份额的 75%。由于双人自行车需要仔细考虑适合度、重量和舒适度,因此买家通常选择在店内购买以确保选择正确的型号。购买前的试骑亲身体验,让消费者对产品品质更有信心,有利于线下销售的主导地位。虽然由于便利性和可近性,线上销售正在稳步增长,但实体店购物仍然是双人自行车买家的首选。

按骑乘者配置划分,双座双人自行车占据最大份额,到 2024 年将占据 86% 的市场份额。其轻巧的设计和用户友好的特性使其适合休閒骑行、通勤和休閒探险。製造商不断在这一领域进行创新,推出采用改良材料、增强悬吊和先进齿轮系统的双人自行车,以满足各种骑乘需求。对于轻型和高效双座车型的持续需求预计将使该类别车型继续占据市场领先地位。

2024 年,美国将主导全球双人自行车市场,占有 80% 的份额。该国拥有完善的自行车文化,有广泛的自行车道、风景路线和国家公园支撑,推动了这个令人印象深刻的市场份额。在美国,越来越多的人选择骑双人自行车来健身、休閒和进行环保交通。政府旨在扩大自行车基础设施和促进永续交通的措施进一步促进了市场成长。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 零件供应商

- 製造商

- 技术提供者

- 经销商

- 最终用户

- 供应商概况

- 利润率分析

- 定价分析

- 成本明细分析

- 技术与创新格局

- 专利分析

- 监管格局

- 衝击力

- 成长动力

- 娱乐和健身活动日益流行

- 对环保交通方式的需求不断成长

- 探险旅游和休閒旅游的成长

- 高度青睐家庭和团体骑行活动

- 产业陷阱与挑战

- 自行车道或小径有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:自行车市场估计与预测,2021 - 2034 年

- 主要趋势

- 路

- 山

- 折迭式的

- 电的

第 6 章:市场估计与预测:按乘客配置,2021 - 2034 年

- 主要趋势

- 双座

- 多座位

第 7 章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 在线的

- 离线

第 8 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 休閒骑手

- 职业自行车手

- 家庭/团体骑行

第 9 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Bike Friday

- Burley Design

- Calfee Design

- Cannondale

- Co-Motion Cycles

- da Vinci Designs

- Dawes Cycles

- Hase Bikes

- Hokitika

- KHS Bicycles

- Kinethic

- Koga

- Lapierre

- MTBT Tandems (Fandango)

- Órbita Bicycles

- Rivendell Bicycle Works

- Santana Cycles

- Schwinn Bicycle Company

- Thorn Bicycles

- Trek Bicycles

The Global Tandem Bike Market was valued at USD 1.9 billion in 2024 and is projected to grow at a CAGR of 4.1% between 2025 and 2034. The increasing enthusiasm for outdoor family activities and group adventures has significantly fueled the demand for tandem bikes. These bicycles offer a unique, enjoyable experience for riders of varying skill levels, making them a popular choice for families, couples, and groups. With more individuals seeking exciting outdoor experiences in urban parks, scenic trails, and tourist destinations, the adoption of tandem bikes continues to rise.

Additionally, the surge in health-conscious lifestyles and the growing preference for recreational cycling have contributed to market expansion. People are increasingly embracing cycling as a means to improve fitness while spending quality time with loved ones, making tandem bikes an appealing option for shared outdoor adventures. Another driving force behind this growth is the rise in eco-friendly transportation alternatives. As cities worldwide invest in cycling infrastructure and sustainability initiatives, tandem bikes are emerging as a viable, environmentally friendly option.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 4.1% |

The tandem bike market is categorized by distribution channels, with offline sales accounting for 75% of the total market share in 2024. Consumers overwhelmingly prefer purchasing tandem bikes from physical retail locations, such as local bike shops and specialty stores, where they can personally examine and test the bicycles before making a decision. Because tandem bikes require careful consideration of fit, weight, and comfort, buyers often opt for in-store purchases to ensure they select the right model. The hands-on experience of test riding before purchase provides confidence in the product's quality, contributing to the dominance of offline sales. While online sales are steadily increasing due to convenience and accessibility, in-person shopping remains the primary choice for tandem bike buyers.

By rider configuration, two-seater tandem bikes represent the largest segment, accounting for 86% of the market share in 2024. These models are widely favored for their ease of use, making them ideal for couples and families looking for a fun, interactive riding experience. Their lightweight design and user-friendly nature make them suitable for leisure rides, commuting, and casual adventures. Manufacturers are continuously innovating in this segment, introducing tandem bikes with improved materials, enhanced suspension, and advanced gear systems to cater to various riding needs. The ongoing demand for lightweight and efficient two-seater models is expected to keep this category at the forefront of the market.

In 2024, the United States dominated the global tandem bike market, holding an 80% share. The country's well-established cycling culture, supported by extensive bike paths, scenic routes, and national parks, has driven this impressive market share. More individuals in the U.S. are turning to tandem bikes for fitness, leisure, and eco-friendly transportation. Government initiatives aimed at expanding cycling infrastructure and promoting sustainable transportation have further contributed to market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 Distributors

- 3.1.6 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Cost breakdown analysis

- 3.6 Technology & innovation landscape

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing popularity of recreational and fitness activities

- 3.9.1.2 Rising demand for eco-friendly transportation options

- 3.9.1.3 Growth in adventure tourism and leisure travel

- 3.9.1.4 High preference for family and group cycling activities

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Limited availability of cycling tracks or trails

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Bike, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Road

- 5.3 Mountain

- 5.4 Folding

- 5.5 Electric

Chapter 6 Market Estimates & Forecast, By Rider Configuration, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Two-seater

- 6.3 Multi-seater

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Recreational riders

- 8.3 Professional cyclists

- 8.4 Family/group riders

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Bike Friday

- 10.2 Burley Design

- 10.3 Calfee Design

- 10.4 Cannondale

- 10.5 Co-Motion Cycles

- 10.6 da Vinci Designs

- 10.7 Dawes Cycles

- 10.8 Hase Bikes

- 10.9 Hokitika

- 10.10 KHS Bicycles

- 10.11 Kinethic

- 10.12 Koga

- 10.13 Lapierre

- 10.14 MTBT Tandems (Fandango)

- 10.15 Órbita Bicycles

- 10.16 Rivendell Bicycle Works

- 10.17 Santana Cycles

- 10.18 Schwinn Bicycle Company

- 10.19 Thorn Bicycles

- 10.20 Trek Bicycles

液压模组化阀市场:按阀类型、驱动方式、压力范围、流量范围和最终用户划分,全球预测,2026-2032年

液压模组化阀市场:按阀类型、驱动方式、压力范围、流量范围和最终用户划分,全球预测,2026-2032年 2026年全球多串联阀市场报告2026年全球液压阀市场报告微流体控装置市场按产品类型、技术、应用和最终用户划分,全球预测(2026-2032年)

2026年全球多串联阀市场报告2026年全球液压阀市场报告微流体控装置市场按产品类型、技术、应用和最终用户划分,全球预测(2026-2032年) 全球液压阀市场-2025-2030年预测

全球液压阀市场-2025-2030年预测 液压阀远端控制系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

液压阀远端控制系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 多联阀:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

多联阀:全球市场份额和排名、总销售额和需求预测(2025-2031 年) 液压法兰配件市场报告:2031 年趋势、预测与竞争分析

液压法兰配件市场报告:2031 年趋势、预测与竞争分析 2024-2028年全球液压阀市场

2024-2028年全球液压阀市场